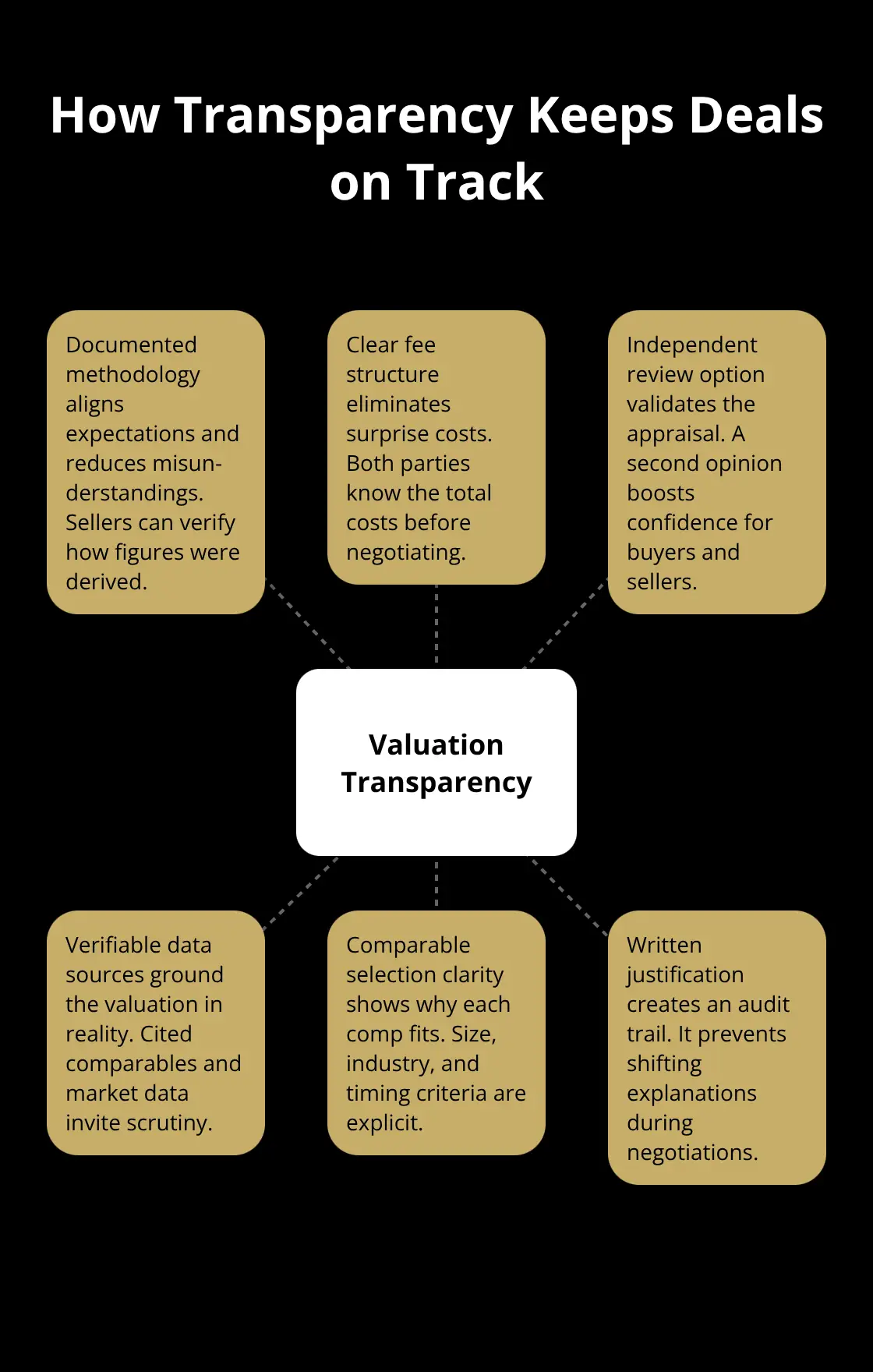

When sellers don’t know how their business was valued, they lose confidence in the entire process. Hidden fees, unclear methods, and vague appraisals create friction that damages deals and relationships.

