Selling your business is one of the biggest financial decisions you’ll make. Getting seller due diligence right separates smooth exits from messy ones that drag on for months.

At Unbroker, we’ve seen firsthand how preparation transforms the sale process. The steps ahead will show you exactly what buyers expect to see.

What Financial Records Do Buyers Actually Need?

Buyers scrutinize financial records harder than anything else during due diligence. They’re looking for consistency, accuracy, and proof that your business generates real, sustainable profit. Pull your last three to five years of tax returns and match them line-by-line against your profit and loss statements. If these don’t align, buyers will assume you’re hiding something or don’t know your own numbers. The gap between what you report to the IRS and what your books show raises immediate red flags. Align them now, before a buyer finds the discrepancy.

Your P&L statements should show clear revenue trends, broken down by customer segment or service line so buyers can see which parts of your business actually drive profit. Many sellers lump everything together, which makes it impossible for a buyer to understand what they’re actually purchasing. Separate recurring revenue from one-time deals. Highlight your largest customers and their revenue contribution, because buyers will worry about customer concentration risk. If your top five customers represent more than 50% of revenue, a buyer will demand a discount or want proof that relationships are contractually locked in.

Bank Statements Reveal Cash Flow Patterns

Bank statements show cash flow patterns that P&L statements can’t capture alone. Compile the last 36 months of statements and reconcile them to your accounting records. Buyers use bank statements to verify that reported revenue actually hit your account and to spot irregular deposits, loans from owners, or unusual transfers that might distort earnings.

Clean up your receivables before diligence starts. If you carry old unpaid invoices, they reduce the working capital a buyer will actually receive at closing, which directly lowers the purchase price. Address past-due accounts now or be transparent about which customers are struggling to pay.

Owner Expenses and Adjusted Earnings

Buyers will look for owner discretionary expenses-your car lease, travel, meals-that inflated costs but won’t exist under new ownership. These adjustments can add back 10 to 20 percent to EBITDA if presented clearly, but only if you can show exactly what they are and prove they won’t recur. Organize invoices, receipts, and vendor statements by category so your accountant or a transaction adviser can prepare a quality of earnings report that defends your adjusted profit figure.

This report separates recurring business performance from noise and gives buyers confidence in what they’re actually purchasing. A strong quality of earnings report strengthens your valuation by identifying add backs and validating EBITDA. The next section covers the assets and intellectual property that round out what a buyer actually acquires.

Assess and Document Your Business Assets

Buyers purchase tangible assets, intellectual property, and the contractual relationships that sustain revenue. Start by creating a comprehensive fixed asset schedule that lists every piece of equipment, machinery, vehicles, and property with acquisition date, original cost, accumulated depreciation, and current condition. Buyers will physically inspect high-value items, so photograph equipment now and document any recent repairs or maintenance. If your equipment is outdated or nearing end-of-life, disclose it upfront rather than hoping a buyer won’t notice during their site visit.

Inventory and Physical Assets

Inventory presents a separate challenge: buyers typically won’t pay for slow-moving or obsolete stock, so clean up your inventory before valuation. Conduct a physical count, remove dead SKUs, and be honest about what actually sells. Your balance sheet inventory value means nothing if the warehouse holds products nobody wants. This step directly affects working capital calculations at closing-buyers will reconcile your stated inventory against what they actually receive, and any shortfall reduces the purchase price dollar-for-dollar.

Intellectual Property Ownership

Intellectual property is where many sellers leave money on the table. Patents, trademarks, proprietary software, customer lists, and trade secrets can represent significant value, yet sellers often fail to document them properly. Verify that all trademark registrations are current and that you own them outright-not your vendor or a contractor. If you’ve developed proprietary processes or software, document the source code, system architecture, and any third-party licenses embedded in your tools. Buyers will conduct IP searches and will demand intellectual property ownership and documentation, so pull your trademark registrations from the USPTO database and your patent filings now.

Contracts and Change-of-Control Clauses

Contracts and licenses require equal attention: review every material agreement-customer contracts, supplier relationships, software licenses, equipment leases, and franchise agreements-for change-of-control clauses that might trigger renegotiation or termination when ownership changes. Some contracts explicitly prohibit transfer without the other party’s written consent, which can crater deal value if you discover this during diligence. Identify which agreements need counterparty approval and start those conversations now. This proactive approach prevents surprises that could delay or derail closing.

