Divorce and business ownership create a complex intersection that most entrepreneurs aren’t prepared for. Without proper planning, you risk losing control of your company, facing unexpected tax bills, or settling for far less than your business is worth.

At Unbroker, we’ve seen how exit planning for divorce can make the difference between a devastating financial outcome and one that protects both your business and your future. This guide walks you through the essential steps to safeguard what you’ve built.

What Counts as Business Assets in Your Divorce

Separating Marital Property from Separate Property

The first mistake most business owners make during divorce is assuming their company’s value equals what they think it’s worth. Courts don’t care about your optimistic projections or what you paid to start the business. They care about what your business is actually worth today, and more importantly, whether it qualifies as marital property that gets divided. If you started your company before marriage, it might remain separate property.

If you built it during the marriage with shared resources or your spouse’s support, it almost certainly becomes marital property subject to division.

About 40 states use equitable distribution laws, meaning they divide assets fairly but not necessarily 50/50. Nine states-including California, Texas, and Washington-use true 50/50 community property rules regardless of when assets were acquired, according to the Journal of Accountancy. This distinction matters enormously. In equitable distribution states, a judge weighs factors like each spouse’s contribution, the length of marriage, and future earning potential. In community property states, your business gets split down the middle unless you have a prenuptial agreement protecting it.

Documentation Protects Your Position

You need to document exactly when you acquired your business, what you paid, how much your spouse contributed financially or through unpaid labor, and whether marital funds were used for growth or improvements. This documentation becomes your evidence in court. Without it, you lose leverage in negotiations and face uphill battles during trial. Courts require proof of separate property status, and vague recollections won’t cut it.

