Business owners often wonder which valuation method will fetch the highest price when selling. The answer isn’t simple-different valuation methods produce vastly different results, and the highest number doesn’t always reflect what a buyer will actually pay.

At Unbroker, we’ve seen how income-based, market-based, and asset-based approaches each tell a different story about your business’s worth. Understanding these methods helps you set realistic expectations and negotiate from a position of strength.

Income Approach to Business Valuation

How the Income Approach Works

The income approach values your business based on what it can earn in the future. This method assumes that a buyer cares most about cash flow-how much money the business generates year after year. Three main techniques fall under this umbrella: discounted cash flow analysis, the earnings multiplier method, and revenue-based valuation. Each produces different numbers, and understanding why matters when you prepare to sell.

Discounted Cash Flow Analysis

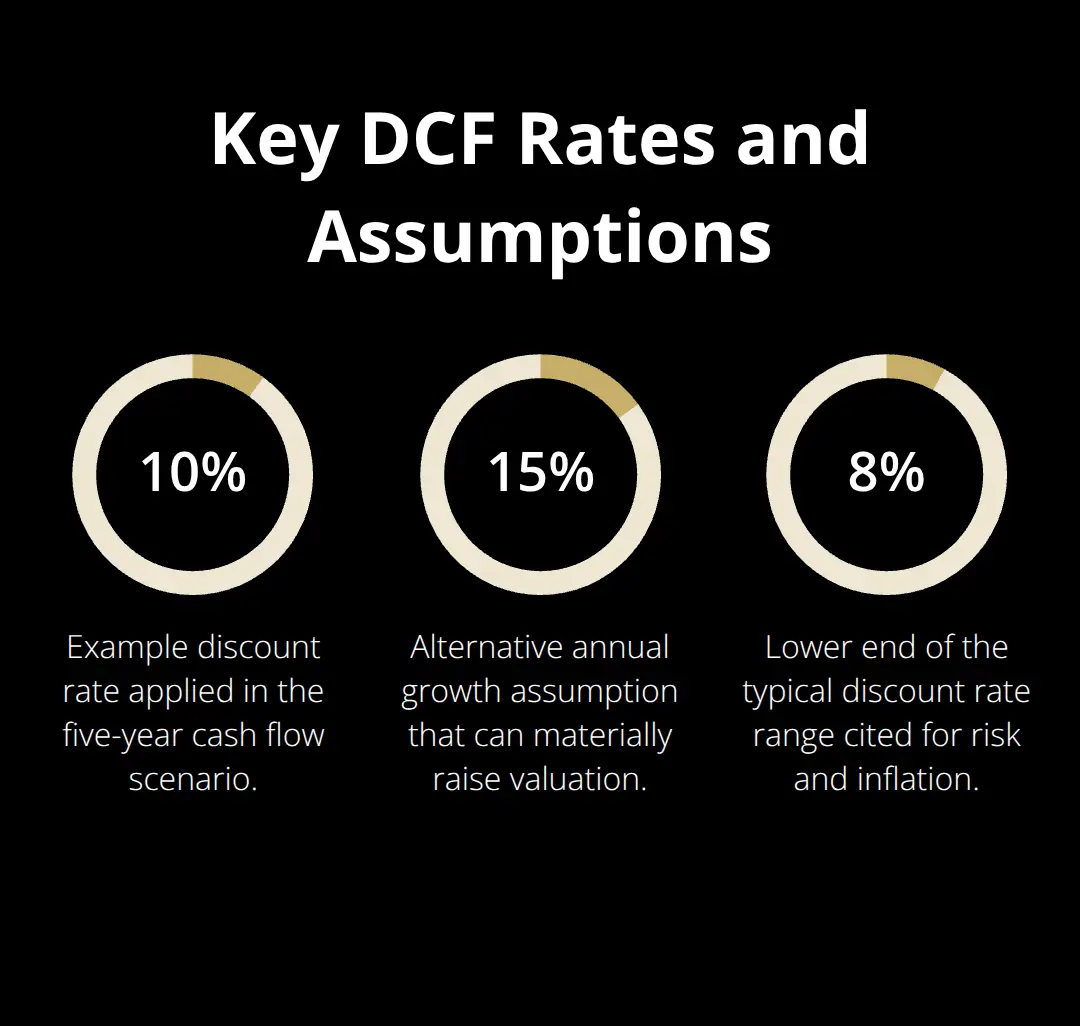

Discounted cash flow analysis projects your future earnings and discounts them back to today’s value using a rate that reflects risk and inflation, typically around 8–12%. A business expected to earn $2 million annually for five years, discounted at 10%, yields roughly $7.6 million. This method captures growth potential because it accounts for how much money you’ll actually receive over time. The challenge lies in the assumptions you make about future performance.

Small changes in growth rates or discount rates swing valuations by hundreds of thousands of dollars. If you project 15% annual growth for five years instead of 10%, your valuation jumps significantly. Buyers scrutinize these assumptions carefully, especially for recurring revenue streams versus one-time project spikes.

Earnings Multiplier and Revenue-Based Methods

The earnings multiplier method works faster than DCF: take your profits and multiply them by an industry-specific factor. For example, $5 million in earnings multiplied by 8 equals $40 million in value. This approach works best for stable, mature businesses with consistent profits. Revenue-based valuation skips profitability entirely and applies a multiple to total sales instead. Tech firms might be valued around 3x revenue, while service firms might be around 0.5x revenue. A software company with $10 million in revenue valued at 3x revenue would be worth $30 million. Revenue-based valuation carries real risk because it ignores profitability entirely-a business generating $10 million in revenue but losing money could still appear valuable on a spreadsheet.

