Selling a business is one of the biggest financial decisions you’ll make. The steps to sell business successfully require careful planning, smart marketing, and solid negotiation skills.

At Unbroker, we’ve helped countless business owners navigate this complex process. This guide walks you through each stage, from preparing your business to closing the deal.

Getting Your Business Ready to Sell

Before you attract serious buyers, your business needs to be in top shape. Most owners underestimate how much work this takes. According to Inc. Magazine, the entire sales process typically runs six to eleven months after preparation, and much of that timeline depends on how well you’ve prepared upfront. The cleaner your financial records, the faster buyers move forward. Start by pulling together your last three years of tax returns, profit and loss statements, and balance sheets. Buyers will scrutinize these documents closely, so any inconsistencies or missing records will slow down negotiations or kill deals entirely. If your bookkeeping has been sloppy, hire an accountant now to clean it up. This investment pays for itself many times over because buyers trust verified numbers.

Organize Your Assets and Liabilities

List every asset your business owns-equipment, inventory, intellectual property, customer lists, and real estate. If you own the building like the supermarket owner in that Reddit post, that real estate becomes a major part of your valuation. Calculate what each asset is worth and what liabilities attach to them. Resolve any outstanding debts, unpaid taxes, or legal disputes before listing. Buyers will uncover these during due diligence anyway, and addressing them proactively prevents last-minute deal collapse. One practical step many owners skip: document your standard operating procedures. Write down how your business actually runs day-to-day. This shows buyers the company can operate smoothly without you constantly involved, which dramatically increases its value. A business that depends entirely on the owner’s presence is worth significantly less than one with documented systems and trained staff ready to transition.

Clean Up Your Compliance Records

Legal compliance matters far more than most sellers realize. Go through your business licenses, permits, registrations, and any industry-specific certifications. Make sure everything is current and properly filed with your state. If you’ve been operating without proper licenses or have unresolved compliance issues, fix them now. Buyers will request proof of compliance, and missing documentation creates red flags that tank offers. Review your contracts too-employment agreements, customer contracts, supplier agreements, and lease terms. Identify which ones transfer to the new owner and which ones terminate at sale. Some contracts have clauses that prevent transfer without the other party’s consent, so you need to know this upfront. If you have employees, review your employment records and payroll documentation. The Worker Adjustment and Retraining Notification Act requires you to give employees advance notice if you’re closing or selling, so understand those obligations early. Organize all of this in a digital data room that buyers can access during due diligence. The more organized and transparent you are, the faster the process moves and the higher confidence buyers have in their offer.