Getting an Accurate Business Valuation

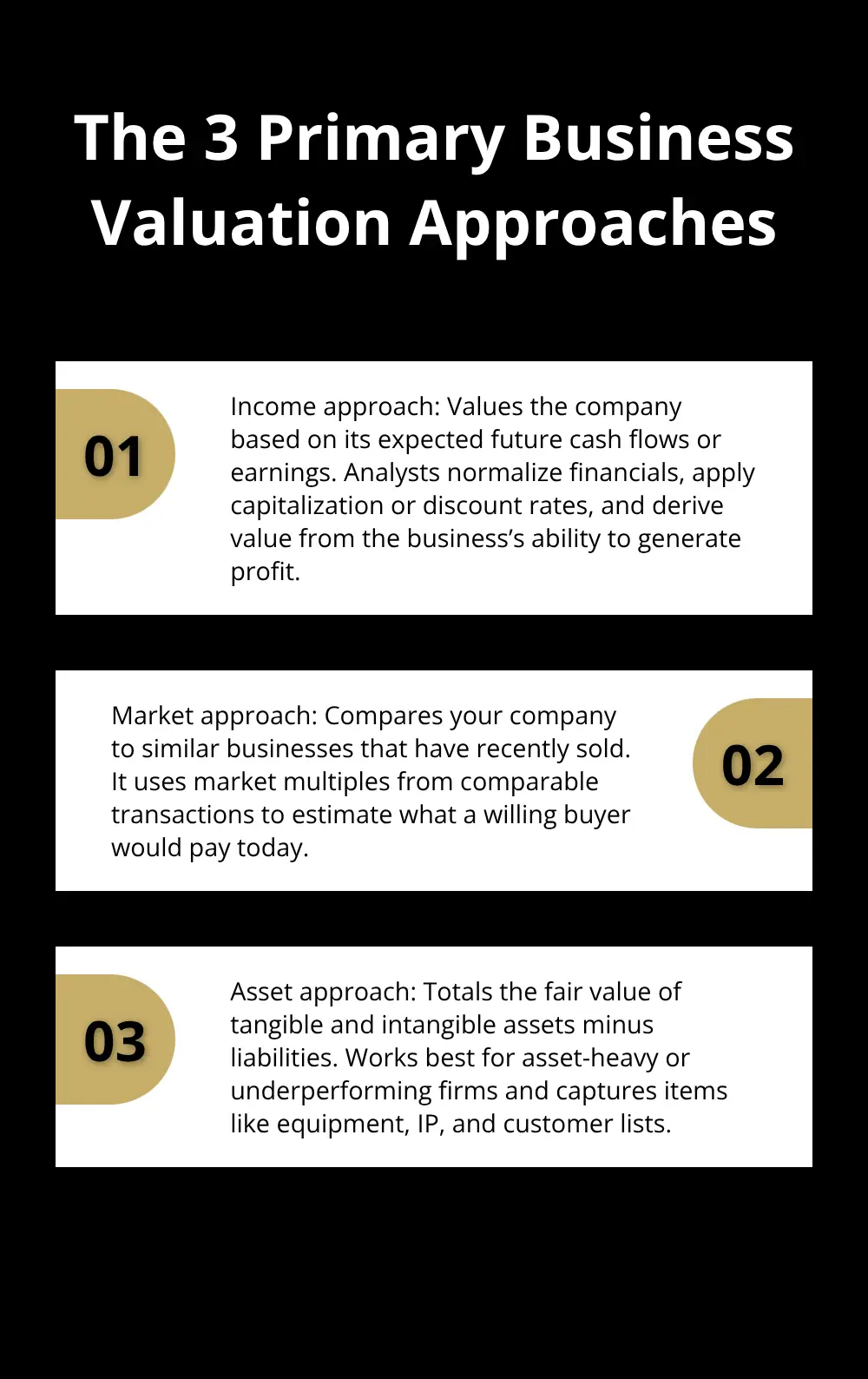

Valuation is where most divorces get expensive and contentious. A business worth $500,000 to you might be worth $750,000 to a court-appointed appraiser, and that difference directly impacts what you owe your spouse. Professional valuators use three main approaches: the income approach (based on what the business generates), the market approach (comparing to similar businesses sold), and the asset approach (totaling all tangible and intangible assets).

You absolutely need a professional business valuation expert, not an estimate from your accountant. Courts require independent assessments, and using a qualified valuator costs between $5,000 and $20,000 but protects you from far costlier disputes. Hire someone with credentials like an Accredited Senior Appraiser designation. Your divorce attorney should work directly with your valuator to ensure the appraisal supports your position.

Timing Your Valuation Strategically

Don’t wait until divorce papers are filed to get this done. The earlier you know your business’s real value, the better you can plan your exit strategy and understand what settlement offers actually mean. Early valuation also gives you time to explore whether you want to buy out your spouse’s interest, sell the business entirely, or structure a payment plan that works for both parties.

How to Shield Your Business From Divorce Claims

Legal structure as your first defense

The legal structure you chose for your business years ago now becomes your first line of defense. If you operate as a sole proprietorship or general partnership, your business assets sit completely exposed to division. Courts treat them identically to your personal assets. However, if you structured your company as an LLC, S-corp, or C-corp, you’ve already created separation between personal and business ownership. An LLC may separate personal and business assets, but courts can still divide ownership interests. The stronger your legal entity structure, the cleaner your exit options become later. If you haven’t formalized your business structure yet, do it immediately, even during divorce proceedings. Courts recognize legitimate entity formation as a protective measure, not a fraudulent scheme to hide assets.