Why Income Methods Often Produce the Highest Numbers

The income approach typically produces the highest valuations because it captures growth potential and future earning power-not just what the business owns today. Recurring revenue commands premium multiples because it’s more predictable. A SaaS company with consistent recurring revenue will fetch a higher multiple than a consulting firm with the same earnings but project-based income. This preference for stability reflects how buyers think about risk and cash flow reliability.

Triangulating Across Income Methods

Rather than relying on one number, compare what each method produces, then investigate the gaps. If DCF yields $8 million but the earnings multiplier yields $5 million, that $3 million difference points to questions about growth assumptions or profit quality that deserve attention before you negotiate with a buyer. These discrepancies reveal whether your valuation rests on solid ground or optimistic projections. The market approach takes a different angle-instead of projecting your future, it looks at what similar businesses actually sold for.

Market Approach to Business Valuation

What Do Similar Businesses Actually Sell For?

The market approach abandons projections and focuses on comparable businesses actually sold for in the real world. Instead of guessing about your future earnings, this method examines transaction data from similar companies and uses those sale prices to value yours. The strength of this approach lies in its grounding in reality-actual buyers paid actual money for actual businesses with characteristics similar to yours. The weakness is equally obvious: no two businesses are identical, and market conditions shift constantly. A software company that sold for 5x revenue eighteen months ago might now fetch only 3.5x revenue because interest rates climbed and buyers grew more cautious.

Industry Multiples Reveal Massive Valuation Gaps

Damodaran’s NYU Stern dataset tracks EBITDA multiples across industries, revealing enormous variation in what buyers will pay. Real estate rental and development operations command around 27.63x EBITDA, while broadcasting sits near 2.3x to 2.4x. Software companies land around 10.59x, restaurants around 17.14x, and food retail around 11.38x. These aren’t theoretical numbers-they reflect thousands of actual transactions weighted by market activity. A business worth $5 million under one industry’s multiple could be worth $50 million under another’s, so knowing your true industry category matters enormously.

