At Unbroker, we understand the challenges small business owners face when seeking financing.

Many entrepreneurs are looking for no collateral small business loans to fuel their growth without risking personal assets.

In this post, we’ll explore how to secure funding without collateral, discuss the types of unsecured loans available, and provide tips to improve your chances of approval.

What Are Unsecured Small Business Loans?

Definition and Mechanics

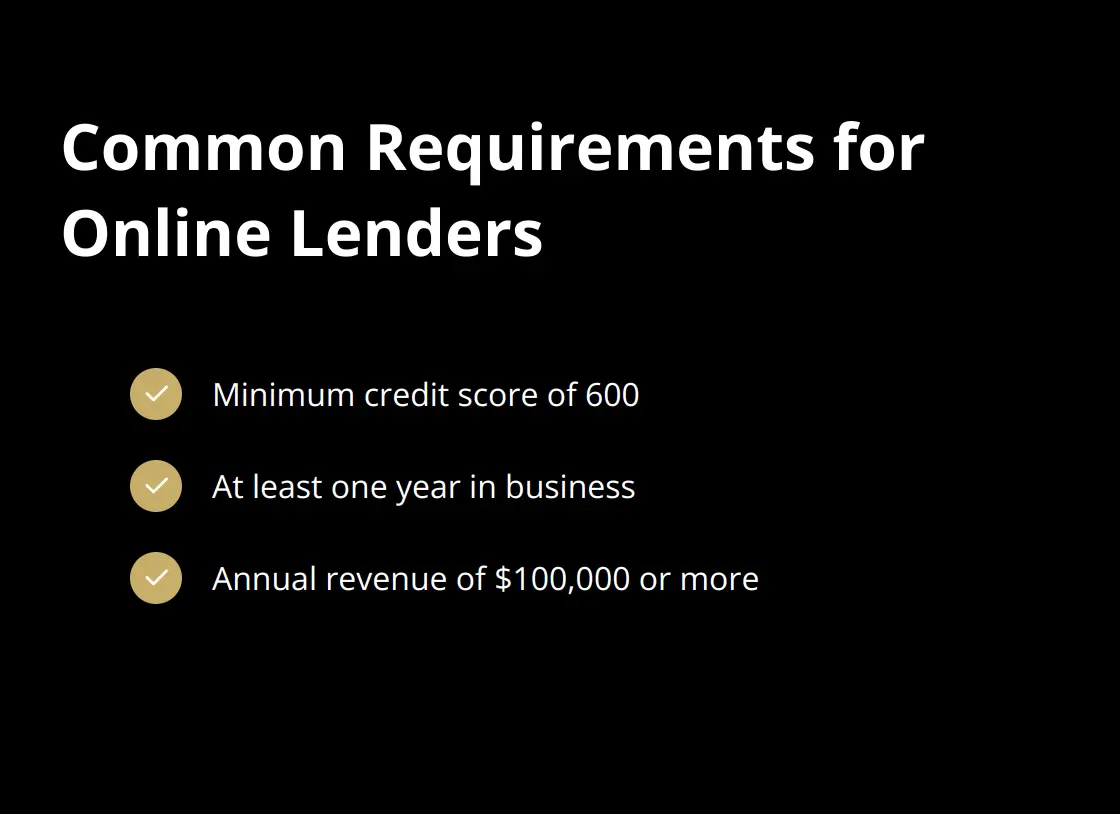

Unsecured business loans provide financial products that don’t require collateral. These loans rely on the borrower’s creditworthiness and business performance. Lenders evaluate factors such as credit scores, annual revenue, and time in business to determine eligibility. For example, online lenders often require a personal credit score above 700 FICO® Score, at least 2 years in business under existing ownership, and $100,000 or more in annual revenue.

