Selling a small business is one of the biggest financial decisions you’ll make. The process involves multiple stages, from preparing your company for market to closing the final deal, and each step matters.

At Unbroker, we’ve helped countless business owners navigate this journey. This guide walks you through small business sale guidelines that turn a complex process into clear, manageable steps.

Getting Your Business Ready to Sell

Before you list your business, you need three things in place: an accurate valuation, organized financial records, and clarity on who you’re selling to. Most owners skip one or more of these steps and regret it during negotiations.

Start With a Professional Valuation

A professional valuation forms the foundation of your asking price. Valuations use three approaches: the income approach (based on cash flow and profit), the market approach (what similar businesses sold for), and the assets approach (tangible and intangible value). For small businesses, the income approach matters most because buyers care about what the business generates. Complete this step before you market; it saves months of back-and-forth over price later.

Clean Your Financial Records

Your financial records must be buyer-ready. This means cleaning up your books and identifying add-backs in financial statements-expenses a business incurs but a new owner likely wouldn’t, such as personal perks or one-time costs. A buyer wants to see sustainable profitability, not inflated costs. Document these add-backs with clear explanations. Buyers also expect to see monthly financial trends over the past 2–3 years, not just annual summaries. If your numbers are messy, hire an accountant to prepare clean statements; this investment often increases your sale price because it builds confidence.

Organize Legal and Operational Records

Your legal and operational records directly affect how fast due diligence moves. Buyers will request articles of incorporation, bylaws, shareholder agreements, employment contracts, customer contracts, lease agreements, and intellectual property documentation. Gather these now. If you can’t find something, recreate or clarify it before marketing. Disorganized records slow deals down by weeks.

Prepare a list of all liabilities: loans, equipment financing, pending lawsuits, and tax liens. Transparency here prevents surprises that kill deals at the finish line. Real estate matters too-if you own the property, document title, any mortgages, and environmental history. If you lease, confirm the lease allows assignment to a new owner and whether landlord consent is required. Many deals stall because landlords raise issues late in the process.

Match Your Business to the Right Buyer Type

Different buyers have different needs. Strategic buyers versus financial buyers have distinct priorities-strategic buyers often are willing to pay more because they can realize operational synergies, while financial buyers focus on cash flow and return on investment. Private equity firms look for growth potential and management depth. Understanding which type fits your business helps you position it correctly and speeds up matching with serious prospects.

If your business has strong margins and recurring revenue, emphasize stability to financial buyers. If you have unique technology or a large customer base, highlight growth potential to strategic buyers. This clarity shapes your listing, your outreach, and ultimately the offers you receive. With your valuation complete, records organized, and buyer profile clear, you’re ready to move into the market phase-where the right positioning and marketing strategy turn qualified prospects into serious offers.

How to Get Your Business in Front of Serious Buyers

Getting your business listed is only half the battle. The other half is making sure qualified buyers actually see it and want to move forward. Most sellers either cast too wide a net and attract tire-kickers, or they stay too quiet and miss serious prospects. The goal is controlled visibility-reaching buyers who can actually close while protecting your confidential information.

Use a Structured Marketplace to Filter Qualified Buyers

A structured marketplace approach works better than informal networking alone. Modern business marketplaces standardize how information flows, gate sensitive data behind NDAs, and let you filter for qualified buyers early. This approach cuts down on time-wasters and speeds up the path to real offers. You control who sees what, and serious prospects self-qualify before reaching out. Virtual data rooms let you share financial statements, tax returns, customer lists, and contracts only with buyers who’ve signed an NDA. This protects confidentiality and prevents information leaks that could damage your business or scare off employees and customers. Most serious sales happen through controlled channels where data sharing is staged and tracked, not through open listings where anyone can download your sensitive files.

