Business valuations have spiraled into dangerous territory. Sellers are being quoted prices that bear little resemblance to what buyers will actually pay, and at Unbroker, we’re seeing the fallout firsthand.

Valuation inflation isn’t just a pricing problem-it’s creating a market where deals collapse, expectations shatter, and both buyers and sellers lose money. This post breaks down what’s really happening and why getting your valuation right matters more than ever.

Where Are Valuations Actually Coming From

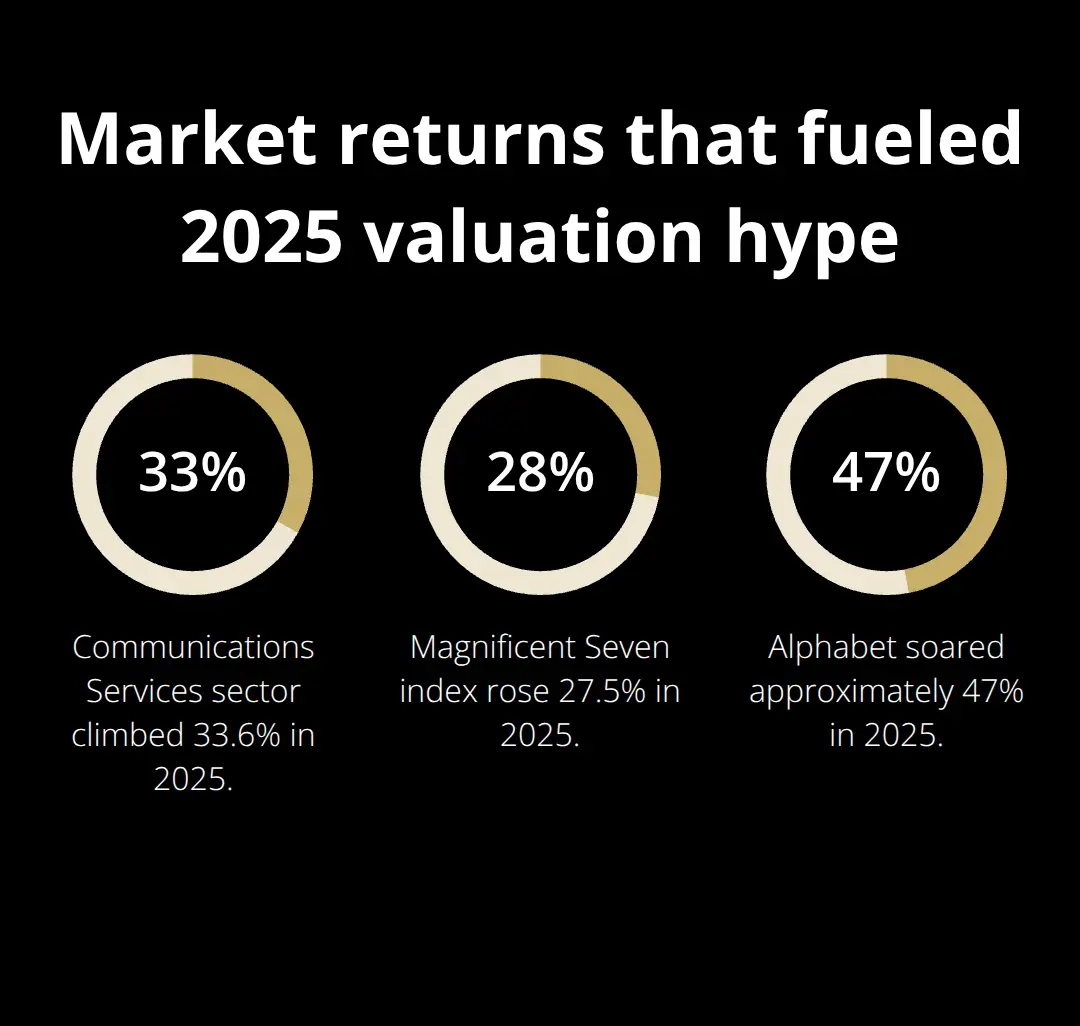

The gap between what sellers hear and what deals actually close at has widened dramatically. In 2025, we’re watching businesses get valued at revenue multiples that would have seemed absurd just three years ago. A software company generating $2 million in annual revenue might receive a quote at 8 to 10 times revenue, translating to a $16 to $20 million asking price. Meanwhile, actual buyer interest sits at 4 to 5 times revenue-a $8 to $10 million realistic valuation. This gap isn’t minor; it’s the difference between a deal that closes and expectations that lead nowhere. The Communications Services sector climbed 33.6 percent in 2025, driven largely by AI exposure and digital media hype. That sector performance gets baked into valuations for any business remotely connected to those narratives, regardless of the company’s actual competitive position or growth trajectory.

