Most business owners have no idea what their company is actually worth. We at Unbroker see this constantly-founders guess, use outdated rules of thumb, or rely on gut feeling.

The truth is simpler than you think. There are three proven practical business valuation methods that give you a realistic price: what you own, what you earn, and what similar businesses sold for.

Asset-Based Valuation: What Your Business Owns

Understanding Net Asset Value

Asset-based valuation strips away guesswork and grounds pricing in concrete numbers: what the business owns minus what it owes. This method works by totaling all tangible assets-equipment, inventory, real estate, accounts receivable-and subtracting liabilities to arrive at net asset value. The appeal is straightforward: it’s objective, defensible, and easy to calculate from your balance sheet. However, this approach has a critical flaw that most owners ignore. Book value, the accounting figure on your balance sheet, reflects historical cost, not current market value. A piece of equipment purchased five years ago might be worth half what you paid for it, yet the books still show the original price. Conversely, your customer list, brand reputation, and proprietary processes-often worth far more than your tangible assets-don’t appear on the balance sheet at all. This gap between book value and reality is why asset-based valuation alone misleads you.

Adjusting Assets to Current Market Value

The fix requires you to adjust assets to current fair market value, not historical cost. Real estate appraisers value property at today’s market rates; equipment buyers pay what a used asset actually costs on the open market; inventory gets assessed at liquidation value if needed. Accounts receivable require a realistic collection rate-not all invoices convert to cash. For businesses with significant tangible assets like manufacturing or retail, this adjustment can swing valuation dramatically. A manufacturing firm with $5 million in book-value equipment might discover that equipment is worth only $2.5 million on the open market, instantly lowering the asset-based value. The opposite can occur with real estate in appreciating markets. The key is brutal honesty: what would a buyer actually pay for each asset right now, not what you think they’re worth or what you paid for them.

When Asset-Based Valuation Works Best

Asset-based valuation works best for asset-heavy businesses-those with substantial real estate, inventory, or equipment where tangible value dominates. It’s less useful for service firms or software companies where intangible assets like client relationships and intellectual property drive the real worth. This limitation means you’ll need a second valuation method to capture what your business actually earns, which often reveals far more value than your balance sheet ever could.