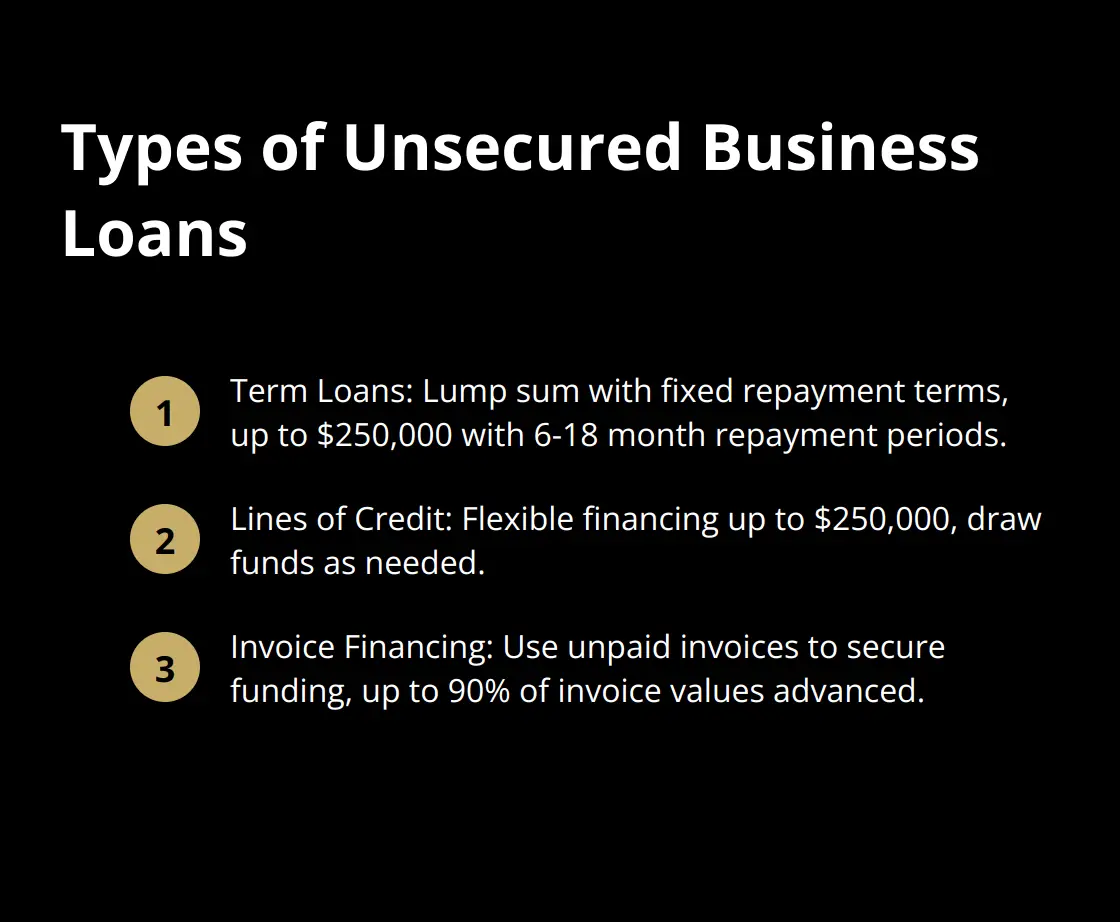

Types of Unsecured Business Loans

Small businesses can access various unsecured loan options:

Advantages and Disadvantages

Unsecured loans offer quick access to funds without risking assets, but they come with trade-offs. Interest rates are generally higher compared to secured loans backed by personal or business assets. Online lenders might charge APRs ranging from 10% to 99%, compared to traditional bank loans that average 3% to 7%.

The streamlined application process stands out as another advantage. Many online lenders provide decisions within minutes and fund approved loans within a day or two. However, loan amounts are often smaller than secured options (typically maxing out at $250,000 for most unsecured products).

Credit Implications

Unsecured loans can help build business credit if managed responsibly. Timely payments are reported to business credit bureaus, potentially improving your company’s credit profile. This can lead to better loan terms in the future.

However, defaulting on an unsecured loan can severely damage your business credit and may result in legal action. Some lenders require personal guarantees, meaning your personal assets could be at risk if the business fails to repay the loan.

As we move forward, it’s important to understand how to qualify for these collateral-free business loans. The next section will explore the specific requirements and factors that lenders consider when evaluating unsecured loan applications.

