Business valuations are where fraud happens most often. Sellers inflate numbers, hide debts, and use accounting tricks to make their companies look worth far more than they actually are.

At Unbroker, we’ve seen buyers lose millions because they didn’t catch these red flags early. The good news is that valuation fraud is preventable if you know what to look for.

What Makes Financial Records Look Fraudulent

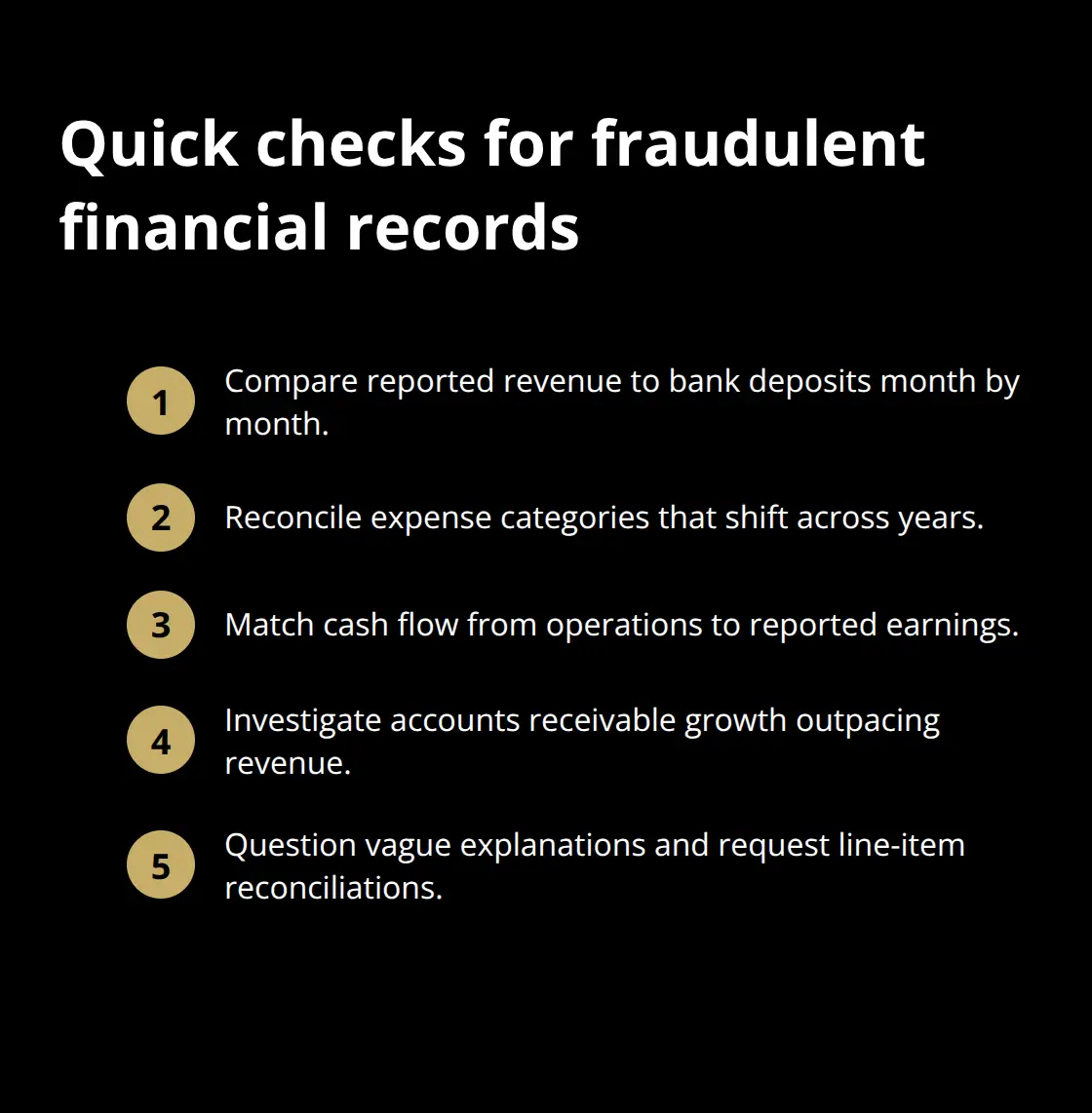

Inconsistent financial records signal that something is wrong. When revenue numbers don’t match bank deposits, when expenses appear in different categories across years, or when cash flow diverges from reported earnings, you’re looking at a potential fraud situation.