Organize Your Documentation Now

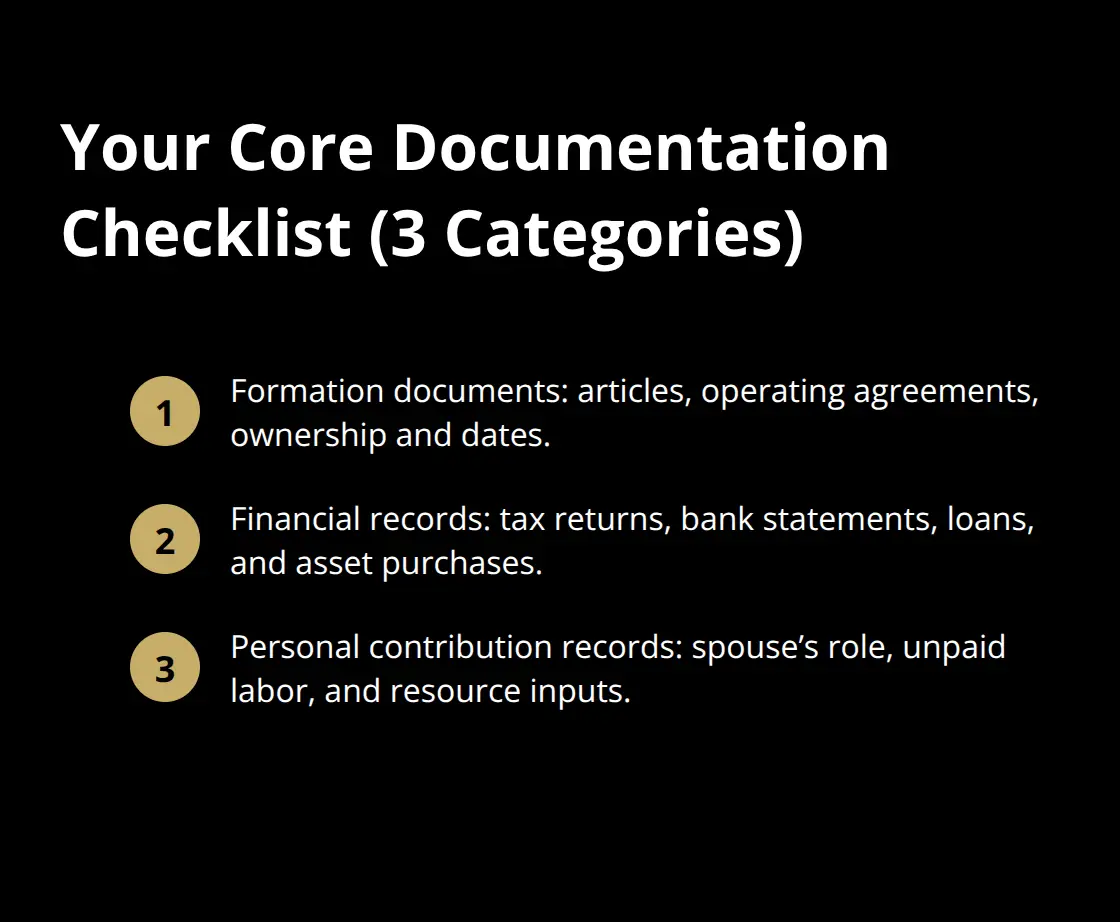

Documentation determines whether you win or lose in divorce court. You need three categories of records: formation documents showing when and how you created your business, financial records proving income and asset growth, and personal records demonstrating what your spouse actually contributed.

Most business owners keep scattered files across multiple devices and cloud accounts, making it nearly impossible to present a coherent case. Instead, create a master folder containing your articles of incorporation or organization, all tax returns for the past five years, bank statements showing business account activity, loan documents and equipment purchases, and any agreements with partners or investors. Store originals in a secure location separate from your spouse’s access, and provide copies to your divorce attorney immediately.

Courts require this documentation to distinguish between marital and separate business assets. Without it, judges make assumptions that typically favor equal division. Your attorney uses these records to argue that pre-marital investments, inherited capital, or personal loans you made to the business should reduce your spouse’s claim. Never alter, delete, or hide documents during divorce. Courts impose severe penalties for document destruction, including unfavorable judgments that assume hidden records prove your spouse’s claims. Your best strategy is transparency with your attorney paired with organized, comprehensive documentation.

Assemble Your Professional Team

Divorce attorneys and business attorneys rarely work together, which creates gaps in strategy. You need both. Your divorce attorney understands marital property law and settlement negotiation, but they typically lack expertise in business valuation, tax implications, or operational continuity. A business attorney specializing in divorce cases understands how to structure buyouts, protect intellectual property, and preserve business value during proceedings. These specialists cost more than general practitioners, typically charging $300 to $500 per hour, but they prevent mistakes that cost exponentially more.

When interviewing attorneys, ask specifically about their experience with business owner clients and whether they’ve handled cases involving business buyouts or sales. Ask how they coordinate with financial advisors and valuators. The worst outcome occurs when your divorce attorney negotiates a settlement that your business accountant later reveals creates massive tax liability you didn’t anticipate. Coordinate your team before settlement discussions begin. Your business valuator, divorce attorney, business attorney, and tax advisor should all review proposed settlement terms before you agree to anything. This coordination costs $5,000 to $10,000 upfront but prevents six-figure mistakes in tax bills or unfair asset divisions.

Protecting Intellectual Property and Client Relationships

Your business value extends beyond equipment and bank accounts. Intellectual property, client lists, trade secrets, and brand reputation often represent your company’s most valuable assets. During divorce, your spouse may claim ownership of these intangibles or threaten to disclose confidential information. Document all intellectual property you created before marriage, including patents, trademarks, copyrights, and proprietary processes. If you developed these assets during the marriage, work with your business attorney to establish how much of their value stems from your personal expertise versus marital resources. Client relationships deserve similar protection. Create a detailed client database showing acquisition dates, contract terms, and revenue history. This documentation proves which clients you brought to the business versus those acquired during the marriage. Your business attorney can structure agreements that prevent your spouse from contacting clients or claiming commission on accounts they didn’t develop. These protective measures, implemented now, determine whether you retain your most valuable business assets after divorce.