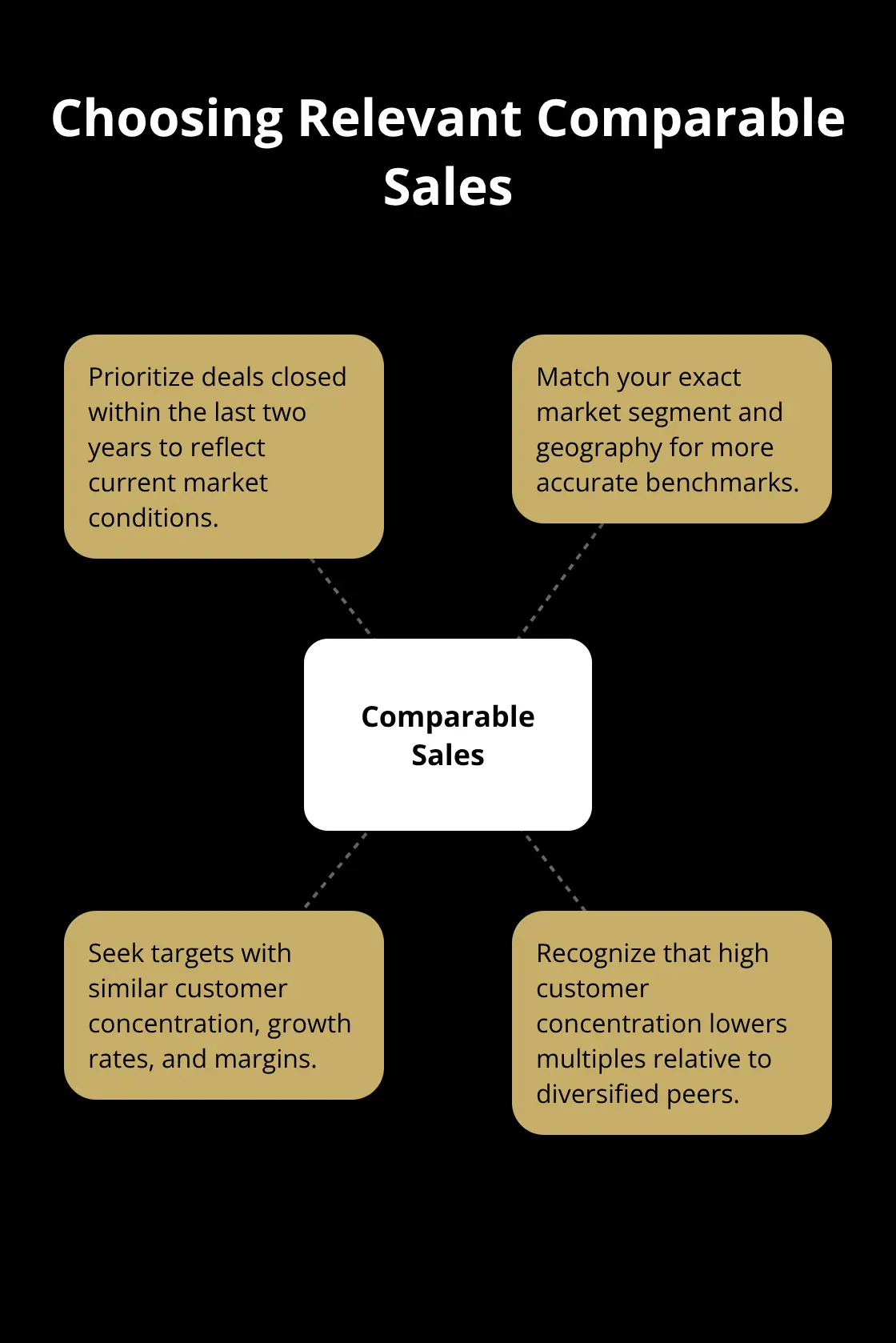

Finding Relevant Comparable Sales

When evaluating comparable sales, focus on deals completed within the last two years in your exact market segment and geographic region. A SaaS acquisition in Silicon Valley in 2024 tells you far more than a SaaS deal from 2022 or one from a completely different region. Look for transactions where the acquired company had similar customer concentration, revenue growth rates, and profit margins to yours.