How AI Narratives Inflate Multiples

The moment a business owner mentions AI capabilities-whether the company genuinely uses machine learning or simply talks about future AI potential-valuators and brokers adjust multiples upward. We’ve seen companies with modest profit margins suddenly valued as if they’re on the cusp of 50 percent annual growth. The Magnificent Seven index rose 27.5 percent in 2025 with Alphabet soaring approximately 47 percent. That performance creates a halo effect where any business touching technology or data receives premium treatment in valuation models.

Growth stocks in the Russell 1000 Growth index underperformed value in 2025, with the Growth index declining 0.6% while value rose 0.7%. This performance gap incentivizes brokers and advisors to push valuations higher because it aligns with what’s working in public markets. The problem surfaces when a private business owner tries to actually sell-buyers don’t apply the same multiples that worked for mega-cap tech companies.

Private Equity’s Distorting Effect on Price

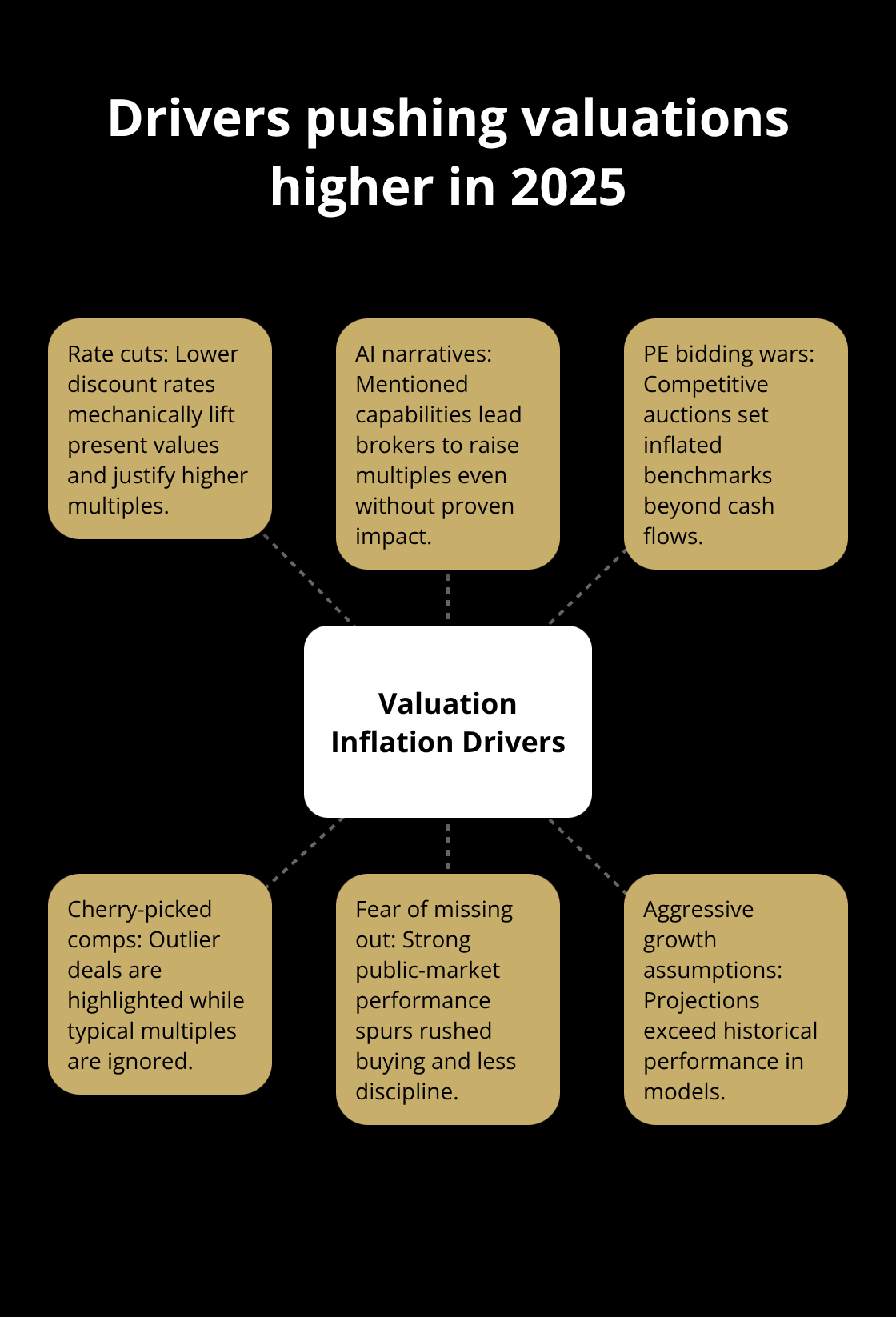

Competitive bidding among private equity firms creates artificial price inflation that ripples through the entire M&A market. When three PE firms compete for a single acquisition target, they drive prices upward beyond what underlying cash flows justify. The winner often overpays to secure the deal, and that inflated price becomes the new benchmark for comparable transactions. Sellers and brokers cite these highest-bidder deals as market evidence, even though most transactions don’t involve PE competition. A manufacturing company selling to a strategic buyer at a reasonable multiple gets ignored in favor of highlighting the one PE-backed outlier that paid a premium. This selective use of comparables artificially inflates valuation expectations across entire industries. Realistic sellers need to distinguish between transactions driven by PE bidding wars and actual market-clearing prices. The median business doesn’t attract PE interest, which means applying PE-level multiples to a typical operation guarantees disappointment when the business hits the open market.

Why Comparable Sales Mislead Most Owners

Brokers and valuators rely on comparable sales to justify asking prices, but they often cherry-pick the highest transactions while ignoring the broader market reality. A deal that closed at 7 times EBITDA gets highlighted prominently, while five other deals that closed at 4 to 5 times EBITDA disappear from the narrative. This selective presentation creates a false sense of what the market will actually pay. When you’re preparing to sell, you need to see the full distribution of recent sales in your industry-not just the outliers that support inflated expectations. The businesses that attract PE bidding wars or strategic buyers with specific synergies represent a tiny fraction of all transactions. Most owners sell to financial buyers or smaller strategic acquirers who apply more conservative multiples based on proven cash flow and risk assessment. Understanding this distinction separates owners who price realistically from those who watch their businesses sit on the market unsold while they wait for offers that never materialize.

