Broker networks control how businesses get bought and sold. They set commissions, control information flow, and create bottlenecks that slow down deals.

At Unbroker, we’ve seen firsthand how these traditional systems waste time and money. This post reveals what actually happens behind closed doors.

How Broker Networks Move Information

Broker networks control how information flows, and whoever controls the data controls the deal. Multiple listing services sit at the center of this ecosystem, aggregating property or business information from thousands of agents and brokers. In real estate, the MLS has been the standard since the 1970s, creating a semi-centralized database that agents access to list and search properties. However, this system has significant limitations. The data is only as current as brokers choose to make it, delays of 24 to 48 hours are common between when a property sells and when the listing is marked as off-market, and information flows through gatekeepers who profit from controlling access.

As networks grow, the one-to-one connections between data sources and the agents who need them become unmanageable bottlenecks.

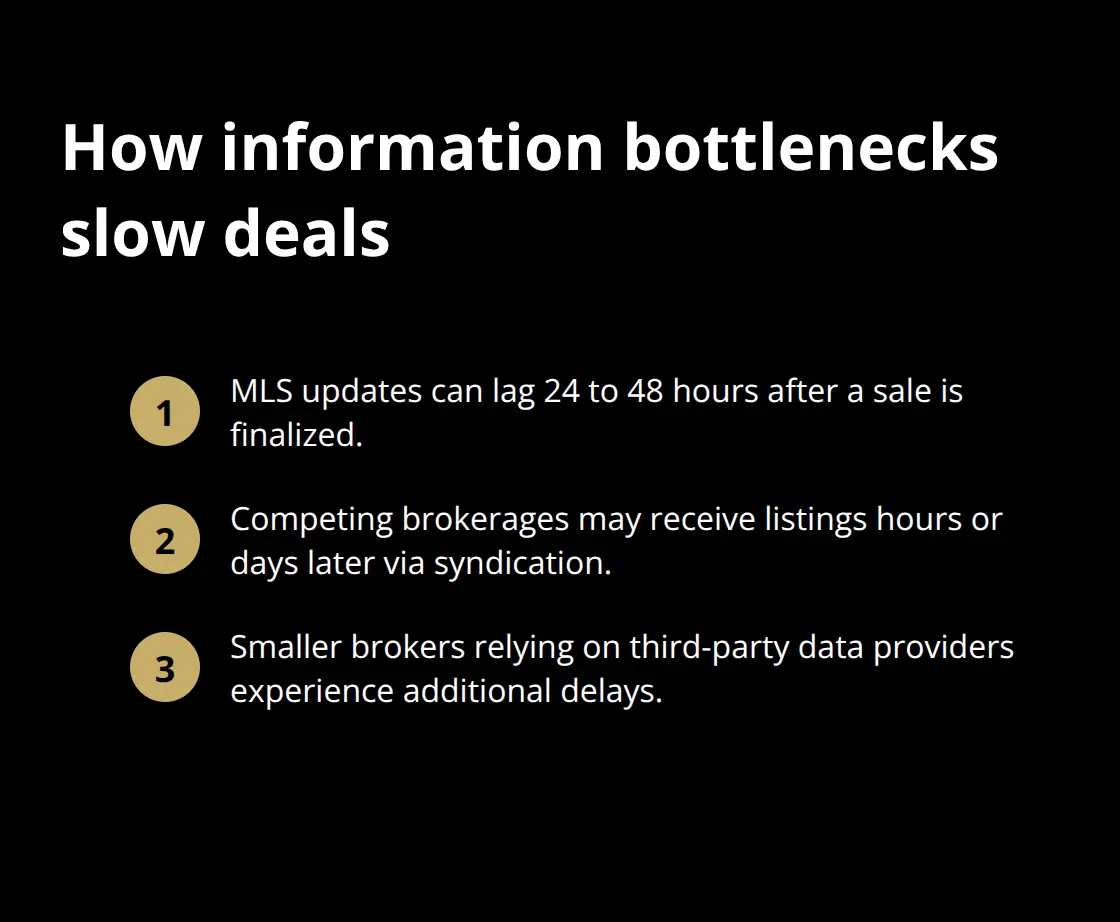

Real-Time Access Remains a Myth

Real-time access does not exist in traditional broker networks. When a listing goes live, it does not reach all potential buyers simultaneously. Agents working for competing brokerages may see properties hours or days later, depending on how their MLS syndicates data. Large brokerages with dedicated IT resources update their internal systems faster, giving their agents an unfair advantage. Smaller independent brokers often rely on third-party data providers, introducing another layer of delay. A buyer working with a slower broker might miss opportunities entirely because their agent did not see the listing in time.

Outdated Technology Creates Friction

The technology supporting these networks-often built decades ago and patched repeatedly-cannot handle modern transaction speeds. Agents still spend hours each week manually entering data, cross-referencing spreadsheets, and calling other brokers to confirm information. This friction directly impacts closing timelines and negotiation leverage. The infrastructure behind broker networks creates artificial scarcity in broker networks. High-end analysis tools and databases have limited ports and capacity, so networks must choose which agents see which data. This filtering means some brokers gain preferential access while others operate with incomplete information.

How Scale Breaks Traditional Systems

The Broker Network in Portland, Oregon found this problem so severe that they switched from scripted answering services to live virtual receptionists, simply because the old system could not handle the volume of inquiries fast enough. When a buyer calls about a property, if that call goes to an answering service or outdated routing system, the lead may never reach the right agent. The delay itself kills deals. Networks that do not invest in modern communication tools lose deals to competitors who do.

The problem is not the concept of broker networks-it is that most operate on infrastructure designed for a different era. Modernizing requires not just new software but rethinking how information flows from listing to buyer. This infrastructure challenge directly shapes the economics of how brokers earn money and distribute commissions across their networks.