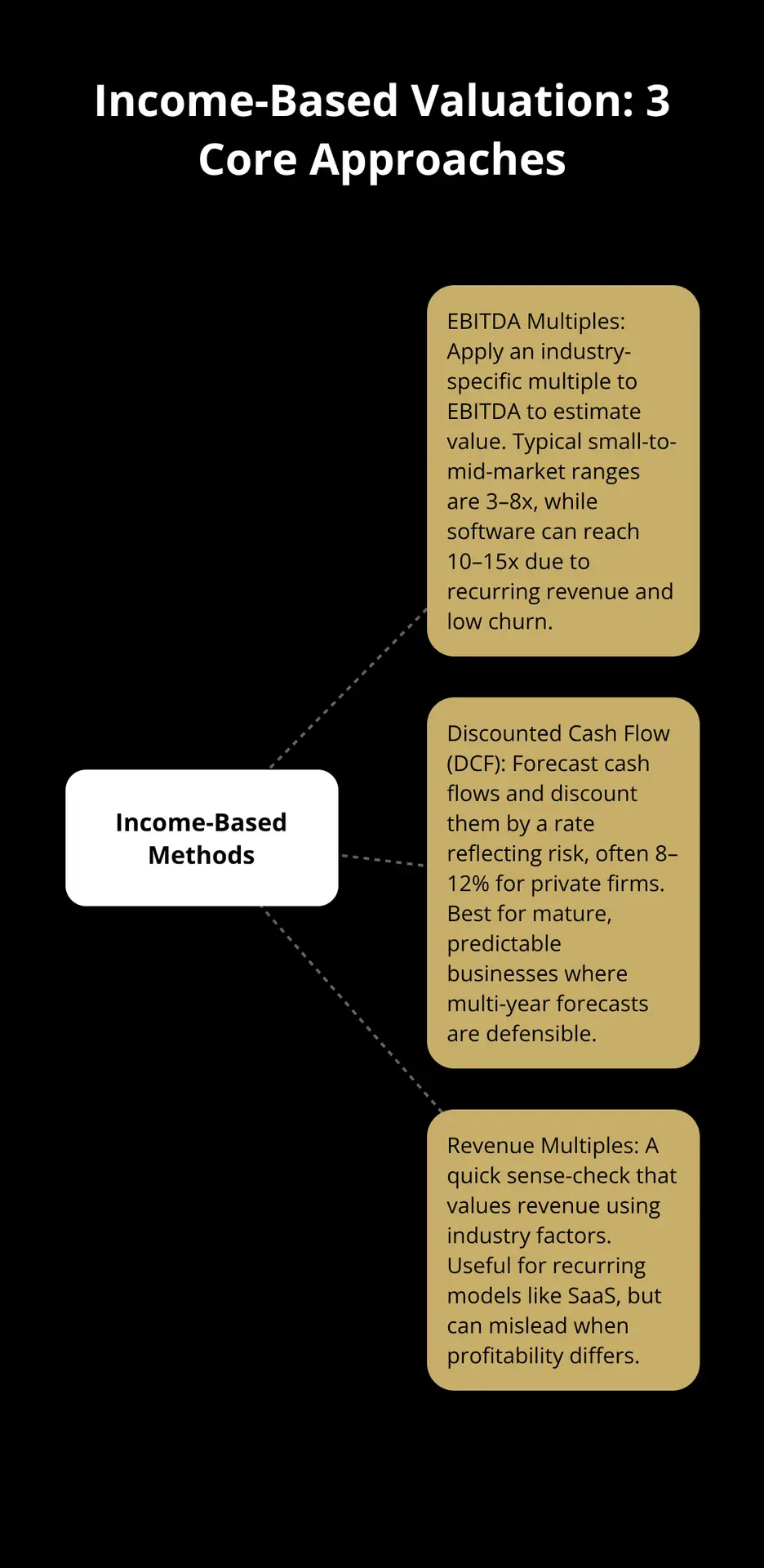

Income-Based Valuation: What Your Business Earns

Income-based valuation flips the asset-based approach on its head. Instead of asking what you own, it asks what you earn-and this distinction matters enormously. A software company with minimal equipment but $2 million in annual profit is worth far more than a manufacturing business with $10 million in machinery that generates only $500,000 in profit.

This is where most owners get valuation badly wrong. They fixate on revenue, not the cash their business actually produces after paying all costs. The income-based approach uses three concrete metrics to price your business: EBITDA multiples, discounted cash flow analysis, and revenue multiples. Each reveals different aspects of value, and choosing the right one depends entirely on your business type and what data you have available.

EBITDA and Profit Multiples: The Industry Standard

EBITDA stands for earnings before interest, taxes, depreciation, and amortization. It strips away financing decisions and accounting choices to show what the business genuinely earns from operations. This matters because two identical businesses can report wildly different net income based solely on how much debt they carry or their tax situation. EBITDA eliminates that noise. To calculate it, take your operating profit and add back depreciation and amortization. A service business earning $1 million in net income with $200,000 in depreciation has $1.2 million in EBITDA. The next step is applying an industry-specific multiple. A typical small-to-mid-market business sells for 3 to 8 times EBITDA, depending on growth rate, customer concentration, and market conditions. Software companies command higher multiples-often 10 to 15 times EBITDA-because recurring revenue and low customer churn create predictable future earnings. A manufacturing business might sell for 4 to 6 times EBITDA due to higher capital requirements and lower growth potential. The specific multiple you apply should come from recent comparable sales in your industry, not industry averages you find online. A business with $500,000 in EBITDA valued at 5 times EBITDA equals $2.5 million. That’s the power of the multiple approach: it’s fast, defensible, and grounded in what actual buyers paid for similar businesses. The risk lies in applying the wrong multiple. Many owners assume their business deserves a premium multiple without justifying it through growth rates, customer retention, or competitive advantage.