The Association of Certified Fraud Examiners found that businesses with weak internal controls experience median losses to fraud. Sellers rationalize these inconsistencies as accounting quirks or one-time adjustments, but vague explanations should trigger skepticism. Ask the seller to reconcile specific line items between their tax returns, bank statements, and accounting records. If accounts receivable grows faster than revenue, that’s a red flag-it suggests the seller recognized sales that customers haven’t actually paid for. Days sales outstanding (DSO) should remain relatively stable year over year. A jump from 30 days to 60 days without explanation means customers aren’t paying, which indicates the revenue quality is deteriorating.

Revenue That Doesn’t Match Supporting Documents

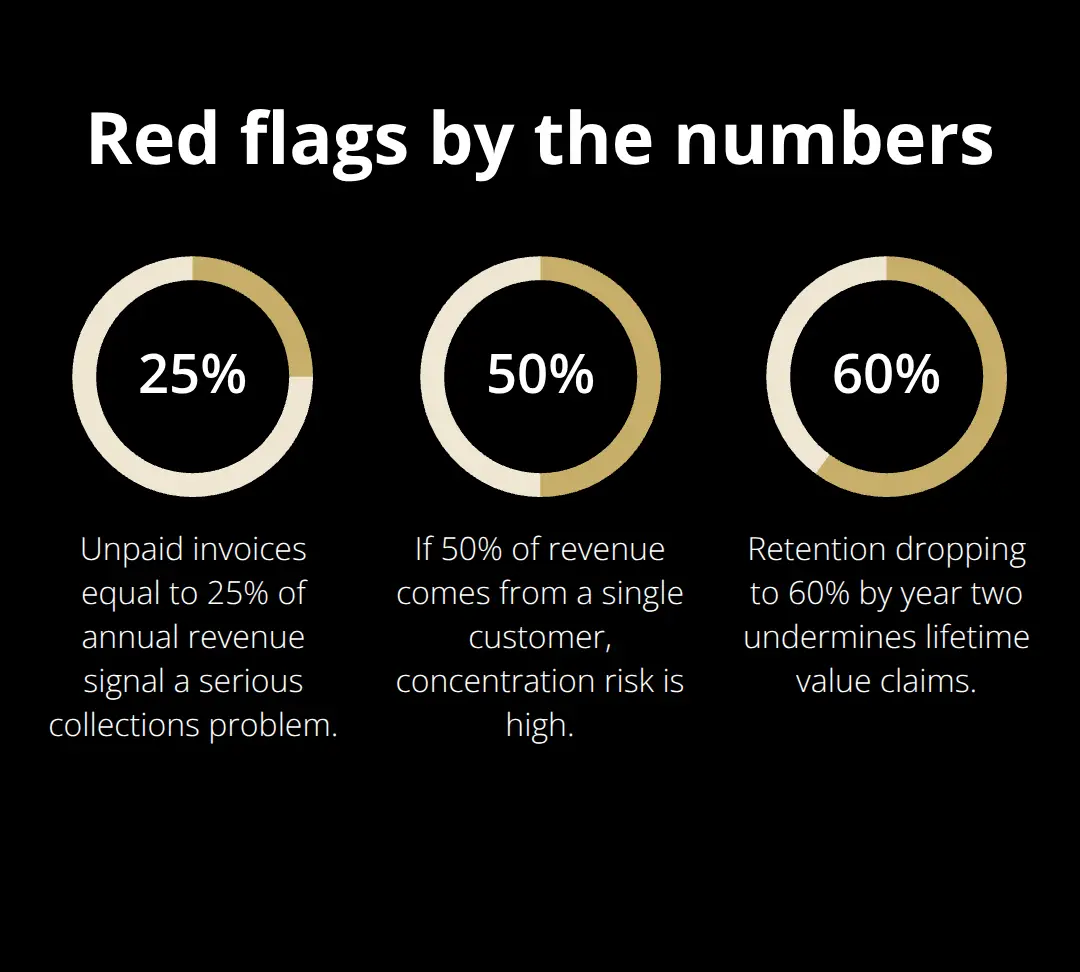

Inflated revenue claims boost valuation multiples directly. A seller claiming $1 million in annual revenue instead of $750,000 artificially inflates business value by 30% or more, depending on the multiple applied. Demand to see actual customer contracts, invoices, shipping records, and payment receipts for the largest revenue transactions. Verify that revenue spikes near reporting periods aren’t artificial-channel stuffing and bill-and-hold schemes are real tactics where sellers pressure customers to purchase early or accept goods they don’t yet need. Cross-check revenue figures against your own industry benchmarks. If a competitor with similar operations reports half the revenue, that’s worth investigating. Look at customer concentration too. If 50% of revenue comes from a single customer, the business is fragile, and that customer might not stay after the sale.

Valuation Methods That Don’t Add Up

Sellers sometimes use unconventional valuation approaches to justify inflated asking prices. EBITDA multiples are popular shortcuts, but they’re dangerous if applied blindly. A seller might claim a 10x EBITDA multiple because they found one comparable company that sold at that rate, ignoring the fact that the comparable company is twice the size, operates in a different market, or benefited from deal-specific synergies. Apply size and risk adjustments. A private company should trade at a lower multiple than a public company because it carries more risk and less liquidity. Revenue multiples without any consideration of profitability are also red flags. A $5 million revenue business at a 3x revenue multiple is worth $15 million only if the business actually generates sufficient cash flow to justify that valuation.