Who Actually Gets Paid in Broker Networks

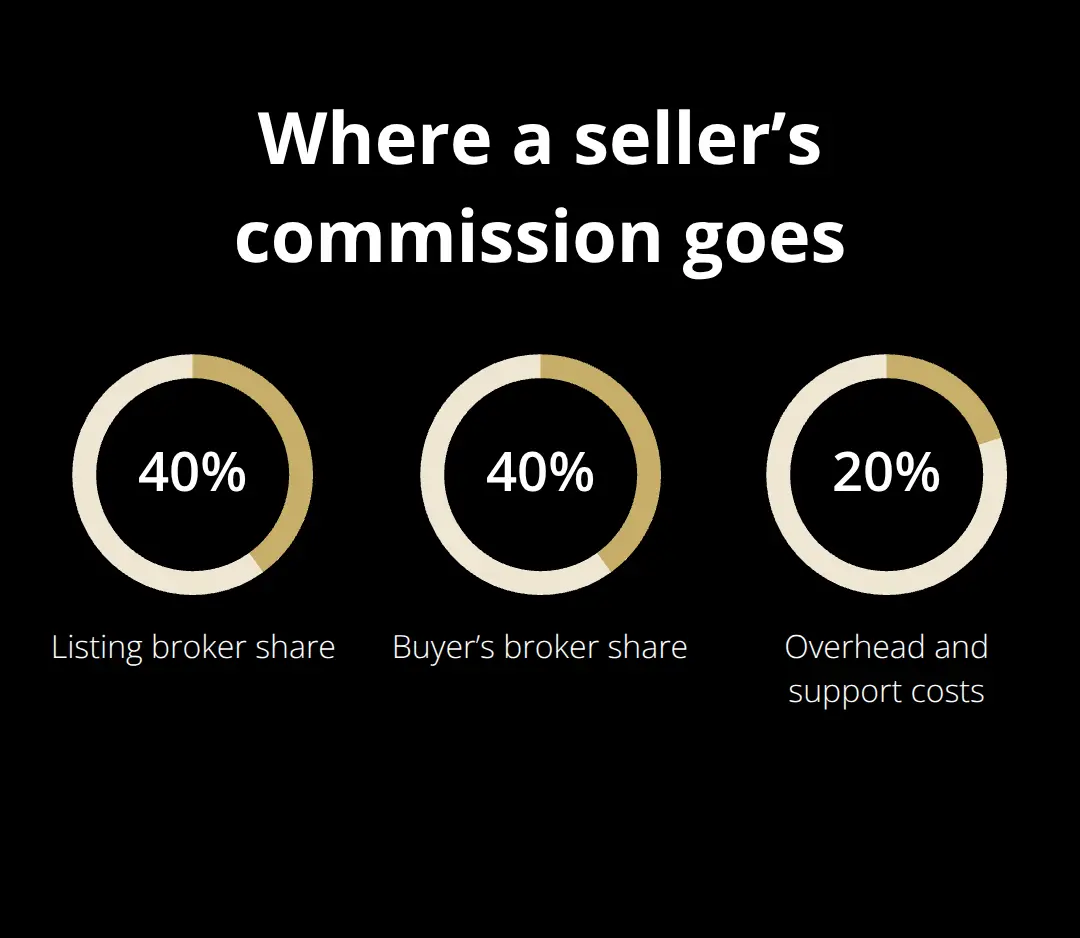

Broker networks operate on a commission-splitting model that benefits established players and punishes newcomers. When a business sells through a traditional broker network, the seller typically pays a commission ranging from 8 to 12 percent of the sale price. That commission gets divided among multiple parties: the listing broker, the buyer’s broker, the brokerage firm itself, and various intermediaries. A seller moving a $1 million business through a traditional network can expect to pay $80,000 to $120,000 in commissions alone.

What makes this worse is the opacity. Most sellers never see a detailed breakdown of where their money goes. The listing broker might keep 40 percent, the buyer’s broker takes another 40 percent, and the remaining 20 percent gets split between support staff, technology infrastructure, and office overhead. Nobody discloses this upfront. Sellers find out after they sign agreements they barely understand.

The Hidden Markup System

Traditional broker networks layer markups on top of commissions. When a broker uses a third-party valuation service, marketing company, or legal resource, they often charge sellers a markup on that service rather than passing through the actual cost. A valuation that costs the broker $800 gets billed to the seller as $1,200. Marketing materials produced by freelancers at $500 get invoiced at $1,500. These hidden costs accumulate silently, and sellers rarely question them because they assume the broker negotiated the best rate. In reality, the broker profits from the spread.