Understand What Drives Your Business Value

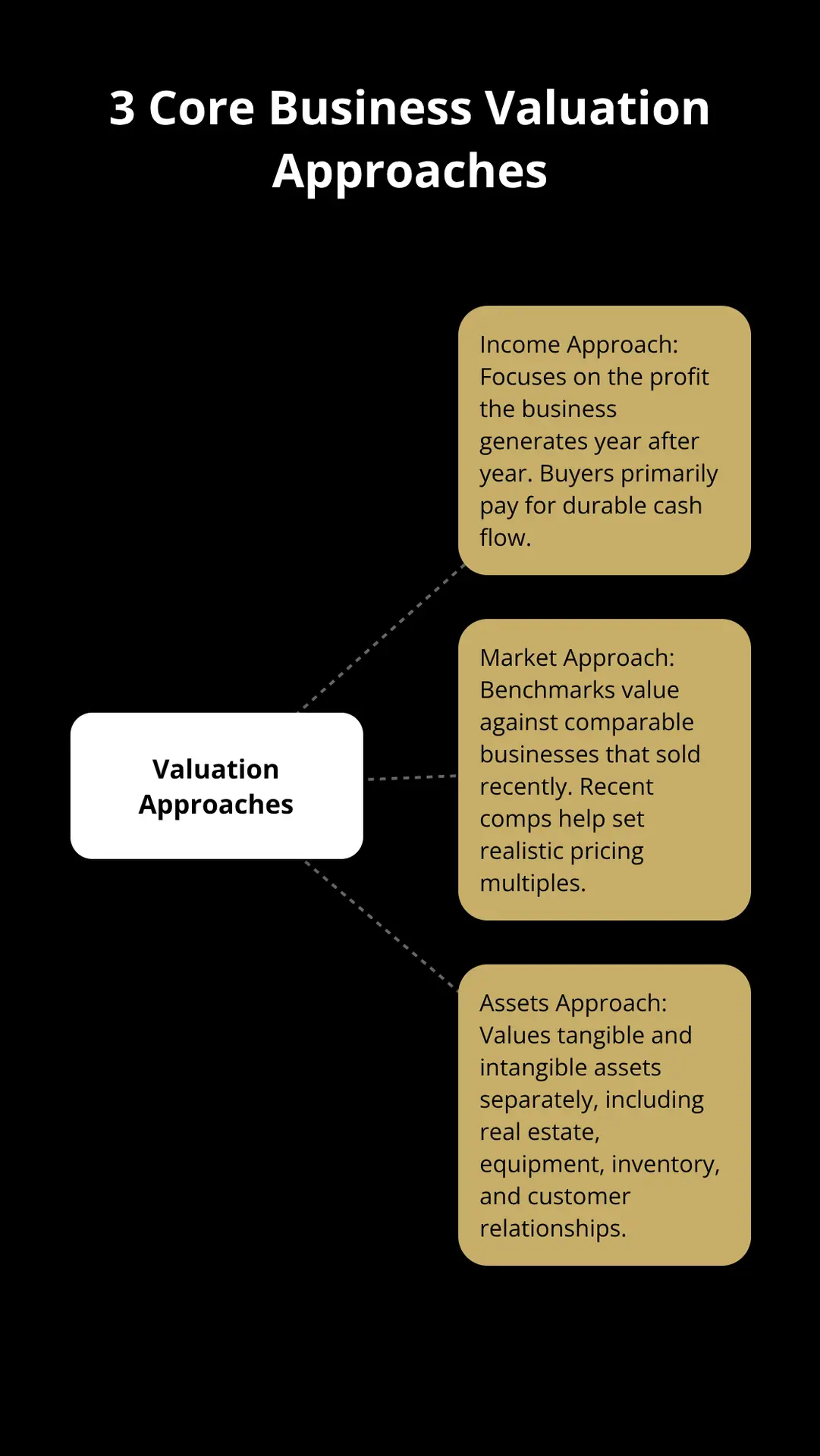

Business valuation isn’t just a multiple of gross revenue, despite what many owners assume. The SBA recognizes three main valuation approaches: the income approach, the market approach, and the assets approach. The income approach looks at what profit the business generates year after year.

