Selling your business is one of the biggest financial decisions you’ll make. Without a clear exit planning checklist, you risk leaving money on the table or missing critical deadlines.

We at Unbroker have helped hundreds of business owners prepare for sale. This guide walks you through the exact steps to maximize your business value and close the deal faster.

Assess Your Business Value and Readiness

Getting an accurate valuation is where most owners fail. Too many business owners either overestimate what their company is worth or accept the first number they hear without verification. A professional valuation forms the foundation of your entire exit strategy. When you know what your business is actually worth, you set realistic asking prices, identify which improvements will move the needle, and negotiate from a position of strength.

Get a Professional Business Valuation

A valuation professional with real M&A deal experience assesses your business using multiple methods: comparing your financials to similar businesses that sold recently, analyzing your cash flow, and evaluating your competitive position. Expect the valuation to be a range rather than a single number. Market conditions, buyer perspectives, and industry trends shift perceived value depending on who’s buying. You need someone who understands your specific industry and has closed comparable deals, not just someone with generic valuation credentials.

Review Financial Records and Tax Returns

Your financial statements are the first thing serious buyers examine. If your bookkeeping is messy, if unexplained expenses appear, or if your records don’t match your tax returns, buyers will either walk away or demand a steep discount. Spend time now fixing accounting errors, reconciling bank statements, and documenting all major transactions. If you’ve run personal expenses through the business, separate them clearly. Buyers want to see your true business performance, and they adjust downward for anything that looks questionable.

Have your accountant prepare clean financial statements covering at least three years, ideally five years if available. Include detailed profit and loss statements, balance sheets, and cash flow statements. Tax returns must match your financial statements exactly. If they don’t, resolve the discrepancies before you talk to buyers. During due diligence, buyers compare your financial documents to your tax filings, and inconsistencies erode their confidence and reduce offers.

Identify Strengths and Weaknesses

Buyers don’t just look at profit-they look at risk. The more dependent your business is on you personally, the less attractive it becomes. If you’re the only person who knows how to serve your largest clients, or if your business falls apart without you, buyers will pay significantly less or pass entirely. Document your key processes, create standard operating procedures for critical functions, and identify which employees could step into important roles.

Assess your customer concentration: if 30 percent of your revenue comes from one client, that’s a major red flag for buyers. Work on diversifying your customer base before the sale. Look at your supplier relationships too.

If you rely on a single vendor, develop alternatives. Evaluate your intellectual property, proprietary systems, and competitive advantages (these justify a premium valuation).

Be honest about weaknesses. Litigation, pending regulatory issues, or contracts that end soon will surface during due diligence anyway, so address them proactively. The goal is to walk into negotiations with a business that’s operationally sound, not dependent on any single person, and positioned for continued growth under new ownership. Once you’ve assessed where your business stands, the next step is preparing it for the market.

Prepare Your Business for Sale

Buyers scrutinize three things before making an offer: your legal standing, your financial clarity, and your operational stability. Most owners underestimate how much work this takes. You’ll find gaps you didn’t know existed, contracts that need updating, and processes that only live in someone’s head. The good news is that fixing these issues now prevents them from torpedoing your deal later.