Closing costs add another layer of opacity. Title insurance, escrow fees, and legal document preparation vary wildly depending on which service providers the broker steers sellers toward. Some brokers have informal relationships with title companies and attorneys that generate referral fees, creating conflicts of interest. A seller might pay $3,000 for title insurance when the actual cost is $1,500, with the broker pocketing the difference without disclosure. These markups are standard across the industry, which is why traditional broker networks have become so profitable while sellers feel squeezed.

Information Asymmetry as a Profit Driver

Broker networks profit from what sellers do not know. Because brokers control access to buyer networks and market data, they claim their commission is justified through exclusive access to qualified buyers. In reality, most qualified buyers in any given market are already known to multiple brokers. The exclusivity is manufactured.

A broker might tell a seller that their buyer network justifies the premium commission, but that buyer network is often just their past clients and referral sources-the same sources available to any broker in the region. Brokers also withhold information about competing offers or buyer interest to maintain negotiating leverage. If a seller knew that five buyers were interested, they could negotiate harder on price and terms. Instead, brokers control the flow of information, revealing only what benefits the deal they prefer.

Why Transparency Threatens Traditional Models

This information advantage directly increases the broker’s bargaining power and protects their commission. Transparency eliminates this advantage, which is why traditional networks resist it so fiercely. When sellers know exactly what they pay, how their money gets distributed, and what buyer network they actually access, commission rates look indefensible.