At Unbroker, we believe a valuation transparency policy isn’t optional-it’s foundational. Sellers deserve to understand exactly how their business worth was calculated, step by step.

What Costs Are Hidden in Your Business Valuation

When a business sells without transparent upfront pricing, sellers often discover unexpected fees only after committing to a sale. Traditional brokers frequently charge commissions on the final sale price, which can result in substantial costs that weren’t clearly itemized upfront. These fees compound when brokers add processing charges, legal review costs, or technology fees buried in fine print. Sellers who don’t understand how their business was valued also can’t challenge inflated cost structures. Transparent upfront pricing allows sellers to know exactly what they’ll pay before moving forward, and the difference proves substantial.

The Opacity Problem in Valuation Methods

Many appraisers use proprietary valuation models that sellers never see. Without understanding whether the valuation relied on comparable sales, income approaches, or asset-based methods, sellers can’t evaluate if their business was fairly assessed. A seller might learn their business was valued at $800,000 when similar businesses in their market sold for $1.2 million, but without access to the appraiser’s methodology and data sources, they have no basis to question the conclusion. Studies on commercial real estate valuations show that when appraisers hide their data sources and adjustment rationale, disputes increase significantly. Clear documentation of how comparables were selected, what market adjustments were applied, and why certain revenue streams were weighted differently allows sellers to verify the valuation independently. Unclear appraisal methods also attract lower-quality buyers who sense vulnerability in the seller’s position.

Distrust Kills Deal Momentum

When valuation processes lack transparency, relationships between buyers and sellers deteriorate quickly. A seller who doesn’t understand their valuation feels manipulated, even if the appraiser acted fairly. This emotional disconnect creates negotiation friction that extends timelines and kills deals that could have succeeded. Buyers also hesitate when they sense sellers don’t trust the process, because buyer confidence depends on knowing that both parties accept the valuation logic. Transparent processes with documented reasoning, independent valuation review options, and clear fee structures eliminate these friction points.

Sellers who understand their valuation are more likely to accept fair offers and close transactions efficiently.

How Documentation Protects Both Parties

Sellers need written justification for every valuation conclusion, not vague summaries that leave room for interpretation. When appraisers document their methodology upfront (comparable selection criteria, market adjustments, revenue weighting), both parties can reference the same facts throughout negotiations. This documentation also protects appraisers from accusations of bias or unfair assessment. Buyers gain confidence knowing the valuation rests on verifiable data rather than subjective judgment. Independent review options further strengthen trust by allowing sellers to have a third party validate the appraisal without starting the entire process over.

The Path Forward Requires Accountability

Sellers deserve to know exactly how their business worth was calculated, step by step. Appraisers who hide their methods or charge hidden fees create the very distrust that derails transactions. The solution isn’t complex: document every step, justify every conclusion, and offer independent review. These practices shift power back to sellers and create the foundation for fair, efficient deals. When both parties understand the valuation logic and accept the fee structure upfront, the stage is set for what comes next.

Why Standard Frameworks Beat Proprietary Black Boxes

Standardized appraisal frameworks exist for a reason: they force appraisers to document their logic transparently. The Uniform Standards of Professional Appraisal Practice (USPAP) require appraisers to disclose their methodology, comparable selection criteria, and market adjustments. This isn’t bureaucracy-it’s a safeguard that prevents appraisers from hiding behind proprietary models that sellers can’t verify. When an appraiser uses a standardized framework grounded in comparable sales, income approaches, or asset-based methods, sellers can actually follow the reasoning. A seller can see that their business was valued at $950,000 because three comparable sales in their market averaged $945,000, adjusted upward by 0.5% for superior location. That’s verifiable. That’s defensible. Proprietary black-box models, by contrast, produce numbers that sellers must accept on faith. Standardized frameworks aren’t just better for transparency-they’re the only ethical foundation for valuation work.