Conduct a Legal Audit

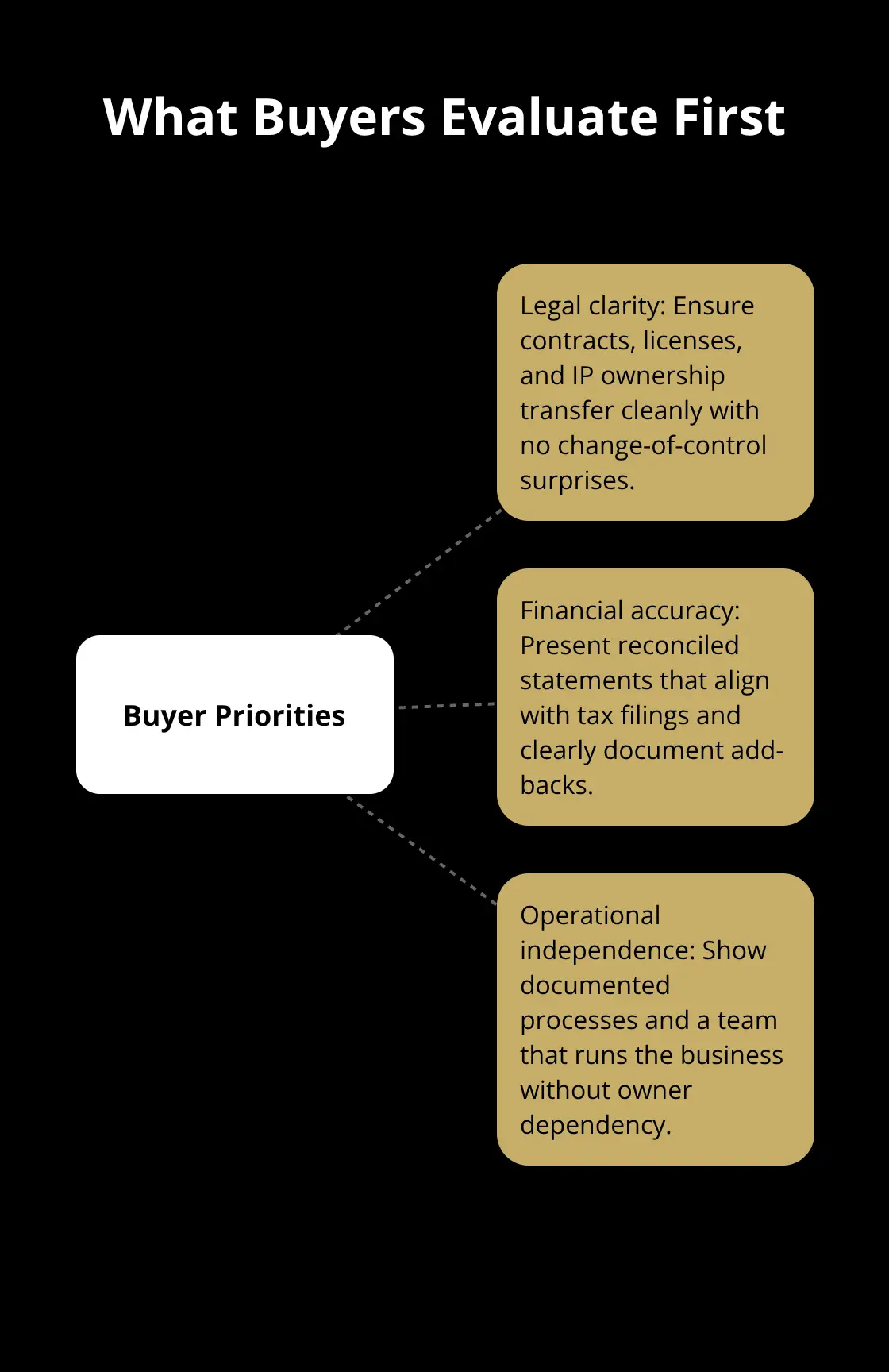

Start with every contract your business has signed: client agreements, vendor contracts, employee agreements, leases, loans, and licensing agreements. Check expiration dates, renewal terms, and any clauses that could complicate a sale. Some contracts contain change-of-control provisions that trigger price increases or termination if ownership changes hands. These are deal killers if you don’t address them upfront.

Identify which contracts need renegotiation before closing, which ones transfer cleanly to a new owner, and which ones might create liability. Your attorney should flag anything that could derail the transaction. While you’re at it, verify that all your intellectual property is properly documented and owned by the business, not you personally. If you hold patents, trademarks, or copyrights in your name instead of the company’s name, transfer them now. Buyers want clear ownership of everything they’re purchasing, and ambiguous IP ownership creates legal uncertainty that kills deals.

Reconcile Your Financial Statements

Clean up your financial statements to match what you’ve already submitted to the IRS. Buyers and their accountants will compare your business financials to your tax returns line by line. If your profit and loss statement shows $500,000 in revenue but your tax return shows $450,000, that discrepancy needs explanation and documentation.

Common issues include personal expenses running through the business, unreported cash income, or accounting errors carried forward for years. Work with your accountant to reconcile everything and prepare adjusted financial statements that clearly separate add-backs (non-recurring expenses, owner perks, and discretionary spending) from core business performance. Buyers care about what they can replicate going forward, not what you spent on your company car. Document these adjustments thoroughly because buyers will question them during due diligence.

