Selling your business is one of the biggest financial decisions you’ll make. Broker selection can make or break that outcome, yet many business owners rush through the process without spotting serious problems until it’s too late.

At Unbroker, we’ve seen countless deals derailed by brokers who hide fees, disappear when you need them, or lack the experience to actually sell your company. This guide shows you exactly what to watch for.

Hidden Fees and Unclear Pricing Structures

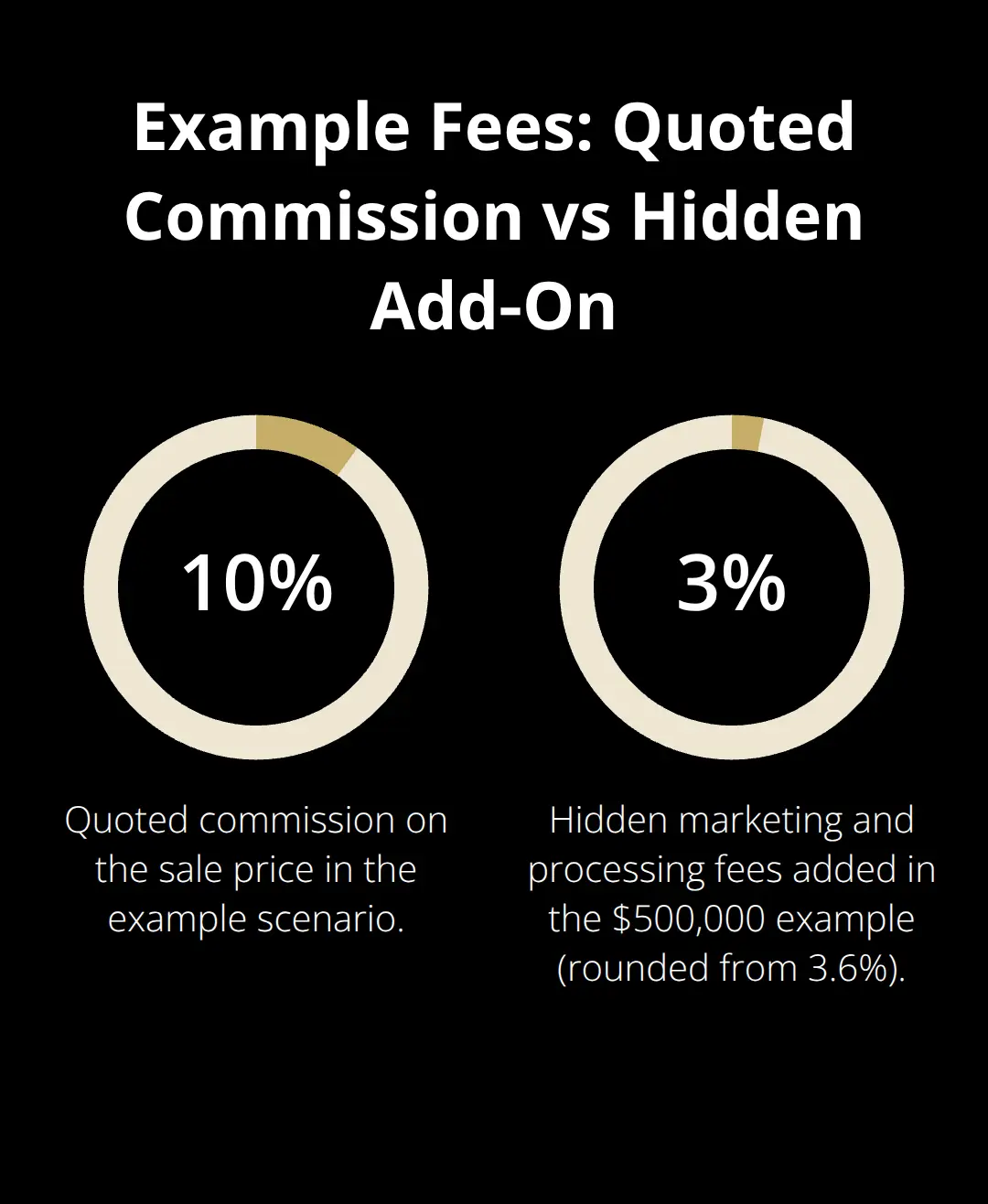

Most brokers won’t tell you upfront what you’ll actually pay. Hidden fees and unclear pricing structures are a documented concern in the industry, yet many brokers bury the full cost breakdown until you’ve already signed. A standard broker might quote you a 10% commission on the sale price, but that’s rarely the complete picture.

