Selling your business is one of the biggest financial decisions you’ll make. Before you list, there are critical exit topics for owners that need your attention-from understanding what your business is actually worth to organizing the paperwork buyers will demand.

At Unbroker, we’ve seen owners stumble because they didn’t prepare these conversations beforehand. This guide walks you through the three areas that matter most.

Understanding Your Business Valuation

Your business value isn’t what you think it is. Most owners overestimate by 20 to 40 percent because they conflate revenue with profit and ignore what buyers actually care about. The market doesn’t pay for sales; it pays for earnings that will continue after you leave. This is why understanding your business valuation before you list matters more than almost anything else you’ll do in the exit process.

The Math Behind Business Value

Small businesses typically sell for multiples of EBITDA, which strips out owner compensation, one-time expenses, and financing costs to show true operating profit. A business earning $500,000 in normalized EBITDA might sell for $2 to $3.5 million, depending on growth rate, customer concentration, and market conditions. The DealStats Value Index reported that median multiples for private companies ranged from 4.5 to 6.5 times EBITDA in early 2025, though this varies sharply by industry.

You must normalize your financials first. Normalized EBITDA and financial adjustments remove owner pay and one-time costs to reveal true earnings power. If your financials are a mess, a fractional CFO or outsourced accounting firm can clean them up in three to six months. The cost-typically $3,000 to $8,000-pays for itself immediately when buyers see credible numbers instead of tax returns designed to minimize your tax bill.