What’s Actually Fueling Higher Valuations Right Now

The Federal Reserve’s rate cuts throughout 2025 fundamentally changed how buyers approach valuations. When discount rates fall, future cash flows become worth more in today’s dollars, which mathematically justifies higher multiples. A business that generates $500,000 in annual EBITDA valued at 6 times that multiple commands $3 million. Drop the discount rate from 12 percent to 8 percent, and suddenly the same cash flow supports a 7.5 to 8 times multiple, pushing the valuation to $3.75 to $4 million without any change to actual business performance. This isn’t speculation-it’s mechanical. Buyers and sellers both feel emboldened to pay more because the financing environment rewards it.

But here’s where reality diverges from math: those lower rates won’t persist forever. Buyers who locked in deals at inflated multiples during this window will regret it when refinancing costs spike. The S&P 500 climbed 25 percent in 2024 and another 16.39 percent in 2025, creating a psychological environment where sitting on cash feels dangerous. That performance gap pushes investors and PE firms toward acquisition activity-they need to deploy capital before missing out entirely.

Fear-Driven Buying Removes Price Discipline

This urgency strips price discipline from negotiations. Sellers sense the competitive tension and anchor their asking prices higher, knowing that multiple buyers might actually close the gap. The problem accelerates when several buyers perceive the same opportunity, triggering bidding wars that have nothing to do with the business’s intrinsic worth and everything to do with relative valuation anxiety across the market. Competitive tension among PE firms creates artificial price inflation that ripples through the entire M&A landscape. When three PE firms compete for a single acquisition target, they drive prices upward beyond what underlying cash flows justify. The winner often overpays to secure the deal, and that inflated price becomes the new benchmark for comparable transactions.

Inflated Growth Assumptions Drive Unrealistic Valuations

Valuation models now routinely assume revenue growth rates that exceed what the business has historically delivered. A company with five years of 8 percent annual growth receives a valuation that assumes 15 percent growth for the next decade. The justification centers on AI integration, new market expansion, or operational efficiencies that remain theoretical. Professionals who conduct these valuations have financial incentive to justify higher multiples-higher valuations mean higher listing prices, which attract more sellers to their services.

The disconnect surfaces immediately after purchase. A buyer acquires the business expecting that 15 percent growth trajectory, implements the promised improvements, and discovers the market won’t support it. The company grows at 9 percent instead. That variance sounds minor until you calculate the impact: a business worth $5 million based on 15 percent growth assumptions might only be worth $3.2 million based on 9 percent actual results. The buyer overpaid by $1.8 million, and the seller has already cashed the check.