Permits and Regulatory Certifications

Permits and regulatory certifications must be transferable and current; if your business requires industry licenses or permits, verify they transfer to a new owner and that no renewal is imminent. A buyer won’t close on a business where critical permits expire in 60 days or require expensive re-certification under new ownership. Document the status of each permit, renewal dates, and any conditions attached to them. With your assets and intellectual property properly inventoried and your contracts reviewed, the next step focuses on the legal and operational issues that could otherwise surface unexpectedly during buyer diligence.

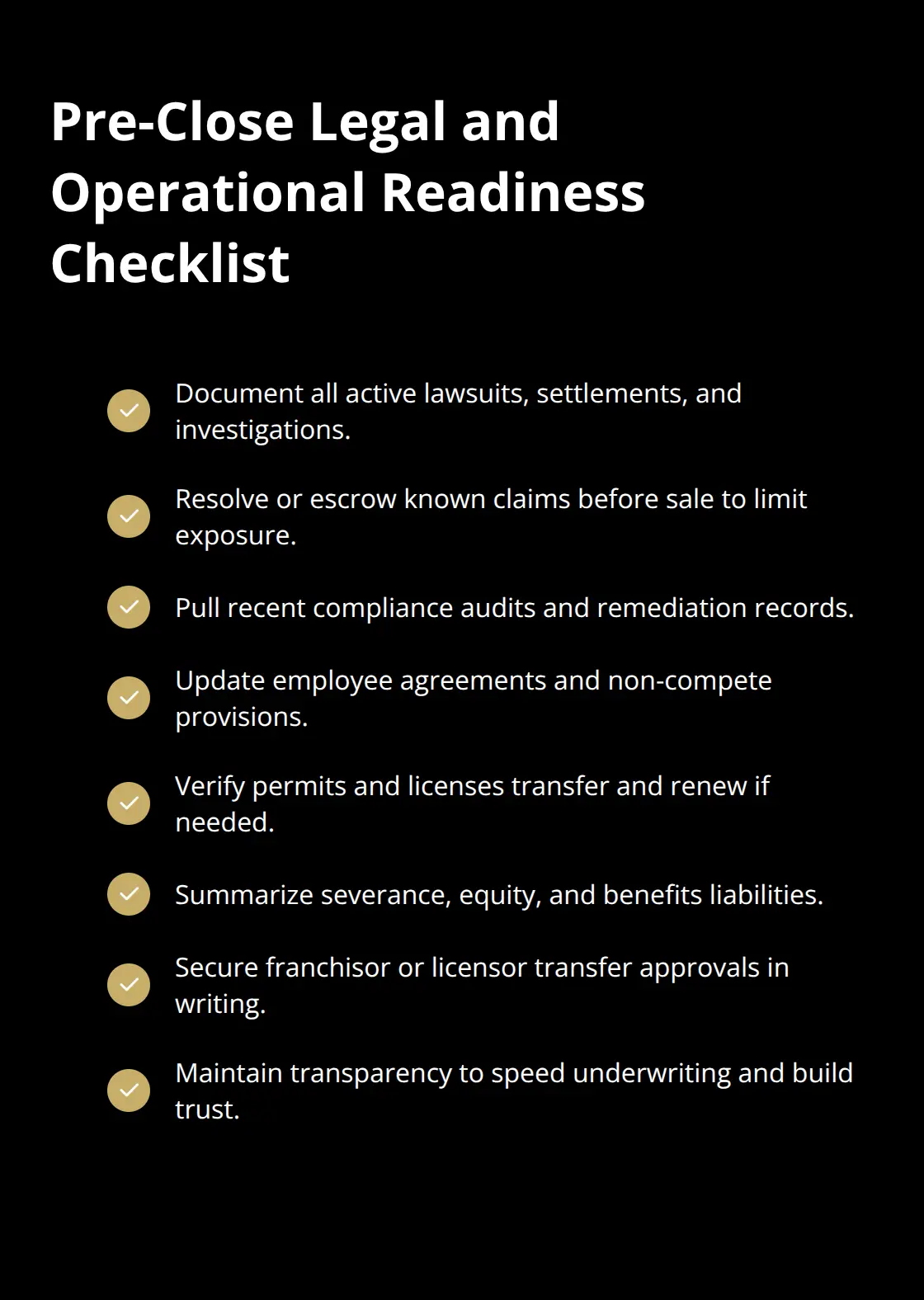

Address Legal and Operational Issues Before Closing

Litigation, compliance gaps, and outdated employee agreements surface immediately during buyer due diligence and can tank a deal. Document every active lawsuit, settlement, or regulatory investigation involving your business.

