Selling a business is one of the biggest financial decisions you’ll make. Getting your small business valuation right determines whether you walk away with fair value or leave money on the table.

At Unbroker, we’ve seen owners price their businesses too high, too low, or based on gut feeling instead of data. This guide walks you through the methods that actually work, the mistakes to avoid, and how to prepare your business for the strongest possible valuation.

How to Calculate What Your Business Is Worth

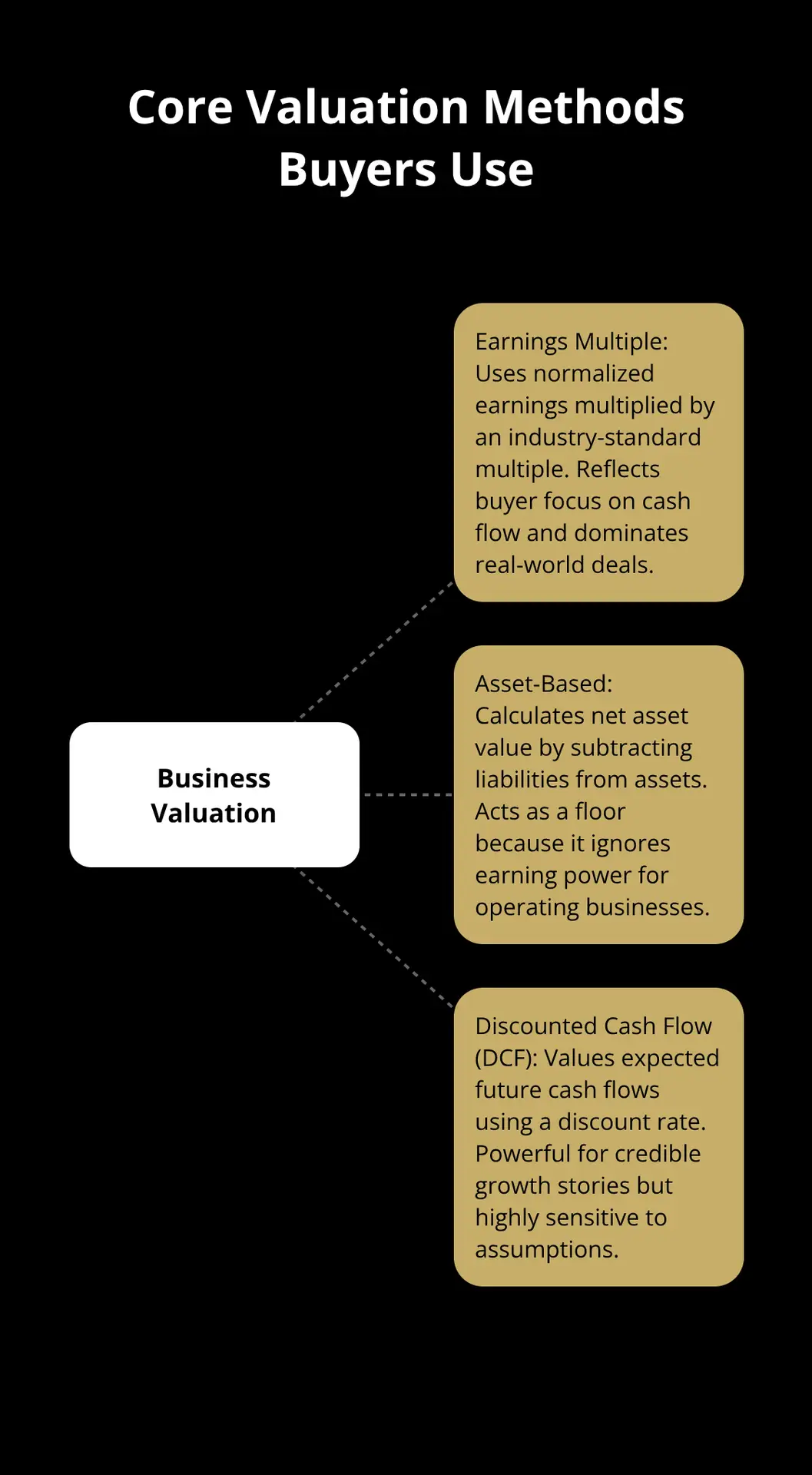

The earnings multiple method dominates real-world business sales. Most buyers of small to mid-sized companies rely on this approach because it reflects what they actually care about: cash flow. Take your normalized earnings-the profit your business generates after removing one-time expenses and owner perks-and multiply it by an industry-standard multiple. A service business might trade at 3 to 5 times earnings, while a software company could reach 8 to 12 times, depending on growth and stability. The math is straightforward: if your business generates $200,000 in normalized annual earnings and your industry trades at a 4x multiple, you’re looking at an $800,000 valuation. This method works because it’s what buyers understand and what they’ll offer.