Data Sources Matter More Than Formulas

Sellers often assume the appraiser’s formula determines fairness, but the real power lies in the data that feeds that formula. An appraiser using comparable sales data pulled from public records, MLS listings, and recent closed transactions grounds the valuation in market reality. An appraiser using outdated or cherry-picked comparables produces a valuation that looks legitimate but isn’t. When sellers receive detailed breakdowns showing exactly which comparables the appraiser selected, what adjustments they applied, and why they weighted certain data points differently, they can challenge weak reasoning immediately. A seller might notice the appraiser used a comparable that sold two years ago in a declining market, or excluded a more recent sale that would have raised the valuation. Transparent data sources allow sellers to spot these errors before signing anything.

Written Justification Shifts Power to the Seller

Appraisers who provide written justification for every valuation conclusion create an audit trail that protects everyone. The seller gains confidence knowing the valuation rests on documented facts, not subjective judgment calls made behind closed doors. The buyer gains assurance that both parties are working from the same information. When an appraiser documents why they weighted revenue streams a certain way, or why they applied adjustments for market conditions, the seller can evaluate whether those decisions were reasonable. This written record also prevents appraisers from changing their story during negotiations. A seller armed with documented methodology can push back on vague explanations or unsupported conclusions. The appraiser who hides their reasoning creates suspicion. The appraiser who documents everything builds credibility instantly.

Independent Review Validates the Numbers

A third-party review of the appraisal provides sellers with objective confirmation that the valuation holds up under scrutiny. When sellers have access to independent appraisers review validation, they eliminate the fear that they’ve been undervalued. This review process doesn’t require starting from scratch-an independent appraiser can examine the original appraiser’s comparable selection, market adjustments, and final conclusion against the documented evidence. If the original appraisal withstands independent review, the seller moves forward with confidence. If weaknesses emerge, the seller has concrete grounds to request a revised valuation before the deal advances. Independent review transforms appraisal from a take-it-or-leave-it proposition into a verifiable process that both parties can trust.