Why Valuation Method Matters More Than You Think

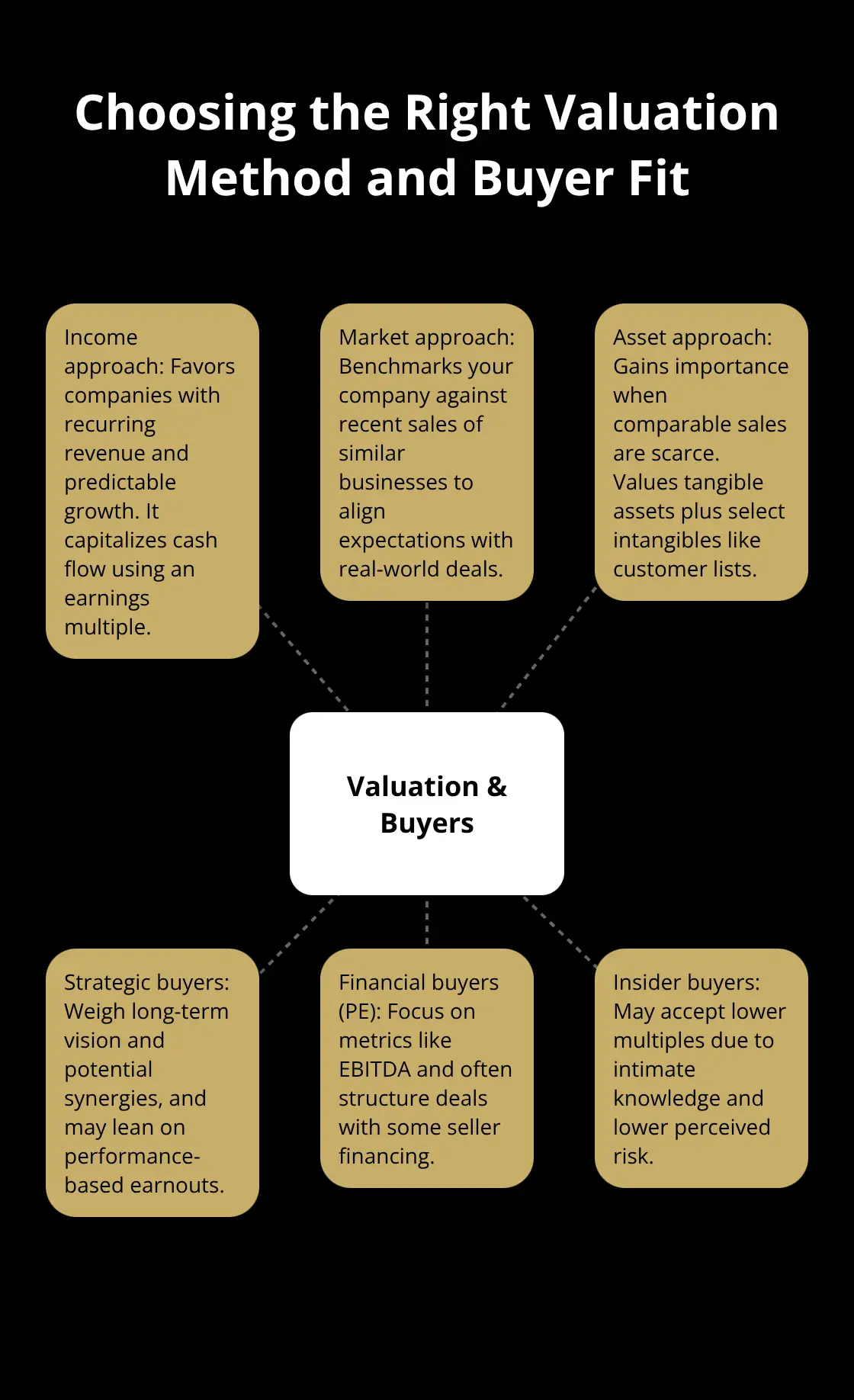

Different valuation approaches produce wildly different numbers, and buyers know this. The income approach uses your cash flow and applies a multiple; the market approach compares your business to recent sales of similar companies; the asset approach values your tangible assets plus intangibles like customer lists. Each method tells a different story.

If your business has strong recurring revenue and predictable growth, the income approach favors you. If comparable sales in your market are scarce, the asset approach becomes more important. Strategic buyers versus private equity buyers have different priorities-strategic buyers consider long-term vision and potential synergies, while financial buyers focus on metrics like EBITDA. Insider buyers may accept lower multiples because they understand the business intimately.

A professional valuation expert who knows your industry will test all three methods and explain which one applies to your situation. This costs $3,000 to $10,000 depending on complexity, but it anchors your asking price and prevents the months of negotiation that follow from being based on inflated numbers. Without it, you’ll either scare away serious buyers or leave money on the table.

Getting Professional Help Before You List

The valuation expert becomes your foundation for everything that follows. They produce a detailed report that explains your business’s strengths, identifies risk factors, and justifies your asking price to potential buyers. This document carries weight during negotiations because it comes from an independent third party, not from you. When you move forward with marketing your business, you’ll reference this valuation constantly-it shapes your listing price, informs your response to offers, and provides credibility when buyers question your numbers.

The next step involves organizing the financial and legal documentation that buyers will request during due diligence.

Preparing Your Financial and Legal Documentation

Buyers don’t ask for documents to be difficult. They ask because they need to verify that your business is what you claim it is, that no hidden liabilities lurk in contracts or tax filings, and that the revenue and profit numbers you’ve presented will actually continue after the sale closes. The documents you organize now determine how quickly due diligence moves and whether skeptical buyers gain confidence or lose it. Most owners underestimate how much paper this requires.