Don’t expect a single precise number; realistic valuations present a range instead. Your business might be worth $750,000 to $900,000 rather than exactly $825,000. The type of buyer also shifts the multiple significantly. An insider purchasing the business might value it at 3x earnings, a private equity buyer around 4 to 5x, and a strategic competitor potentially higher if they see synergies.

This is why modeling multiple buyer scenarios matters more than chasing one “correct” number.

The Asset-Based Reality Check

Asset-based valuation focuses on calculating net asset value by subtracting liabilities from assets. Add up equipment, inventory, real estate, and accounts receivable, then subtract liabilities. This method rarely produces the highest valuation for operating businesses because it ignores earning power. A consulting firm with strong cash flow but minimal physical assets would appear worthless on an asset sheet, yet it generates real value.

Asset-based valuation works best as a floor price-it tells you the absolute minimum your business is worth if sold for parts. Use it to sanity-check your earnings-based valuation. If your earnings-based value is $500,000 but your net assets total $750,000, something deserves scrutiny. Either your earnings are understated, or you’re carrying underperforming assets. For most small business owners, this method is secondary, but it prevents you from accepting offers below what the physical business itself is worth.

Cash Flow Projections and Growth Assumptions

Discounted cash flow analysis estimates the value of an investment based on its expected future cash flows. This approach appeals to buyers betting on growth. If your business has grown 20 percent annually and shows no signs of slowing, DCF can justify a higher valuation than simple earnings multiples. However, this method requires credible projections, not wishful thinking.

Buyers scrutinize growth assumptions heavily. Claiming 30 percent annual growth when your industry averages 8 percent will kill your credibility. The discount rate you apply also shapes the result dramatically-a 10 percent discount rate versus 20 percent can swing your valuation by 50 percent or more. Unless your business shows consistent, documented growth trends backed by market data, stick with earnings multiples.

They’re more defensible and align with how most buyers actually price acquisitions.

The mistakes you make during valuation often stem from how you present these numbers to potential buyers. Understanding what drives buyer decisions helps you avoid the pitfalls that tank deals before they start.

Where Owners Go Wrong With Valuations

Most business owners overestimate what their company will sell for. The gap between expectation and reality stems from three specific mistakes that appear repeatedly during the valuation process.

