Most business owners spend decades building something valuable, then wait until their sixties to think about selling. By then, it’s often too late to fix the problems that kill deal value.

At Unbroker, we’ve seen countless owners leave millions on the table because their exit planning started too close to retirement. The difference between a strategic exit and a desperate one comes down to timing and preparation.

What Happens When You Wait Until Your Sixties to Plan

Pressure Kills Deal Value

Last-minute exit planning destroys value in ways most owners don’t see coming until it’s too late. When you wait until your sixties, you’re forced to make decisions under pressure, and buyers know it. They’ll lowball you because they understand you need to move fast. Research from the Center for Retirement Research at Boston College shows that average retirement ages sit around 64.6 for men and 62.6 for women, yet most owners haven’t built a real exit strategy at that point. That compressed timeline means accepting whatever offer lands on your desk, not the premium price your business actually deserves.

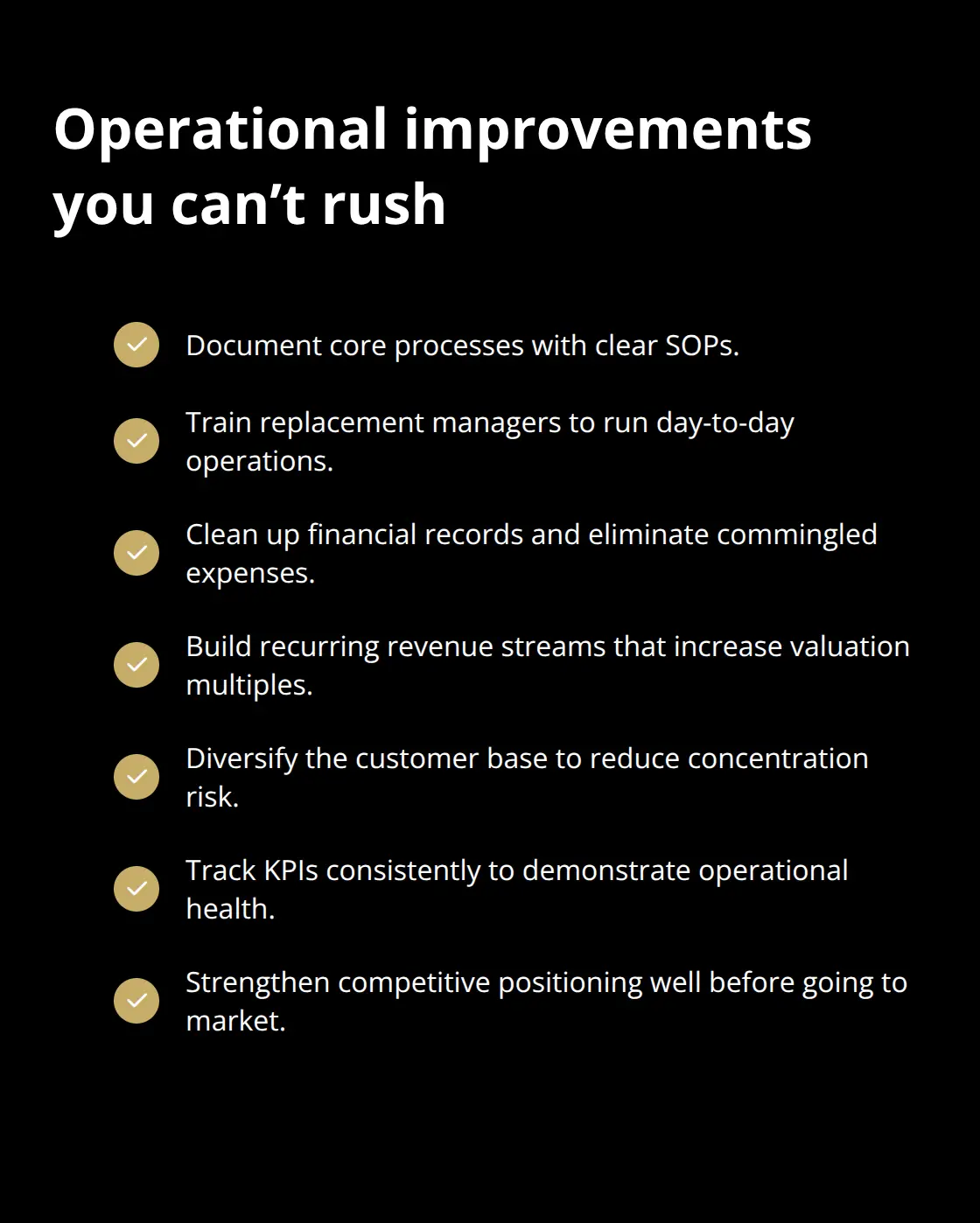

A rushed sale also means missing the chance to implement the operational improvements that separate a $2 million exit from a $5 million one. You can’t suddenly document your processes, train replacement managers, or clean up financial records when a buyer is already reviewing your books. Those fixes take years, not months.