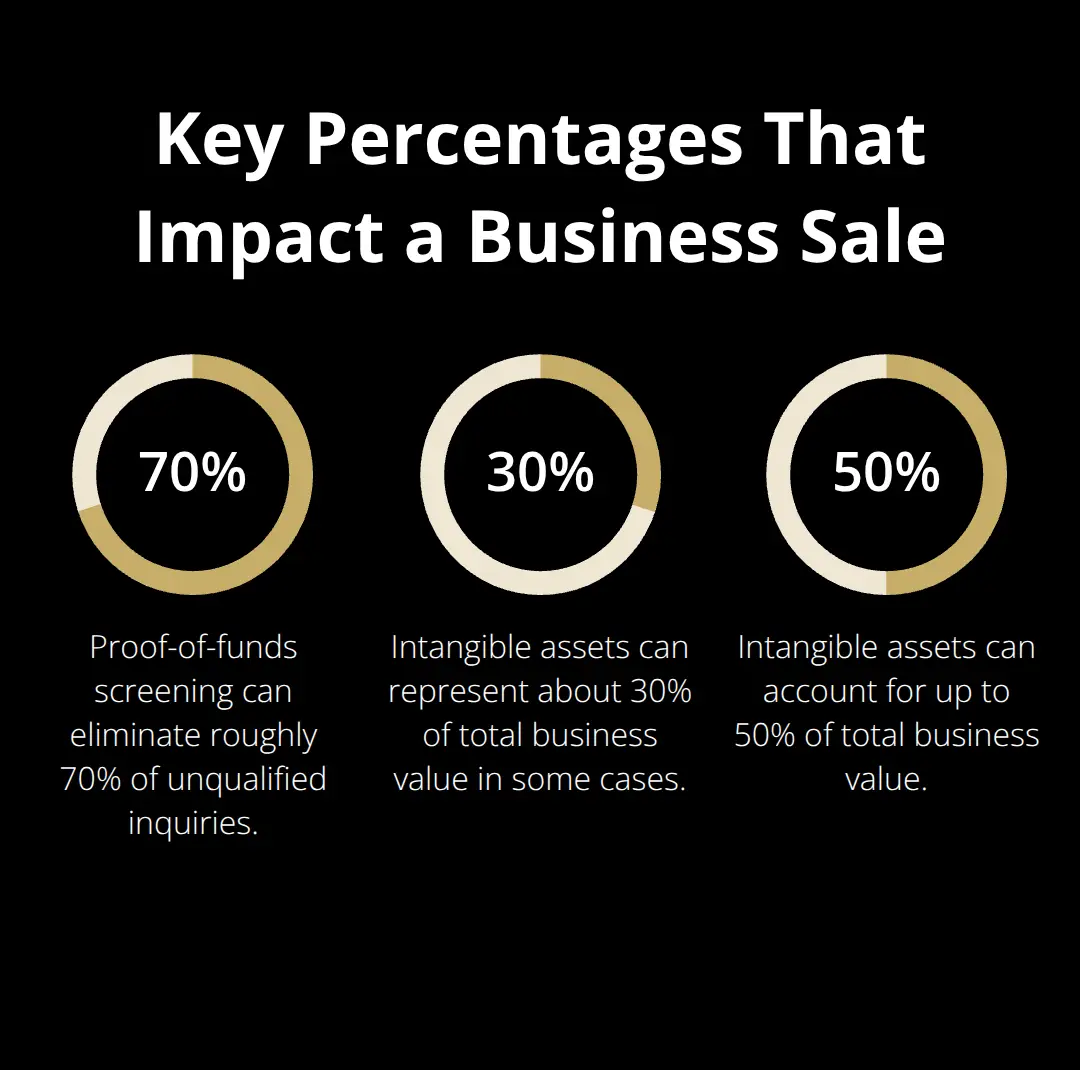

A supermarket with $2 million in annual revenue might look impressive, but if profit margins are only 2 percent, that’s just $40,000 in annual profit. The market approach compares your business to similar businesses that sold recently. If comparable supermarkets in your area sold for five times annual profit, that becomes your benchmark. The assets approach values the tangible and intangible assets separately. For the supermarket owner, this includes the retail building, the mini strip mall with tenants, equipment, inventory, and the customer relationships built over years. Intangible assets like brand reputation, customer loyalty, and the lease agreements on those retail spaces often represent 30 to 50 percent of total value. Hire a professional business valuation specialist to assess your business properly. This can range from $5,000 to $20,000 or more but prevents you from massively underpricing or overpricing your business. An overpriced listing sits on the market and signals weakness to buyers. An underpriced business leaves money on the table that you’ll never recover.

Create Your Marketing Strategy

With your financials verified, assets catalogued, and compliance records organized, you’re ready to market your business to potential buyers. The next phase requires you to craft an attractive listing and reach qualified prospects through multiple channels.