Tell a Clear Story About Your Business

Your listing itself must tell a clear story about what the business does, why it’s stable, and what the buyer inherits. Don’t just list financials and call it done. Explain your competitive edge, customer retention patterns, recurring revenue streams, and why margins are healthy. If you’ve been in business for five years with 90 percent customer retention and growing annual revenue, lead with that. Buyers want to understand the business narrative before they ask for spreadsheets.

Include a realistic overview of what’s included in the sale-inventory, equipment, intellectual property, customer contracts, and any non-compete agreements. Clarity here prevents mismatches and wastes of everyone’s time.

Match Your Listing Language to Buyer Type

Positioning is about matching your business to buyers who value what you’ve built. If you identified your buyer type during preparation, now you shape your listing language accordingly. For financial buyers focused on cash flow, emphasize predictable revenue, profit margins, and operational efficiency. For strategic buyers, highlight growth opportunities, unique technology, customer relationships, or market position.

The same business can appeal to both types, but the messaging differs. A software company with strong recurring revenue appeals to financial buyers on stability; it appeals to strategic buyers on the potential to cross-sell to their existing customer base. Your listing should be discoverable by the right people. Use platforms that attract serious buyers and filter by industry, revenue size, and location so prospects self-qualify before reaching out. Avoid posting on generic job boards or classified sites where casual browsers outnumber actual buyers.

Build Relationships With Brokers and Buyer Networks

A qualified broker or intermediary expands your reach to buyers you wouldn’t find on your own. Brokers have relationships with private equity firms, strategic acquirers, and financial buyers actively looking for businesses in your industry. They also handle the logistics of outreach, initial screening, and confidentiality agreements so you stay focused on operations.

Traditional broker fees run 5 to 10 percent of the sale price, which adds up quickly on a multi-million-dollar deal. Direct outreach to potential buyers also works if you have existing relationships. Strategic buyers in your industry-competitors, suppliers, or companies serving adjacent markets-may have genuine interest. Approach these conversations carefully with an NDA in place. Personal introductions through your network, advisors, or industry contacts often yield the most serious prospects because they come with credibility.

Choose Your Sales Channel Wisely

The combination of a structured marketplace, professional broker support, and targeted outreach gives you multiple pathways to qualified buyers. Each channel has trade-offs: marketplaces offer standardized processes and broad visibility, brokers provide deep networks and hands-on guidance, and direct outreach builds on existing relationships. Your choice depends on your timeline, comfort level with the process, and how much support you want. Once you’ve positioned your business and attracted serious interest, the next phase shifts to evaluating offers and moving toward negotiations-where the real work of closing begins.

From Offer to Closing: What Actually Happens

Once you attract serious buyers, the real negotiation starts. Most sellers think this phase is about price haggling, but that’s only one piece. The actual negotiation covers purchase price, payment structure, employee transitions, transition support, and risk allocation. A Letter of Intent, or LOI, typically arrives first-a nonbinding document that outlines the buyer’s offer, including headline price, whether they want assets or stock, earnout terms if any, and a timeline for exclusive negotiations. The LOI signals serious intent. Set a deadline for exclusivity, usually 30 to 60 days, to create urgency and prevent the buyer from shopping your business to competitors while you’re locked in talks.

