Selling your business online exposes you to real risks. Fraudsters, data thieves, and social engineers are actively targeting deals like yours.

At Unbroker, we’ve seen what happens when sellers skip security steps. The good news is that secure online transactions are entirely within your control when you know what to protect and how.

What Threatens Your Business Sale Online

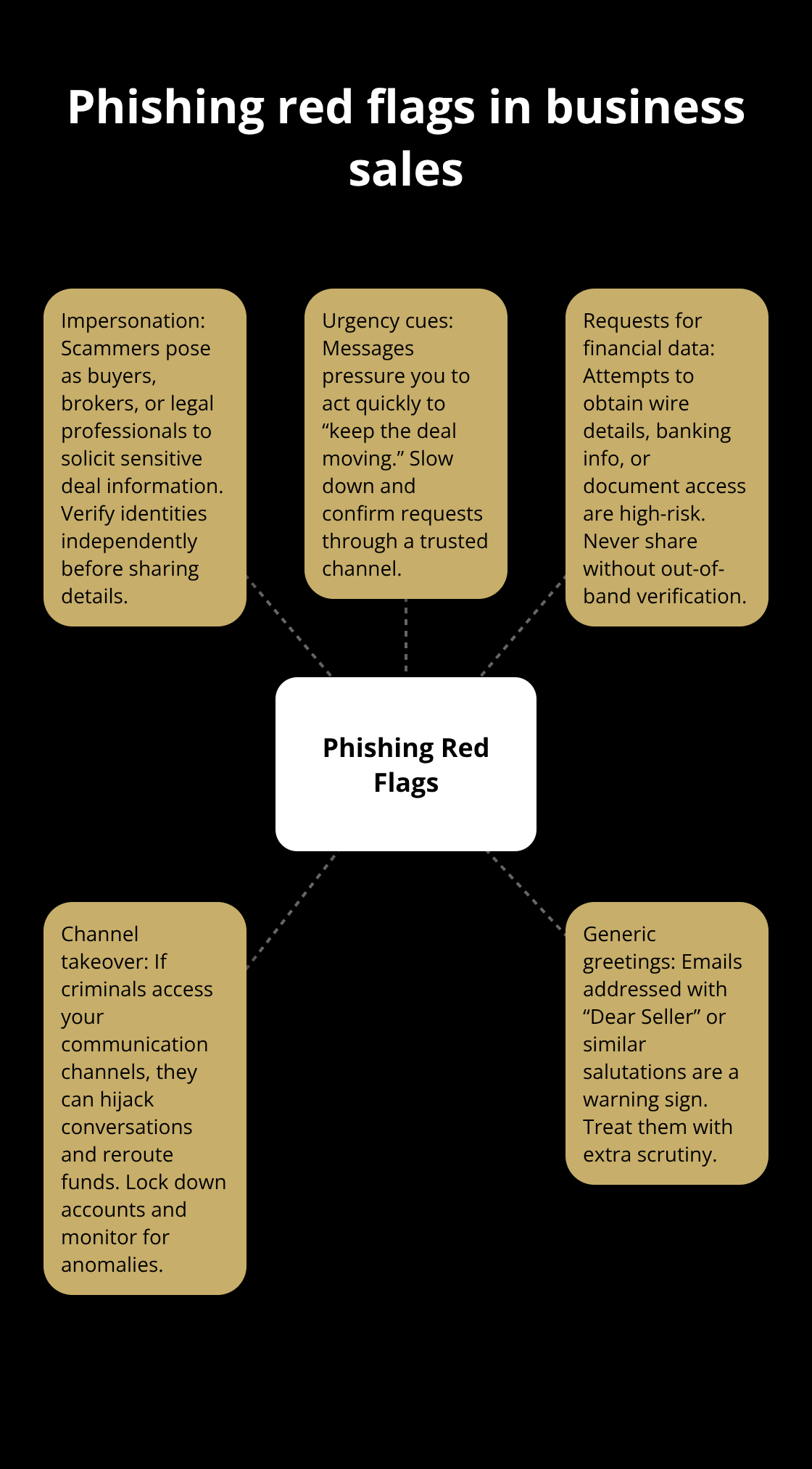

Phishing Attacks Target Sellers Directly

Phishing attacks targeting business sellers have become increasingly sophisticated. Scammers impersonate buyers, brokers, or legal professionals to extract sensitive information about your deal. The FTC reported that imposter scams remained the top consumer fraud for the ninth consecutive year. When you sell a business, you become an attractive target because transaction values are high and verification processes can be rushed.

