Exiting a husband-and-wife cleaning business can be a complex process, filled with emotional and financial challenges. At Unbroker, we’ve seen many couples navigate this transition successfully with the right approach.

This guide will walk you through creating an exit strategy for your husband-and-wife cleaning business, ensuring a smooth transition for all parties involved. We’ll cover everything from preparing for the exit to managing the transition, helping you protect your legacy and secure your financial future.

Preparing Your Business for Sale

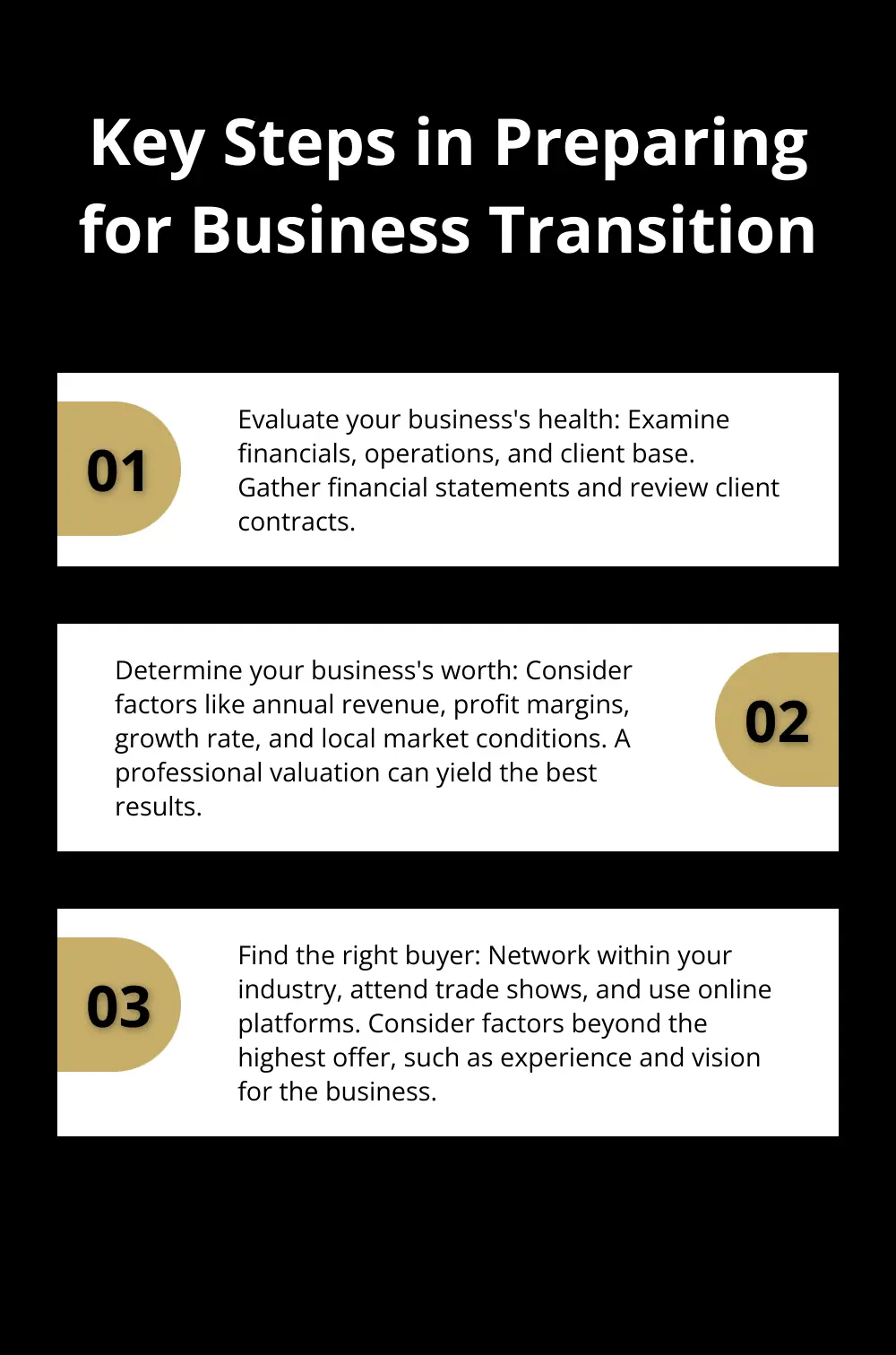

Evaluating Your Business’s Health

The first step in exiting a husband-and-wife cleaning business involves a thorough assessment of your company’s current state. This process requires a close examination of your financials, operations, and client base. Gather the last three years of financial statements, including profit and loss statements, balance sheets, and cash flow reports. It typically takes six to twelve months to sell a business, but there are many variables between individual businesses.

Next, review your client contracts. How many are long-term? What’s your client retention rate? Cleaning businesses with a high percentage of recurring revenue attract more buyers. The American Cleaning Institute reports that businesses with over 80% recurring clients often command higher sale prices.

Don’t overlook your equipment and vehicles. Are they in good condition? Up-to-date maintenance records can increase your business’s value. The National Cleaning Association suggests that well-maintained equipment can boost a cleaning business’s valuation by up to 15%.