The real cost of these hidden economics extends beyond the seller’s wallet. Brokers who profit from opacity have no incentive to speed up transactions or reduce friction. They earn the same commission whether a deal closes in two months or six months. They earn the same markup whether they use the cheapest or most expensive service provider. This misalignment between broker incentives and seller outcomes creates the delays and inefficiencies that plague traditional networks. Understanding who actually gets paid reveals why these systems move so slowly and why sellers pay far more than they should.

Why Broker Networks Move at a Snail’s Pace

Outdated Systems Create Unnecessary Work

Broker networks operate on systems designed for a slower era, and modernizing would undermine the very economics that make them profitable. Agents still spend 5 to 10 hours per week on data entry, manual confirmation calls, and spreadsheet reconciliation because the underlying infrastructure cannot automate these tasks. A broker managing 50 active listings must coordinate with 20 different counterparties, each requiring phone calls or emails to confirm details, availability, or contingencies. This friction is not accidental-it creates dependency. Brokers profit when transactions take longer because longer deals mean more opportunities for additional service charges, extended marketing fees, and repeated consultations.

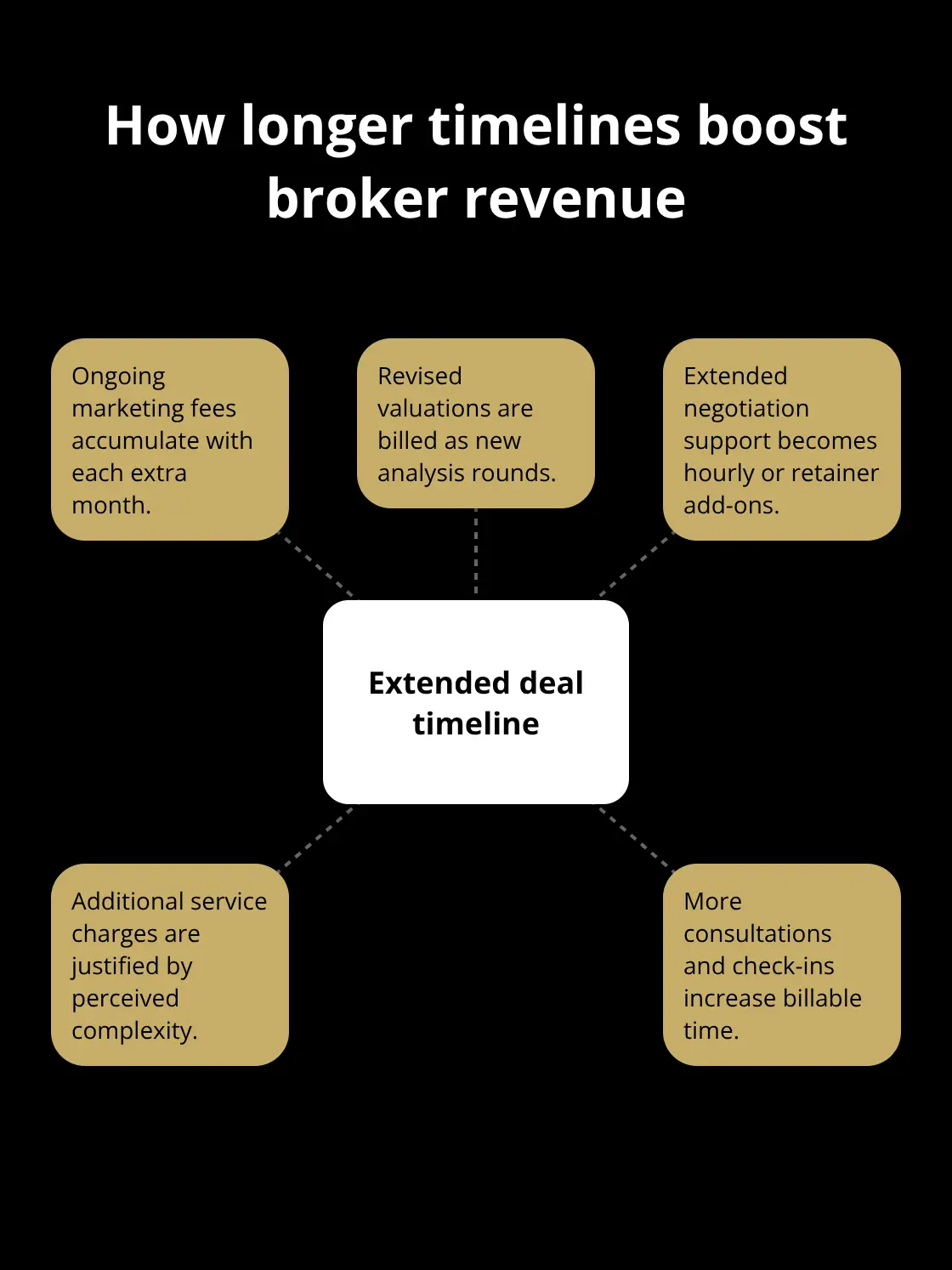

How Extended Timelines Boost Broker Revenue

When a business sale stretches across an extended timeline, the broker’s total revenue often increases through incremental charges that accumulate silently. The longer a deal remains open, the more justification brokers have to charge for ongoing marketing, revised valuations, or extended negotiation support. Sellers never see these costs itemized-they simply receive invoices for services rendered over an extended period.

Traditional brokers lack urgency to accelerate deals because slow transactions generate more revenue per transaction than fast ones.

Information Control Extends Deal Cycles Deliberately

Information asymmetry reinforces these delays intentionally. A seller calling to ask about competing offers hears the broker explain that other interested parties are not yet qualified, or that their offer terms are weaker, or that timing is uncertain. The broker controls what the seller knows, which controls what the seller will accept. When a buyer’s broker calls to negotiate, the listing broker can claim the seller has other offers without proving it, which strengthens the listing broker’s negotiating position and justifies higher asking prices.