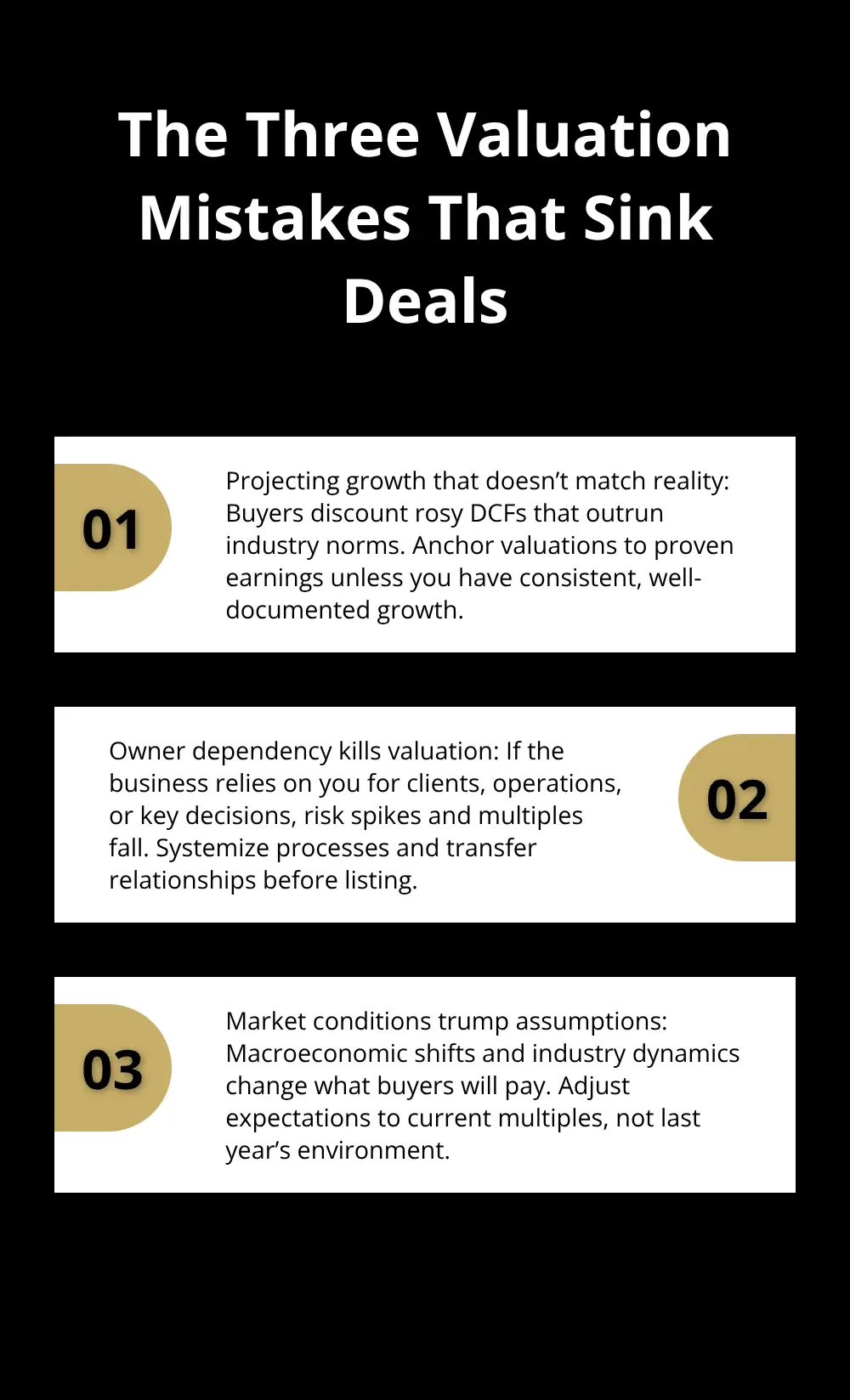

Projecting Growth That Doesn’t Match Reality

Owners frequently anchor on their best year or assume the next three years will mirror their strongest performance, then build valuations around those inflated numbers. A software company that grew 25 percent in a single year because of one major contract win might assume 25 percent growth going forward. Buyers won’t pay based on that assumption. Real-world buyers apply heavy skepticism to growth projections, especially when they diverge sharply from industry averages. If your industry grows at 8 percent annually and you claim 20 percent, expect buyers to discount your valuation significantly or walk away entirely.

The earnings multiple method works precisely because it sidesteps this problem-it values what you’ve actually earned, not what you hope to earn. When you use discounted cash flow analysis with aggressive assumptions, you essentially bet that buyers will share your optimism. They rarely do. Stick with what the numbers show, not what you project.

Owner Dependency Kills Valuation

The second critical error is ignoring how your business depends on you personally. If clients work with you directly, if you’re the only person who understands the operations, or if key relationships disappear when you leave, your valuation takes a major hit. Buyers pay less for businesses they perceive as risky, and owner dependency represents a massive risk flag.

A business where you personally manage all client relationships might sell at a lower multiple because the buyer faces significant uncertainty after the sale. This isn’t theoretical-it’s how real transactions price. You combat this by documenting processes, delegating client relationships to team members before listing, and proving the business runs without you. The stronger your systems and the less dependent the business is on your presence, the higher the multiple buyers will accept.

Market Conditions Trump Your Assumptions

The third mistake compounds the first two: ignoring what’s actually happening in your market and industry. Economic downturns, supply chain disruptions, shifting customer preferences, and rising competition all affect what buyers will pay. A retail business owner who valued their company at a 4.5x multiple in 2022 might find the market only supports 3x in 2026 due to e-commerce pressure and changing consumer behavior.

