At Unbroker, we understand the challenges of selling a business due to aging parents. It’s a decision that requires careful planning and consideration.

This guide will walk you through the process of exiting your business while preparing to care for your parents. We’ll cover everything from assessing your exit options to creating a financial plan for long-term care expenses.

What Are Your Business Exit Options?

Selling Your Business Outright

Liquidation provides a quick exit and cash to pay off debts. This exit strategy is typically used by failing businesses, or companies with significant assets. Owner readiness depends on a planning process that should start as soon as the owner purchases or starts the business. However, selling a business requires time and preparation. Start the process at least 18 months before your intended exit date. This timeline allows for thorough operational and financial assessment, which can significantly increase your business’s value.

To maximize your sale price, strengthen your financial records and ensure a competent management team is in place. These factors make your business more attractive to potential buyers. The success of your exit can greatly impact your ability to fund your parents’ care, so try to achieve the highest possible valuation.

Transitioning to a Family Member or Employee

Passing your business to a family member or trusted employee can preserve your legacy while providing continuity for clients and staff. This option often appeals to owners who want to keep the business “in the family.” However, it requires careful planning to avoid conflicts and ensure the successor’s ability to lead.

If you consider this route, start succession planning now. Follow these 7 essential steps to create a strong succession plan that ensures leadership continuity, minimizes risk, and supports long-term business success. Involve them in key decisions, introduce them to important clients, and gradually hand over responsibilities. This transition period not only prepares them for leadership but also reassures stakeholders about the business’s future stability.

Hiring a Management Team

If you want to step back from daily operations but retain ownership, hiring a professional management team could be the answer. This option allows you to focus on caregiving while still benefiting from the business’s income.

To make this work, invest time in finding and training the right team. Look for individuals with a track record of success in your industry. Be prepared to offer competitive compensation packages, possibly including performance-based incentives or equity stakes to align their interests with the business’s success.

Liquidating Assets and Closing Down

While not always the first choice, liquidation can be a viable option if other exit strategies aren’t feasible. This approach involves selling off business assets and closing operations. It’s typically the fastest way to exit, but it may not maximize the value of your business.

If you consider liquidation, consult with financial advisors to understand the tax implications. Plan the process carefully to ensure you meet all legal obligations and maximize the value of your assets.

Whichever exit strategy you choose, professional guidance proves invaluable. Accountants, attorneys, and financial advisors can help navigate complex issues and optimize your exit for both financial gain and peace of mind as you transition into your caregiving role. With your exit strategy in place, it’s time to turn your attention to planning for your parents’ care needs.

How to Plan for Your Parents’ Care

Assess Current Health and Future Needs

Start an open conversation with your parents about their health and care preferences. Schedule appointments with their primary care physician and specialists to obtain a clear picture of their current health status and potential future needs. This medical assessment will guide your care planning decisions.

According to the Family Caregiver Alliance, 60% of caregivers providing 21 or more hours of care per week feel a sense of obligation. This sense of obligation is even higher for live-in caregivers at 64%. Understanding the level of care your parents might need will help you prepare for the time commitment involved.

Explore Care Options

Research various care options to find the best fit for your parents’ needs and preferences. In-home care allows seniors to age in place, maintaining their independence while receiving necessary support. Assisted living facilities offer a balance of independence and care, while nursing homes provide round-the-clock medical attention for those with complex health needs.

A new AARP survey finds that adults don’t think their homes and communities will be able to support them as they get older. However, it’s essential to weigh this preference against safety and care requirements.

Calculate Long-Term Care Costs

Long-term care can be expensive, with costs varying widely depending on the level of care and location. According to Genworth’s 2021 Cost of Care Survey, the national median cost for a private room in a nursing home is $9,034 per month, while assisted living facilities average $4,500 monthly.

Factor in potential increases in care costs over time. The Genworth survey indicates that nursing home costs have increased by 3.3% annually over the past five years.