The next phase of protecting your business involves business valuation and tax implications in divorce settlements. Your documentation, legal structure, and professional team now position you to explore these options from a position of strength rather than desperation.

How to Exit Your Business After Divorce

Your three paths forward are buying out your spouse’s interest, selling the business outright, or structuring a hybrid arrangement that lets you keep partial ownership while paying your spouse over time. Each option carries vastly different financial, tax, and operational consequences, and selecting the wrong one costs more than any other divorce decision you’ll make.

The Buyout Path: Keeping Your Business

The buyout works best when you have the cash flow or financing to pay your spouse their share while maintaining business operations. If your business generates $200,000 annually and your spouse’s marital interest equals $150,000, a buyout requires either $150,000 upfront or a structured payment plan spanning three to five years. Most business owners choose payments because liquidating cash tanks operations. However, payments create ongoing risk-if your business fails, your spouse holds a secured claim against remaining assets, and divorce courts have ordered asset seizure when buyout payments stop.

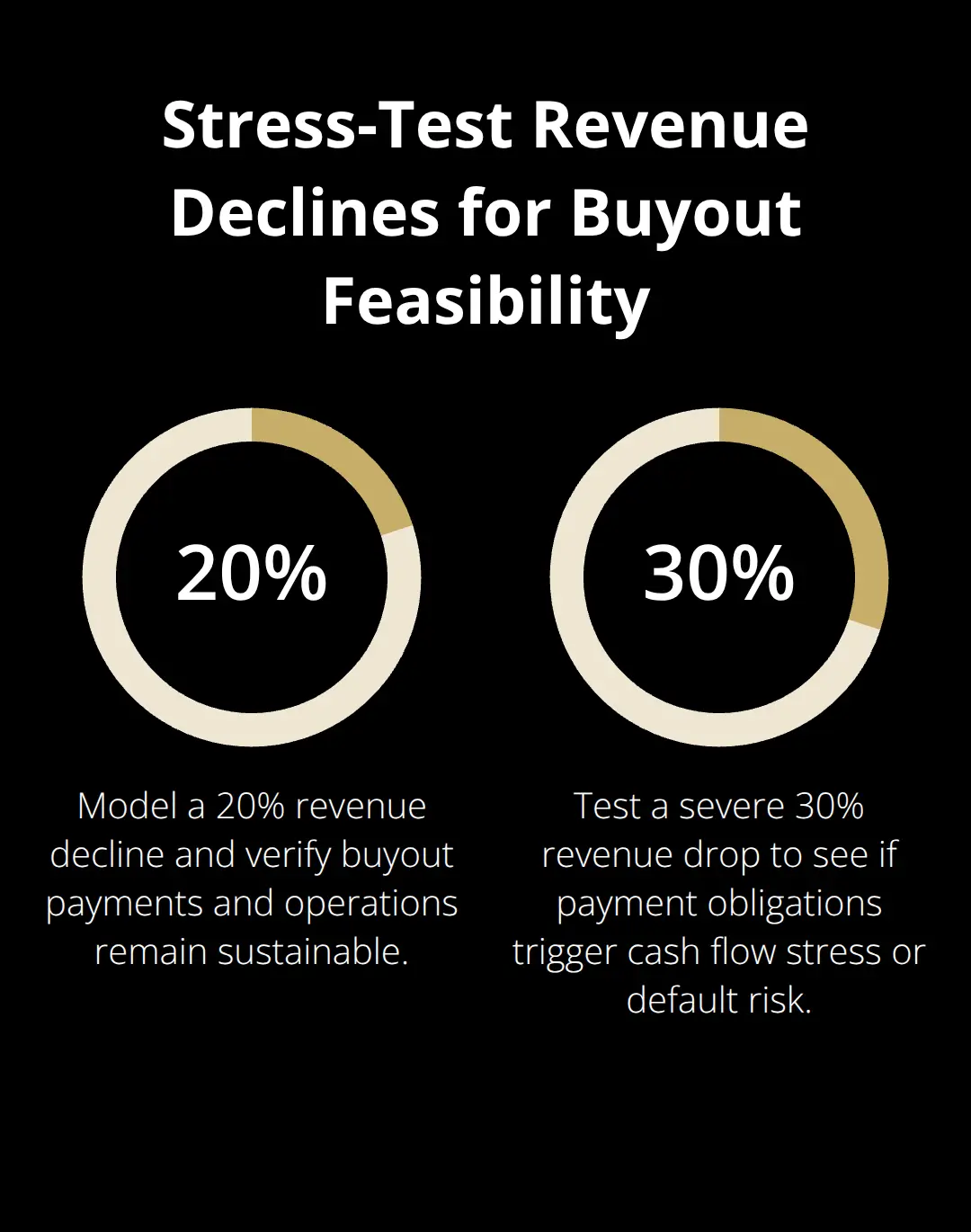

Before committing to a buyout, stress-test your financials with your accountant. Run scenarios showing what happens if revenue drops 20 or 30 percent. If your business can’t sustain payments during downturns, a buyout becomes a liability, not a solution.