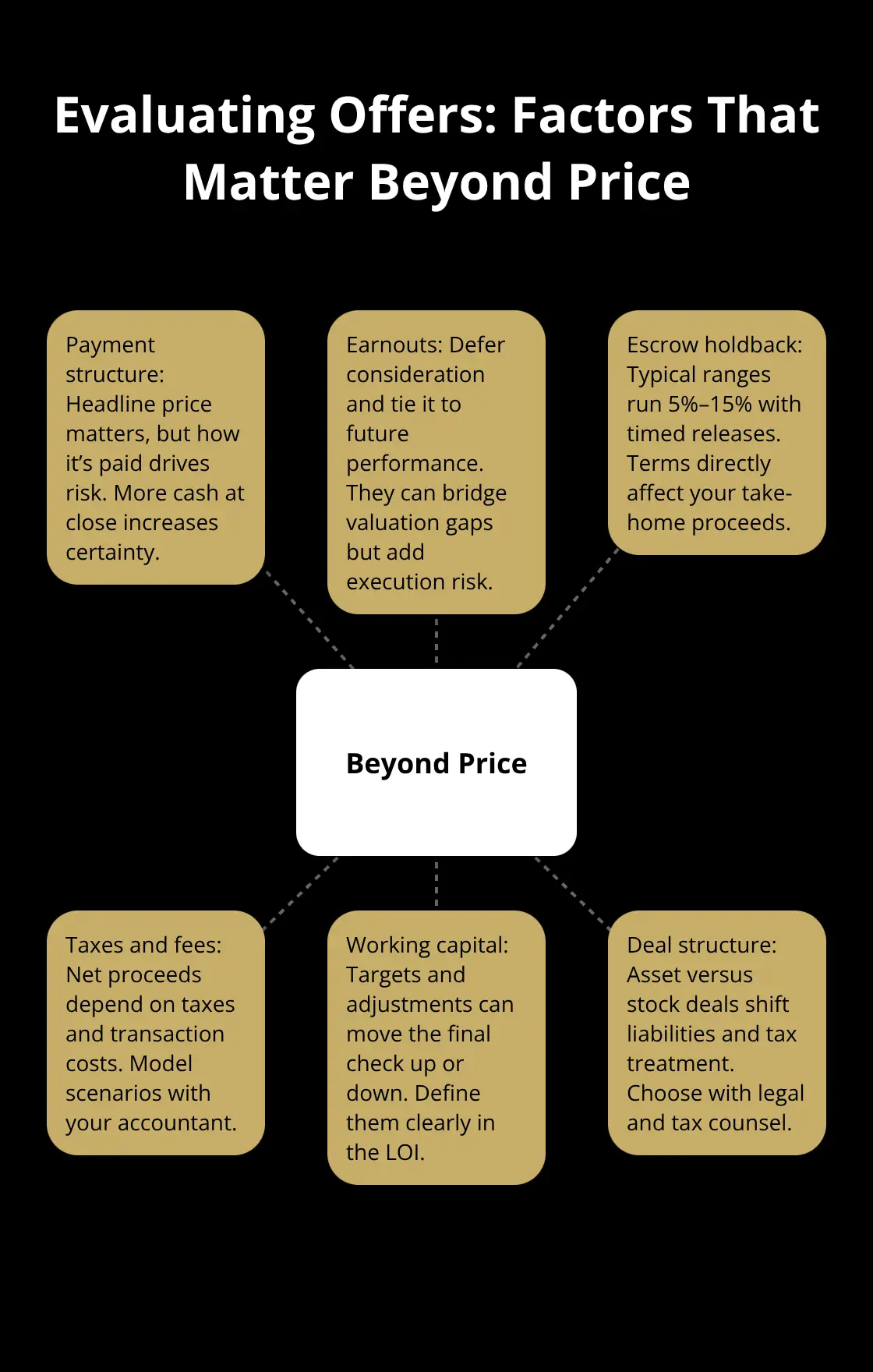

Evaluate Offers Beyond the Headline Price

Price isn’t everything when you evaluate an offer. A buyer offering $2 million in all cash at close beats a buyer offering $2.5 million with $1 million tied up in a two-year earnout.

Enterprise value is quoted on a cash-free, debt-free basis, meaning the buyer assumes your debt and you keep your cash. Work with your accountant to calculate net proceeds after debt payoff, transaction costs, and taxes. Small business sales typically use escrow holdbacks between 5% and 15% of the purchase price, with the escrow period lasting 12 to 24 months. This is normal and protects the buyer. Negotiate the escrow terms carefully: a 6-month release of half the holdback, with the remainder at 12 months, is reasonable. An 18-month full holdback favors the buyer too heavily.

