Selling a business is challenging, but doing so while facing legal troubles adds layers of complexity. At Unbroker, we’ve seen entrepreneurs grapple with the question of how to sell a business while incarcerated or dealing with legal issues.

This guide explores the legal implications, strategies, and value protection measures for business owners in this difficult situation. We’ll provide practical advice to help you navigate this complex process and achieve the best possible outcome.

Legal Hurdles When Selling a Business

The Value Impact of Legal Issues

Legal troubles can significantly reduce a business’s market value. Buyers often hesitate to inherit potential liabilities, which leads to lower offers or deters potential purchasers. The American Bar Association reports that since the development of laws addressing children and youth, the specific needs of homeless youth have rarely been taken into account.

To minimize this value loss, you must understand your business’s worth clearly. Hire a professional business appraiser to provide an objective valuation, considering the potential financial impact of your legal situation. This information will prove invaluable during negotiations and help set realistic expectations for the sale.

Transparency and Disclosure Requirements

When you sell a business, full disclosure of legal issues is not just ethical-it’s a legal requirement. If you fail to disclose pending lawsuits, investigations, or other legal matters, you risk severe consequences (including the buyer’s right to rescind the sale or sue for damages).

The Securities and Exchange Commission (SEC) requires that companies disclose certain information, including financial statements, business risks and prospects, and a description of the stock to be offered. Transparency builds trust and can actually improve your negotiating position by demonstrating honesty and integrity.

Navigating Buyer Interest and Negotiations

Legal troubles inevitably complicate negotiations. Buyers may request additional due diligence, extended escrow periods, or indemnification clauses to protect themselves. You should prepare for these requests and consider engaging a skilled attorney to help navigate these complex negotiations.

Despite these challenges, you can employ strategies to maintain buyer interest. Focus on highlighting the strengths of your business that exist independently of the legal issues. Emphasize strong cash flow, a loyal customer base, or unique market positioning. If possible, demonstrate how you actively address and resolve the legal issues.

Mitigating Risks for Potential Buyers

To attract serious buyers despite legal challenges, you must take steps to mitigate their perceived risks. Consider the following strategies:

- Offer detailed documentation: Provide comprehensive records of all legal proceedings, including any resolutions or ongoing negotiations.

- Create a contingency fund: Set aside a portion of the sale proceeds to cover potential legal costs or settlements. A financial contingency plan should document your course of action in times of crisis that threaten the stability of your company.

- Propose creative deal structures: Explore options like earn-outs or seller financing to align your interests with the buyer’s and demonstrate your confidence in the business’s future.

- Engage in pre-emptive problem-solving: Address any issues that you can resolve quickly to show proactive management of the situation.

While legal issues complicate a business sale, they don’t make it impossible. With the right approach and professional guidance, you can successfully navigate these challenges and achieve a favorable outcome in your business sale. As you prepare to tackle these legal hurdles, let’s explore specific strategies for selling your business despite ongoing legal challenges.

Navigating Legal Challenges When Selling Your Business

Timing Considerations

Selling a business while facing legal issues requires careful timing. If your legal issues are minor and will resolve quickly, you should wait. This approach can help you avoid selling at a discount and preserve your business’s value.

However, if you face serious charges or prolonged legal battles, you should sell sooner. In such cases, quick action can help you preserve more of your business’s worth.

Assembling Your Professional Team

Don’t attempt to navigate this complex process alone. You should assemble a team of professionals who can guide you:

- Business Attorney: Seek one with experience in both business sales and your specific legal issues. They can structure the sale to protect you from future liability.

- Accountant: They will ensure your financials are in order and help you understand the tax implications of the sale.

- Business Broker: Choose one with experience in distressed sales. They can find buyers who are comfortable with some level of risk.

- Valuation Expert: They will give you a realistic picture of your business’s worth, considering the legal challenges.

Creating a Contingency Plan

You should develop a detailed contingency plan that outlines how you’ll handle various legal outcomes. This plan should cover:

- Worst-case scenarios: What happens if you’re convicted or face significant fines?

- Best-case scenarios: How will you proceed if charges are dropped or you’re acquitted?

