Most small business owners have no idea what their company is actually worth. Whether you’re planning to sell, seeking a loan, or just want to know your financial standing, understanding valuation methods explained is the first step.

At Unbroker, we’ve helped countless business owners navigate this process. The right valuation method depends on your industry, your goals, and the specific details of your business.

Why Your Business Valuation Matters Now

Knowing your business’s value isn’t just for when you’re ready to sell. It affects decisions you’re making right now-whether you’re applying for a loan, bringing in a partner, planning for retirement, or simply understanding if your hard work is paying off. Without a clear valuation, you’re operating blind. You might think your business is worth $500,000 when it’s actually worth $250,000, or vice versa. That gap creates real problems when banks reject your loan applications or investors walk away from the table. A formal valuation gives you concrete numbers backed by financial data, not guesses. It also protects you legally. If you ever face a partnership dispute, divorce proceedings, or inheritance matters, courts and lawyers demand documented valuations from qualified professionals. Most business owners have never had their company formally valued, which represents a missed opportunity.

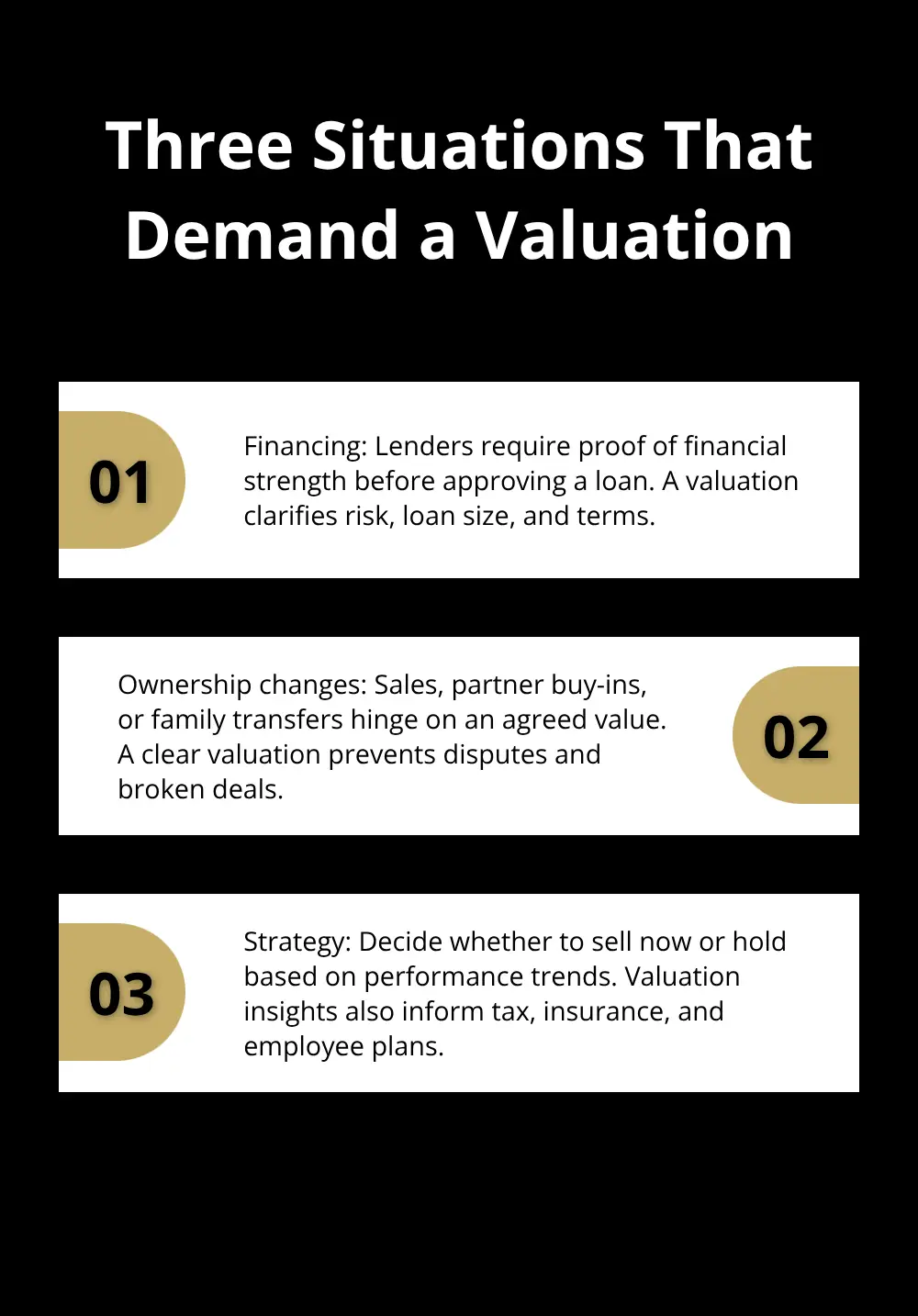

Three Situations That Demand a Valuation

Financing comes first. Banks and lenders won’t touch a loan application without knowing your business’s financial foundation. They use business valuation for loan applications to assess risk and determine how much they’ll lend.

Ownership changes come second. Whether you’re selling, bringing in partners, or transferring the business to family, everyone involved needs agreement on what the business is worth. Disagreements here destroy deals and relationships. Strategic decisions come third. You might want to know if it’s smarter to sell now or hold for another five years. A valuation reveals whether your profitability is trending up or stagnating, informing that choice. Tax planning, insurance coverage decisions, and employee stock plans all benefit from knowing your actual value. The cost of professional valuation typically ranges from a few thousand dollars for smaller businesses to much higher amounts for complex operations, but it’s an investment that pays for itself when it prevents costly mistakes or enables better decisions.