You can’t control market conditions, but you can acknowledge them. Industry consolidation alters valuations through predictable cycles that reward prepared sellers and punish those who wait too long. Understanding these external forces helps you set realistic expectations and positions you to negotiate from a grounded perspective rather than wishful thinking.

These three mistakes shape how buyers perceive risk and value. Addressing them directly-before you list-transforms your negotiating position and opens the door to stronger offers.

How to Build a Business Buyers Actually Want to Pay For

The valuation mistakes we covered earlier stem partly from misunderstanding what buyers evaluate during due diligence. Fixing these problems before listing transforms your negotiating position. Three specific areas determine whether a buyer accepts your valuation or walks away: the quality of your financial records, the independence of your operations from you personally, and the trajectory of your profitability and cash flow.

Financial records that buyers trust without hesitation

Buyers spend weeks questioning your numbers. They request financial documents from the seller. If these documents tell conflicting stories or contain obvious gaps, they assume you hide something and discount your valuation accordingly. The fix is straightforward: prepare normalized financial statements that isolate your discretionary spending and one-time expenses. If you paid $50,000 for a company vehicle you personally use, add that back. If you expensed a one-time lawsuit settlement, remove it from operating costs. These add-backs show your true earnings power, and they represent standard practice among serious buyers.

A CPA should prepare these recasts formally rather than you handling it yourself. A professional recast costs between $2,000 and $5,000 but prevents the credibility damage that comes from buyer skepticism. Keep detailed records of every add-back with supporting documentation. Buyers want proof, not promises. The cleaner your financials appear and the more thoroughly you document what’s normal versus exceptional, the less room exists for negotiation pushback based on accounting questions.

Operations that function without your presence

Your business generates value only if it survives your departure. If you personally manage all client relationships, handle every sales call, or make every operational decision, you’ve created a job for yourself, not a saleable asset. Start removing yourself from daily operations at least six months before listing. Delegate client relationships to team members and have those team members take the first meetings and handle ongoing communication.

Document every process in writing, from how you onboard clients to how you handle complaints to how you manage inventory or projects. This documentation serves two purposes: it proves the business runs without you, and it gives the buyer a roadmap for day-one operations. Buyers pay significantly higher multiples for businesses that operate independently. A business worth 3.5x earnings when owner-dependent might command 5x earnings once systems are in place and client relationships transfer to your team. That difference matters substantially on a $500,000 business. The investment in building these systems costs time but pays dividends immediately upon sale.

Cash flow improvement in the months before listing

Most owners miss the window where they can meaningfully improve cash flow before sale. Start 12 months ahead of your target listing date. Review customer concentration: if one client represents more than 20 percent of revenue, start diversifying immediately. Buyers heavily discount businesses dependent on a handful of customers because losing even one creates catastrophic revenue loss.

Reduce unnecessary expenses without compromising operations. Cut subscriptions you don’t use, negotiate supplier contracts, and eliminate low-margin work that consumes resources without generating profit. A 10 percent improvement in profit margins translates directly to higher valuation. If your business generates $300,000 in earnings at a 30 percent margin, improving to a 33 percent margin adds $9,000 in annual earnings, which at a 4x multiple equals $36,000 in additional valuation. That represents a meaningful return on the effort invested in operational tightening. Collect outstanding receivables aggressively and reduce inventory sitting unused. These actions improve your cash position and demonstrate financial discipline to buyers.

Final Thoughts

Your small business valuation determines whether you walk away with fair compensation or leave substantial money on the table. The methods we’ve covered-earnings multiples, asset-based approaches, and cash flow analysis-give you the framework to understand what buyers will actually pay. Start now by cleaning up your financial records, moving client relationships to your team, and tightening operations to improve cash flow before listing.

These actions compound into real value. A business with clean financials, independent operations, and improving margins commands higher multiples and attracts more qualified buyers. The difference between a business valued at 3.5x earnings and one valued at 5x earnings is substantial on any sale price, and that gap comes from the preparation work you do today, not from hoping buyers will overlook weaknesses.

When you’re ready to list, Unbroker offers a modern platform for selling businesses with transparent pricing and no hidden fees. The platform handles confidentiality, legal documents, and negotiation assistance so you can focus on running your business through the sale while accessing a vast buyer network and premium marketing tools without traditional brokerage commissions.