Determining Your Business’s Worth

Putting a price tag on your business is a critical step. While general rules of thumb (such as 2-3 times annual profit for small cleaning businesses) exist, a professional valuation often yields the best results. Sellers can gain significant value when they plan ahead for the sale.

Consider factors like your annual revenue, profit margins, growth rate, and local market conditions. A business that has grown at 10% annually for the past three years presents a strong selling point. The Small Business Administration reports that cleaning businesses with consistent growth rates above 7% tend to sell faster and at higher multiples.

Finding the Right Buyer

Identifying potential buyers plays a crucial role in a successful exit. Your ideal buyer might be a competitor looking to expand, an individual seeking to enter the industry, or even one of your employees. Exit planning is crucial, as sometimes no potential buyer seems good enough to purchase and run your business.

Start by discreetly networking within your industry. Attend trade shows, join professional associations, and use online platforms designed for business sales. (Unbroker’s vast network of pre-qualified buyers can significantly expand your reach, increasing your chances of finding the perfect match for your business.)

The right buyer isn’t just about the highest offer. Consider factors like their experience in the industry, their vision for the business, and how they plan to treat your employees and clients. A smooth transition often depends on finding a buyer who aligns with your business values and can maintain the quality of service your clients expect.

With your business thoroughly prepared, accurately valued, and potential buyers identified, you’ve laid a solid foundation for your exit strategy. The next crucial step involves navigating the legal and financial considerations that come with selling a husband-and-wife cleaning business.

Navigating Legal and Financial Hurdles

The sale of a husband-and-wife cleaning business involves complex legal and financial considerations. Proper planning can significantly impact the success of your exit strategy.

Examining Partnership Agreements

Start with a thorough review of your partnership agreement. This document outlines the structure of your business relationship with your spouse. Focus on clauses related to dissolution, asset division, and dispute resolution. If a formal agreement doesn’t exist, create one immediately. As business partners, you and your ex are responsible for any debts, taxes, and other business liabilities and agreements that were entered into as a business.

Review client contracts as well. Identify any clauses that might activate due to ownership changes. Some contracts may allow clients to terminate services if the business changes hands. Address these issues early to prevent the loss of valuable clients during the transition.

Obtaining Professional Advice

Professional guidance proves invaluable during this process. A business attorney who specializes in small business sales can help you navigate complex legal issues. They can draft sales agreements, handle negotiations, and ensure compliance with local regulations.

A certified public accountant (CPA) experienced in business sales provides essential financial advice. Accountants can help streamline financial processes, minimize risks, and provide valuable insights to drive business growth and success.

Understanding Tax Implications

The tax consequences of selling your business can significantly impact your profits. The structure of your sale – whether it’s an asset sale or a stock sale – affects your tax bill. The sale of capital assets results in capital gain or loss. The sale of real property or other assets may result in ordinary income or loss.

Consider the timing of your sale. A sale at the beginning of a tax year provides more time to plan for the tax impact. Be aware of potential capital gains taxes. If you’ve owned the business for more than a year, you might qualify for long-term capital gains rates, which are typically lower than ordinary income tax rates.

Preparing for the Transition

As you navigate these legal and financial hurdles, start preparing for the actual transition of your business. This process involves more than just paperwork and numbers – it requires careful planning to ensure a smooth handover to the new owners.