What Actually Drives Your Business Value

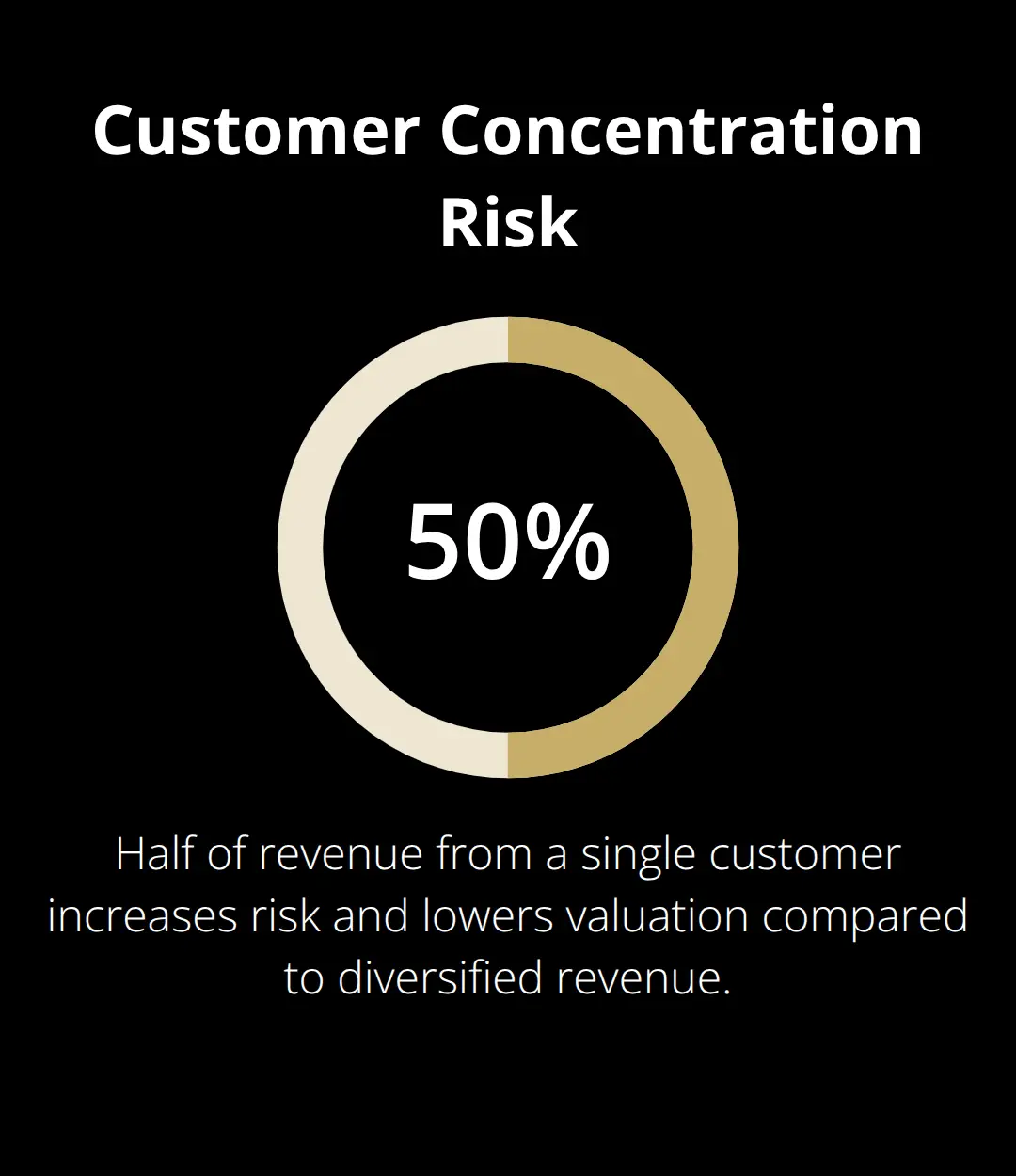

Cash flow matters most. A business that generates $100,000 in annual profit is fundamentally more valuable than one that generates $50,000, regardless of its size. This is why earnings-based valuation methods focus on profitability and cash flow stability. Inconsistent cash flow signals risk and lowers value. If your business swings from $50,000 profit one year to $150,000 the next, buyers and lenders see volatility and discount your valuation accordingly. Stability commands premium multiples. Your industry also shapes value dramatically. A software company with recurring subscription revenue might trade at 6-8x earnings, while a local service business might trade at 3-4x earnings. Growth businesses attract higher multiples. Your customer base composition matters too. If 50% of your revenue comes from one customer, your business is riskier and worth less than a competitor with diversified clients. The same applies to employee dependency-if you’re the only person who can serve clients, your business value collapses if you leave.

How Location and Intangibles Affect Your Worth

Location and market conditions directly influence value. A business in a thriving economic region outperforms an identical business in a declining area, and that difference shows up in valuation. Intangible assets like brand reputation, intellectual property, customer loyalty, and proprietary systems add real value that pure asset calculations miss. This is why comprehensive valuations look beyond the balance sheet. Your industry, revenue stability, growth trajectory, and asset composition all determine which valuation approach actually works. A service-based consulting firm generates value differently than a retail store with inventory. A professional practice like an accounting firm values its client relationships as its primary asset, while a manufacturing business depends on equipment and production capacity. Understanding these differences is essential before you select a valuation method that fits your situation.