What Brokers Actually Charge Beyond Commission

Additional marketing fees often run $2,000 to $5,000, valuation services can cost $2,500 to $30,000 depending on the broker, and some charge transaction fees at closing that weren’t mentioned during your initial conversation. One business owner expected a 10% commission on a $500,000 sale but discovered $18,000 in hidden marketing and processing fees only after signing the engagement letter. That’s an extra 3.6% nobody anticipated.

Reputable brokers disclose everything in writing before you commit, including exact percentages, any marketing expenses, third-party costs, and when each fee gets paid. If a broker refuses to provide a written fee schedule upfront or says pricing depends on the deal structure, walk away. Transparency matters because misaligned incentives lead to bad outcomes. A broker paid only on commission has motivation to close quickly at any price. A broker charging retainers upfront might push deals that benefit them rather than you.

Commission Scales That Shift Without Warning

Watch for brokers who quote a percentage but then negotiate different terms once you’re committed. Some use tiered structures where the commission changes based on the final sale price, and they won’t spell out those tiers clearly. Others claim a Double Lehman formula (5% of the first $1 million, 4% of the second $1 million, 3% of the third $1 million, 2% of the fourth $1 million, and 1% of everything above), but then add exclusions or adjustments that weren’t explained initially.

Ask exactly how much you’ll pay if the sale closes at $500,000, $1 million, and $2 million. Get the answer in writing. Another tactic involves brokers quoting low upfront fees but then charging success fees, earnout management fees, or buyer-financing coordination fees that accumulate. The U.S. lacks standardized national licensing for business brokers, so oversight varies by state and enforcement is inconsistent. This creates an environment where questionable fee structures go unchecked.

Demand a one-page fee summary showing every cost, the exact percentage or dollar amount, and the payment schedule. If the broker resists or makes it complicated, that’s a major red flag.

New Charges Appearing After You Sign

Some brokers introduce new charges after the engagement letter is signed. A seller might discover that the broker charges extra for confidentiality agreements, additional buyer outreach, or legal document preparation that should have been included. One common trick involves charging separate fees for different phases: listing fees, marketing fees, negotiation support, and closing coordination, each billed independently.

The broker justifies this by claiming these are third-party costs, but often they’re padding their margins. Request an itemized breakdown showing which costs are truly external and which are the broker’s own charges. Confirm that core services like marketing, buyer qualification, and negotiation support are covered under the primary fee structure, not added later.

A written contract should specify exactly what’s included and what costs extra before you ever sign. If a broker starts introducing new fees during the sale process, you have grounds to renegotiate or terminate the agreement depending on your contract terms. This fee creep signals that the broker prioritizes extracting maximum revenue over serving your interests-a pattern that often continues throughout the entire transaction.

Lack of Transparency and Communication

A broker who goes silent during critical moments will sink your deal. You discover this problem only after you sign and need answers about buyer interest, negotiation strategy, or documentation deadlines. Many brokers juggle dozens of listings simultaneously, treating each seller as a transaction rather than a priority. If your broker takes three days to respond to an email about a serious buyer’s questions, the process becomes painfully slow when timing matters most.

Responsiveness during initial conversations often masks what happens once you commit. A broker who called you twice weekly before signing might vanish for two weeks after the engagement letter is executed. Test this early by asking specific questions during your vetting process and timing how long responses take. If a broker takes more than 24 hours to answer straightforward questions before you hire them, they’ll likely perform worse after you commit.