Talk with your business lender now about refinancing capacity before divorce proceedings begin. Lenders scrutinize businesses mid-divorce, viewing them as higher risk, and refinancing becomes harder once legal proceedings start.

The Sale Option: Clean Separation

Selling the business entirely removes the operational complexity but forces an immediate exit you may not want. The advantage is clean separation-your spouse receives their share from proceeds, and you start fresh without ongoing entanglement. However, business sales typically take six to twelve months to complete, and divorce timelines rarely accommodate that delay. Courts expect asset division to conclude within one to two years.

If you’re mid-sale when divorce finalizes, your spouse may claim ownership of the sale proceeds, creating litigation that extends well beyond the divorce itself. Tax implications crush most sellers who don’t plan carefully. If you sell a business you’ve owned for fifteen years, capital gains taxes can consume a significant portion of proceeds depending on your income level and whether you qualify for Section 1202 small business stock exclusions. A $500,000 sale might net only $350,000 after federal and state taxes.

Tax Consequences and Settlement Structure

Your divorce attorney needs to understand tax consequences before settlement discussions. Ideally, structure the sale within the divorce settlement so both spouses understand the actual after-tax proceeds available for division. This prevents disputes where your spouse expects $250,000 from a $500,000 sale but receives only $175,000 after taxes.

Payment structures matter enormously for tax purposes. If you sell to a third party and use proceeds to pay your spouse, that’s straightforward. If you structure an installment sale where your spouse receives payments over time, you face complexity around spousal maintenance versus asset division-tax treatment differs significantly based on how courts characterize payments. Your tax advisor and divorce attorney must coordinate on this point before settlement. Many business owners made the mistake of structuring payments as alimony to gain tax deductions, only to discover later that alimony deductions for the payer are no longer available under current tax law. That strategy no longer works, and you’ve locked yourself into unfavorable terms based on outdated assumptions.

The Hybrid Approach: Partial Ownership and Payments

The hybrid approach-keeping your business while paying your spouse their share-requires careful structuring to work. You might refinance business debt, take an SBA loan, or arrange seller financing from a potential buyer to generate cash for buyout payments. This approach lets you maintain business ownership and future upside while satisfying immediate divorce obligations. However, it only succeeds if your business can service additional debt without operational strain.

Your timeline determines which exit strategy actually fits your situation. If you need to exit within eighteen months, a business sale likely won’t complete in time. A buyout becomes your only realistic option, which means securing financing immediately. If you have flexibility and can delay exit for two years, a sale becomes viable. If you have no timeline pressure, a structured buyout with payments over five years distributes your burden across multiple years. Start by clarifying with your divorce attorney which timeline is realistic given your state’s laws and court backlogs. Then work backward from that deadline to determine which exit strategy actually works rather than forcing a strategy that sounds best theoretically.

Final Thoughts

Exit planning for divorce protects what you’ve built and determines your financial stability after separation. Business owners who navigate divorce successfully start planning before crisis forces their hand-they gather documentation, understand their business’s actual value, assemble professional teams, and explore exit options from a position of strength. Your immediate action items matter: obtain a professional business valuation now, organize your documentation into a master file, interview both divorce and business attorneys who specialize in owner transitions, and stress-test your finances against your chosen exit strategy.

The timing of your exit strategy matters as much as the strategy itself. A business sale takes six to twelve months, a buyout requires financing secured before divorce proceedings complicate lending decisions, and a hybrid approach demands careful structuring to avoid tax disasters. Your divorce attorney and business attorney must coordinate on these timelines before settlement discussions begin, since tax implications often determine whether a settlement actually works financially. Discovering tax consequences after you’ve agreed to terms creates expensive regrets that proper planning prevents.

Your professional team coordinates across legal, financial, and tax expertise to prevent the mistakes that cost business owners six figures. If your exit strategy involves selling your business, we at Unbroker offer transparent options without the high brokerage fees that drain proceeds. The business owners who emerge strongest from divorce treat exit planning as a strategic business decision rather than a legal problem to endure.