These information gaps prevent sellers from making decisions based on reality-they make decisions based on what brokers tell them. Deals stall while brokers conduct endless back-and-forth conversations that would disappear if all parties had simultaneous access to the same data. Closing timelines stretch because brokers benefit from controlling the pace of disclosure.

Why Transparency Threatens Broker Economics

A transparent system where all parties see the same offers, timelines, and buyer qualifications simultaneously would compress deal cycles dramatically, but it would also eliminate the broker’s information advantage and the fees that advantage generates. The incentive structure of traditional networks actively punishes speed and transparency, which explains why efficiency improvements remain rare despite decades of available technology. Brokers who profit from opacity have no reason to invest in systems that would expose their margins or accelerate transactions.

Final Thoughts

Traditional broker networks profit from the very inefficiencies that harm sellers. High commissions, hidden markups, delayed information flow, and extended timelines are not bugs in the system-they are features that generate revenue for brokers. Sellers pay 8 to 12 percent commissions while brokers control data, manufacture scarcity, and deliberately slow transactions to extract additional fees. This model worked when alternatives did not exist, but it no longer does.

Sellers increasingly reject the opacity of traditional broker networks and demand to know exactly what they pay and where their money goes. They want access to buyer networks without paying gatekeepers. They want deals to close in weeks, not months. They want to negotiate based on real information, not information filtered through brokers who profit from withholding it.

When brokers stop profiting from delays and information asymmetry, transactions accelerate and costs drop. Sellers keep more money, buyers get better access to opportunities, and the market functions more efficiently because everyone operates with the same information and aligned incentives. Unbroker replaces the traditional broker network middleman with transparent technology that trusts sellers with information and competes on value rather than opacity.