How to Qualify for Unsecured Business Loans

Improve Your Credit Score

Your personal and business credit scores significantly impact your eligibility for unsecured loans. Most lenders require a minimum personal credit above 700 FICO® Score, with some demanding 720 or higher for the best terms. To enhance your credit score:

- Pay all bills on time

- Keep credit utilization below 30%

- Dispute any errors on your credit report

For business credit, establish trade lines with suppliers and ensure they report to business credit bureaus (Dun & Bradstreet, Experian, and Equifax are the main ones).

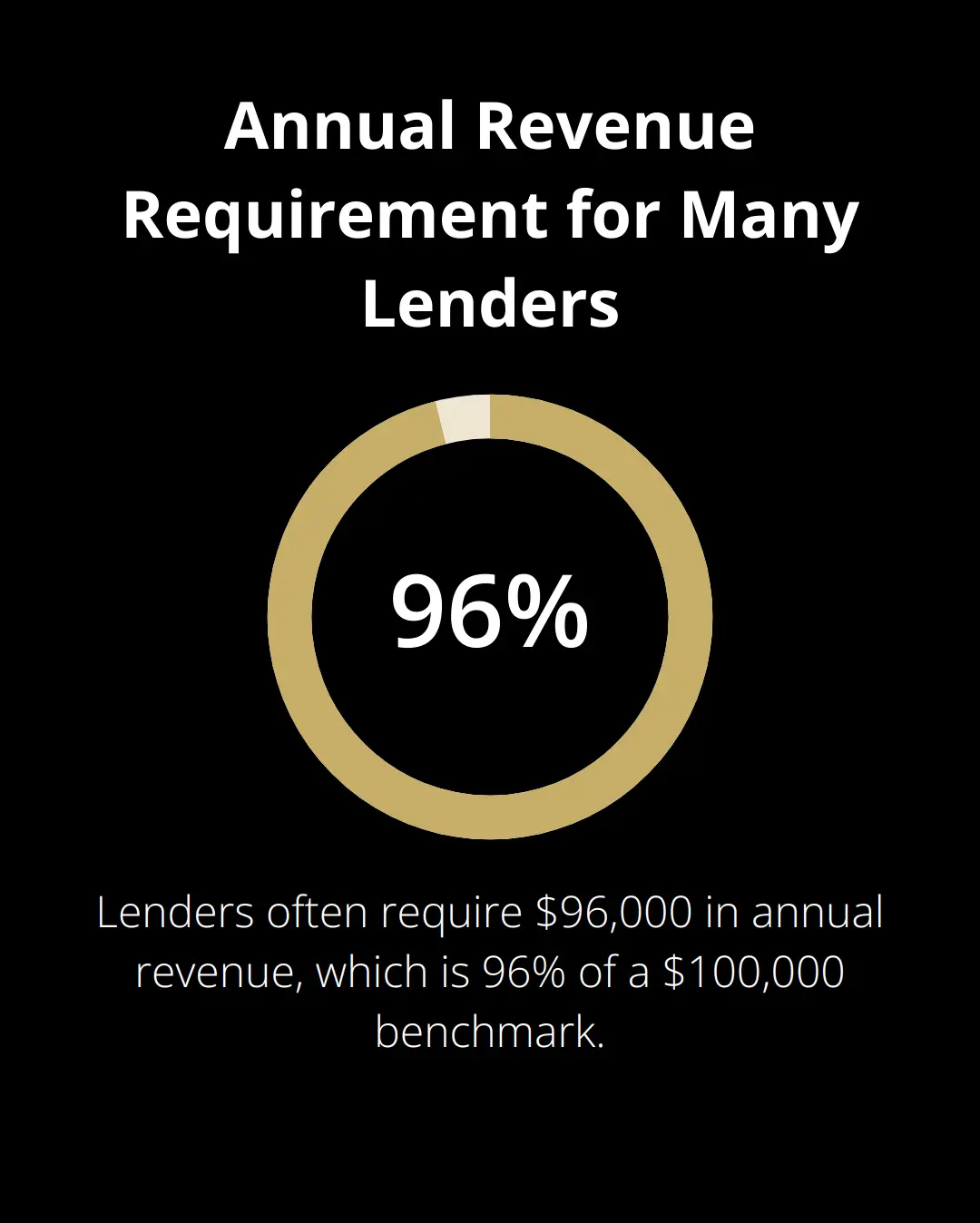

Show Strong Revenue and Longevity

Lenders want to see that your business generates consistent income. Many require at least $96,000 in annual revenue, with some setting the bar higher. Prepare detailed financial records, including:

- Profit and loss statements

- Cash flow projections

- Bank statements

Time in business also matters. Most lenders prefer companies that have operated for at least two years. Newer businesses might need to explore alternative lending options or focus on building a strong track record before applying.