The Buyer Network That Doesn’t Exist

Many brokers keep their buyer network vague or nonexistent. They claim access to hundreds of qualified buyers but can’t name a single recent sale to a specific buyer type or explain how many buyers they’ve actually contacted for similar businesses in your industry. When you ask for proof that they have buyers ready for your deal size and sector, they deflect with claims about confidentiality or say they’ll activate their network once you list. This is backwards.

A legitimate broker tells you exactly how many potential buyers fit your profile, what industries or deal sizes they specialize in, and provides concrete examples of recent sales they’ve facilitated. Ask them to name three businesses they’ve sold in your industry within the past 18 months and provide details about those transactions. If they hesitate or refuse, their buyer network likely doesn’t exist.

Missing Timelines and Vague Processes

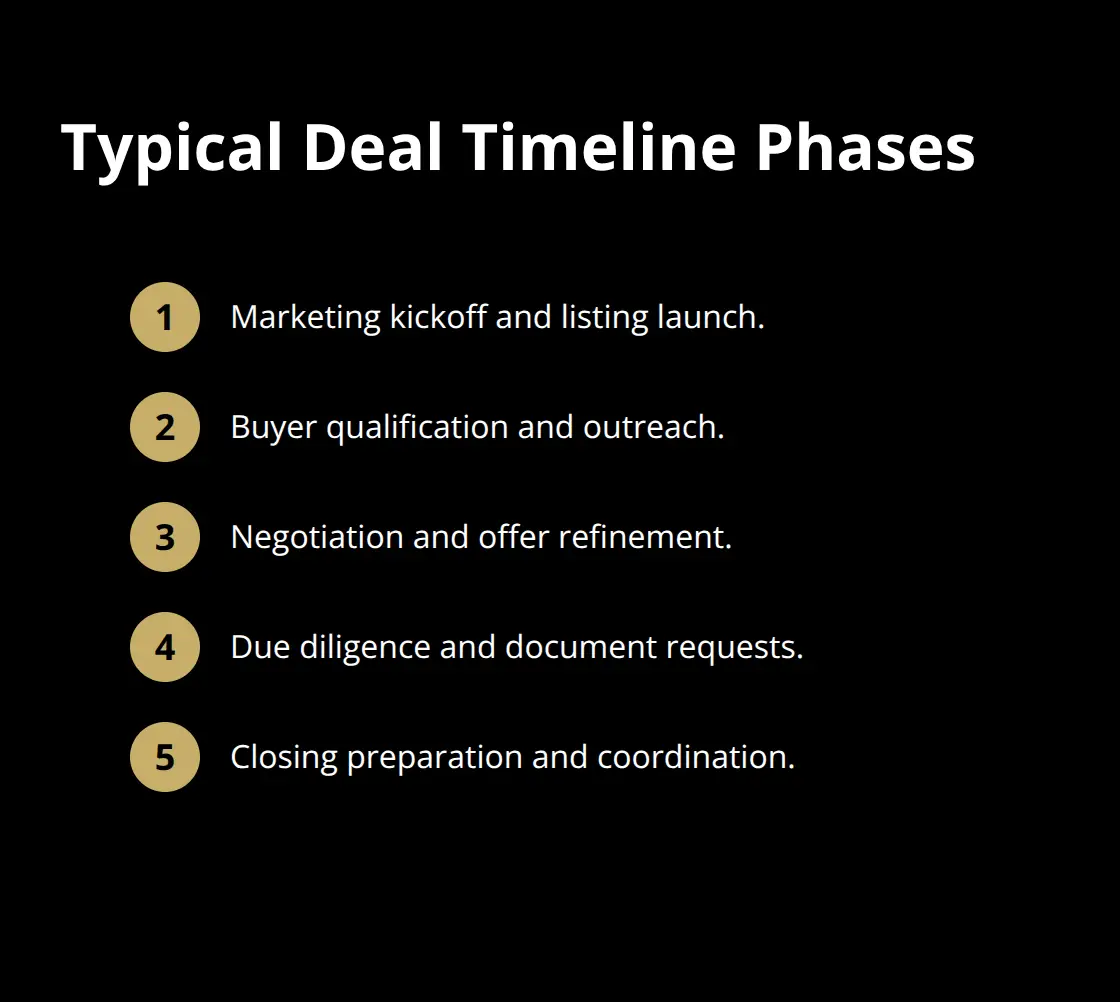

The broker’s process and timeline should be crystal clear before you sign anything. You need to know how long each phase typically takes from listing to closing, what happens if a buyer emerges, what documentation you’ll need to prepare, and when you’ll receive updates. A vague response like “we’ll keep you posted” or “it depends on the buyer” signals that the broker operates without structure.

Demand a written timeline showing estimated days for marketing, buyer qualification, negotiation, due diligence, and closing. If the broker resists putting timelines in writing or claims every deal is different so no timeline is possible, that’s a sign they lack a repeatable process.

You’ll be stuck waiting without clarity on what’s happening next. This lack of structure compounds when you move into the next critical area: evaluating whether your broker actually has the track record to back up their promises.

