Selling a business you’ve built from the ground up triggers real anxiety. The exit fear is understandable-you’re not just handing over a company, you’re letting go of years of work and identity.

At Unbroker, we’ve seen countless founders struggle with this decision. The good news is that preparation and the right guidance make the process manageable.

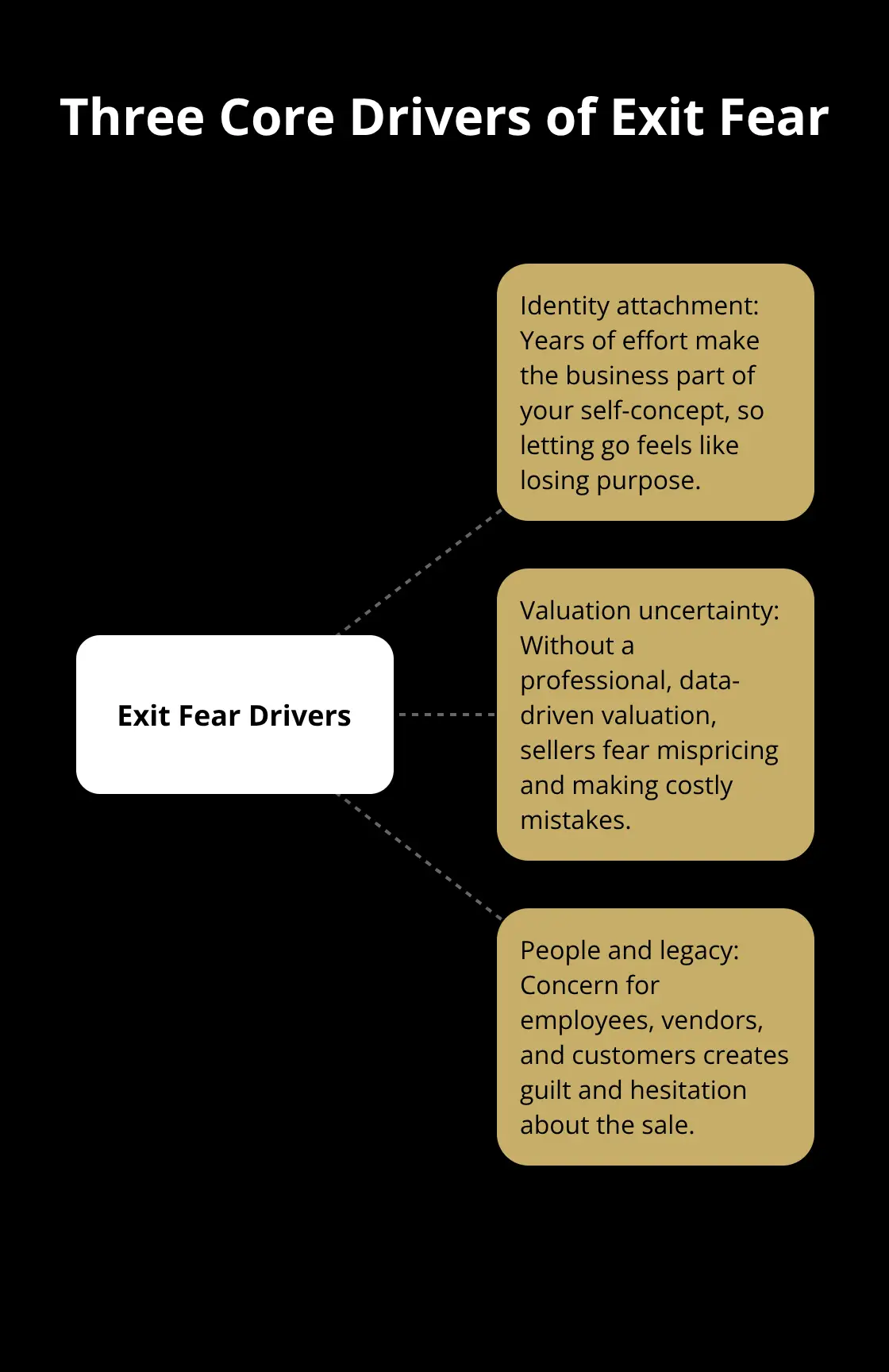

Why Sellers Really Fear Letting Go

The fear of selling your business isn’t abstract-it’s rooted in three concrete realities that keep founders awake at night. First, your business has become inseparable from who you are. Entrepreneurs typically spend 50 to 60 hours per week on their companies, according to data from the Small Business Administration. That’s more time than most people spend with their families. Over years or decades, the business becomes your identity, your daily purpose, and your sense of accomplishment. Letting go means redefining yourself entirely.