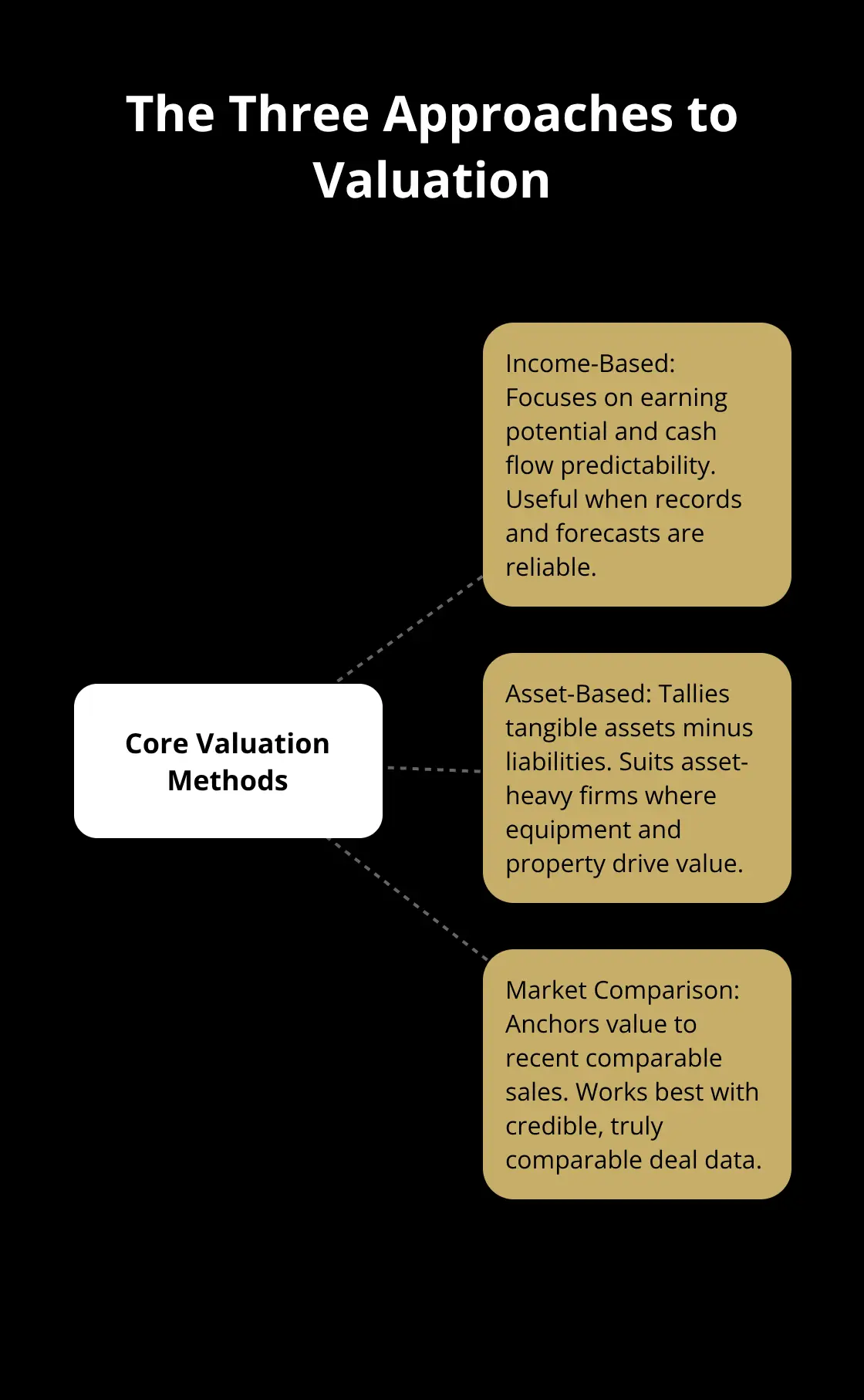

The Three Ways to Value a Small Business

Income-Based Valuation: What Your Business Earns

Income-based valuation focuses on what your business actually earns and projects those earnings forward. This method works by taking your annual profit (or a normalized version of it) and multiplying it by an earnings multiple that reflects your industry and risk level. A consulting firm generating $80,000 in annual owner profit might be valued at $240,000 to $400,000 depending on growth trajectory and stability, using multiples between 3x and 5x earnings. Software companies with recurring revenue typically command 6x to 8x multiples because their cash flows are more predictable.

The challenge lies in determining the right multiple for your specific situation. Industry benchmarks from sources like the Business Reference Guide vary significantly by sector, and applying the wrong multiple creates wildly inaccurate valuations. If your business has inconsistent earnings, you’ll need to normalize profits by adding back owner expenses that a new owner wouldn’t pay (like your inflated salary or personal vehicle costs).

Discounted cash flow represents the more rigorous income approach. You project future cash flows year by year and discount them to present value using a rate that reflects your business’s risk. This method works best when you have clear financial records spanning at least three years and can reasonably forecast the next three to five years of performance. Most small business owners lack the financial sophistication to execute this properly, which is why many rely on the simpler earnings multiple approach instead.

Asset-Based Valuation: Counting What You Own

Asset-based valuation calculates what your business is worth by adding up tangible assets (equipment, inventory, property) and subtracting all liabilities. A retail store with $200,000 in equipment and inventory minus $50,000 in debt would have a base asset value of $150,000. This method works well for asset-heavy businesses like manufacturing, retail, or equipment rental but severely undervalues service businesses where the real value sits in client relationships and expertise, not physical assets.

The major limitation is that asset-based valuation ignores your earning power entirely, which is why a profitable consulting firm with minimal assets would be dramatically undervalued using this approach alone. You need additional methods to capture the full picture of what your business can actually produce.

Market Comparison: What Similar Businesses Sold For

Market comparison valuation looks at what similar businesses actually sold for recently and uses those prices as benchmarks for yours. You choose comparable companies by looking for businesses with similar characteristics, such as industry, size, growth prospects, and other factors. The problem is finding truly comparable sales data. Most small business sales are private transactions with non-disclosed prices, and Canada has over 923 different industries making apples-to-apples comparisons extremely difficult.