Poor Track Record and Credibility Issues

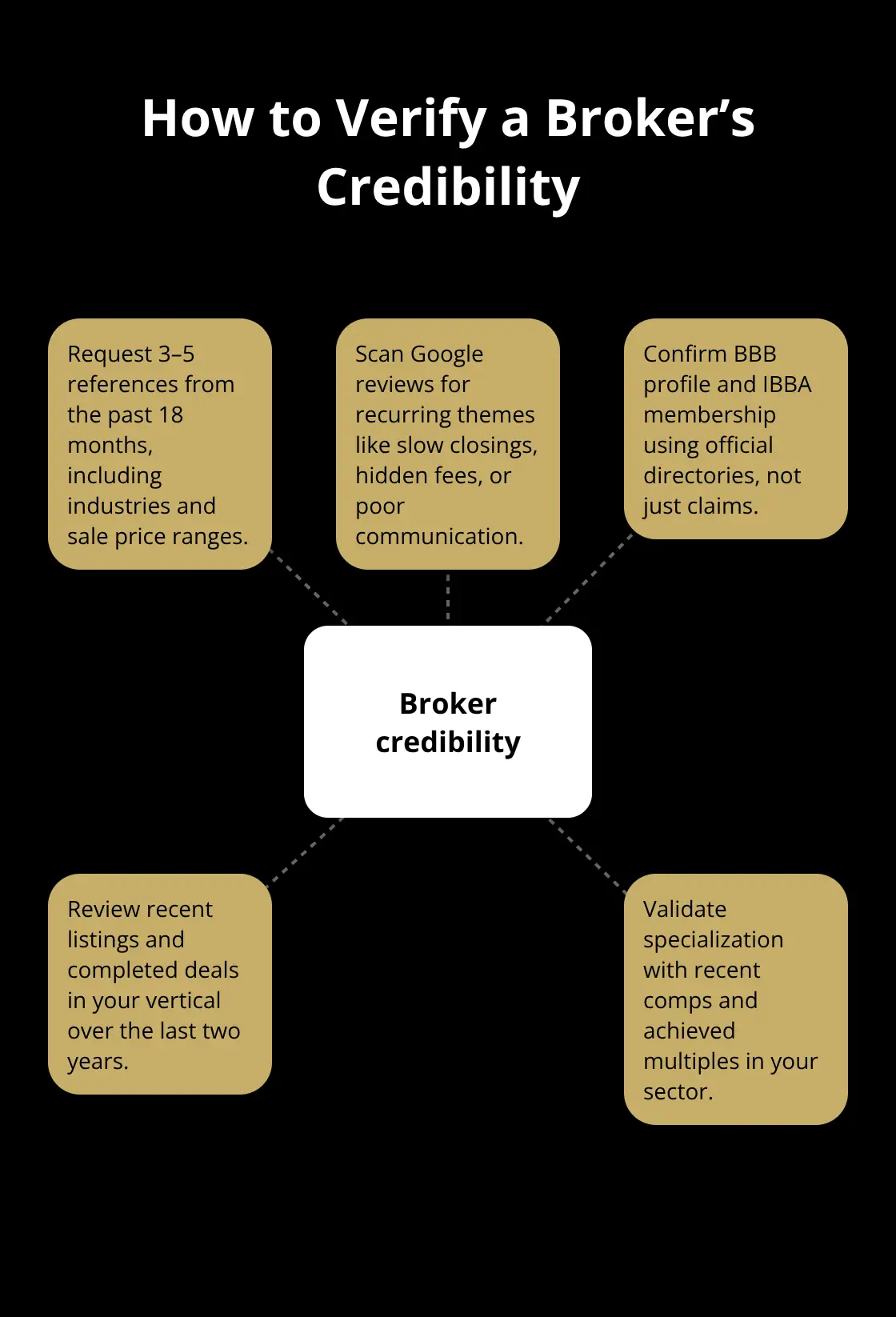

A broker without verifiable past sales asks you to trust them with your largest asset based on promises alone. When you ask for references, a legitimate broker provides contact information for three to five business owners they sold companies for within the past 18 months, along with the sale price ranges and industries involved. If a broker claims confidentiality prevents them from sharing client names, that’s a dodge. Confidentiality agreements never prevent a broker from confirming they completed a sale or introducing you to a willing reference.

Ask directly: Can you connect me with three sellers from the past year whose businesses you sold? If the answer is no, the broker either has no track record or is hiding poor results.

Verifying Sales History and References

Google reviews reveal patterns that single complaints cannot hide. Search the broker’s name plus your state and look for recurring themes. One negative review might reflect a disgruntled buyer, but three or four complaints about slow closings, hidden fees, or unresponsive communication expose systemic problems.

Check the Better Business Bureau and verify IBBA membership if they claim it. The International Business Brokers Association publishes member directories, so you can confirm whether they’re actually affiliated or just name-dropping.

Request to see their recent listings in your industry and ask how many transactions they’ve completed in your vertical over the past two years. Fewer than three deals in your specific sector signals they’re not truly specialized, regardless of what they claim.

Industry Specialization That Actually Matters

Industry specialization separates brokers who know your market from generalists who treat all businesses the same. A broker claiming expertise selling SaaS companies but whose portfolio shows mostly retail shops and restaurants lacks the knowledge to value your software business correctly or target the right buyers. Ask them to name the five most recent SaaS companies they sold, the revenue ranges, and the multiple they achieved. If they cannot answer this with specific numbers, they’re guessing on valuation.