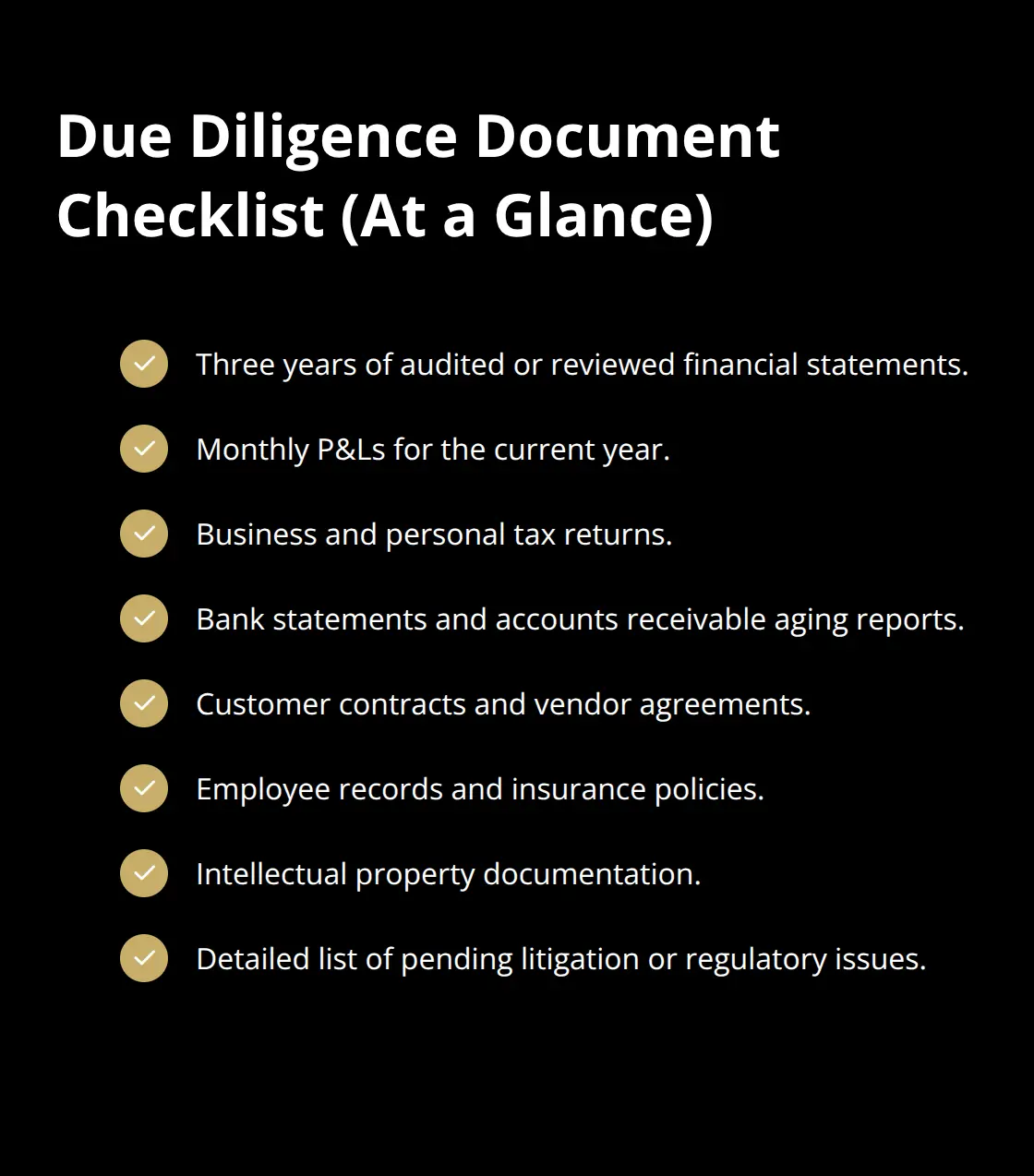

Expect to produce three years of audited or reviewed financial statements, monthly P&Ls for the current year, tax returns for both the business and yourself personally, bank statements, accounts receivable aging reports, customer contracts, vendor agreements, employee records, insurance policies, intellectual property documentation, and a detailed list of any pending litigation or regulatory issues. If your financial records have been inconsistent or your records scattered, this phase alone takes two to four months to complete properly.

One fractional CFO worked with a $3 million revenue manufacturing company that had kept financial records across three different accounting systems over five years. Organizing this into a coherent narrative cost $6,000 and took eight weeks, but it prevented the deal from collapsing during due diligence when the buyer discovered unexplained discrepancies. Buyers who encounter disorganized or incomplete records assume you’re hiding something, they demand deeper investigation, and they typically reduce their offer by 10 to 15 percent to account for unknown risks.

Normalizing Your Numbers So Buyers See Reality

Your tax return was designed to minimize what you owe the IRS, not to show what your business actually earns. Owner compensation, vehicle expenses, travel that’s partly personal, insurance premiums, and one-time restructuring costs all depress reported profit. When you normalize your financials, you add back these items to show true operating earnings.

A business owner taking a $150,000 salary when the market rate is $100,000 needs to adjust that down. A business that spent $50,000 on a one-time software migration needs to add that back. These adjustments aren’t fictional; they’re standard practice that every serious buyer expects. Normalized EBITDA is the metric buyers actually use to calculate multiples. Without normalization, you’re presenting a financial picture that doesn’t match reality, and buyers know it.

Create a detailed schedule that lists every adjustment, explains why it makes sense, and provides supporting documentation. This transparency actually accelerates deals because buyers see you’re organized and honest, not evasive. If your business has multiple revenue streams or complex cost structures, hire a transaction accountant to prepare this schedule. The cost runs $2,000 to $5,000, and it becomes the foundation for all offer discussions.

Addressing the Liabilities Buyers Will Uncover Anyway

Every business has problems. Customer contracts that aren’t formally documented, an unpaid property tax bill from three years ago, a wage-and-hour complaint from a former employee, equipment financed through a loan that has a change-of-control clause, or intellectual property that a contractor created but never formally assigned to you-buyers will find these issues during due diligence. The question is whether you disclose them first or whether they discover them and assume you were hiding them.

Disclosure first dramatically improves your negotiating position. If you reveal that one major customer has a contract expiring in six months, the buyer can plan for it and price accordingly. If the buyer discovers this themselves after signing, they’ll claim you misrepresented the business and demand a price reduction or walk away entirely.

Start with a candid inventory of every potential problem: unpaid taxes, pending litigation, compliance violations, customer concentration risk, supplier dependencies, intellectual property gaps, environmental issues, and regulatory approvals needed for a change of control. Organize this into a disclosure schedule that your attorney reviews before you share it with buyers. This document protects you legally because it demonstrates good faith, and it prevents deal collapse when problems surface.