Marketing Your Business to Potential Buyers

Craft a Listing That Attracts Serious Buyers

Your listing makes the first impression potential buyers receive, so it must stand out immediately. A weak listing sits dormant for months while a strong one generates qualified inquiries within weeks. Lead with a headline that emphasizes what makes your business valuable, not just what it is. Instead of “Established Pizza Restaurant,” write “Profitable Pizza Restaurant with Three Locations and 40-Year Customer Base.” Include specific numbers: annual revenue, profit margins, customer count, years in operation, and growth rate. Buyers scan dozens of listings, so concrete details separate your business from generic postings.

Describe your competitive advantages clearly. What do you do better than competitors? Exclusive supplier contracts, proprietary systems, loyal repeat customers, or a prime location all matter. If your business generates recurring revenue or holds long-term customer contracts, highlight that prominently because it signals stability to buyers. High-quality photos of your storefront, operations, and unique assets like real estate or equipment help buyers visualize what they’re purchasing. Create a one-page executive summary that walks through financials, growth trajectory, and why this represents a smart acquisition. This summary becomes your sales document when prospects inquire.

Price your listing strategically based on your professional valuation, not gut feeling. Overpriced listings languish and signal weakness to sophisticated buyers. Underpriced listings sell quickly but leave substantial money on the table. Your valuation specialist provides the right starting price.

Reach Buyers Through Multiple Channels

Qualified buyers exist across different platforms, so you must cast a wide net rather than relying on a single channel. Industry-specific marketplaces attract serious buyers actively shopping in your sector. General business sale platforms cast a wider net but include more casual browsers. LinkedIn and industry networks connect you with strategic buyers who understand your market. Consider hiring a business broker who maintains relationships with acquisition firms, private equity groups, and individual investors actively seeking businesses like yours. Brokers typically charge 8 to 10 percent commission but accelerate the timeline and filter out unqualified prospects.

Protect Your Information With Strategic Screening

When you start outreach, require every interested party to sign a non-disclosure agreement before accessing detailed financial information. An NDA protects your competitive secrets and prevents information from reaching your competitors or employees. Serious prospects sign NDAs without hesitation; tire-kickers and competitors trying to gather intelligence will push back.

Screen prospects by requiring proof of financial capability before sharing sensitive documents. Ask for bank statements or letters from their lender confirming they can fund the purchase. This single step eliminates roughly 70 percent of unqualified inquiries and saves you months of wasted conversations. Control information flow carefully by starting with basic business description and financials stripped of identifying details.

Only after a prospect signs an NDA and demonstrates financial readiness do you provide detailed customer lists, specific locations, supplier contracts, and operational data.

Timing matters here: reveal information gradually as trust builds and the prospect moves toward a serious offer. This staged approach protects your business while keeping qualified buyers engaged throughout the process. Once you’ve attracted serious prospects and screened them properly, you’ll shift focus to evaluating their offers and navigating the negotiation phase.

Navigating Negotiations and Due Diligence

Once serious buyers emerge from your screening process, the real work starts. Most sellers misjudge this phase entirely. They either accept the first offer out of relief or reject reasonable proposals because they’re anchored to an inflated asking price. The truth is harder: your job now is to evaluate offers objectively against your valuation, understand what each buyer’s terms actually mean financially, and negotiate from a position of knowledge rather than emotion.

Evaluating Offers Beyond the Headline Price

When an offer arrives, don’t fixate on the headline number. A $500,000 offer with seller financing at 3 percent interest over five years is fundamentally different from a $480,000 all-cash offer at closing. The all-cash offer is worth more because you receive the money immediately and eliminate collection risk.

Calculate the net present value of each offer by accounting for payment timing, interest rates on any financed portion, and earnout provisions that tie part of your payment to future performance. If a buyer proposes an earnout where you receive $100,000 only if the business hits revenue targets you don’t control, that money may never arrive. Many sellers discover post-close that earnout conditions were written so tightly that buyers could never trigger them. Insist that earnout metrics are realistic and tied to metrics the new owner can actually influence.