The multiple matters enormously. Since 2019, SaaS companies have consistently traded above 20.0x EV/EBITDA, while a local service business sells for 2 to 3 times EBITDA. A broker unfamiliar with your sector will either overprice your business and scare away qualified buyers or underprice it and leave money on the table. This knowledge gap directly impacts your final sale price and the speed at which you close. Accurate financial records and transparency about known issues are what serious brokers expect from sellers-and what you should expect from them in return.

Final Thoughts

Red flags in broker selection appear early if you know what to look for. Hidden fees buried in fine print, communication that vanishes after signing, and track records that don’t hold up under scrutiny expose patterns that repeat across bad brokers. The common thread remains misaligned incentives-when a broker prioritizes their commission over your outcome, corners get cut and problems compound.

Your broker selection determines whether you sell quickly at fair value or watch months slip by while your business sits unsold. Vetting takes time upfront but saves you thousands in wasted fees and lost opportunity. Ask for written fee schedules, demand verifiable references from recent sales in your industry, and test responsiveness before you commit.

We at Unbroker offer a modern alternative with transparent pricing starting at $485 upfront and $4,500 after your sale closes, eliminating the bloated commissions that drain value from your deal. You get access to a vast buyer network, professional marketing materials, legal document templates, and negotiation support without hidden charges appearing mid-transaction. The best broker selection comes down to finding someone who answers your questions directly, proves their track record with specific examples, and charges fairly for the work they do.