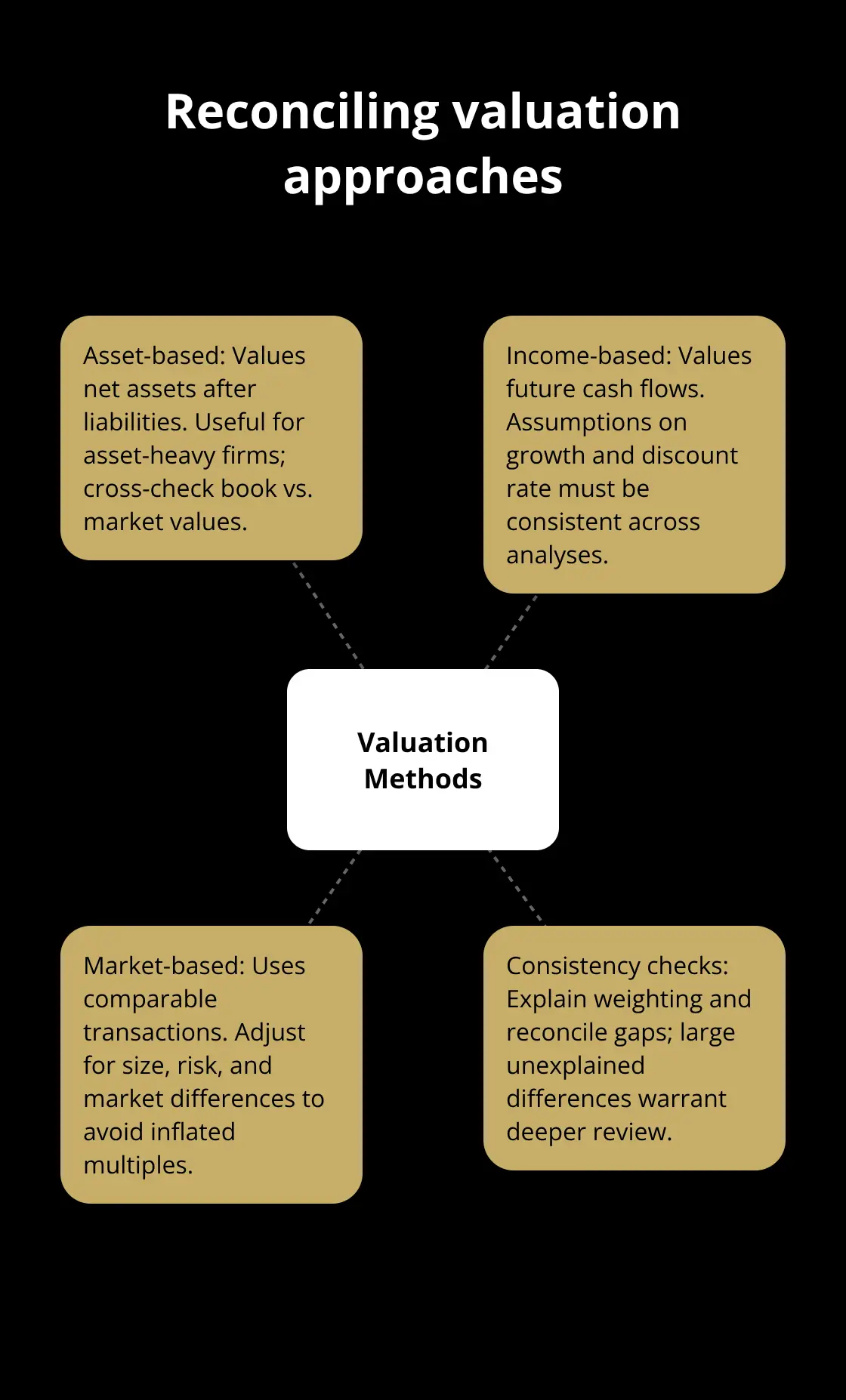

Spotting Inconsistencies Across Valuation Methods

Request the seller’s valuation report and check whether they used consistent assumptions across all three approaches-asset-based, income-based, and market-based. Inconsistencies between methods signal either sloppy work or intentional manipulation.

When you compare the three valuations, large gaps (especially when one method produces a significantly higher result) warrant deeper investigation. The seller should explain why they weighted one method more heavily than another and provide clear documentation for each calculation. If the seller can’t reconcile the differences or dismisses them as normal variation, that’s a warning sign. A credible valuation shows how all three methods support a defensible range, not three wildly different numbers presented without justification.

What Happens When You Miss These Red Flags

Buyers who overlook these inconsistencies often discover problems after closing. A valuation error of 20% to 30% isn’t uncommon when fraud goes undetected, which means you could overpay by hundreds of thousands of dollars. The financial discrepancies that inflate valuation also create operational problems post-acquisition-hidden liabilities emerge, customer relationships deteriorate, and cash flow falls short of projections. These issues compound quickly and can threaten the viability of your investment. The next section covers how to verify business financials through systematic checks that catch these problems before you commit capital.

How to Verify Business Financials

Request Tax Returns and Bank Statements