Conservative Buyers Apply Discounts to Unproven Claims

This pattern repeats across industries. Valuations built on projected growth rather than demonstrated performance create deals that feel right in the moment but generate buyer remorse within eighteen months. The realistic approach requires separating what a business has proven it can do from what management claims it might accomplish. Conservative buyers apply a 3 to 5 percent discount to any growth assumption that lacks supporting historical data. Sellers who insist their business will suddenly accelerate growth after sale watch their valuations compress when they encounter actual buyers willing to pay based on evidence rather than narratives.

The gap between what sellers hear and what deals actually close at has widened dramatically because valuation inflation has become systemic. Sellers receive quotes at revenue multiples that would have seemed absurd just three years ago. A software company generating $2 million in annual revenue might receive a quote at 8 to 10 times revenue, translating to a $16 to $20 million asking price. Meanwhile, actual buyer interest sits at 4 to 5 times revenue-a $8 to $10 million realistic valuation. This gap isn’t minor; it’s the difference between a deal that closes and expectations that lead nowhere. Understanding where these inflated numbers originate helps owners recognize when their own valuation has drifted into dangerous territory, and it reveals what happens when sellers finally encounter the market’s actual price discipline.

What Happens When Overvalued Businesses Hit the Market

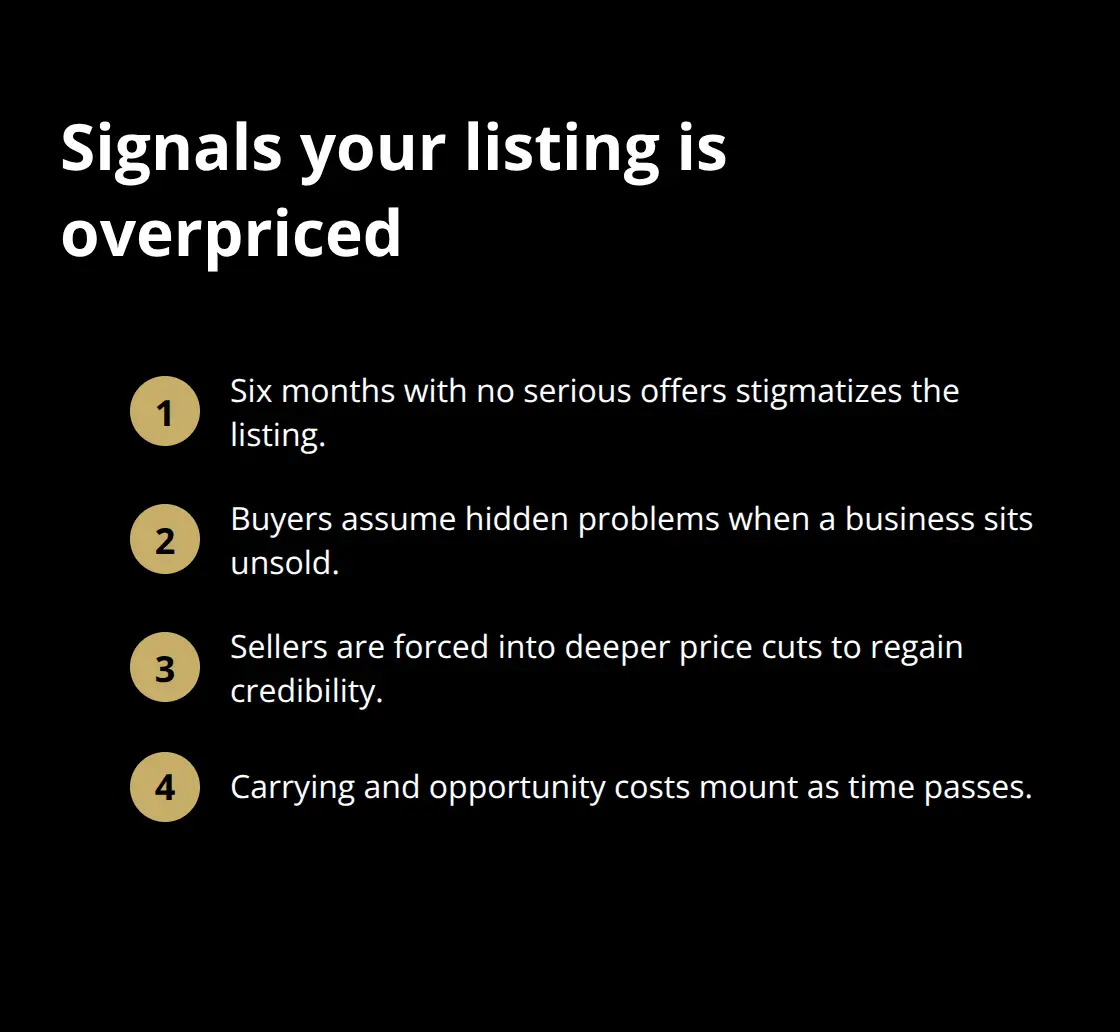

Overvalued businesses sit unsold while sellers watch months slip by with zero serious offers. The gap between asking price and buyer willingness to pay creates an immediate credibility problem. When a business lists at $5 million but comparable recent sales closed between $2.8 and $3.2 million, savvy buyers recognize the disconnect immediately and move on to better-priced opportunities. Sellers often blame market conditions or claim the right buyer hasn’t emerged yet, but the real issue is straightforward: the price reflects valuation theater rather than market reality.

How Unsold Listings Signal Weakness

Unsold listings signal weakness to potential buyers. After six months on the market with no serious interest, a business becomes stigmatized. New buyers ask why it hasn’t sold, and they interpret the lack of offers as evidence that something is wrong with the operation itself, regardless of the actual cause. This perception forces sellers to drop their asking price far below the original inflated valuation, often ending up worse off than if they’d priced realistically from day one.

The financial cost compounds when sellers finally capitulate and accept lower offers after burning months of opportunity cost and carrying costs they didn’t anticipate.

The Post-Sale Reckoning for Buyers

Buyers who acquired businesses at inflated valuations during the bidding war environment face a harsh reality within twelve to eighteen months. Growth assumptions embedded in the purchase price don’t materialize. A buyer who paid $4 million for a business based on projected 20 percent annual revenue growth discovers the actual growth trajectory is 8 percent. That gap translates directly into overpayment. If the business should have been valued at $2.3 million based on realistic growth assumptions, the buyer sits on a $1.7 million loss that won’t show up on financial statements until years later when they try to refinance or resell.