How to Manage the Transition When Selling Your Cleaning Business

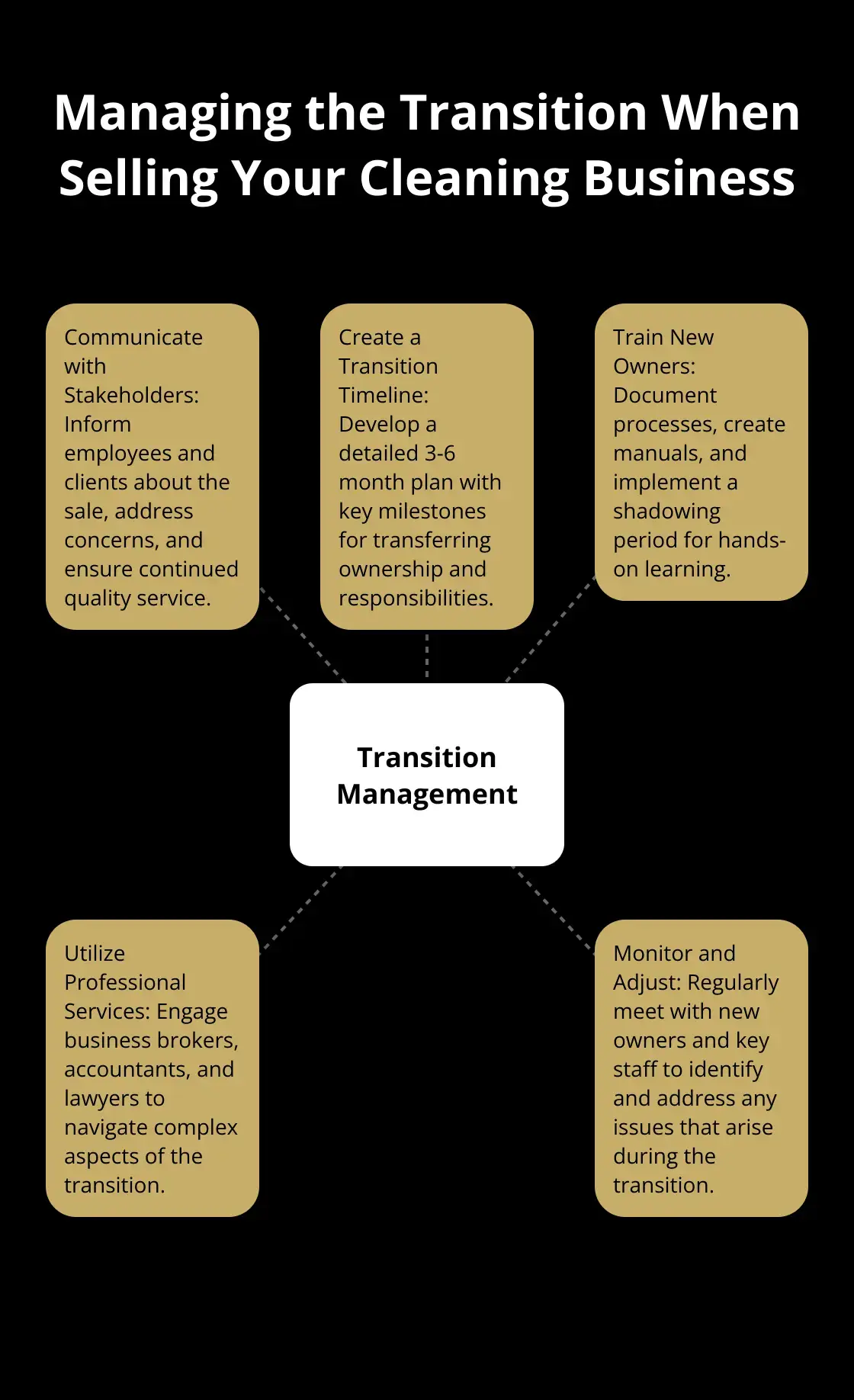

Communicate with Stakeholders

Open and honest communication forms the backbone of a successful ownership transition. Inform your employees about the sale first. The Society for Human Resource Management reports that 71% of employees who experience poor communication during organizational changes will likely leave within a year. To prevent this exodus, schedule a meeting to explain the situation, address concerns, and discuss how the sale might affect their roles.

Next, contact your clients. Customized communication and service help clients feel recognized and appreciated, which builds loyalty. Draft a letter to explain the change in ownership, assure them of continued quality service, and introduce the new owners. Follow up with phone calls to key clients to address any questions personally.

Create a Transition Timeline

Develop a detailed timeline for the transfer of ownership. The Small Business Administration recommends a transition period of 3-6 months for small service businesses. This timeline should include key milestones such as:

- Finalize the sale agreement

- Transfer licenses and permits

- Update insurance policies

- Change bank accounts and credit cards

- Transfer utility bills and vendor contracts

Assign responsibilities for each task and set deadlines. Regular check-ins with the buyer will help ensure everything stays on track.

Train the New Owners

Proper training of the new owners or management team is essential for a smooth transition. SHRM data revealed that 76 percent of surveyed employees are willing to stick with a company that offers continuing learning and development opportunities.

Start by documenting your operational processes. Create detailed manuals covering everything from cleaning techniques to client communication protocols. Spend time working alongside the new owners, demonstrate your methods and introduce them to key clients and vendors.

Consider implementing a shadowing period where the new owners can observe and learn from you in real-time. This hands-on approach can significantly reduce the learning curve and maintain service quality during the transition.

Utilize Professional Services

Professional services can streamline the transition process. Business brokers (like Unbroker) offer valuable expertise in managing the sale and transition of small businesses. They can provide tools and resources to facilitate the process, ensuring both sellers and buyers are well-prepared for the ownership change.

Accountants and lawyers specializing in business transitions can also offer invaluable assistance. They can help navigate complex financial and legal issues (such as tax implications and contract transfers), reducing the risk of costly mistakes.

Monitor and Adjust

Throughout the transition process, monitor progress closely and be prepared to adjust your approach as needed. Regular meetings with the new owners and key staff members can help identify and address any issues that arise. This flexibility can make the difference between a smooth transition and a rocky one.

Final Thoughts

Exiting a husband-and-wife cleaning business requires careful planning and clear communication. You must assess your business’s health, determine its value, and identify potential buyers to lay the groundwork for a smooth transition. Professional guidance can make a significant difference in this process.

We at Unbroker offer valuable resources and support for business sellers. Our platform combines modern technology with expert assistance to streamline the sale process and connect you with qualified buyers. Our services can help you navigate the complexities of selling your business effectively.

A well-executed exit strategy for a husband-and-wife cleaning business not only benefits you as the seller but also ensures the continued success of the business you’ve built. You set up your cleaning business – and its new owners – for future success when you take the time to plan and implement a thoughtful exit (this approach protects your interests and preserves the value of your hard work).