High customer concentration valuation impact signals less predictable cash flows and can depress your multiple compared to the industry average. If your business shows this risk, buyers will anchor their offers to lower multiples, and comparable sales from diversified competitors won’t help your negotiating position.

Accessing Transaction Data and Benchmarks

The challenge with precedent transactions is that detailed deal data rarely becomes public. Most private business sales stay confidential, so the universe of known comparables is always incomplete. Investment banks and M&A advisors maintain proprietary databases with thousands of deals, but accessing this information costs money and requires expertise to interpret correctly. When you lack access to transaction databases, focus on what you can observe: public company acquisitions in your space, announced deals in trade publications, and tax records or regulatory filings for businesses that sold recently. Industry benchmarks published by groups like the National Business Brokers Association or specialized research firms for your sector provide statistical anchors even when individual deal terms stay hidden.

Combining Market Data with Income Projections

The real power of the market approach emerges when you combine it with the income approach. If comparable companies sold for 6x EBITDA but your discounted cash flow analysis suggests 8x EBITDA based on superior growth, that gap signals either that your growth assumptions are too optimistic or that you’ve found a genuine competitive advantage that buyers will reward. Conversely, if comparables show 6x but your DCF shows 4x, something in your business model-customer concentration, declining margins, or churn risk-is suppressing value relative to peers. This tension between methods reveals truth more effectively than any single number can. Asset-based approaches take yet another path, valuing what your business owns rather than what it earns or what similar businesses sold for.

Asset-Based Approach and Hybrid Methods

Tangible and Intangible Asset Valuation

The asset-based approach values your business by tallying what it owns minus what it owes. This method works differently from income and market approaches because it ignores future earnings and comparable sales entirely. Instead, it focuses on tangible assets like equipment, inventory, and real estate, plus intangible assets like brand reputation, customer relationships, and intellectual property. For most service and tech businesses, intangible assets dwarf tangible ones. A software company worth $20 million might own only $2 million in physical assets, meaning $18 million of value sits in code, patents, and customer lists that don’t appear on a traditional balance sheet.

Net Asset Value Calculation

Calculating [net asset value](https://www.investopedia.com/terms/n/nav.asp] means taking total assets and subtracting total liabilities. Facebook’s net asset value sits around $156.2 billion when you subtract $22.69 billion in liabilities from $178.89 billion in assets, though this figure tells you almost nothing about what a buyer would actually pay for the company. The asset-based approach works best for asset-heavy businesses like manufacturing, real estate, or equipment rental. For knowledge-based businesses, it systematically undervalues the company because it struggles to quantify what makes the business special.