Transparency Exposes Weak Methodology Immediately

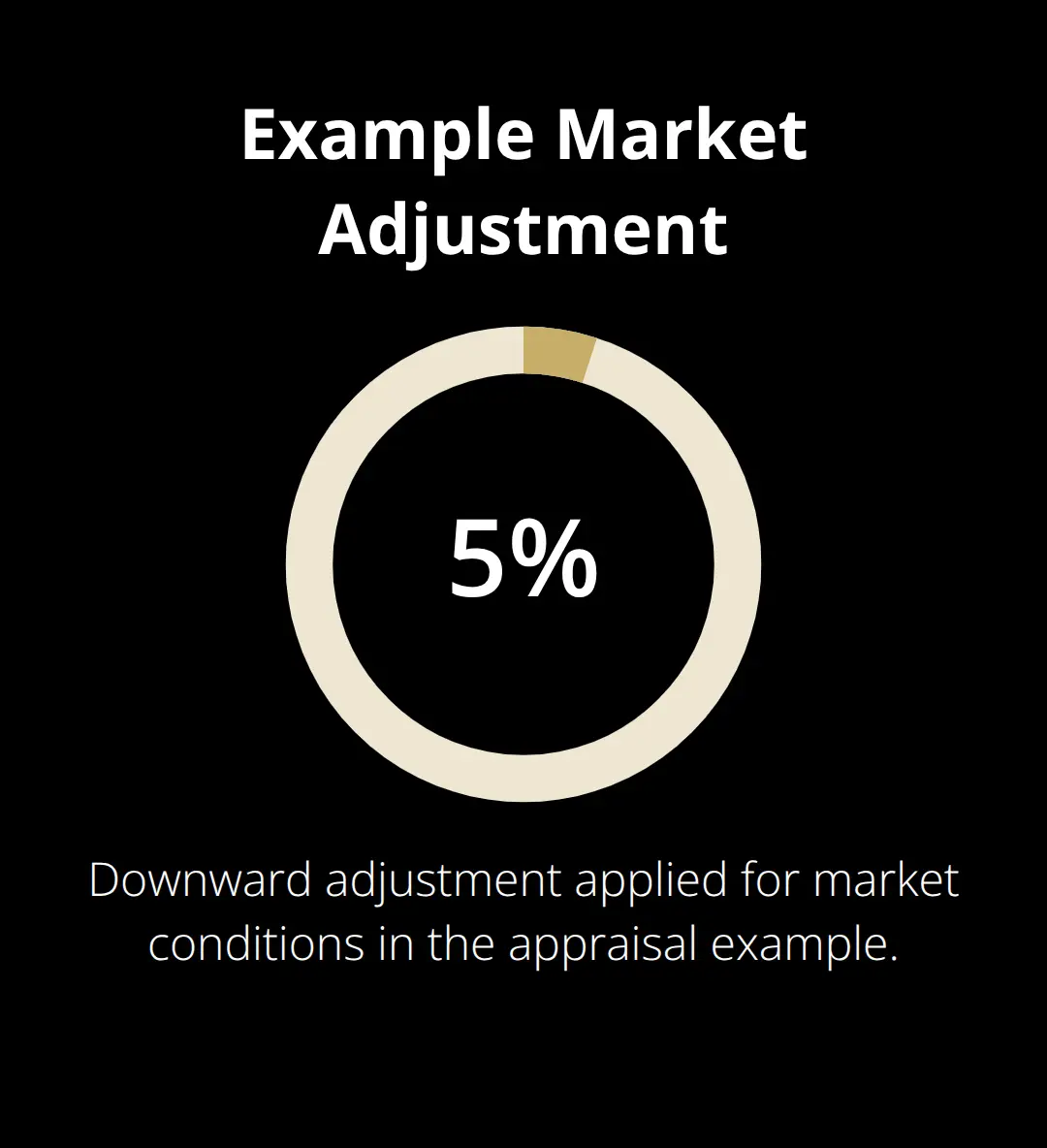

When appraisers hide their methods, sellers discover problems too late-often after they’ve already committed to a sale. Transparent documentation exposes weak methodology before commitments harden. A seller reviewing the appraiser’s comparable selection might immediately spot that the appraiser excluded recent sales that would have supported a higher valuation, or included sales from markets that don’t match the seller’s business profile. A seller examining the market adjustments might question why the appraiser applied a 5% downward adjustment for market conditions when recent comparable sales suggest the market has stabilized. These conversations happen early and constructively when documentation is clear.

Sellers who understand the appraisal logic can work with appraisers to refine the analysis, or they can seek a second opinion before moving forward. Opacity, by contrast, leaves sellers discovering problems during final negotiations when leverage has shifted.