- Middle-ground outcomes: What if you face probation or lesser charges?

For each scenario, outline how it would affect the sale process, price, and terms. This level of preparation can impress potential buyers and give them confidence in the transaction.

Strategic Disclosure

Transparency is essential, but so is strategy. You should disclose legal issues to serious buyers at the right time – typically after they’ve shown genuine interest but before they invest significant time in due diligence.

When you disclose, frame the information carefully. Focus on how you’re addressing the issues and mitigating risks. If possible, have your attorney present during these discussions to answer technical questions. Ensure you have a non-disclosure agreement in place before providing any information to a prospective buyer.

Your goal is to show that while there are challenges, they’re manageable and don’t fundamentally undermine the value of your business.

These strategies can help you navigate the complex process of selling your business despite legal challenges. It won’t be easy, but with the right approach and team, you can achieve a successful sale. Now, let’s explore how to protect your business value during legal proceedings.

How to Protect Your Business Value During Legal Troubles

Maintain Operational Excellence

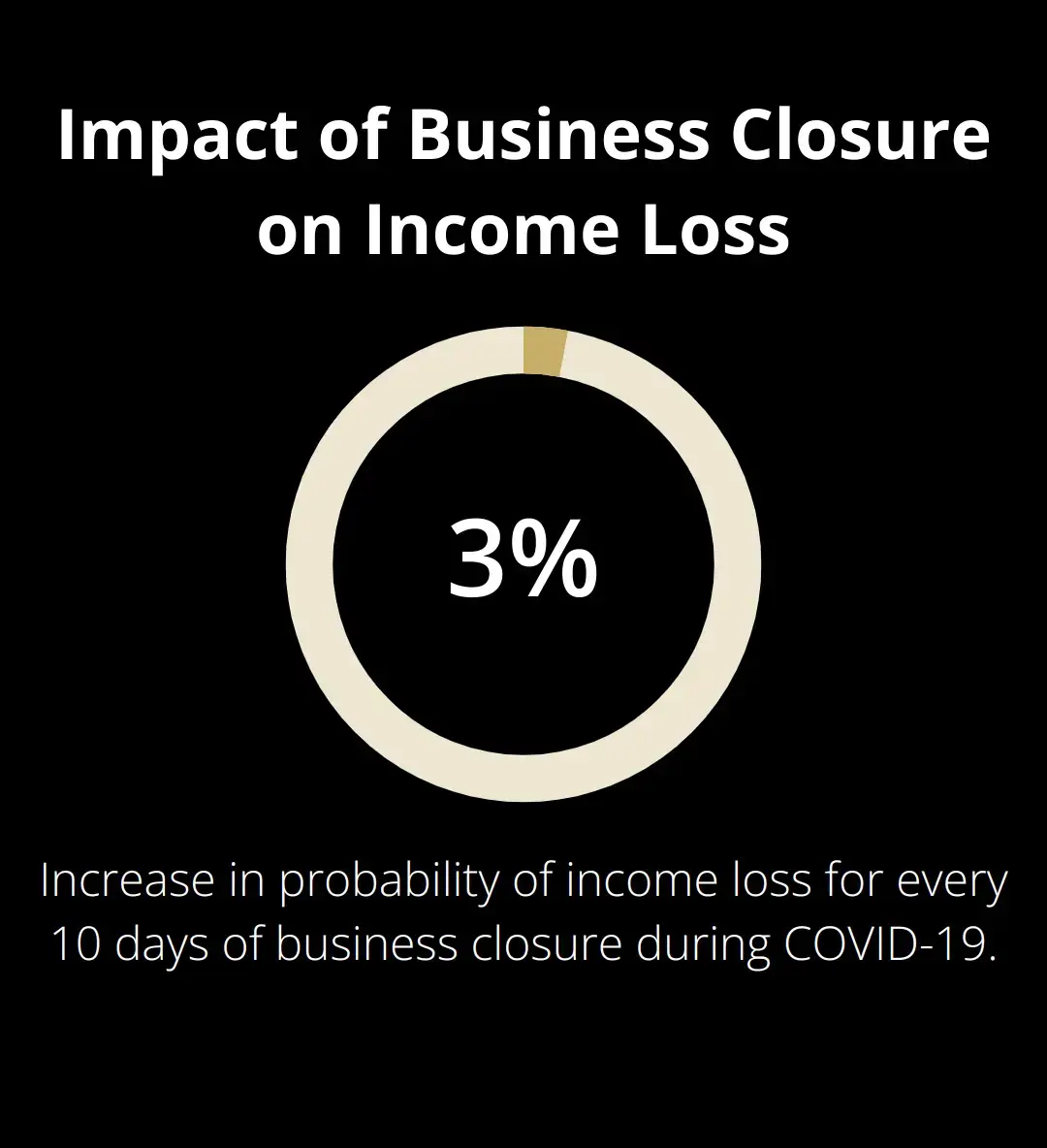

The protection of your business value starts with the continuation of smooth operations. This requires a laser focus on core business activities, even as legal issues loom. A study suggests that for every ten days of business closure during the COVID-19 shutdown, the probability of the business having income loss increased by 3%.

To achieve this, you must delegate responsibilities effectively. Identify key team members who can assume additional roles to keep the business running smoothly. You should implement robust systems and processes that can operate with minimal oversight. This approach not only maintains business performance but also proves to potential buyers that the company can thrive independently of its current owner.

