The wrong buyer financing choice kills 40% of business sales before they reach closing. Most sellers focus entirely on finding buyers but ignore whether those buyers can actually secure funding.

We at Unbroker see this mistake repeatedly. Smart sellers understand that financing options directly impact deal success, timeline, and final purchase price.

What Financing Options Actually Work

Cash buyers represent only 15% of business acquisitions, yet sellers often waste months chasing these unicorns. The Federal Reserve Bank of Boston found that SBA-backed transactions have evolved significantly since the global financial crisis, which makes SBA loans a key financing path. Traditional bank financing works for established businesses with strong cash flow, but small business lending has increased by 7.5% in recent quarters according to the Kansas City Fed.

SBA Loans Dominate Middle Market Sales

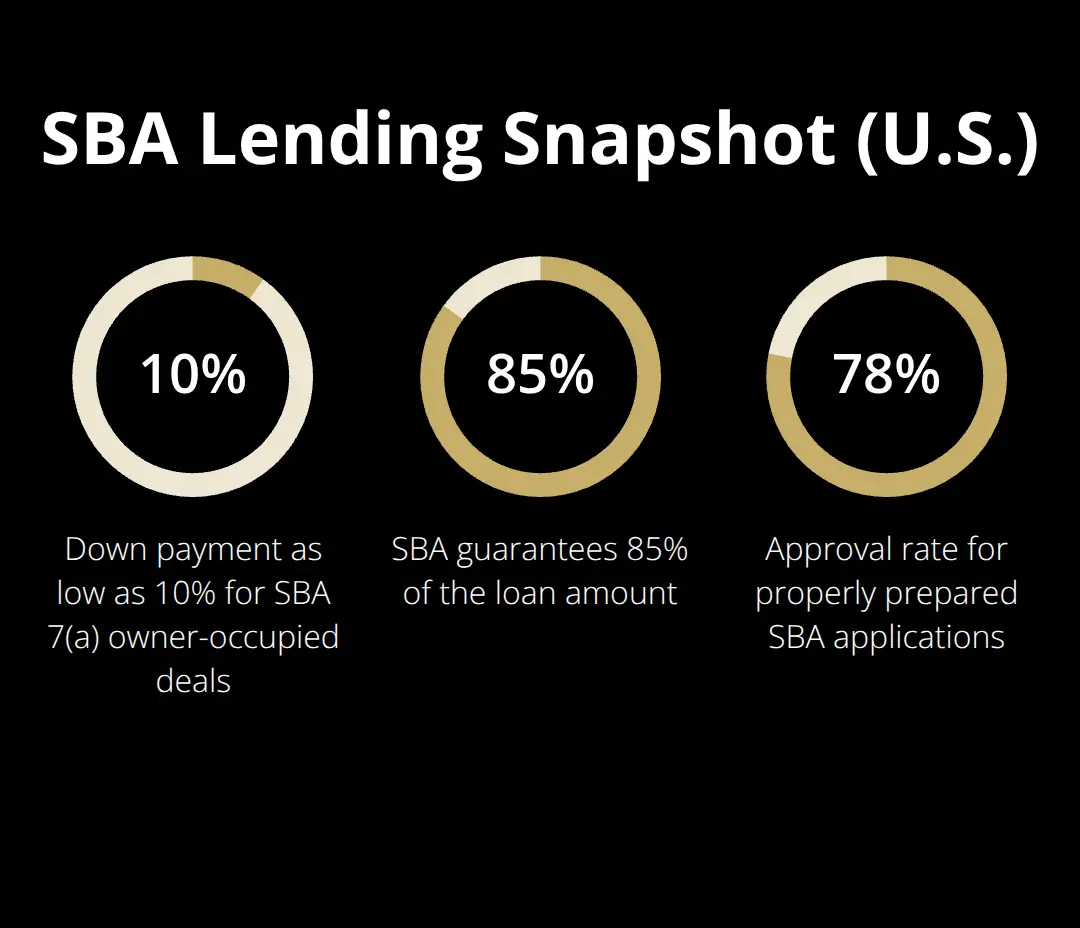

SBA 7(a) loans finance up to $5 million with down payments as low as 10% for owner-occupied businesses. The Small Business Administration backs 85% of the loan amount, which reduces bank risk and increases approval odds. Processing takes 60-90 days, but approval rates hit 78% for properly prepared applications. SBA Express loans cap at $500,000 but close in 30 days (perfect for smaller transactions).