Develop a Financial Strategy

Create a comprehensive financial plan to cover ongoing care expenses. Review your parents’ assets, income sources, and insurance policies. Long-term care insurance can be a valuable resource if your parents have a policy in place.

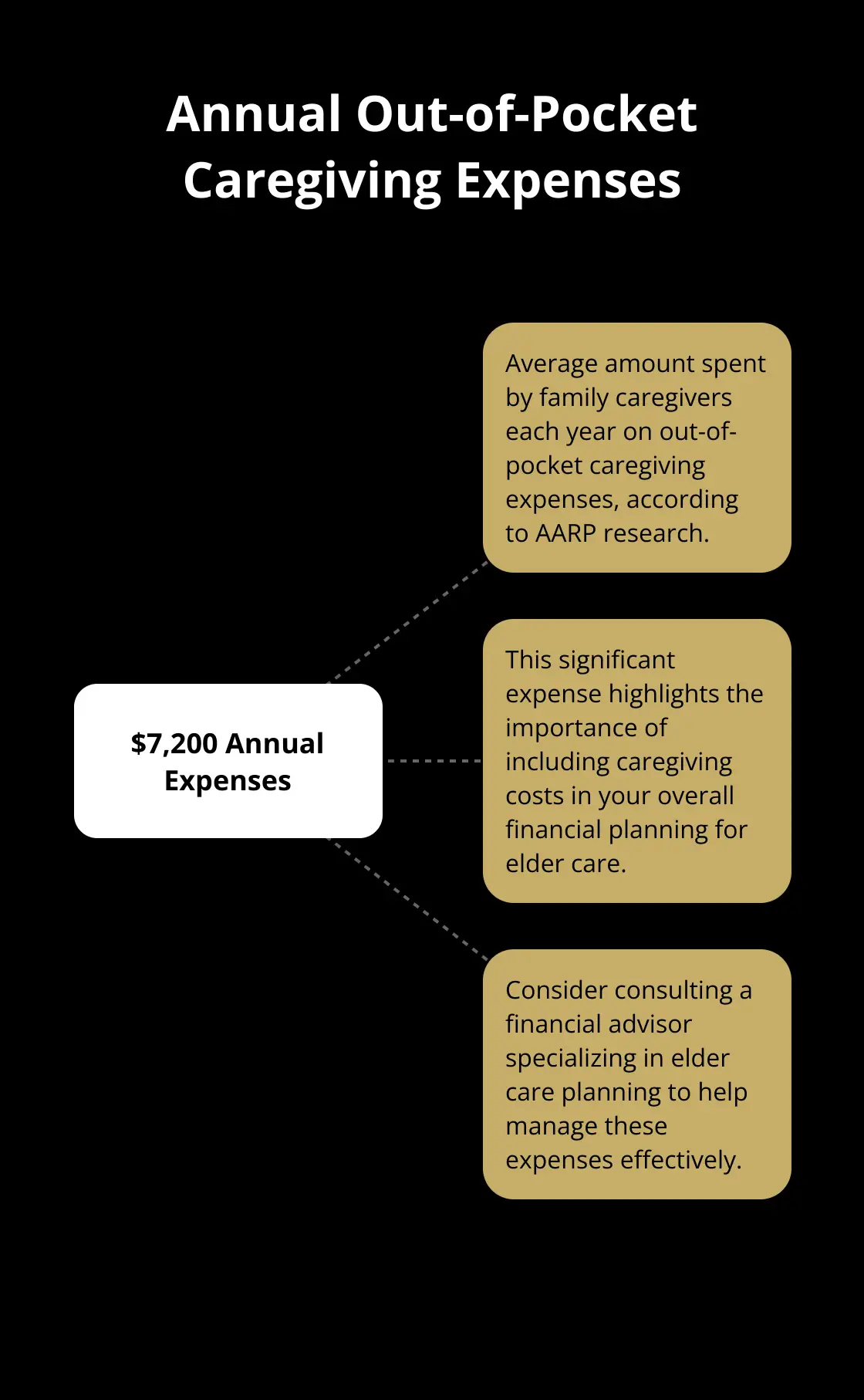

Consider consulting a financial advisor specializing in elder care planning. They can help you explore options like reverse mortgages, life insurance conversions, or Medicaid planning to fund long-term care.