Address Reputational Challenges

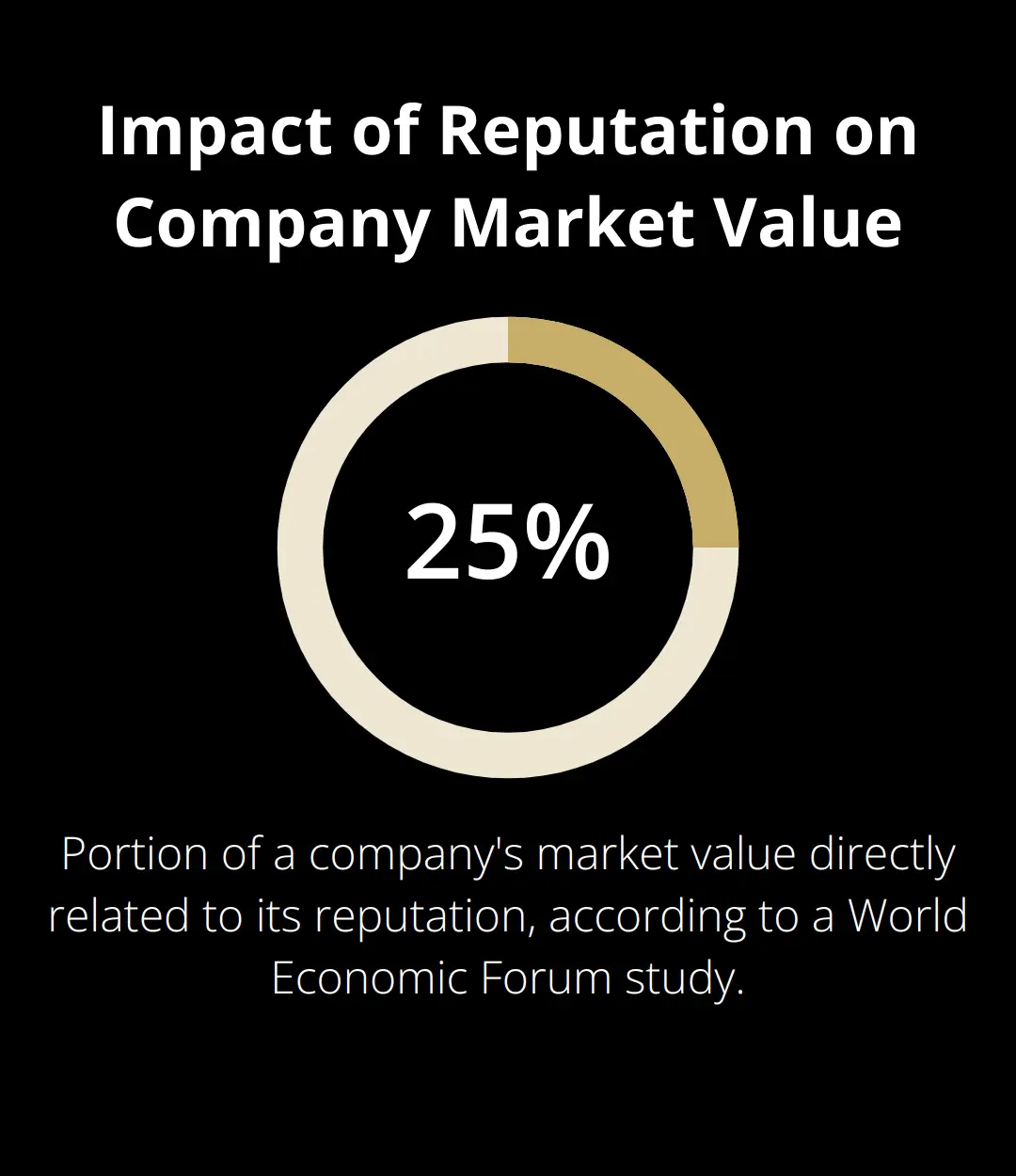

Legal troubles often result in reputational damage, which can significantly impact your business value. A study by the World Economic Forum suggests that more than 25% of a company’s market value directly relates to its reputation. To tackle this issue:

- Create a crisis communication plan. Prepare to respond quickly and transparently to stakeholders (including employees, customers, and suppliers).

- Manage your reputation proactively. Monitor online reviews and social media mentions. Respond promptly and professionally to negative feedback.

- Highlight your company’s positive contributions. Showcase community involvement, charitable work, or industry leadership to offset negative perceptions.

- Consider professional help. Reputation management firms can craft and execute a strategy to mitigate reputational damage.

Implement Risk Mitigation Strategies

The protection of your business value also involves the minimization of future risks. You should implement strategies that address current legal issues and prevent future problems. This approach can reassure potential buyers about the long-term viability of your business.

Start with a comprehensive risk assessment. Identify areas of vulnerability in your business operations, compliance procedures, and corporate governance. Once you pinpoint these risks, develop and implement mitigation strategies.

For example, if your legal troubles stem from compliance issues, invest in a robust compliance program. The U.S. Department of Justice describes specific factors that prosecutors should consider in conducting investigations of corporations, including the existence and effectiveness of the corporation’s pre-existing compliance program.

If your challenges relate to product liability, consider the enhancement of quality control measures or the restructuring of your warranty program. These steps not only address current issues but also demonstrate to potential buyers that you take concrete action to protect the business’s future value.

Seek Professional Guidance