Phishing emails often use generic greetings like “Dear Seller” or claim urgent action is needed to move the deal forward. They request wire transfer details, banking information, or access to confidential documents. The danger escalates when fraudsters gain access to your communication channels-they can intercept buyer-seller conversations and redirect payments to accounts they control.

Unauthorized Access Exposes Your Entire Transaction

Unauthorized access to your data compounds this risk significantly. A single compromised email account gives attackers visibility into your entire transaction, including buyer identity, pricing, and payment schedules. Data breaches from outdated software or weak password practices expose business information that criminals sell on dark web marketplaces. According to Juniper Research, cumulative merchant losses to online payment fraud globally between 2023 and 2027 will exceed $343 billion. This means every step of your sale-from initial buyer contact through final payment-requires active protection.

Payment Fraud at Closing Represents the Highest Risk

Payment fraud at closing represents the highest-value attack. Criminals either intercept legitimate payment instructions and redirect funds, or they pose as buyers and submit fraudulent payments that fail after you transfer ownership documents. Real-time fraud monitoring with machine learning can catch these attempts, but only if your payment processor uses advanced detection.

Synthetic identity fraud, where attackers create fake buyer profiles with fabricated credentials, represents a growing threat to transaction security. Verification gaps are the weakness here. Many sellers accept buyer credentials without independently confirming them through multiple channels.

How to Verify Payment Instructions Before You Transfer Anything

The solution requires encryption for all communications containing payment details, multi-factor authentication on every account involved in the transaction, and direct verification of payment instructions through a separate communication method from the one used to send them. If a buyer sends wire instructions via email, call them directly using a previously known phone number to confirm those details before you authorize any transfer. Never use contact information provided in the same message requesting payment.

These threats are real, but they’re preventable. The next section covers the specific practices that protect your business sale at every stage.

How to Lock Down Your Transaction at Every Stage

Verify Buyer Identity Through Independent Channels

Request government-issued identification from the buyer and cross-reference their business registration details through your state’s Secretary of State database or the Federal Trade Commission’s resources. Don’t accept digital copies alone-request verification through independent channels. Call the buyer’s registered business phone number directly, using a number you find yourself, not one they provide. Ask specific questions about their business that only the real owner would answer. Running a basic background check on serious buyers eliminates guesswork; services like ZoomInfo or Bloomberg provide ownership verification for a small fee. Many sellers skip this step because it feels awkward, but it stops most fraud before it starts.

Once you’ve confirmed identity, require all communication about payment details, wire instructions, and closing documents to happen through encrypted channels only. Standard email lacks encryption-use a platform like ProtonMail or Signal, which encrypt messages end-to-end so only you and the buyer can read them. This prevents man-in-the-middle attacks where fraudsters intercept unencrypted messages and inject fake payment instructions. If your transaction involves a broker, attorney, or escrow agent, verify their contact information independently before communicating about sensitive details. Criminals frequently spoof legitimate professional email addresses, changing a single character so the address looks nearly identical to the real one.

Encrypt All Communication About Payment Details

Encrypted channels protect your transaction from interception at every stage. When you send wire instructions, payment schedules, or banking details, encryption ensures that only the intended recipient can read them. Unencrypted email travels through multiple servers and can be accessed by anyone with network access to those servers. Encrypted platforms route your messages through secure servers that scramble the content so that even the platform itself cannot read your messages.

Set up encrypted communication before you need it. Test the platform with your buyer early in the process so both parties understand how to use it. This prevents confusion or delays when you’re ready to exchange sensitive information. If your buyer resists using encrypted channels, that’s a red flag. Legitimate buyers understand why security matters in high-value transactions.