The financial implications of caregiving can be significant. AARP research shows that the average family caregiver spends around $7,200 per year out of pocket on caregiving expenses, which you should include in your financial planning.

Implement Legal and Administrative Measures

Ensure that all necessary legal documents are in place. These may include power of attorney (for both healthcare and finances), advance directives, and a living will. These documents will allow you to make important decisions on behalf of your parents if they become unable to do so themselves.

Additionally, organize important documents such as insurance policies, bank statements, and medical records. Having these readily accessible will streamline the caregiving process and reduce stress during emergencies.

With a solid care plan in place for your parents, you can now turn your attention to the challenging task of balancing your business exit with your new caregiving responsibilities.

How to Balance Business Exit and Caregiving Responsibilities

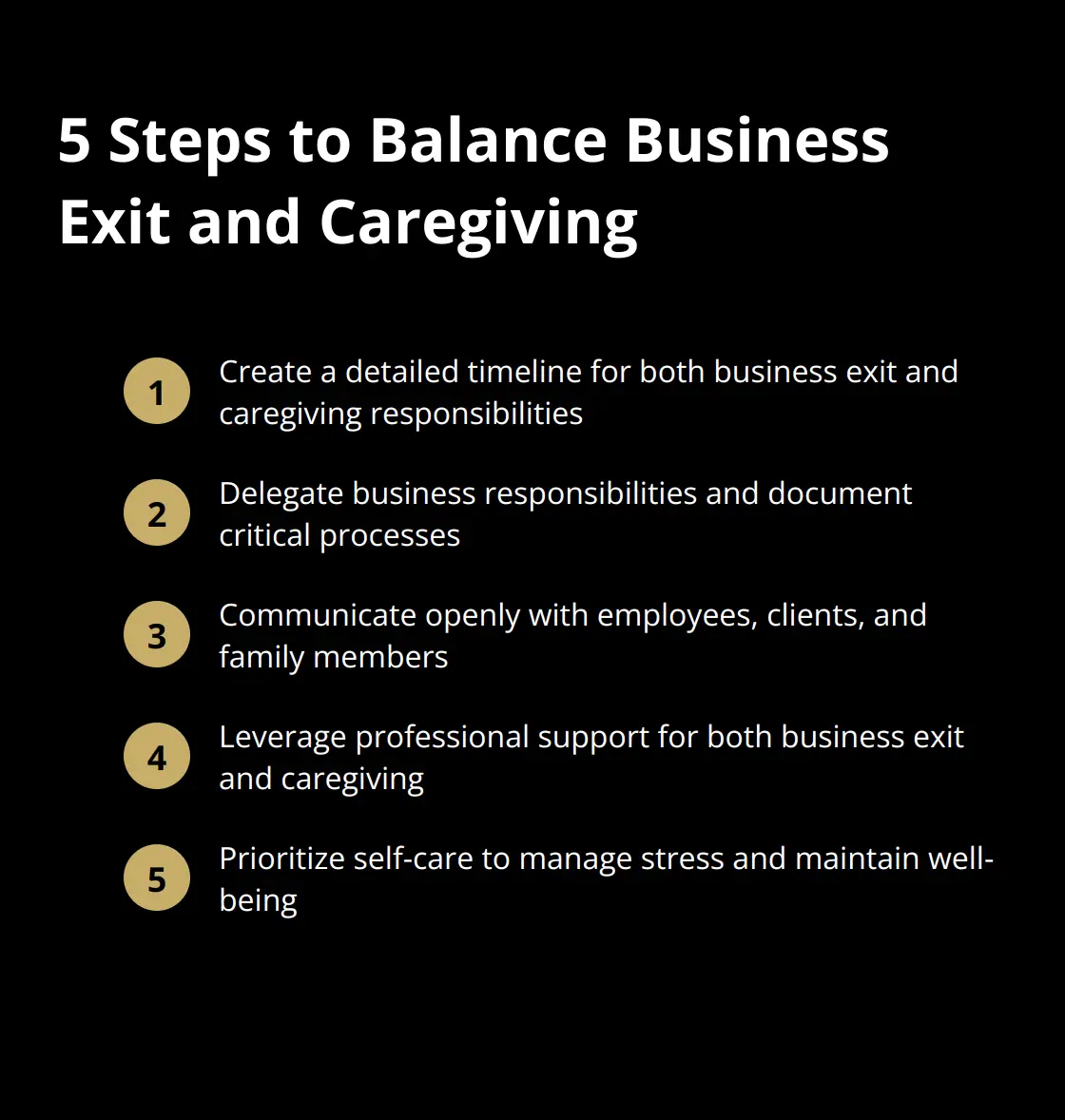

Create a Detailed Timeline

Map out a realistic timeline for your business exit. Most exit strategies require at least 18 months to execute properly. Break this timeline into manageable phases, each with specific goals and deadlines. You might allocate three months for financial audits, six months for identifying potential buyers, and another six months for negotiations and due diligence.

Outline your caregiving timeline simultaneously. Anticipate when you need to step into a more active caregiving role. Align this with your business exit timeline. Prepare to adjust both timelines as circumstances change.

Delegate and Document

Prepare to step away from your business by delegating responsibilities and documenting processes. Identify key employees who can take on additional roles. Invest in training these individuals to ensure they handle increased responsibilities.

Document all critical business processes (from daily operations to client relationships). This documentation helps your team maintain consistency in your absence and increases your business’s value to potential buyers.

This guide offers practical strategies for business owners facing this complex situation, exploring how to plan your exit and prepare your business.

Communicate Openly and Frequently

Open communication proves vital during this transition period. Be transparent with your employees about your plans to exit the business. Provide a general timeline and reassurances about the company’s future to help maintain morale and productivity.