Due Diligence Reveals Hidden Deal-Killers

Due diligence usually lasts 6 to 12 weeks and covers financials, operations, legal compliance, HR records, and customer contracts. The buyer’s accountant will scrutinize your tax returns, verify add-backs, and test profit margins. Their lawyer will review employment agreements, customer contracts, lease terms, and intellectual property ownership. Expect them to contact your top customers to confirm relationships and check for hidden dependencies. Organize your records now so you can respond fast. Slow responses kill momentum and give buyers time to lose interest or find problems they’d otherwise overlook. Create a data room with folders for financials, legal documents, employee records, customer agreements, and real estate docs. Use a virtual data room service if your deal size justifies it; for smaller deals, a password-protected folder works.

Disclose liabilities upfront. If you have pending litigation, customer concentration risk (one customer representing over 20 percent of revenue), or environmental issues on your property, tell the buyer immediately. Buyers find out anyway, and surprises during due diligence tank deals faster than known problems disclosed early. Real estate due diligence matters more than many owners realize. If you own the building, the buyer will order a Phase I environmental assessment. If contamination is suspected, they’ll demand a Phase II, which costs thousands and delays closing. If you lease, confirm the landlord will consent to assignment or that the lease allows it without consent. Landlord issues cause delays in 15 to 20 percent of small business sales.

The Asset Purchase Agreement and Disclosure Schedules

The Asset Purchase Agreement, or APA, is the binding contract. It specifies what’s being sold, the purchase price, closing conditions, representations and warranties, and indemnification provisions. Representations are promises you make about the business, such as ownership of assets, absence of undisclosed liabilities, and compliance with laws. Warranties stand behind those promises. Indemnification means the buyer can claw back money from escrow if a representation proves false. Have an M&A attorney draft or review the APA. The cost, typically $3,000 to $10,000, saves far more in disputes later. Disclosure schedules, the detailed lists attached to the APA, are critical. These list every exception to your reps and warranties: customer contracts with termination clauses, equipment leases, pending regulatory issues, and litigation. Accuracy here prevents post-closing disputes.

Closing and Transition Support

Closing happens when all conditions are met and documents are signed. Most small business closings are now virtual: signatures via DocuSign, funds wired directly, and title transferred electronically. Closing typically takes a day, though the paperwork process may span a week. Expect a closing statement that itemizes the purchase price, adjusts for net working capital, deducts transaction costs, and shows your net proceeds. After closing, you may owe transition support. Many buyers expect the seller to stick around for 30 to 90 days to answer questions about operations, customer relationships, and vendor contacts. Agree to this upfront and document it in the purchase agreement. Buyers who feel abandoned post-close sometimes pursue indemnification claims aggressively. A smooth transition protects your reputation and the holdback escrow.

Final Thoughts

Selling a small business demands preparation, strategy, and patience. The small business sale guidelines we’ve covered-from valuation and documentation through negotiation and closing-form a roadmap that transforms complexity into clarity. Owners who skip preparation steps pay for it later with lower offers, longer timelines, and deal friction. Those who organize early, position their business correctly, and evaluate offers holistically close faster and walk away with better outcomes.

Most owners underestimate how much work preparation requires. You cannot rush a professional valuation or expect buyers to trust messy financials. You also cannot assume that posting your business online attracts serious prospects. Qualified buyers exist, but they expect organized information, clear positioning, and transparent disclosure. Owners who treat the sale like a project with defined stages and deadlines move faster than those who hope things work out. A $2 million all-cash offer at close beats a $2.5 million offer with half the money tied up in earnouts and escrow, so calculate net proceeds after debt, taxes, and transaction costs before you celebrate an offer.

After closing, your job continues. Transition support matters more than most owners realize-buyers who feel supported post-close are less likely to pursue indemnification claims against your escrow. Spend 30 to 90 days answering questions about operations and customer relationships. We at Unbroker built our platform to remove friction from this process, and Unbroker offers transparent, low-cost options that eliminate high brokerage fees while connecting you to a vast buyer network. Your next step is to run a professional valuation, organize your records, and clarify your timeline.