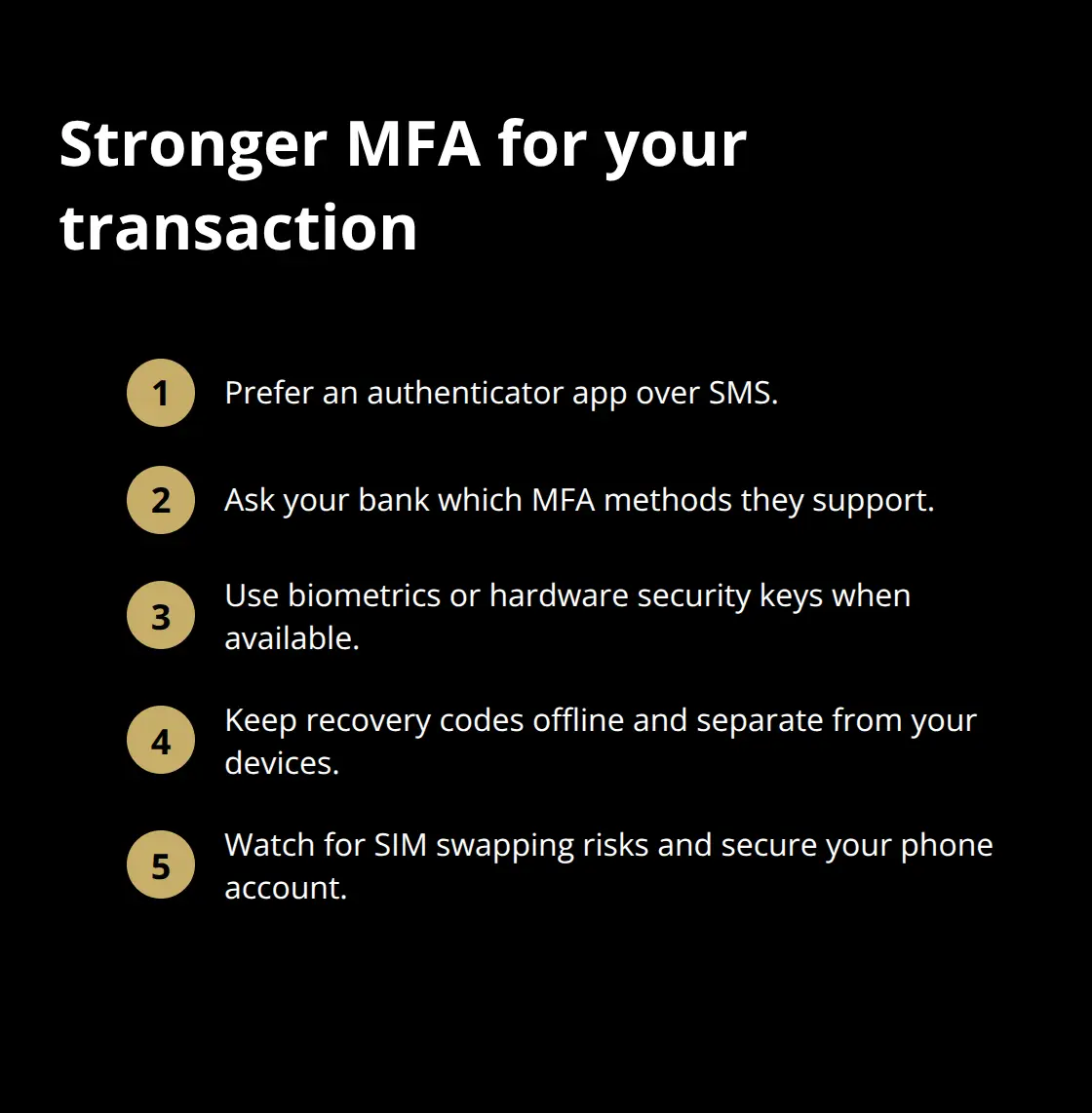

Enable Multi-Factor Authentication on Every Account

Multi-factor authentication adds a second verification step that stops account takeovers cold. Enable MFA on every email account, banking platform, and document storage service involved in your sale. This means if a criminal steals your password, they still cannot access your account without a second form of proof-typically a code from an authenticator app like Google Authenticator or Authy, or a text message to your phone. This protection significantly reduces account compromise risk compared to passwords alone.

Use an authenticator app rather than SMS when possible; text messages can be intercepted through SIM swapping, where attackers trick your phone carrier into transferring your number to a device they control. For your banking accounts specifically, contact your bank and ask what authentication methods they support. Many banks now offer biometric authentication or hardware security keys, which are more secure than app-based codes. Store recovery codes in a secure location separate from your devices-if you lose access to your authenticator app, these codes let you regain account access without waiting for customer service.