The Stress of Scrambling at the Finish Line

The stress compounds because you’re simultaneously managing the business, negotiating terms, handling due diligence, and worrying about your retirement timeline. Many owners in this position report losing sleep over whether they’ll have enough money, whether the deal will close on time, and whether they’re leaving money on the table. The Transamerica Center for Retirement Studies found that health deterioration and involuntary job loss are the top reasons people exit the workforce early, and most of those exits happen without a solid financial cushion in place.

Why Buyers Discount Rushed Sellers

When you start planning in your late fifties or sixties, you forfeit the chance to build buyer confidence through documented systems and proven management depth. Buyers pay premiums for businesses that can run without the owner involved in daily operations. If your operation depends entirely on you, a strategic buyer will discount the price significantly because they’re inheriting execution risk.

You also lose the ability to execute tax-efficient exit structures. A qualified tax advisor can help you explore asset versus stock sales, installment sale options, and other strategies that minimize your tax burden, but these require planning well in advance. Starting late forces you into whatever structure the buyer prefers, which often costs you tens of thousands in unnecessary taxes.

The Improvements You Can’t Make in Time

Additionally, you miss the window to build recurring revenue streams, diversify your customer base, or strengthen your competitive position. These improvements take two to five years to show real results, and they’re worth substantial multiples when valuation time arrives. Late planners also struggle to attract quality buyers because the market senses urgency. Strategic buyers-the ones willing to pay the most-want to see a business with momentum and stability, not one being rushed to market by an owner counting down to retirement. This is precisely why early planning transforms your entire exit trajectory.