Start with tax returns and bank statements covering at least three to five years. These documents don’t lie the way seller spreadsheets do. Compare the tax return revenue to bank deposits month by month. If a seller claims $2 million in annual revenue but tax returns show $1.5 million, you’ve found your first problem. Request bank statements directly from the bank, not from the seller’s accounting software. Fraud often involves doctored internal records that don’t match bank reality.

Analyze Accounts Receivable and Cash Flow

Cross-check accounts receivable aging reports against revenue claims. When a business shows $500,000 in unpaid invoices but only $2 million in annual revenue, that’s a 25% collection problem that will hit you after closing. Look at cash flow statements specifically.

A seller might report strong net income while actual cash from operations declined. This gap signals either inflated revenue or hidden expenses. Compare year-over-year numbers for consistency. If gross margins jumped from 35% to 55% without explanation, demand specifics. Real margin improvements come from operational changes you can verify, not accounting adjustments.

Hire Independent Auditors and Forensic Accountants

Independent audits from CPAs carry weight because auditors have liability and professional standards to maintain. A business that’s been audited annually is far less likely to contain major fraudulent claims than one relying on internal bookkeeping. When audits exist, request the full audit report including any management letters or notes about internal control weaknesses. These letters often flag problems the seller would prefer to hide. For businesses without formal audits, hire a forensic accountant to review the last three years of records. Forensic accountants specialize in finding manipulation and typically cost $5,000 to $15,000 depending on complexity, which is cheap insurance against a million-dollar mistake.