Seller Financing Changes Everything

Seller financing accelerates closings and attracts buyers who cannot qualify for traditional loans. The International Business Brokers Association reports that seller financing accounts for 14% or less of most deals. Typical structures involve 20-30% seller notes with 3-5 year terms at market rates plus 1-2%. Earn-out arrangements tie payments to future performance, which reduces buyer risk but creates collection challenges for sellers. Smart sellers limit earn-outs to 12-18 months maximum.

Cash Deals Remain the Gold Standard

Cash transactions close fastest and carry the lowest risk of deal failure. These buyers often pay 5-10% below asking price but eliminate financing contingencies entirely. Cash buyers typically include private equity groups, strategic acquirers, and high-net-worth individuals (though they represent a small buyer pool). Sellers must verify proof of funds early to avoid wasting time on unqualified prospects.

The key lies in understanding how each financing option affects your specific deal structure and timeline.

How Financing Impacts Your Deal Success

Financing choice determines whether your business sells within 90 days or sits on the market for 18 months. The International Business Brokers Association found that deals with pre-approved SBA financing close 65% faster than those that require buyer financing approval during due diligence.

Cash deals average 45 days to close, while SBA transactions take 75-90 days, and seller-financed deals close in 60 days. Purchase prices vary dramatically based on financing structure. Cash buyers typically offer 8-12% below asking price but eliminate deal risk entirely. SBA buyers pay full asking price but require extensive financial documentation and appraisals that can derail deals.