Resolve what you can before marketing the business. Pay off that unpaid tax bill, settle the wage claim if it’s legitimate, and get customer contracts formalized in writing. The cost of fixing these issues now is typically far less than the price reduction you’ll accept if buyers discover them during negotiations.

Moving Forward With Deal Structure

With your financial house in order and your liabilities disclosed, you’re ready to shape how the actual transaction will work.

Structuring Your Deal and Responding to Offers

The deal structure you choose determines not just how much you receive, but when you receive it, what tax consequences follow, and how much risk you carry after closing. Most owners fixate on price and ignore structure, which is a mistake. A $3 million all-cash offer at closing beats a $3.5 million offer split across three years of seller financing if you need liquidity or if the buyer defaults. The structure also signals what kind of buyer you’re dealing with.

Understanding Deal Structures and Buyer Types

Strategic buyers often propose earnouts tied to future performance, which means they’re betting on synergies they haven’t fully explained. Private equity buyers typically offer upfront cash but demand seller financing for 10 to 20 percent of the purchase price as a holdback. Insider buyers almost always need seller financing because they lack the capital for a full cash purchase. Each structure carries different negotiating leverage, tax implications, and post-sale risks that you need to understand before you see your first offer.

Determining What You Actually Need

Start by deciding what you actually need from the sale. If you’re retiring and need immediate capital, a mostly-cash deal at closing is non-negotiable, even if it means accepting a lower multiple. If you’re staying on as a consultant or have other income sources, you can afford to be flexible on timing. The typical middle-market deal in 2025 involved roughly 70 to 80 percent cash at closing, with the remainder split between an earnout and seller financing.

Earnouts are dangerous because they tie your payout to future performance you won’t control. If the buyer mismanages the business or the market shifts, you lose money you thought you’d earned. Earnouts should be capped at 10 to 15 percent of total consideration and have clear, auditable performance metrics tied to EBITDA or revenue targets, not vague operational goals.

Setting a Realistic Price Based on Market Data

Pricing realistically requires separating what you want from what the market will actually pay. Overpricing kills deals before they start; underpricing leaves millions on the table. The DealStats Value Index showed that small-business multiples ranged from 4.5 to 6.5 times EBITDA in early 2025, but this varies dramatically by industry and buyer type. A software company with high gross margins and sticky customers commands 6 to 8 times EBITDA. A manufacturing business with commodity products and thin margins sells for 3 to 4.5 times.

Your professional valuation report anchors your asking price, but you need to pressure-test it against recent comparable sales in your market. Ask your M&A advisor or business broker what similar companies actually sold for in the past 12 months, not what they listed for. Listing price and sale price diverge significantly. Most owners should expect to negotiate down 5 to 15 percent from their asking price, which is why you set your initial price 10 to 20 percent above your walk-away number.

Responding to Offers Strategically

When offers arrive, respond strategically. Multiple qualified offers give you leverage; a single offer puts you at the buyer’s mercy. If you receive only one serious bid, resist the urge to negotiate aggressively because you might kill the deal entirely. If you have two or three competing buyers, you can push harder on price and terms because you have alternatives.

Respond to every offer in writing through your attorney, not verbally. Verbal conversations create misunderstandings and give buyers room to claim they never agreed to something. Your attorney should propose counteroffers that address not just price but structure, earnout terms, seller financing duration, noncompete covenants, and post-sale support requirements. Negotiate all of these simultaneously, not sequentially, because they’re interconnected. A buyer willing to pay 5.5 times EBITDA might demand a 20 percent earnout and 15 percent seller financing. A buyer offering mostly cash might accept 4.8 times EBITDA. You need to see the full picture before you decide which offer actually benefits you most.

Final Thoughts

Selling your business requires preparation across three critical areas: understanding what it’s actually worth, organizing the financial and legal documentation buyers demand, and structuring a deal that serves your goals. The valuation work you do upfront determines everything that follows, while normalized financials and disclosed liabilities accelerate due diligence and build buyer confidence. Deal structure matters as much as price because it determines when you get paid, what taxes you owe, and how much risk you carry after closing.

Start these conversations now, even if you’re not selling for another year. The businesses that command premium multiples are the ones where owners have already normalized their financials, resolved liabilities, and assembled the right advisory team. You’ll negotiate from strength instead of scrambling to organize documents while buyers wait, and you’ll address the exit topics for owners that separate successful sales from mediocre ones.

We at Unbroker help owners navigate this entire process with transparent, low-cost options that eliminate the high brokerage fees traditional brokers charge. Unbroker offers tools, templates, and access to a vast buyer network designed to make selling straightforward and fair, whether you need full-service support or expert guidance as you handle the sale yourself.