Second, you face genuine uncertainty about what your business is actually worth. Most sellers either overestimate value by 30 to 40 percent based on emotional attachment or underestimate by accepting the first offer out of fear. Without a professional valuation grounded in real market data and comparable sales, you’re essentially guessing. Sidharth Ramsinghaney, Director of Strategy and Operations at Twilio, emphasizes that professional valuation establishes a realistic price range and prevents the costly mistake of misaligned expectations. Third, you worry about what happens to the people who depend on your business. You’ve built relationships with employees, trusted vendors, and loyal customers. A sale threatens their security and stability, which creates real guilt and hesitation.

Your Identity Is Not Your Business

The attachment runs deep because you’ve invested years of mental and emotional energy into building something from nothing. But here’s the hard truth: clinging to the business for the sake of identity keeps you trapped. Founders who separate their self-worth from their company’s ownership actually make better decisions during the sale process. They negotiate more confidently because they’re not defending their life’s work-they’re executing a transaction. The reframe matters. Instead of thinking about selling as losing yourself, think about it as graduating to a new chapter where you have options. You can consult, invest in other ventures, pursue a passion project, or simply rest. None of those paths remain available if you’re still running the business.

Valuation Uncertainty Paralyzes Decision-Making

Without concrete numbers, fear takes over. Prepare three years of financials in advance, including normalized EBITDA with clear add-backs and detailed customer retention analytics, according to Ramsinghaney’s guidance from the Twilio exit process. This documentation gives you and potential buyers a shared reality. A professional valuation before you list the business anchors your expectations. Use EBITDA-based pricing and industry multiples as your foundation. A business that generates $500,000 in annual EBITDA values reasonably based on the multiples in your industry. That’s the conversation you should have with advisors, not a number you invented because you feel the business deserves more.

The Employee and Legacy Question

Your employees didn’t sign up for a sale, and that creates real responsibility. Communicate strategically: inform key employees after you’ve signed an NDA with serious buyers, not during early marketing. Time disclosures to protect both deal value and morale. Document your company culture, values, and operating systems in writing so the new owner can maintain continuity. Many founders negotiate earn-outs or advisory roles that let them stay involved after closing, reducing the sense of complete loss while protecting their legacy. These arrangements also signal to potential buyers that you stand behind the business and its people, which strengthens their confidence in the transition ahead.

What Sellers Get Wrong About Price, Paperwork, and Communication

Most founders sabotage their exit before a single buyer even sees the business. The mistakes aren’t subtle or forgivable-they’re costly. The first trap is pricing without market reality. Founders anchor to an imaginary number based on what they think their business should be worth rather than what buyers will actually pay. Sidharth Ramsinghaney at Twilio found that sellers typically overshoot market value by 30 to 40 percent, which kills deal momentum immediately. Buyers spot inflated pricing in the first conversation and either walk away or use it as leverage to negotiate hard during due diligence.

Price Your Business on Market Data, Not Emotion

A professional valuation before listing establishes your realistic range. Use EBITDA multiples specific to your industry as your floor, not your ceiling. If comparable businesses in your space sell at 4 to 6 times EBITDA, and your business generates $400,000 in annual EBITDA, your realistic range is $1.6 to $2.4 million. Anything above that requires documented justification through proprietary technology, exclusive contracts, or exceptional growth rates. Without this grounding, you’ll spend months marketing an overpriced asset while qualified buyers move to other opportunities.

Organize Your Financial Records Before Buyers Ask

The second critical mistake is showing up unprepared with financial records. Buyers today are sophisticated and demand transparency. Start by gathering financial statements for the past three to five years, review revenue streams, margins, and expenses, and clarify any accounting adjustments you’ve made. Many founders scramble to compile this during due diligence, which signals either poor management or something to hide. Both assumptions kill buyer confidence and tank valuation.

Separate personal expenses from business expenses, document recurring revenue versus one-time sales, and maintain clear records. Crystal Stranger, CEO of Optic Tax, emphasizes that tax history matters deeply-maintain solid records and prepare extra years of returns for due diligence to avoid penalties or delays. Buyers will request this information anyway, so having it ready accelerates the process and demonstrates professional management.