Statistics Canada reports just over 1 million small businesses operating across the country, yet comparable sales data remains scarce for most sectors. Online valuation calculators that promise quick estimates typically use rules of thumb like 4x cash flow or 1x to 2x revenue, but these oversimplifications miss critical factors like customer concentration, growth rate, and management dependency that separate a $200,000 business from a $500,000 one with identical revenue.

Combining Methods for Accuracy

Professional valuators typically use a combination of all three methods, cross-checking results to arrive at a defensible range rather than a single magic number. Each approach reveals different aspects of your business’s worth. The income method captures earning potential, the asset method shows what you own, and the market method grounds your valuation in real-world transaction data. When these three approaches align reasonably well, you have confidence in your valuation.

When they diverge significantly, that gap itself tells you something important about your business-perhaps your assets are underutilized, or your earnings are unusually strong compared to market norms. Understanding which method applies best to your situation depends on your industry type and what you’re trying to accomplish with the valuation.

Which Valuation Method Works for Your Business Type

Match Your Industry to the Right Valuation Approach

Your industry determines which valuation method actually makes sense for your situation, and forcing the wrong approach wastes time and money. A software company with recurring subscription revenue needs income-based valuation because its value lives entirely in predictable future earnings, not in equipment or inventory. A manufacturing business with substantial machinery, tooling, and real estate requires asset-based valuation as a foundation because physical assets represent real collateral and replacement costs. A consulting firm values its client relationships above all else, making income-based methods essential since the client list is the primary asset.

Service businesses typically rely on earnings multiples because they generate cash flow without significant tangible assets. The mistake most owners make is trying to apply one method universally. A retail store owner who values their business using only asset-based calculations will dramatically undervalue the business if it has strong cash flow and customer loyalty. Conversely, a manufacturing business owner who ignores asset value and focuses only on earnings multiples may overvalue a business that depends on expensive equipment requiring constant reinvestment.

Align Your Valuation Goal with the Right Method

Your valuation goal shapes which method deserves priority. If you seek bank financing, lenders care most about cash flow stability and your ability to service debt, making income-based methods their primary focus. If you sell the business, buyers in your industry will use whatever method market participants typically use, so understanding local market practices matters enormously. If you plan for retirement or estate purposes, a comprehensive approach using all three methods provides the defensible documentation courts and tax authorities demand.

Why Online Tools Fall Short

DIY valuation tools and online calculators promise quick answers but deliver rough estimates at best. Most online tools ask for last 12 months sales and profit, then apply generic rules without considering customer concentration, growth trends, employee dependency, or industry-specific multiples. These tools miss the details that separate a $300,000 business from a $500,000 one with identical revenue.

What Professional Valuators Actually Do

Professional valuators spend time understanding your specific circumstances, normalizing your financial statements, analyzing your customer base composition, and applying industry benchmarks from sources like the Business Reference Guide that tracks hundreds of business types. They create defensible documentation that holds up in financing negotiations, partnership disputes, or tax audits, whereas online calculator results carry no credibility with lenders or lawyers. The cost difference between a $3,000 professional valuation and a free online calculator becomes negligible when the professional valuation prevents you from accepting a lowball offer or overpaying when acquiring a business.

Final Thoughts

You now understand how the three core valuation methods explained-income-based, asset-based, and market comparison-each reveal different aspects of your business’s worth. Income-based valuation captures your earning potential, asset-based valuation shows what you own, and market comparison grounds your value in real transaction data. The strongest valuations combine all three approaches, cross-checking results to arrive at a defensible range rather than chasing a single number that doesn’t exist.

Your next step depends on where you stand right now. If you prepare to sell, a professional valuation prevents costly mistakes and positions you for better negotiations. If you seek financing, a formal valuation demonstrates financial credibility to lenders and accelerates approval timelines. If you plan for retirement or handle ownership transitions, professional documentation protects you legally and provides the evidence tax authorities and courts demand.

Start by gathering three years of financial statements, tax returns, and detailed profit-and-loss records-clean financial data is non-negotiable. Document your customer base composition, revenue stability, and growth trends, then identify any one-time expenses or owner costs that distort your true earning power. Unbroker offers transparent, low-cost options that eliminate high brokerage fees while providing access to a vast buyer network and expert support throughout the process.