Deal Failure Rates Reveal the Truth

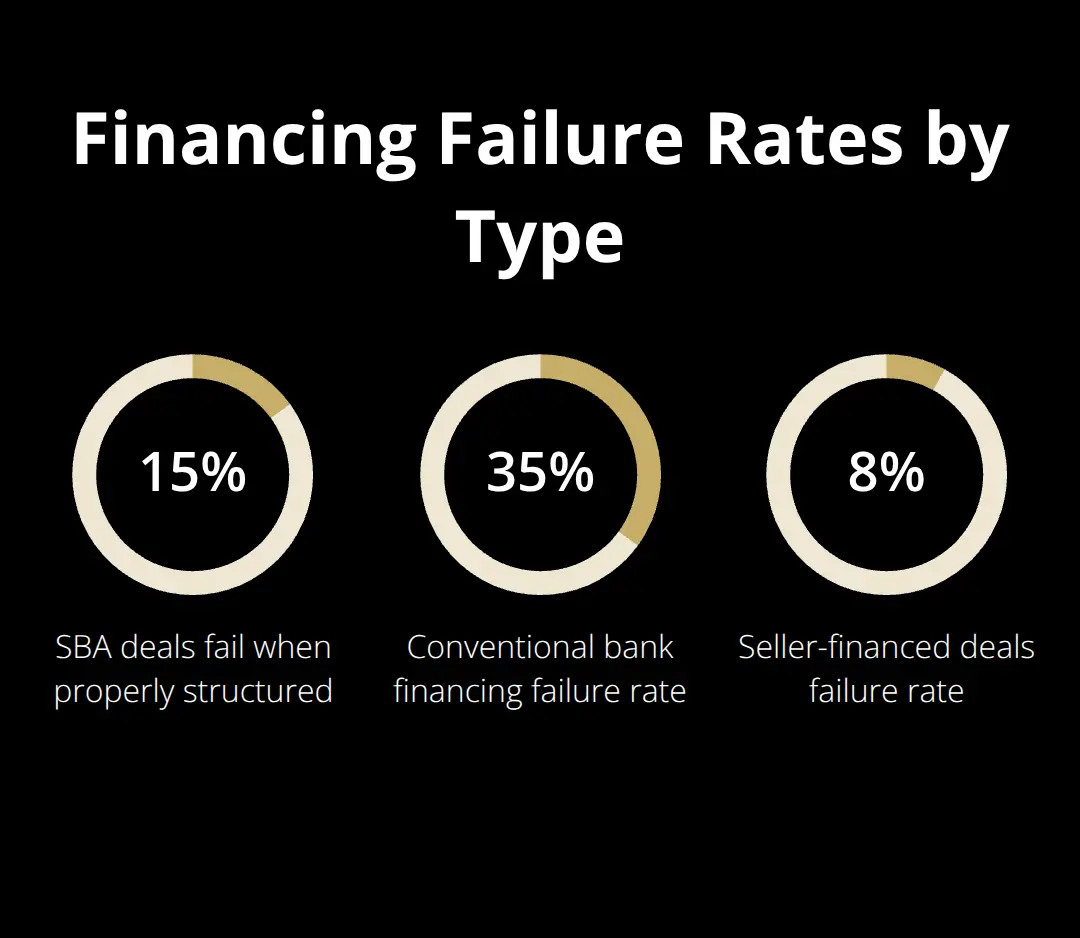

Business sales face significant financing challenges, with financing issues being a major cause of deal collapse after buyer qualification problems. SBA deals fail at 15% rates when properly structured, compared to 35% failure rates for conventional bank financing.

Seller financing reduces failure risk to 8% but creates collection challenges later. The timing of financing approval matters tremendously. Deals where buyers secure pre-approval before they make offers succeed 78% of the time versus 52% success rates for buyers who seek financing after contract signing.

Structure Drives Success or Failure

Asset-based deals qualify for financing more easily than stock purchases because banks prefer tangible collateral. Service businesses with recurring revenue streams get approved 40% more often than project-based companies.

Businesses with EBITDA above $200,000 access multiple financing options, while smaller deals depend heavily on SBA programs or seller financing. The debt-to-equity ratio in your deal structure directly impacts approval odds. SBA loans require buyers to inject 10-15% equity, while conventional loans demand 25-30% down payments.

Market Conditions Shape Financing Success

Current prime rates at 7% have tightened lending standards across all business financing categories. Banks now scrutinize cash flow projections more carefully and require stronger personal guarantees from buyers.

This environment favors businesses with consistent revenue patterns and established customer relationships. Seasonal businesses or those dependent on a few large clients face additional financing hurdles that sellers must address proactively.

Smart sellers structure deals to maximize financing options rather than optimize only for purchase price. This strategic approach becomes even more important when you prepare your business for the financing approval process.

How to Position Your Business for Maximum Financing Success

Lenders have varying approval rates for business acquisition loans, with full approval rates being highest at small banks, credit unions, and finance companies, yet most sellers wait until after they find a buyer to organize their records. Smart sellers prepare complete financing packages before they list their business, which significantly reduces approval time.