Making Transparency Non-Negotiable in Your Appraisal

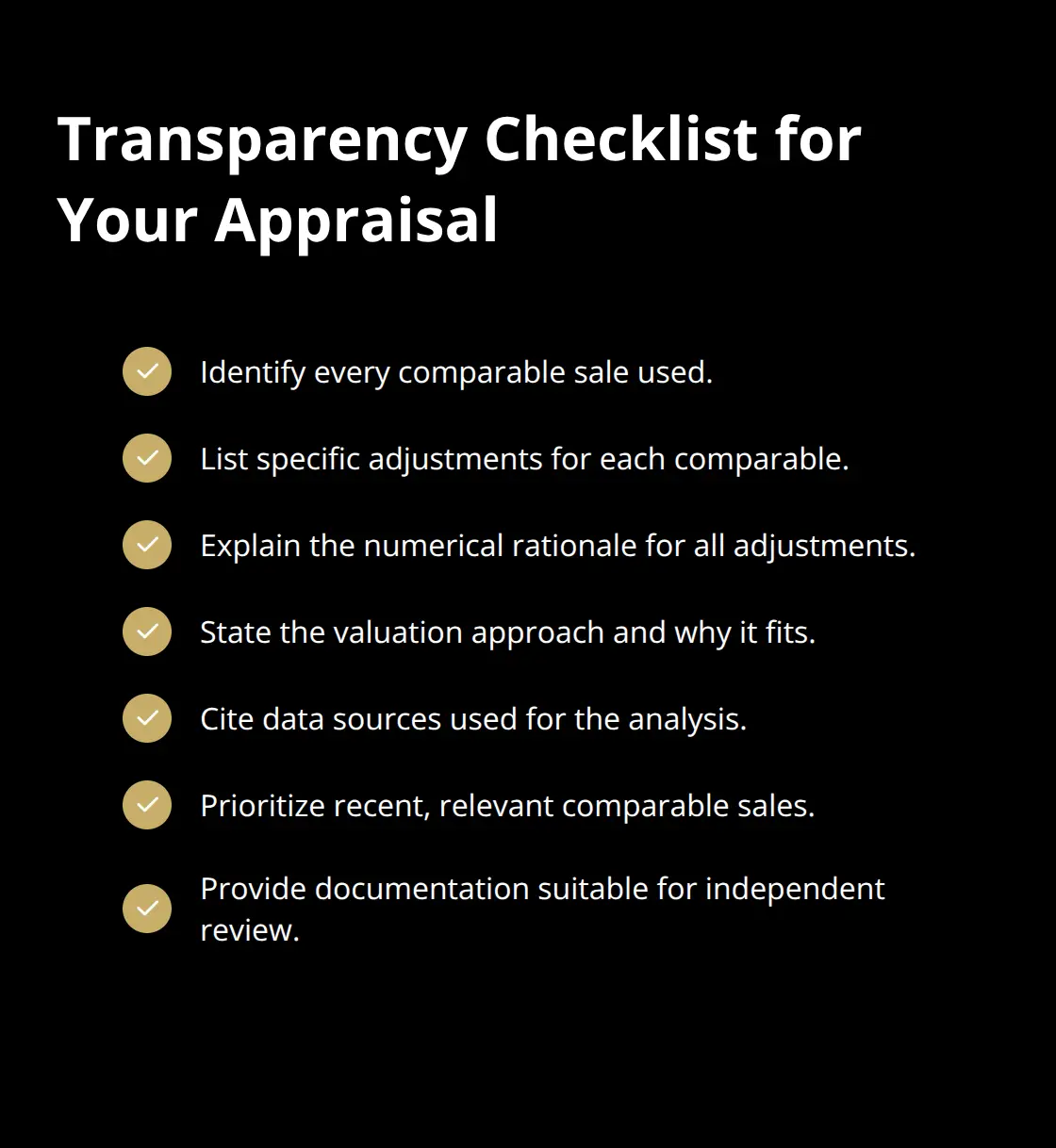

Transparent appraisals don’t happen by accident. Appraisers must commit upfront to specific documentation standards, and sellers must demand them. The first step is establishing what transparent documentation actually looks like. An appraiser should provide a detailed written report that identifies every comparable sale used, the specific adjustments applied to each comparable (location adjustment, market conditions, property condition), and the numerical rationale for those adjustments. If an appraiser selects three comparable businesses that sold for $900,000, $950,000, and $1,100,000, the report should explain why the $1,100,000 sale received a downward adjustment of 8% due to superior location in the comparable, while the seller’s business received no such adjustment. This level of detail transforms an appraisal from a black box into a verifiable analysis. Sellers should also receive a clear breakdown of which valuation approach the appraiser used (comparable sales, income approach, or asset-based method) and why that approach fit their specific business.

When an appraiser documents their data sources, sellers can verify whether the information came from public records, industry databases, or direct market research. An appraiser relying on stale comparable data from 18 months ago produces a different result than one using sales from the past 90 days. Written documentation forces this distinction into the open.