Discounted Cash Flow: The Theoretically Superior But Demanding Method

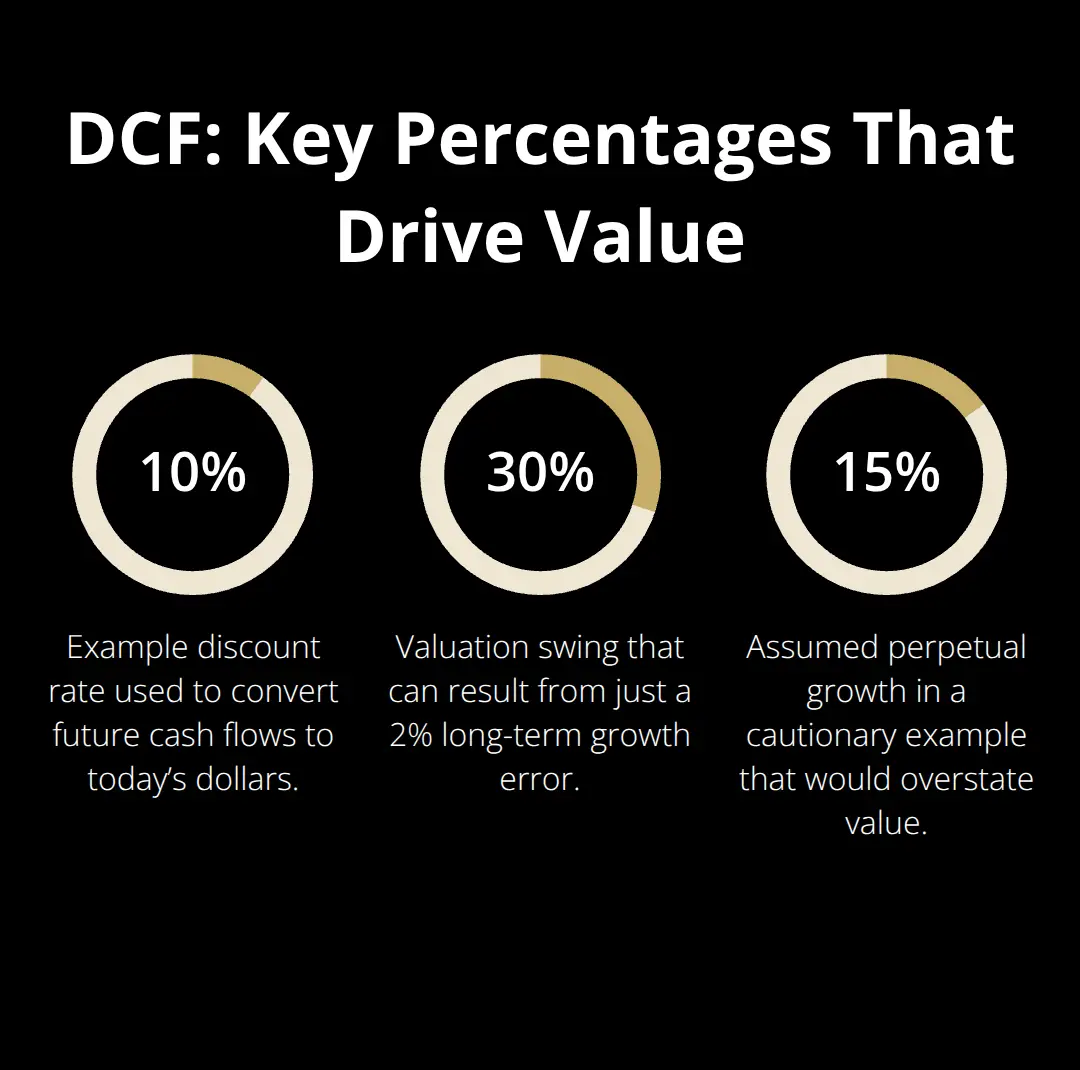

Discounted cash flow analysis projects your business’s future cash flows and discounts them back to today’s dollars using a rate that reflects your company’s risk profile. If your business generates $500,000 in annual free cash flow and you discount it at 10 percent, the present value over five years is roughly $1.9 million. The formula requires you to forecast revenue growth, operating margins, capital expenditures, and working capital needs for typically five to ten years, then assume a terminal growth rate for years beyond that. This method captures your specific business trajectory, not just industry averages. However, it demands accuracy you may not have. A 2 percent error in your long-term growth assumption can swing valuation by 30 percent or more. Most owners overestimate future growth because they’re optimistic about their prospects.

Buyers underestimate it because they’re skeptical. A realistic DCF requires three years of audited financial statements, a detailed understanding of your cost structure, and honest assumptions about market expansion. If your historical revenue growth is 8 percent annually and you assume 15 percent growth forever, your valuation is fiction. Use your actual track record as the foundation. A business that grew revenue 6 percent last year, 7 percent the year before, and 8 percent the year before that likely sustains 7 to 8 percent growth forward, not 12 percent. The discount rate-typically 8 to 12 percent for private businesses-accounts for risk and the time value of money. A riskier business or one with customer concentration requires a higher discount rate, which lowers valuation. A stable, diversified business with long-term contracts supports a lower rate, raising valuation. DCF works powerfully for mature businesses with predictable earnings, but it’s less reliable for early-stage companies or those in volatile markets where forecasting five years out is guesswork.

Revenue Multiples: The Quick Shortcut with Real Limitations

Revenue multiples value your business by multiplying total revenue by an industry-specific factor. A software-as-a-service company might sell for 3 to 5 times revenue; a service firm might sell for 0.5 to 1 times revenue. The appeal is simplicity: multiply your $2 million revenue by 2 times and you get a $4 million valuation. The danger is that revenue tells you almost nothing about profitability or cash generation. A business doing $5 million in revenue with 30 percent operating margins is worth far more than a business with $5 million in revenue and 5 percent margins. Revenue multiples work only when applied to comparable companies with similar cost structures and profitability profiles. They’re useful as a quick sanity check-if your EBITDA-based valuation is $3 million and your revenue is $4 million, that’s a 0.75 times revenue multiple, which is reasonable for a service business. If it calculates to 10 times revenue, something is wrong. Try revenue multiples as a reality test, not as your primary valuation method. They’re most reliable for recurring revenue models like SaaS, where customer lifetime value is predictable and churn rates are stable. Once you’ve calculated your business value using these three income-based approaches, you’ll have a range rather than a single number. The next step is to test that range against what comparable businesses actually sold for in your market.