Beyond price structure, evaluate what the buyer wants included in the sale. Are they purchasing the business entity itself, or just the assets? Does the sale include customer contracts, supplier agreements, and intellectual property? Are you expected to stay on for three months training the new owner, or are you walking away at closing? Each element affects your tax liability and post-sale obligations. Have your accountant and attorney model the tax consequences of different deal structures before you commit to negotiating around any particular offer.

Preparing for Due Diligence Requests

When a buyer moves past the initial offer stage, they request extensive documentation. This is where most deals either accelerate or stall. Buyers will ask for five years of tax returns, detailed customer contracts, employee records, supplier agreements, insurance policies, and any litigation history. They’ll want access to your accounting software to verify financial claims independently. Some buyers hire forensic accountants to reconstruct your books from scratch. This isn’t adversarial; it’s standard practice because buyers need certainty before committing millions of dollars.

The speed at which you respond to these requests directly correlates with deal momentum. Sellers who organize documents in advance and respond within 48 hours to requests signal professionalism and move deals toward closing. Sellers who drag out responses or provide incomplete documentation create doubt that kills deals.

Maintain a digital data room with organized folders for financial records, legal documents, contracts, employee information, and compliance records. When buyers request specific items, you’re not scrambling through files for weeks. You’re sending documents within hours. During due diligence, buyers will also interview your key employees and sometimes your major customers. Prepare your team for these conversations in advance. Brief them on confidentiality and what information they should and shouldn’t discuss. A careless comment from an employee about declining margins or customer complaints can tank buyer confidence and destroy your negotiating position.

Addressing Buyer Concerns Transparently

Address buyer concerns transparently when they arise. If your profit margins declined last year, don’t hide it. Explain what caused the decline and what steps you’ve taken to reverse it. Buyers respect sellers who acknowledge problems and present solutions far more than sellers who pretend problems don’t exist. This honesty builds trust and accelerates the process toward closing.

Negotiating Payment Structure and Terms

Price negotiation matters less than most sellers think once you’ve established a defensible valuation. Where real negotiation happens is in payment structure, transition support, warranties, and post-sale obligations. A buyer might offer to increase price by 5 percent if you agree to stay on for six months training their team. That six-month commitment could be worth far more than the price increase if it means lower stress and smoother transition. Conversely, they might offer price concessions in exchange for you accepting liability for any customer contracts that fail post-close. Understand what each term costs you before trading it away.

Work with your attorney to draft a comprehensive Sale and Purchase Agreement that specifies exactly what you’re selling, what price you’re receiving, when payment occurs, what happens if assets are discovered to be missing or damaged, and what your obligations are post-close. The SPA protects you from buyer claims that they didn’t receive what they expected. Without clear documentation, disputes erupt after closing when you no longer control the business but still face liability.

Negotiate non-compete and confidentiality clauses carefully. If the buyer requires you to sign a two-year non-compete preventing you from starting a similar business, understand the geographic scope and whether it’s reasonable given your industry. Some buyers demand non-competes that are so broad they’re unenforceable anyway, so push back on unreasonable terms. Once you’ve agreed on price, structure, and all major terms, have your attorney review the final SPA before you sign anything. This final legal review catches provisions you might have missed and ensures your interests are protected through closing.

Closing Your Business Sale

Finalize all legal documentation with your attorney before closing arrives. The Sale and Purchase Agreement must specify exactly what transfers to the buyer, what remains yours, and how you’ll handle disputes after the sale concludes. Your accountant should review the final agreement to confirm the tax treatment matches your earlier negotiations, and request proof of funds from the buyer before you sign any closing documents.