The navigation of legal troubles while protecting business value often requires expert assistance. You should consult with legal professionals who specialize in business law and have experience with situations similar to yours. They can provide invaluable advice on how to structure your business operations and transactions to minimize legal exposure.

Additionally, financial advisors can help you understand the potential fiscal implications of your legal situation and develop strategies to protect your assets. They may suggest restructuring options or ways to separate personal and business finances to limit liability.

Maintain Transparent Communication

Open and honest communication with stakeholders (employees, clients, and partners) is essential during legal challenges. You should provide regular updates about the situation without divulging sensitive information that could compromise your legal position. This transparency can help maintain confidentiality during the sale process and preserve business value.

Final Thoughts

Selling a business while facing legal challenges requires careful planning and expert guidance. You must maintain open communication with potential buyers and stakeholders throughout this process. Proactive addressing of legal issues and implementation of risk mitigation strategies will protect your business value and increase the likelihood of a successful sale.

Timing plays a crucial role when you decide to sell your business amid legal troubles. You should assemble a team of professionals (including attorneys, accountants, and business brokers) to navigate the intricacies of your situation. Their expertise will prove invaluable in structuring the sale, managing negotiations, and ensuring compliance with all legal requirements.

At Unbroker, we understand the unique challenges of selling a business under difficult circumstances, including how to sell a business while incarcerated. Our modern platform offers transparent, low-cost options for business sellers, eliminating high brokerage fees while providing expert support throughout the sale process. You can navigate this complex journey successfully by balancing legal challenges with your business sale goals.