Earnout provisions can mask this problem temporarily, but they also create conflict between buyer and seller when performance targets aren’t met. Sellers who negotiated earnouts based on inflated growth assumptions face clawback demands or disputes over metrics, damaging relationships and potentially triggering litigation. The deal that felt successful at closing becomes a source of regret and financial damage for both parties.

Hidden Costs That Reduce Final Proceeds

Hidden transaction costs amplify the damage beyond the purchase price itself. Legal fees, accounting reviews, due diligence expenses, and working capital adjustments typically consume additional costs that sellers didn’t budget for when they heard their initial valuation. These expenses reduce actual proceeds significantly, and sellers often discover them only after committing to a transaction.

Why Realistic Pricing Attracts Qualified Buyers

A business priced at market-clearing levels attracts multiple qualified buyers quickly, creating genuine competition that validates the price. When several credible buyers compete for a reasonably priced asset, the seller achieves strong returns without the risk of post-sale buyer remorse that creates disputes and damages reputation. The transaction closes faster because buyer expectations align with actual business performance. Financing approval happens more smoothly when the purchase price matches what lenders believe the business supports.

Sellers who price realistically from the start save months of carrying costs, marketing expenses, and the psychological burden of watching their business languish on the market. They also avoid the scenario where they finally accept a deeply discounted offer after months of rejection, ending up with less than they would have received if they’d priced correctly initially. The difference between an inflated valuation that generates zero offers and a realistic valuation that closes quickly often exceeds $500,000 on mid-market transactions (accounting for both the lower final price and the carrying costs during the extended marketing period).

Final Thoughts

Valuation inflation has become the default in 2025, but it doesn’t have to define your transaction. Businesses that sell successfully and generate genuine buyer satisfaction share one characteristic: they’re priced based on what the market will actually pay, not what brokers claim is possible. Transparent pricing protects both sides because when a seller knows their business is worth $3 million based on demonstrated cash flow and realistic growth, they can confidently reject offers below $2.7 million while remaining open to serious buyers in that range.

Sustainable business sales happen when expectations match reality from day one. A transaction that closes at a fair price generates positive outcomes for both parties-the buyer implements their strategy without discovering they overpaid for growth that won’t materialize, and the seller receives proceeds they can actually count on without watching their business sit unsold for months. Your historical revenue growth, proven profit margins, and demonstrated market position form the foundation of valuation, while projected improvements should adjust your multiple upward by 10 to 15 percent at most, not double or triple your asking price.

We at Unbroker see the damage that valuation inflation creates every day. Sellers who work with us establish what their business is actually worth, then market it at that price to attract genuine buyer interest. Our transparent pricing platform eliminates the incentive for inflated valuations, giving you the clarity you need to make confident decisions about selling your business.