Share Information Strategically, Not Recklessly

The third mistake is failing to communicate with buyers in a structured way. Founders either overshare confidential information early out of eagerness, or they stay so guarded that buyers can’t assess the business properly. The middle ground is the answer. Share enough detail to prove the business works, but require NDAs before discussing sensitive metrics. Provide a clear narrative around growth initiatives, customer acquisition costs, and retention rates.

Many sellers hide operational weaknesses or strategic challenges, which buyers inevitably uncover during diligence. When they find undisclosed issues, they either withdraw or use them to slash the offer. Transparency about challenges actually builds trust if you frame them alongside solutions you’ve tested or improvements you’ve made. This approach signals confidence in the business and prevents the buyer from feeling blindsided later.

The path forward requires honest assessment of your numbers, your records, and your communication strategy. Once you address these three areas, you’re ready to navigate the actual sale process with real leverage and credibility.

Ready Your Business and Yourself for Sale

Selling your business demands more than hoping a buyer shows up. The preparation phase separates founders who walk away satisfied from those who regret their decision. Start by documenting every system and process your business runs on. Most founders operate intuitively after years of building, which means critical knowledge exists only in their heads. Write down how customer onboarding works, how you handle billing disputes, what triggers a refund, how vendors get paid, and how decisions get made when something breaks. This documentation serves two purposes: it proves to buyers that your business can operate without you, and it protects your legacy by ensuring the new owner can maintain what you built.

Document Your Operations Before Listing

Sidharth Ramsinghaney at Twilio recommends developing a structured 100-day transition plan that covers customer communication, employee retention, and operational integration. Start this documentation now, not when you’re actively selling. Buyers will request operational manuals, process flows, and decision trees during due diligence. Having this ready demonstrates professional management and accelerates the entire process. The documentation also reveals which parts of your business depend too heavily on you personally-information that helps you strengthen those areas before potential buyers spot the weakness.

Get a Professional Valuation Before You List

A professional valuation grounds your expectations in market reality rather than emotion or wishful thinking. Work with a valuation expert who understands your industry and can justify their numbers using comparable sales and EBITDA multiples. The valuation process also identifies gaps in your financial records or operational metrics that buyers will scrutinize anyway. You’ll learn which parts of your business add value and which ones don’t, which means you can focus your final months of operation on strengthening what matters. This step is non-negotiable if you want to avoid the common trap of pricing yourself out of the market.

Assemble Your Advisory Team Now

You need a transaction lawyer who handles business sales, an accountant familiar with tax implications of your exit, and ideally a broker or business advisor who knows your industry. These advisors aren’t luxury-they’re insurance against costly mistakes. John Silvestri, General Counsel at Craveworthy Brands, emphasizes that strategic communication with key employees and customers requires careful timing and confidentiality agreements. Your advisors help you navigate this minefield and handle the emotional weight of the sale, which matters more than most founders realize.

You’ll face moments of doubt, pressure from buyers to lower your price, and anxiety about what comes next. Having trusted professionals in your corner lets you step back, breathe, and make rational decisions instead of reactive ones. Start assembling this team before you need them urgently.

The right advisors also know which platforms and services can streamline your sale process-whether that’s a broker, a modern platform with transparent fees, or a combination of both. What matters is that you have experienced people who’ve guided other founders through this exact situation.

Final Thoughts

Selling your business ranks among the biggest decisions you’ll make as a founder. The exit fear you feel is legitimate, but it shouldn’t paralyze you. You’ve already proven you can build something valuable from nothing, and executing a well-planned sale is simply the next skill to master.

The path forward is clear: document your operations, obtain a professional valuation, and assemble advisors who’ve guided other founders through this exact process. These three steps transform selling from an emotional crisis into a structured transaction. When you separate the business from your identity, ground your price in market data, and communicate transparently with buyers, the anxiety loses its grip.

Selling your business opens doors that staying closed off never will-financial freedom to invest in new ventures, time to pursue interests you’ve postponed, or simply the ability to rest without guilt. Start now by gathering your financial records, reaching out to a valuation expert, and beginning to document your systems. If you want support navigating the sale with transparent fees and expert guidance, Unbroker offers modern tools and advisory support designed specifically for business owners like you.