How Early Planning Builds Buyer Confidence

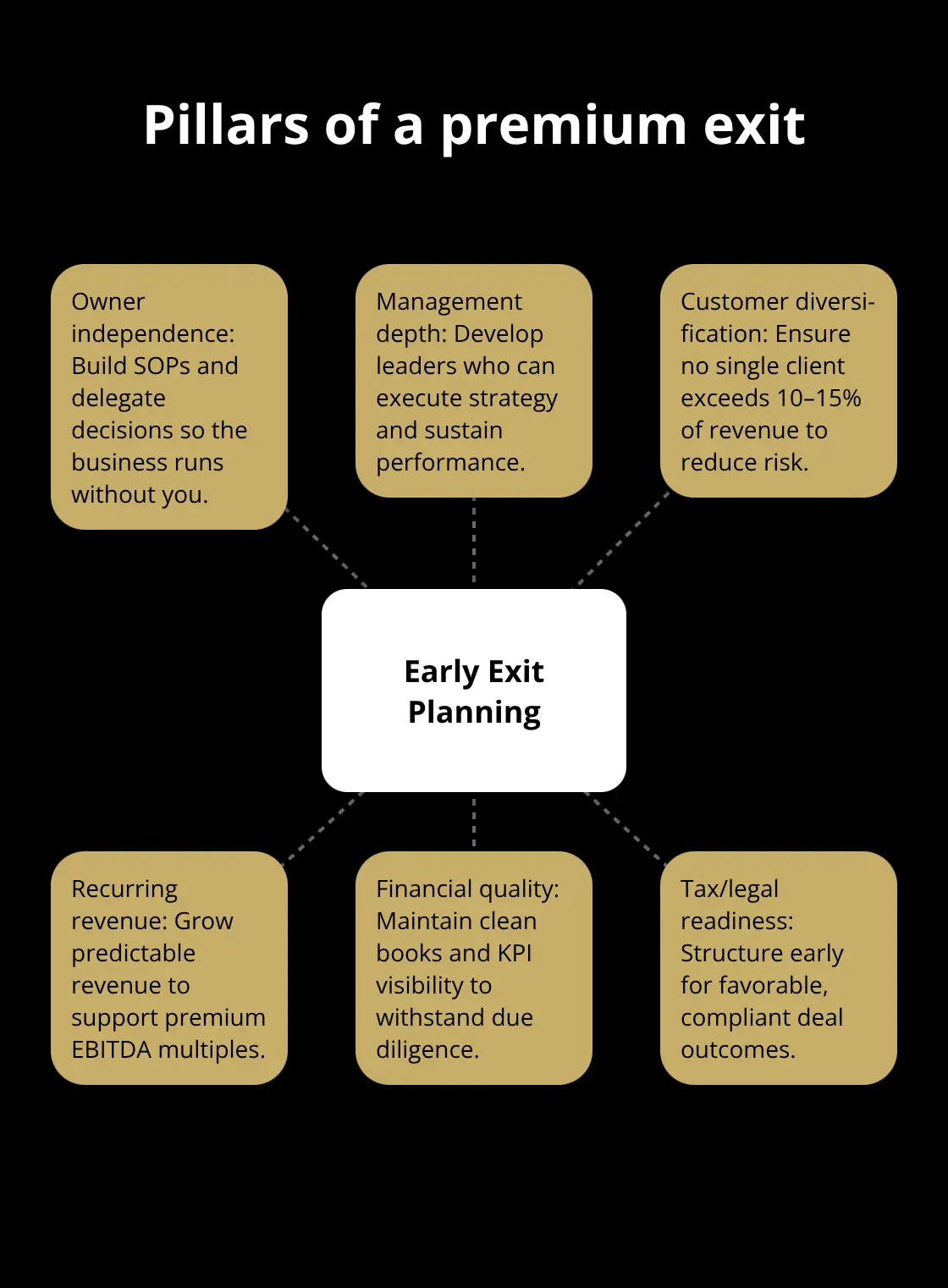

Starting your exit plan five to seven years before you want to sell transforms how buyers perceive your business. When you have that window, you can implement the operational systems that separate a commodity business from a premium asset. Buyers will pay more for a business that runs without you in the room every day, and that independence takes time to build. You need to create standard operating procedures for critical functions, train managers to make decisions without your input, and document your processes so they’re transferable. A business heavily dependent on the owner signals higher risk to buyers, which means they’ll apply a discount to your valuation. Early planning lets you eliminate that risk discount before negotiations even start.

Over a five to seven year timeline, you can also diversify your customer base so no single client represents more than 10 to 15 percent of revenue, build recurring revenue streams that buyers value at premium multiples, and strengthen your competitive position so the business has genuine momentum heading into a sale.

These improvements compound in value. A customer base that’s 80 percent recurring revenue might command a 4 to 5 times multiple on EBITDA, while a transactional business gets 2 to 3 times. That’s the difference between a five million dollar exit and a three million dollar one, and it’s built over years, not months.

Financial Records That Command Premium Prices

Clean financial records are non-negotiable for a premium valuation, and they take time to establish credibility with buyers. Your accountant needs to separate personal and business expenses completely, maintain consistent job costing across all projects, and track key performance indicators that show the health of your operation. During due diligence, buyers will scrutinize your accounting practices, and if they find commingled expenses, inconsistent revenue recognition, or poor documentation, they’ll assume you’re hiding problems. That assumption costs you money.

A formal business valuation performed two to three years before your planned exit reveals exactly which financial metrics buyers will focus on and which operational improvements will move your valuation needle. EBITDA normalization adjusts earnings to remove one-time costs and owner compensation quirks. Early planning gives you time to implement accounting improvements that make your financials shine, while late planners get whatever discount their messy books deserve.

Positioning Yourself for Tax Efficiency

Waiting until your sixties to consult a tax advisor means you’ve already missed the window for the structures that save you the most money. A qualified tax professional can help you explore whether an asset sale or stock sale makes more sense for your situation, whether an installment sale spreads your income across multiple years to reduce your tax bracket, and whether you qualify for favorable treatment under tax code sections like the 1202 small business stock exclusion. These decisions compound over years.

Starting early also gives you time to work with an estate planning attorney to align your business exit with your overall wealth strategy, potentially using techniques to freeze wealth for your heirs and minimize estate taxes. Last-minute tax planning often locks you into whatever structure the buyer prefers, which is designed to benefit them, not you. Early planning puts you in control of the structure that maximizes your after-tax proceeds, setting the stage for the final piece of your exit strategy: assembling the right advisory team to guide you through the sale process itself.