Verify Payment Instructions Through a Separate Channel

The moment a buyer sends wire instructions or payment details, verify them through a completely separate communication method. If a buyer sends wire instructions via email, call them directly using a previously known phone number to confirm those details before you authorize any transfer. Never use contact information provided in the same message requesting payment. This simple step catches most payment fraud attempts because criminals cannot intercept a phone call they didn’t initiate.

Create a protocol for payment verification before your sale reaches closing. Document who will authorize wire transfers, which accounts will receive funds, and how you will verify instructions. Share this protocol with your attorney or escrow agent so everyone follows the same process. When closing day arrives, you’ll execute a plan rather than improvise under pressure. This layer of protection is non-negotiable when you’re handling five or six figures, and it sets the stage for the legal safeguards that formalize your transaction’s security.

Legal Safeguards and Documentation Lock Down Your Sale

Escrow Services Protect Both Parties Until Closing

Escrow services hold funds and documents until both parties fulfill their obligations, eliminating the risk that one side walks away with money or ownership. When you sell a business, an escrow agent acts as a neutral third party, releasing funds only when the buyer confirms receipt of all promised assets and documentation. You don’t transfer ownership until payment clears, and the buyer doesn’t pay until they verify what they’re acquiring is legitimate.

Choose an escrow provider that specializes in business sales rather than real estate, since business transactions involve different assets and verification requirements. Ask your escrow agent to confirm they use encrypted communication for all instructions and verify wire routing details through multiple channels before transferring funds. A reputable escrow company maintains errors and omissions insurance and walks you through their verification process upfront.

Non-Disclosure Agreements Survive the Transaction

Non-Disclosure Agreements and confidentiality clauses protect your business information during negotiations, but they only work if you enforce them. A properly drafted non-disclosure agreement sets expectations and signals M&A buyers you’re well-represented when selling your company. This prevents them from disclosing financial details, customer lists, or supplier relationships to competitors.

Include specific penalties for breaches so the agreement carries real weight. A vague NDA with no consequences fails to deter misuse. Specify what information qualifies as confidential and how long the restriction lasts (typically three to five years post-closing). Have your attorney draft the NDA rather than using a template, since business-specific language matters more than generic language.

Title Verification Confirms Ownership Before Closing

Title verification and ownership confirmation happen in parallel with escrow. Your attorney should conduct a title search confirming you own all assets free and clear of liens or claims. For service businesses, transfer all client contracts and verify that non-compete agreements don’t block the buyer from serving existing customers. For product-based businesses, confirm trademark registrations, domain ownership, and inventory rights transfer to the buyer.

Document this verification in writing so there’s no dispute later about what the buyer actually acquired. Have your attorney review all closing documents at least five business days before the scheduled close date, not the day before. This timing provides space to address discrepancies without pressure.

Title Insurance Protects Against Future Ownership Claims

The buyer’s lender or investors often require title insurance for business sales, which protects against future claims against ownership. If the buyer requests it, cooperate fully since it strengthens the entire transaction’s legitimacy and reduces your liability after closing. Title insurance costs vary based on the purchase price, but the buyer typically covers this expense as part of their due diligence.

Request a preliminary title report before closing so you and the buyer understand what the insurance will and won’t cover. Some policies exclude certain asset categories or prior claims, so clarity upfront prevents disputes later. Work with your escrow agent to coordinate title insurance issuance with the final fund transfer.

Final Thoughts

Secure online transactions require action at three levels: technical protection, legal documentation, and verification discipline. You’ve now seen how phishing attacks, unauthorized access, and payment fraud threaten sellers, and you understand the specific defenses that stop them. Encrypted communication channels, multi-factor authentication, and independent verification of buyer identity eliminate most attack vectors before they reach your transaction. Escrow services, non-disclosure agreements, and title verification create a legal framework that protects both you and the buyer while establishing clear ownership transfer.

The reality is this: secure online transactions don’t happen by accident. They happen because you implement each protection layer deliberately. Verify payment instructions through a separate communication channel before you authorize any wire transfer. Require encrypted platforms for all sensitive discussions, enable multi-factor authentication on every account involved in your sale, and have your attorney, escrow agent, and buyer understand the verification process before closing day arrives (this removes improvisation and pressure from the moment when mistakes cost the most).

At Unbroker, we’ve built our platform around this principle: transparent, secure processes that protect sellers throughout the entire transaction. Whether you handle the sale yourself or work with professional support, the security measures in this guide apply to every business sale. Explore how Unbroker supports secure business sales with tools and guidance designed for sellers like you.