Keep your clients and stakeholders informed as well. Reassure them about the continuity of service and introduce them to key team members who will be their primary contacts moving forward.

In your role as a caregiver, maintain open lines of communication with your parents and other family members. Regular family meetings can help ensure everyone understands care plans and responsibilities.

Leverage Professional Support

Don’t manage everything on your own. Engage professional support both for your business exit and your caregiving responsibilities.

For your business, consider hiring a transition manager or working with a company to guide you through the exit process. These professionals can handle many time-consuming aspects of selling a business, freeing you up to focus on caregiving.

On the caregiving front, explore professional care options. Even if you plan to be the primary caregiver, professional support can provide much-needed respite and ensure your parents receive comprehensive care.

Prioritize Self-Care

Balancing a business exit with new caregiving responsibilities can be overwhelming. Try to prioritize your own well-being during this transition. Schedule regular breaks, maintain a healthy diet, and get adequate sleep. Consider joining a support group for caregivers or seeking counseling to manage stress.

Final Thoughts

Selling a business due to aging parents requires careful planning and strategic decision-making. Start your exit planning at least 18 months before your intended departure to allow for comprehensive business valuation and smooth handovers. Maintain transparent communication with your employees, clients, and family members throughout the process.

Professional guidance can provide invaluable support in both your business exit and caregiving responsibilities. Financial advisors, elder care specialists, and legal professionals can offer expert insights to optimize your decisions. Don’t hesitate to seek help when needed.

Unbroker offers transparent, cost-effective solutions for business owners looking to exit their companies. Our platform can handle the complexities of your business sale while you focus on caring for your aging parents. With proper planning and support, you can successfully transition into your new role while ensuring the best outcome for your business and your parents’ well-being.