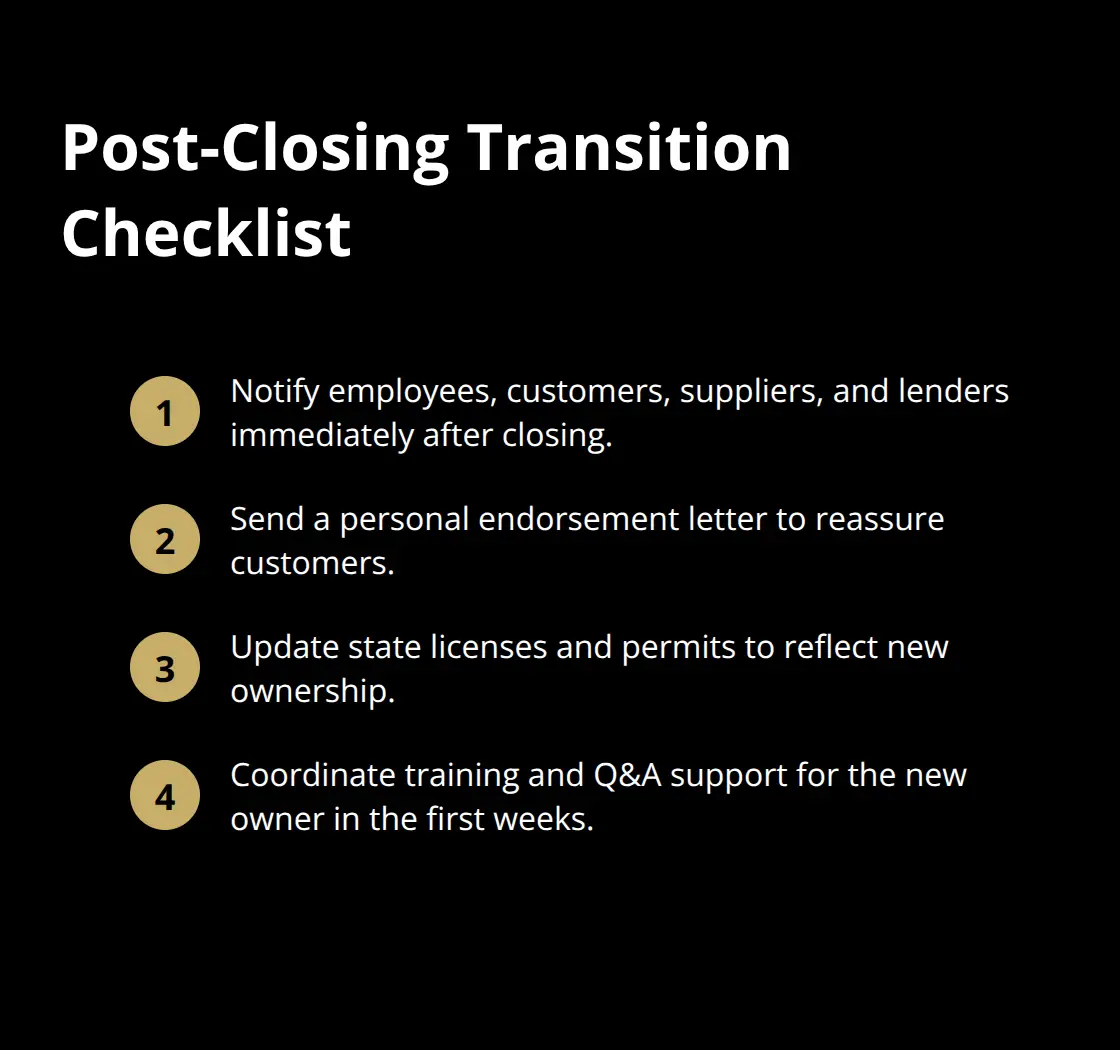

Notify your employees, customers, suppliers, and lenders immediately after closing transfers ownership. Send a personal letter from you endorsing the new owner to reassure customers that service quality will remain strong, and update your business licenses and permits with the state to reflect the ownership change.

The steps to sell business successfully culminate at closing, but your responsibility for a smooth transition continues for weeks afterward as you train the new owner and answer questions about the transition.

We at Unbroker recognize that selling a business involves complex legal, financial, and operational decisions at every stage. Our platform provides legal document templates and access to qualified buyers so you can navigate this process with confidence and transparency throughout your exit.