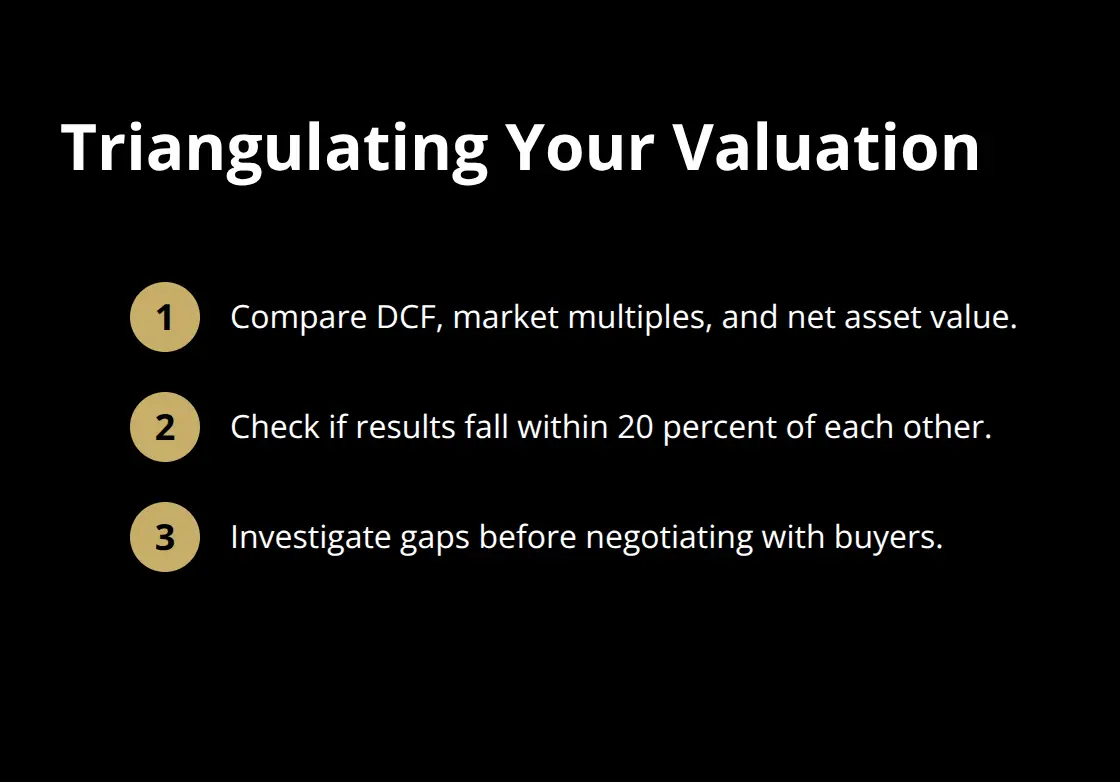

Combining Multiple Approaches for Accuracy

Compare what DCF produces, what market multiples suggest, and what net asset value shows. If all three methods land within 20 percent of each other, your valuation rests on solid ground. If they diverge wildly, something deserves investigation before you talk to buyers.

A boutique fitness studio that showed $800,000 in net asset value but $2.1 million in DCF valuation had a gap pointing to underutilized capacity and inefficient staffing. After addressing those operational issues, the studio’s valuation jumped nearly $180,000 within twelve months.

Identifying Value Leaks and Competitive Advantages

Conversely, if asset value exceeds income-based value, your assets aren’t generating adequate returns and a buyer might strip out underperforming equipment or real estate. The gap between methods reveals where your business leaks value or where competitive advantages justify premium pricing. Professional valuators triangulate across all methods precisely because no single approach captures complete truth. These gaps point to specific operational improvements that can lift your final sale price before you approach potential buyers.

Final Thoughts

The income approach typically produces the highest valuations because it captures future earning power and growth potential. DCF analysis especially tends to generate premium numbers when growth assumptions are aggressive. Market multiples ground valuations in reality by showing what actual buyers paid for comparable businesses, often producing lower figures than income-based projections. Asset-based approaches usually yield the lowest numbers for service and tech businesses because they ignore intangible value like customer relationships and intellectual property.

The highest valuation method isn’t always the right one. A buyer won’t pay based on your most optimistic DCF model if market comparables show similar businesses selling for significantly less. The gap between valuation methods reveals critical information about your business-if DCF and market multiples diverge sharply, something in your assumptions or competitive position needs examination before you approach potential buyers. Customer concentration matters enormously; a business dependent on three customers for 50 percent of revenue will command lower multiples than a diversified competitor with identical profits.

Recurring revenue streams fetch premiums over project-based income because they’re more predictable, while profit margins signal competitive strength and justify higher multiples. Management team depth reduces perceived risk and supports higher valuations, and intellectual property plus defensible competitive advantages justify premium pricing because they’re harder to replicate. Explore how modern platforms can streamline the selling process while keeping costs transparent and manageable, positioning you to negotiate from strength and maximize your final sale price.