Market-Based Valuation: What Comparable Businesses Sell For

Anchoring Price to Real Transactions

Market-based valuation cuts through guesswork by anchoring your business price to real transactions. Instead of projecting future cash flows or applying theoretical multiples, you find what similar businesses sold for recently and adjust for differences. This method works because actual buyers have already decided what they’ll pay, and their decisions reveal market reality far better than any formula. The challenge is accessing reliable data. Most private business sales happen quietly without public disclosure, which means you work with incomplete information. Databases like BizComps and Pratt’s Stats aggregate transaction data from thousands of private sales and provide multiples benchmarked by industry, revenue size, and profitability. These aren’t guesses-they’re actual prices paid for actual businesses.

Using Comparable Sales to Set Your Range

For a manufacturing firm with $2 million in EBITDA, Pratt’s Stats might show that comparable businesses sold for 5.2 times EBITDA over the past two years, with a range from 4.1 to 6.8 times depending on growth rate and customer concentration. That range becomes your starting point. A business with strong recurring revenue, diversified customers, and 10 percent annual growth sits at the higher end; one with customer concentration risk and flat growth sits lower. The recency of comparable sales matters enormously. A transaction from six months ago in your market tells you far more than one from three years ago, especially in industries experiencing rapid change. Public market comparables offer another angle. If you own a software company, you can examine recent acquisitions of similar SaaS firms and the multiples paid. Public M&A data from sources like Crunchbase or industry-specific trackers reveals what strategic buyers and private equity firms are willing to pay, though those prices often exceed what financial buyers pay for the same business type.

Adjusting Comparables for Your Business Differences

Adjusting for differences between your business and comparables is where most owners fail. Two software companies with identical $1 million revenue can sell for vastly different prices if one has 40 percent gross margins and the other has 70 percent. A service business with three major clients representing 60 percent of revenue trades at a steep discount to one with 50 clients where the largest represents 8 percent of revenue. Customer acquisition cost, retention rates, and the presence of long-term contracts all shift value. A business with annual contracts and 90 percent customer retention commands a premium; one with month-to-month customers and 50 percent annual churn does not. When you find a comparable sale, list the key differences: growth rate, profit margin, customer concentration, contract length, recurring versus one-time revenue. For each material difference, adjust the multiple up or down. If the comparable business grew 20 percent annually and yours grew 8 percent, apply a 20 to 30 percent discount to its multiple.

If the comparable has twice your customer concentration risk, discount further. This adjustment process is subjective, which is why triangulating across multiple valuation methods matters.

Validating Your Market-Based Valuation

Your asset-based value, income-based value, and market-based value should fall within the same ballpark. If your EBITDA multiple approach suggests $3 million but comparable sales suggest $5 million, that gap demands investigation. Either your business is undervalued relative to peers, or you’ve misidentified the right comparables. Real estate and equipment brokers have decades of transaction data and can validate whether your adjusted asset values match what buyers actually pay. Industry advisors, investment banks, and M&A firms have access to deal databases and recent transaction information that private owners cannot access independently. Their insight on current market multiples in your specific niche often reveals that online industry benchmarks are outdated or don’t account for regional differences. The market approach works best when you have multiple recent transactions to reference and when your business is reasonably similar to those comparables. For niche or highly specialized businesses, you may have limited comparables, which pushes more weight onto your income-based valuation.

Final Thoughts

You now have three proven methods to price your business realistically. Asset-based valuation grounds you in what you own, income-based valuation reveals what you actually earn, and market-based valuation anchors you to what buyers paid for similar businesses. The real power comes from combining all three, which produces a credible range rather than a single number that may mislead you.

Your business type determines which method carries the most weight. A manufacturing company with significant real estate and equipment leans heavily on adjusted asset value, while a software company with recurring revenue relies more on income-based multiples. Before you price your business for sale, get your financial house in order by preparing three years of audited or reviewed financial statements, separating personal expenses from business expenses, and documenting your customer contracts (especially long-term agreements that boost valuation by 20 to 40 percent).

Practical business valuation methods work only when grounded in accurate data and realistic assumptions. If you’re serious about selling, consider working with an advisor who has access to current market data and recent transaction information in your industry-we at Unbroker help business owners navigate the entire sale process with transparent pricing and access to a broad buyer network, and our valuation resources provide the foundation you need to move forward with confidence.