Present a Solid Business Plan

A well-crafted business plan can significantly boost your chances of approval. Include:

- Detailed market analysis

- Clear financial projections

- Strategies for growth and risk mitigation

Your industry experience and qualifications can also sway lenders. Highlight any relevant certifications, awards, or successful past ventures in your loan application.

Understand Lender Criteria

Each lender has unique criteria. Some online lenders might offer more flexibility with credit scores but charge higher interest rates. Traditional banks often have stricter requirements but offer better terms. Shop around and compare offers to find the best fit for your business needs.

To qualify for a bank loan, you must demonstrate strong creditworthiness and business acumen. Most banks look for key factors such as a solid credit score, consistent revenue, and a well-prepared business plan.

The next section will explore the top sources for unsecured business loans and help you choose the right option for your company’s financial needs.

Where to Find Unsecured Small Business Loans

Online Lenders: Speed and Flexibility

Online lenders transform small business financing. Companies such as OnDeck provide unsecured loans for covering short-term costs, such as buying equipment or inventory, purchasing furniture and supplies, and paying utilities.

The application process takes less than 10 minutes to complete. Lenders make approval decisions within hours and deposit funds in as little as one business day. This convenience, however, comes at a price. Annual Percentage Rates (APRs) range from 10% to 99%, which exceed traditional bank loan rates.

Most online lenders require:

SBA Microloans: Government Support

The U.S. Small Business Administration (SBA) offers a microloan program that provides loans up to $50,000 to help small businesses and certain not-for-profit childcare centers start up and expand.

Nonprofit community-based organizations administer SBA microloans. Interest rates typically range from 8% to 13%, with maximum repayment terms of six years. Many microloan programs focus on the borrower’s character and ability to repay rather than collateral.

To apply, contact your local SBA district office or use the SBA’s Lender Match tool online. Prepare a detailed business plan, financial projections, and proof of your business management experience.

Alternative Financing Options

For businesses that struggle to qualify for traditional loans, alternative financing options provide quick access to capital without collateral requirements.

Invoice Factoring

Invoice factoring allows you to sell your unpaid invoices to a factoring company at a discount. Companies like BlueVine and Fundbox offer fast, revolving credit options for small businesses.

Merchant Cash Advances

Merchant cash advances provide a lump sum in exchange for a portion of your future credit card sales. They offer quick funding without collateral, but the costs can be high. Effective APRs can exceed 100% in some cases.

Both these options have easier qualification requirements than traditional loans, but they come with higher costs and potential risks to your cash flow. Review the terms carefully and consider the impact on your business before you proceed.

Unbroker: A Modern Alternative for Business Sellers

While not a direct lender, Unbroker offers a modern platform for selling businesses with transparent, low-cost options. This eliminates high brokerage fees and provides an alternative path to accessing capital through business sale. Unbroker’s services include Full Service Business Sale and Assisted Business Sale, both designed to support business owners in their exit strategies.

Final Thoughts

No collateral small business loans offer entrepreneurs a path to growth without risking personal assets. Lenders evaluate credit scores, revenue, and business plans when considering applications. Online lenders provide quick approvals, while SBA microloans and alternative financing methods like invoice factoring present additional options.

The right financing choice depends on your specific business needs and financial situation. Online lenders might offer faster funding at higher interest rates, while traditional bank loans or SBA programs could provide better terms for those who meet stricter criteria. Always compare multiple offers and read the fine print before you commit to any loan agreement.

For business owners considering an exit strategy, Unbroker provides a modern platform for selling businesses. This approach eliminates high brokerage fees and offers an alternative path to accessing capital. You can secure the funding necessary to elevate your small business without putting up collateral if you understand your options and prepare thoroughly.