Eliminate Operational Dependencies

Most small business owners are the bottleneck. You know all the clients, you handle the biggest contracts, you make the critical decisions. This concentration of knowledge destroys valuation. Start documenting your key processes in writing. Create standard operating procedures for your top revenue-generating activities. Identify your most critical employees and cross-train others to handle their responsibilities.

If your largest client relationship depends entirely on your personal relationship with the decision-maker, work now to introduce your team to that client and build their confidence in your business independent of you. The goal is to demonstrate to buyers that your business generates revenue through systems and people, not through your personal heroics.

These three areas-legal clarity, financial accuracy, and operational independence-form the foundation that buyers evaluate before they even consider price. With these fundamentals in place, you’re ready to position your business in the market and attract qualified buyers.

Market Your Business Effectively

Getting your business in front of the right buyers requires more than listing it on a website and hoping someone calls. Most owners treat the sale like a retail transaction when it’s actually a highly targeted process. You need a business summary that speaks to buyer motivations, a distribution strategy that reaches qualified prospects, and strict confidentiality controls that protect your competitive position while you operate.

Develop a Compelling Business Summary

Your summary is your first impression, and it determines whether a buyer requests more information. Focus on what buyers actually care about: revenue, profitability, growth trajectory, and risk mitigation. Highlight your customer retention rate (if it’s above 85 percent, that’s a major selling point), your recurring revenue percentage, and any contracts that extend beyond the sale closing.

Include specific numbers about your market position, such as your share of a defined market segment or your year-over-year growth rate. If you reduced customer concentration from 40 percent to 20 percent over the last two years, state that explicitly. Buyers want to see that you’ve already addressed the structural weaknesses they worry about.

Write your summary using clear language that a non-technical buyer understands. Avoid industry jargon unless your target buyer operates in that industry. A private equity buyer cares about EBITDA margins and scalability; a strategic buyer in your industry cares about how your customer base complements theirs; a family office investor cares about stability and recurring revenue. Tailor your summary to match the buyer profile you’re pursuing.

Reach Qualified Buyers Through Multiple Channels

Distribution matters as much as the summary itself. Most brokers rely on their existing network and a few industry databases, which limits exposure. A multi-channel approach works better: start with your professional network and industry associations (these often produce the highest-quality leads), then move to targeted outreach to strategic buyers who have acquired similar businesses, then use online platforms and business marketplaces to cast a wider net.

Research recent acquisitions in your industry using SEC filings, press releases, or acquisition databases to identify which companies actively buy. Reach out to them directly through their business development teams. Many acquisitions happen quietly through direct contact, not public listings. Simultaneously, maintain strict confidentiality throughout this process.

Protect Confidentiality and Control Information Flow

Use non-disclosure agreements before sharing financial details with any prospect. Require signed confidentiality agreements even before you share your business summary with potential buyers. Your goal is to pre-qualify buyers before you reveal sensitive information that could harm your business if it becomes public knowledge.

If competitors learn you’re selling before you’re ready, they’ll poach your customers and employees. If your team finds out prematurely through rumors, productivity drops and retention becomes impossible. Control the narrative by deciding exactly when and how your employees, customers, and vendors learn about the sale.

Most owners wait until a letter of intent is signed before telling their team. This protects your business during negotiations and prevents premature departures. When you communicate internally, frame the sale as a positive transition that benefits the business and its people, not an abandonment of what you’ve built.

Final Thoughts

Selling your business requires discipline, preparation, and the right support system. The exit planning checklist you’ve worked through-from valuation and financial cleanup to operational independence and strategic marketing-addresses the exact issues that derail deals or destroy value. Most owners who regret their sale either skipped these steps or tried to navigate them alone, and that decision cost them real money.

Your business represents your largest asset, and treating the sale process casually destroys significant value. A professional valuation prevents you from leaving hundreds of thousands on the table, clean financial statements eliminate buyer skepticism and speed negotiations, and operational independence removes the discount buyers apply when they perceive risk. Strategic marketing gets your business in front of qualified buyers instead of tire kickers, and a two-year timeline gives you space to fix structural weaknesses without rushing into compromises that reduce offers.

We at Unbroker built a platform specifically to help business owners navigate the sale process without paying traditional brokerage fees. Unbroker offers transparent, low-cost options including full-service support or assisted selling with expert guidance, premium marketing tools, legal templates, and access to a vast buyer network. Schedule a conversation with advisors who understand your industry and have closed comparable deals, bring your financial statements and timeline, and let that clarity guide every decision ahead.