Buyers will conduct litigation searches through courthouse records, so hiding pending claims only delays closing and destroys trust. If you face a lawsuit, work with your attorney to resolve it before sale or reach a settlement agreement that transfers liability to the buyer through escrow holdbacks. Unresolved litigation typically triggers a purchase price reduction because buyers demand protection against unknown exposure.

Environmental violations, labor disputes, or tax audits create similar friction. If your business operates in a regulated industry-healthcare, construction, financial services-pull your compliance audit records and remediation documentation now. Show buyers that you addressed violations and that your operations meet current standards. This transparency moves deals forward rather than stalling them during final underwriting.

Update Employee Agreements and Non-Compete Clauses

Employee agreements require immediate review because non-compete clauses, severance obligations, and equity arrangements transfer complexity to the buyer. Pull every employment contract, offer letter, and bonus agreement on file. If you promised severance to key employees upon sale, that liability reduces purchase price dollar-for-dollar unless the buyer assumes it.

Non-compete clauses matter significantly: if your non-compete prevents you from competing post-sale but does not bind your employees, the buyer inherits the risk that your team walks out and starts a rival firm. Update all non-compete language to run with the business under new ownership and extend the term post-closing. This protects buyer value and demonstrates operational maturity.

If you granted equity or profit-sharing to employees, document the vesting schedules, strike prices, and any acceleration clauses triggered by sale. Buyers will demand clarity on how much equity vests at closing versus post-close, because this affects their actual net proceeds and creates retention incentives for key staff. Have your HR counsel prepare a summary showing total employee liabilities, benefits obligations, and any pending severance claims. This document prevents surprises and speeds underwriting approval.

Verify Permits and Licenses Transfer to New Ownership

Permits and licenses often determine whether a buyer can operate the business immediately after closing. Contact your state regulatory agency and each licensing authority to verify that permits transfer to new ownership and that no renewal deadlines approach. If your business holds an occupancy permit, health department license, or professional certification, confirm the transfer process and timeline with the issuing agency now.

Some permits require the new owner to apply for their own certification-a process that delays business operations post-closing. Others prohibit transfer entirely, forcing the buyer to operate under a temporary permit or cease business temporarily. Document these transfer requirements in writing from the regulatory body so the buyer understands the timeline and cost. If a critical permit expires within 12 months of closing, renew it before sale to eliminate buyer risk. This signals operational strength and removes a negotiation point that could derail the deal.

Address Franchise and License Transfer Requirements

Franchise agreements and exclusive distribution licenses require similar attention. Contact your franchisor or licensor and request written confirmation that the agreement transfers to a new owner without renegotiation or termination fees. If transfer requires franchisor approval, initiate that conversation early-some franchisors demand new fees or impose stricter terms on successor owners, costs that reduce buyer valuation. Getting written approval from your franchisor before closing prevents last-minute complications that could delay or kill the transaction.

Final Thoughts

Seller due diligence work you complete now-organizing financial records, documenting assets, resolving legal issues, and verifying permits-directly determines whether your sale closes on time or stalls in negotiation. Buyers move fast when they see a well-prepared business, and they move slowly when they uncover surprises. The steps outlined here address what buyers actually scrutinize, from financial records that align with tax filings to intellectual property properly registered and contracts reviewed for change-of-control clauses.

Thorough preparation delivers real benefits. You’ll command a higher purchase price because adjusted earnings are clearly documented and defensible. You’ll close faster because buyers won’t waste weeks chasing down missing documents or resolving ambiguities. You’ll avoid last-minute renegotiations triggered by discovered liabilities, and you’ll protect your reputation and the legacy of the business you built.

We at Unbroker understand that selling a business involves complexity and risk. That’s why we’ve built a platform that removes friction from the process-whether you choose our Full Service Business Sale or our Assisted Business Sale, you get access to legal document templates, negotiation assistance, and a network of qualified buyers. Visit Unbroker to explore how we can support your exit.