Benchmark Against Industry Standards

Benchmark the business against industry peers using metrics like gross margin, operating expense ratios, and return on assets. If the seller’s business shows a 50% gross margin while industry average is 35%, investigate why. Sometimes there’s a legitimate reason. Often there isn’t. Trade associations and industry databases provide these benchmarks. The SBA and various industry groups publish profitability standards by sector. A business that outperforms industry norms dramatically should raise questions about data accuracy rather than celebration. These verification steps reveal whether the seller’s financial claims hold up under scrutiny, but they only work if you know what specific fraud tactics to watch for in the valuation itself.

How Sellers Manipulate EBITDA and Hide Real Costs

The EBITDA Add-Back Problem

Sellers inflate EBITDA by adding back non-recurring expenses and claiming one-time revenue that won’t repeat. A seller might report $500,000 in EBITDA by adding back a $100,000 legal settlement, $50,000 in consultant fees they claim were for a special project, and $75,000 in owner perks like a company car or travel that they say a new owner wouldn’t need. The problem is that many of these add-backs are actually recurring. That consultant might still be needed. The legal issues might resurface. The owner perks might transform into salary increases or benefits for new management.

When you apply a 6x EBITDA multiple to inflated EBITDA, you pay for value that doesn’t exist. Demand itemized add-backs with documentation. Ask whether each add-back truly won’t recur under new ownership.

Verifying Add-Backs Against Tax Records

If the seller can’t produce receipts or contracts proving the expense happened, it shouldn’t count as an add-back. Cross-check add-backs against tax returns. The IRS Form 1120 doesn’t allow sellers to deduct phantom expenses, so if an add-back doesn’t appear on the tax return, it’s likely fabricated. This simple verification catches most EBITDA manipulation schemes before they inflate your purchase price.

Uncovering Hidden Liabilities

Hidden liabilities destroy post-acquisition value faster than any other fraud tactic. A seller might omit pending lawsuits, unpaid vendor invoices, lease obligations, or tax liabilities from their balance sheet. You inherit these problems the moment you close. Request a complete list of all debt, including equipment leases, vendor payment plans, and deferred compensation owed to employees. Verify against the balance sheet and cross-check with credit reports and UCC filings. These steps reveal obligations the seller hoped you wouldn’t find.

Exposing Customer Economics Fraud

Customer acquisition cost and lifetime value manipulations are equally damaging. A seller might claim customers cost $500 to acquire and generate $5,000 in lifetime value, justifying a 10x customer value multiple. Reality often differs sharply. Request actual customer data showing how many customers the business acquired in the past 24 months, total acquisition spending, and actual retention rates. Calculate the real payback period by dividing total customer acquisition spend by annual revenue from new customers. If acquisition costs exceed 30% of first-year customer revenue, the unit economics are weak and the valuation is overstated. Demand proof that customer lifetime value projections rest on actual cohort data, not assumptions. Sellers frequently project 5-year retention when real retention drops to 60% by year two.

Final Thoughts

Valuation fraud follows predictable patterns that systematic verification catches before you close. Sellers who manipulate financials leave traces in mismatched bank statements, undocumented add-backs, and metrics that diverge from industry norms. You stop overpaying by demanding original documents from banks and tax authorities, hiring a forensic accountant to review three to five years of records (typically costing $5,000 to $15,000), and benchmarking every financial metric against industry standards.

Due diligence separates buyers who lose millions from those who make confident acquisition decisions. You protect yourself by asking sellers to explain any significant deviations from industry norms and verifying that add-backs actually won’t recur under new ownership. This investment in verification prevents you from inheriting hidden liabilities, inflated EBITDA claims, and manipulated customer economics that destroy value after closing.

We at Unbroker built our platform to remove the pressure to hide problems and the incentive to inflate valuations. Unbroker connects buyers and sellers through straightforward options with no hidden fees, giving both parties access to clean, verified information. Apply the verification methods in this guide, trust your skepticism when numbers don’t add up, and you’ll make acquisition decisions based on honest financials and fair value.