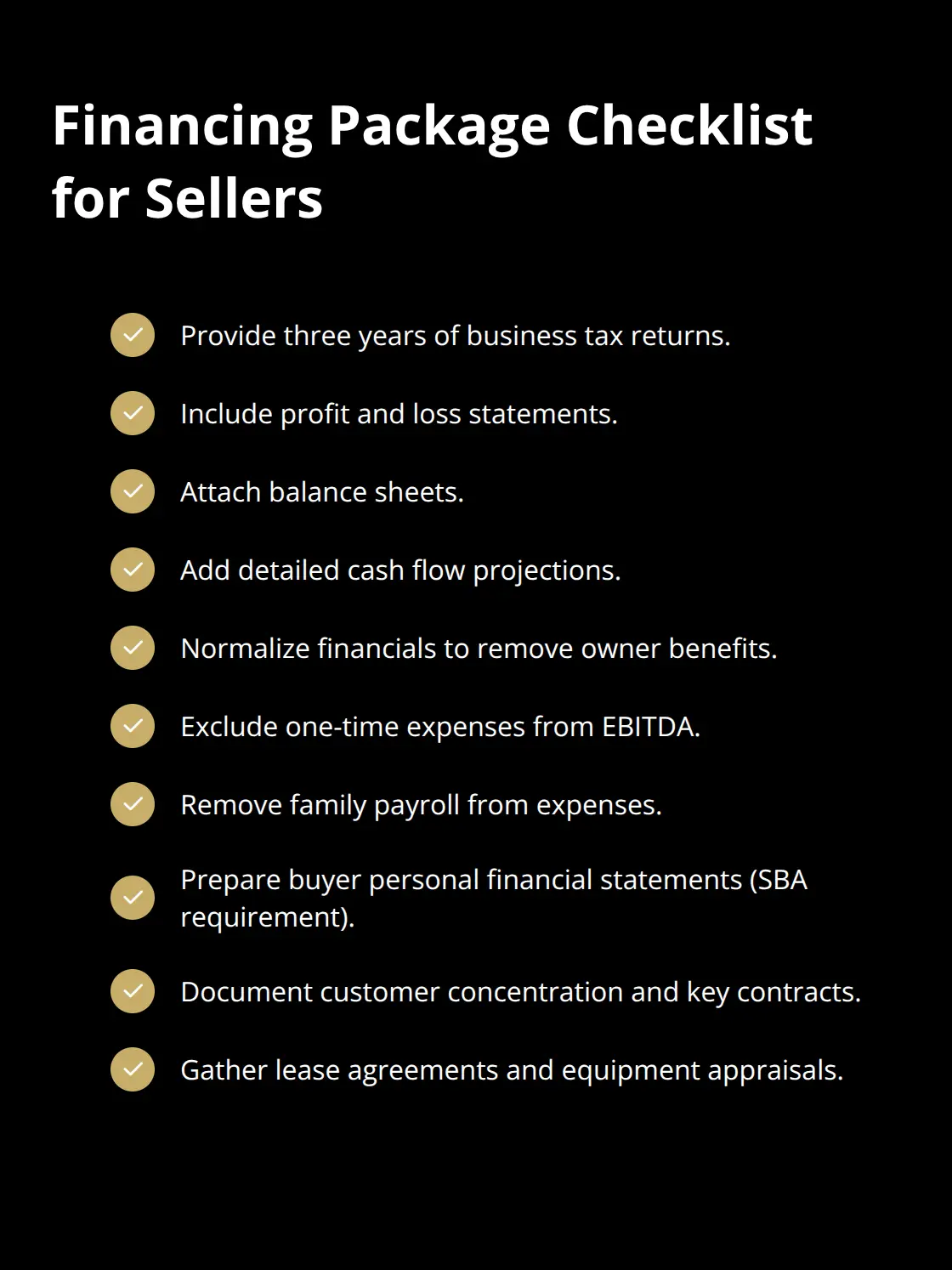

Your financial package must include three years of tax returns, profit and loss statements, balance sheets, and detailed cash flow projections. Banks scrutinize working capital calculations, so normalize your financials to remove owner benefits, one-time expenses, and family payroll. The SBA requires personal financial statements from buyers, but sellers who provide clean business financials increase approval odds substantially.

SBA-Approved Partners Accelerate Deal Closures

The entire SBA loan process generally takes about 60 to 90 days, though SBA Preferred Lenders can streamline this timeline through their enhanced approval authority. Only 3,800 lenders nationwide hold SBA Preferred status, so you create competitive advantage when you connect buyers with these institutions.

SBA Resource Partners like SCORE provide free consultation to buyers, which improves their loan applications and reduces seller risk. Smart sellers maintain relationships with 2-3 SBA lenders before they list their business (not after they sign a purchase agreement).

Structure Deals for Maximum Appeal

Asset sales differ from stock purchases in what is being transferred and how each structure affects taxes, liability and deal complexity. Real estate inclusion increases loan approval rates since buildings provide additional security for lenders.

Seller notes of 10-20% demonstrate confidence in your business and reduce bank risk exposure, which improves approval odds significantly. Avoid earn-out structures that exceed 15% of purchase price because banks view future performance payments as speculative.

Documentation Standards That Banks Demand

Banks require normalized EBITDA calculations that exclude owner salary above market rates, personal expenses, and one-time costs. Your accountant should prepare a detailed normalization schedule that explains each adjustment with supporting documentation.

Working capital adjustments should be clearly defined upfront to prevent delays during due diligence. Banks also want to see customer concentration analysis, lease agreements, and equipment appraisals for asset-heavy businesses. Before promoting your business, ensure all financial statements and key business documents are organized and ready for review.

Final Thoughts

Buyer financing determines whether your business sells quickly or sits on the market for months. The data shows that 40% of deals fail due to financing issues, yet most sellers ignore this reality until it’s too late. Smart sellers prepare complete financial packages before they list, maintain relationships with SBA-approved lenders, and structure deals to maximize financing options.

Cash buyers pay less but close faster, while SBA financing attracts the largest buyer pool with 78% approval rates for properly prepared applications. The key lies in understanding that financing choice affects purchase price, timeline, and deal success probability. Sellers who position their business for multiple financing options create competitive advantages that translate into faster sales and better terms.

We at Unbroker help sellers navigate these complexities through our transparent platform that eliminates high brokerage fees while providing expert support throughout the financing process. Don’t let buyer financing derail your sale. Start preparing your financial documentation today, build relationships with qualified lenders, and structure your deal to attract the broadest possible buyer pool.