What Happens When You Rush Due Diligence and Accept the First Offer

Most business owners who wait until their sixties don’t realize that due diligence is where deals either hold together or fall apart. When you’re under pressure to close quickly, you skip the preparation that protects your interests. A buyer’s team will spend weeks or months auditing your financial records, customer contracts, employee agreements, and operational processes. If you haven’t already organized and reviewed these materials, you’ll scramble to answer questions, and that scrambling signals weakness to the other side. Buyers exploit weakness by lowering their offers or adding contingencies that protect them at your expense. Owners who wait until late planning frequently accept offers 15 to 25 percent below market value because they lack the leverage that comes from preparation.

When you start planning your business exit strategy five to seven years early, you identify documentation gaps, fix accounting inconsistencies, and resolve contract issues before a buyer ever sees them. This eliminates surprises during due diligence and keeps the conversation focused on your business’s value, not its problems.

The Danger of Accepting Below-Market Offers

Desperation pricing happens when owners feel the clock running out. A buyer will sense your timeline pressure and anchor their offer low, knowing you’re unlikely to walk away and start over with another buyer. The gap between a desperate sale price and a market-rate price often reaches hundreds of thousands of dollars for small to mid-market businesses. An owner with a five-year runway can afford to reject a lowball offer, interview other buyers, and negotiate from strength. An owner in their late sixties cannot. The market value for your business depends on factors like recurring revenue, customer concentration, management depth, and financial quality. These metrics take years to improve, not months. If you’ve spent decades building a business where one client represents 40 percent of revenue, or where you personally close every deal, you’ve built a business that buyers will discount heavily. Fixing that structure in the final year before you want to exit is impossible. You’ll take whatever offer materializes because you have no time to reshape the business or develop competing offers.

Tax and Legal Structures You Can’t Undo at the Last Minute

A qualified tax advisor will tell you that the structure of your sale-whether you sell assets or stock, whether you take cash upfront or spread payments over time, whether you qualify for preferential tax treatment-determines how much money actually lands in your pocket after taxes. The difference between a tax-efficient exit and a tax-inefficient one can easily exceed $200,000 for a mid-market business. These decisions require advance planning because some structures take years to set up properly. For example, if you’re a C corporation and you want to minimize double taxation on an asset sale, you might explore a 338(h)(10) election, but that election has strict timing requirements and documentation needs that can’t be handled overnight. Similarly, if you qualify for the 1202 small business stock exclusion (which can exclude up to $10 million in gains from federal taxation), you need to have held the stock for at least five years. Wait until your sixties and you’ve already missed that window.

Legal Issues That Compound Your Problems

Legal gaps compound this problem significantly. If your customer contract transferability lacks clear terms, a buyer will demand price reductions to cover their risk. If your employee agreements don’t include non-competes or confidentiality clauses, buyers will factor in the risk that key staff will leave immediately after the sale. These gaps take months or years to address properly through renegotiation or new agreements. A late-planning owner gets stuck with whatever legal position they’re already in, and buyers will exploit every gap they find. The owner who starts planning early works with their tax advisor and attorney to structure the business for maximum after-tax outcome, eliminate legal risks before they become negotiating points, and preserve optionality when buyer conversations begin.

Final Thoughts

The math is straightforward: waiting until your sixties to plan your exit costs you hundreds of thousands of dollars. You forfeit the chance to build systems that buyers value, clean up financial records that raise your valuation, and structure your sale for tax efficiency. Most importantly, you lose leverage, and a buyer facing a desperate seller will anchor their offer low, knowing you have limited options and a ticking clock.

Starting your exit planning now, regardless of your current age, shifts the entire dynamic. Five to seven years gives you time to eliminate the operational risks that trigger buyer discounts, diversify your customer base so no single client dominates your revenue, and build recurring revenue streams that command premium multiples. You’ll work with a tax advisor on structures that minimize your tax burden, align your business exit with your estate plan, and resolve legal gaps before they become negotiating points.

The owners who maximize their exit value aren’t the ones with the biggest businesses-they’re the ones who started planning early enough to fix what matters. Unbroker offers modern tools and expert support to guide you through the process without the high fees that traditional brokers charge, and we help business owners at every stage of their exit planning journey.