Justification Prevents Silent Assumptions

Appraisers make countless micro-decisions during valuation that sellers never see unless those decisions appear in writing. They decide which revenue streams to weight heavily and which to discount. They determine whether to apply adjustments for market conditions, seasonal fluctuations, or customer concentration risk. They choose comparable businesses based on criteria that may or may not match the seller’s situation. When these decisions remain unwritten, sellers cannot evaluate whether they were reasonable. A seller might later discover the appraiser excluded a recent comparable sale because it occurred in a different geographic market, but the appraiser never explained why geographic proximity mattered more than business type similarity. Written justification prevents this problem entirely. The appraiser who documents their reasoning creates accountability that protects the seller and strengthens the appraisal’s defensibility. Independent appraisers reviewing the original work can quickly assess whether the logic holds up. Buyers examining the appraisal can understand the valuation foundation instead of wondering whether hidden assumptions inflated or deflated the number. This written record also prevents appraisers from shifting their rationale mid-negotiation. A seller armed with documented methodology can point to specific language in the appraisal report and say, “You applied this adjustment here; why would you ignore it now?” The appraiser cannot claim to have meant something different without contradicting their own written work.

Third-Party Review Creates Objective Confirmation

Independent appraisal review serves as a critical quality control mechanism that sellers should insist on before committing to a sale. A second appraiser examines the original work and validates whether comparable selection was appropriate, whether adjustments were reasonable, and whether the final valuation reflects the documented methodology. This review process costs significantly less than a full appraisal because the independent appraiser works from existing documentation rather than starting from scratch. Sellers who invest in independent review typically discover either that their original appraisal was sound and they can proceed with confidence, or that specific weaknesses exist and they have grounds to request revision before the deal advances. The independent appraiser might identify that the original appraiser used comparables that were too large or too small relative to the business, or that market adjustments didn’t align with actual market conditions in the seller’s area. These findings give sellers leverage to address problems while appraisers can still revise their work. Without independent review, sellers discover these issues too late, during final negotiations when their position has weakened. Sellers should explicitly request that appraisers provide their work in a format that allows independent review, and they should budget for a second opinion before moving forward on any significant business sale.

Demand Detailed Comparable Selection Criteria

Appraisers must explain exactly how they selected comparable companies and why those selections matched the business being valued. A seller reviewing the appraiser’s work should see clear criteria: business size (revenue range), industry type, geographic location, age of the business, and profitability metrics. If the appraiser selected comparables that sold for $800,000 to $1.2 million, the report should state whether those businesses had similar revenue (within 10-20% of the subject business) or whether the appraiser applied larger adjustments to account for size differences. A seller might question why the appraiser included a comparable from a different state or excluded a recent sale from their own market. Transparent documentation answers these questions upfront. Appraisers who hide their comparable selection criteria leave sellers vulnerable to discovering later that the analysis rested on weak foundations. Clear criteria also help buyers understand why the valuation makes sense for their investment decision.

Verify Data Sources and Market Conditions

Sellers need to know exactly where the appraiser obtained their data and whether that data reflects current market conditions. An appraiser should disclose whether comparable sales came from public records, MLS listings, industry databases, or direct market research. The timing matters enormously. Comparable sales from the past 90 days reflect current market conditions far better than sales from a year ago. If market conditions have shifted (interest rates changed, supply increased, buyer demand declined), the appraiser should document how they adjusted for these changes. A seller examining the appraisal should see specific language explaining that market adjustments of 3-5% were applied because comparable sales occurred during a period of higher interest rates. This transparency allows sellers to evaluate whether the adjustments were reasonable or whether the appraiser missed important market shifts. Appraisers who rely on outdated data or fail to document market condition adjustments create valuations that don’t reflect reality.

Final Thoughts

Valuation transparency policies establish the foundation that keeps real estate markets functioning fairly. When appraisers document their methodology, justify their conclusions, and allow independent review, they attract serious buyers who trust the process. Buyers hesitate when they sense opacity because hidden assumptions create risk, while transparent valuations eliminate that friction and show exactly how comparable sales were selected, what market adjustments were applied, and why the final number makes sense.

Clear processes prevent disputes that drain time and money from both parties. When sellers understand their valuation upfront, they don’t challenge it later during negotiations, and when buyers see documented methodology, they don’t second-guess the numbers after committing capital. Transparent appraisals reduce disputes by establishing shared facts that both sides accept before moving forward, which protects everyone involved in the transaction.

At Unbroker, we’ve built our platform around valuation transparency as a core principle. Explore how Unbroker puts transparency first and see what fair selling actually looks like.