Selling a private business or asset without proper buyer vetting is like handing over the keys before checking if anyone’s home. The wrong buyer can derail your entire transaction, expose sensitive information, or leave you with unpaid commitments.

At Unbroker, we’ve seen deals collapse because sellers skipped the vetting process. The right buyer vetting tools separate serious, qualified purchasers from time-wasters and bad actors.

Why Buyer Vetting Protects Your Deal

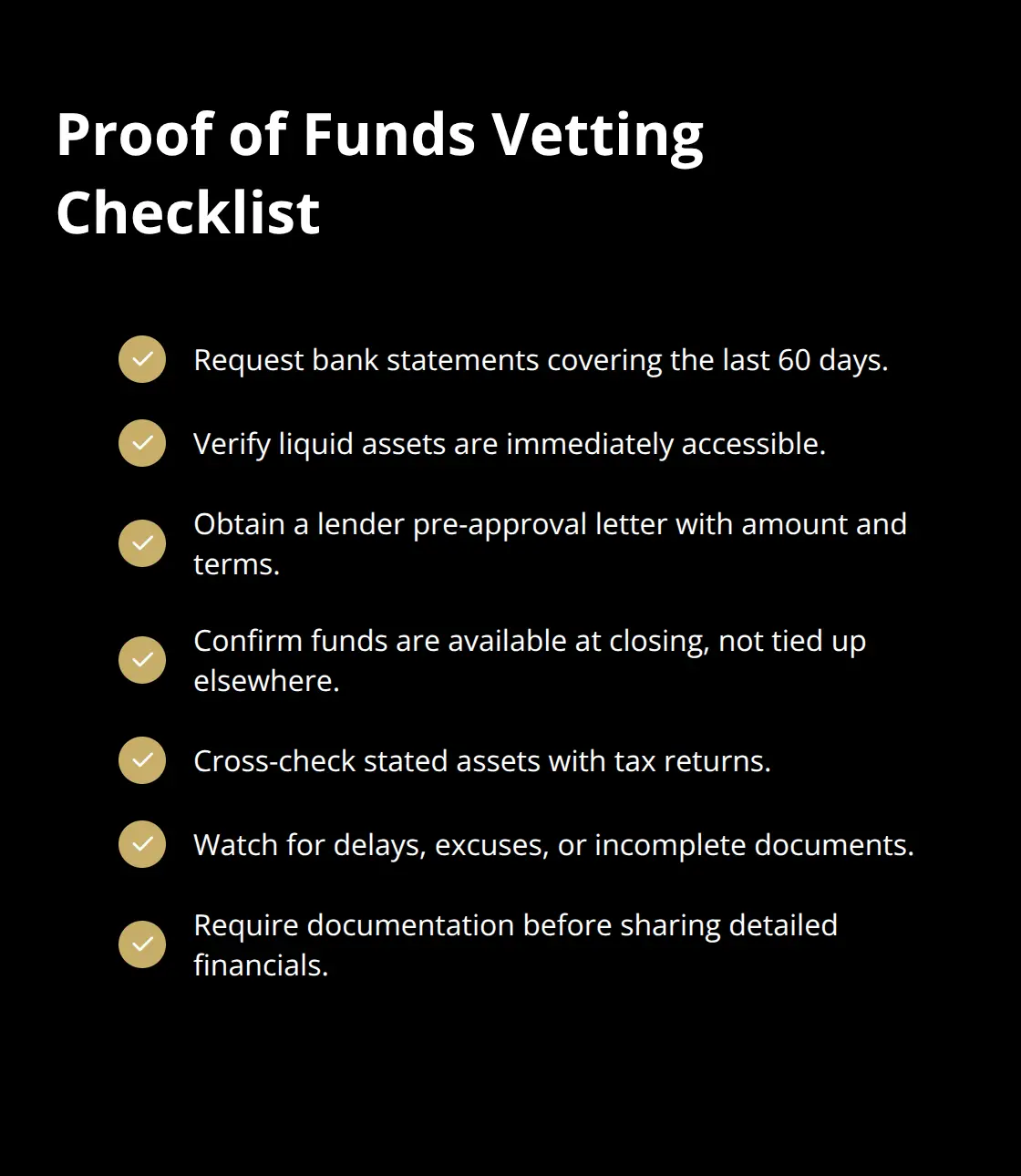

Failed transactions cost real money and time. When a buyer lacks actual funds or walks away mid-process, you waste weeks or months that could have gone toward finding a legitimate purchaser. Vetting filters out buyers who cannot close, hold unrealistic expectations, or lack the financial capacity they claim. The same rigor that organizations apply to verification processes across industries applies directly to business sales. Require proof of funds before sharing detailed financials. Ask for bank statements, proof of liquid assets, or a pre-approval letter from a lender. Buyers with genuine capital move fast and provide documentation without hesitation. Those who stall or make excuses signal weakness.

Confidentiality protects your negotiating position

Sensitive business information leaks when you vet poorly. A buyer who shares your financials with a competitor, posts acquisition plans on social media, or uses the information to negotiate with other sellers damages your reputation and negotiating position. Non-disclosure agreements become non-negotiable before you share any meaningful data. Require NDAs before you reveal revenue figures, client lists, supplier relationships, or operational details. Screen buyers by checking their professional background, industry experience, and track record with previous acquisitions. A buyer with relevant experience and verifiable references handles confidential information far more carefully than someone new to acquisitions. Verify their stated business affiliations and speak directly with references they provide. If a buyer refuses an NDA or becomes evasive about their background, move on immediately. The cost of protecting confidentiality pales compared to the damage of exposed information.

Financial legitimacy determines whether you actually get paid

A buyer’s financial legitimacy determines whether you receive payment at closing. Verify income sources, employment history, and credit standing through professional background checks. Credit reports reveal payment history and outstanding obligations that indicate whether someone can manage debt responsibly. For buyers seeking financing, confirm they have pre-approval from a lender before you advance negotiations. SBA loans, conventional bank financing, and private lending all require vetting, and pre-approval proves a lender already validated their financial position. Cross-reference stated assets with tax returns and bank statements. Buyers claiming $500,000 in liquid capital should produce documentation showing exactly that. Discrepancies between claims and evidence raise immediate concerns. Require proof that funds are genuinely available at closing, not tied up in pending deals or illiquid investments. A buyer with clean financials, documented income, and pre-approval has already cleared the hardest hurdle and closes far more reliably.

Red flags emerge when you ask the right questions

Inconsistent information signals trouble. A buyer who changes their story about funding sources, employment history, or acquisition timeline reveals either carelessness or deception. Ask direct questions and document their answers. Unwillingness to provide financial documentation is perhaps the clearest warning sign. Legitimate buyers expect these requests and comply immediately. Those who resist, delay, or offer vague alternatives lack the resources they claim. Pressure to expedite the sale process often masks financial weakness or unrealistic timelines. A serious buyer respects your need for thorough vetting and understands that proper due diligence protects both parties. When a buyer pushes you to skip steps or move faster than your process allows, trust your instincts and step back.

The vetting process you establish now determines the quality of your final transaction. Qualified buyers appreciate rigorous screening because it confirms they’re competing against serious contenders, not tire-kickers. Your next step involves structuring the actual sale terms and understanding what deal structure works best for your situation.

Tools That Actually Separate Serious Buyers from Pretenders

Professional Background Checks Form Your Foundation

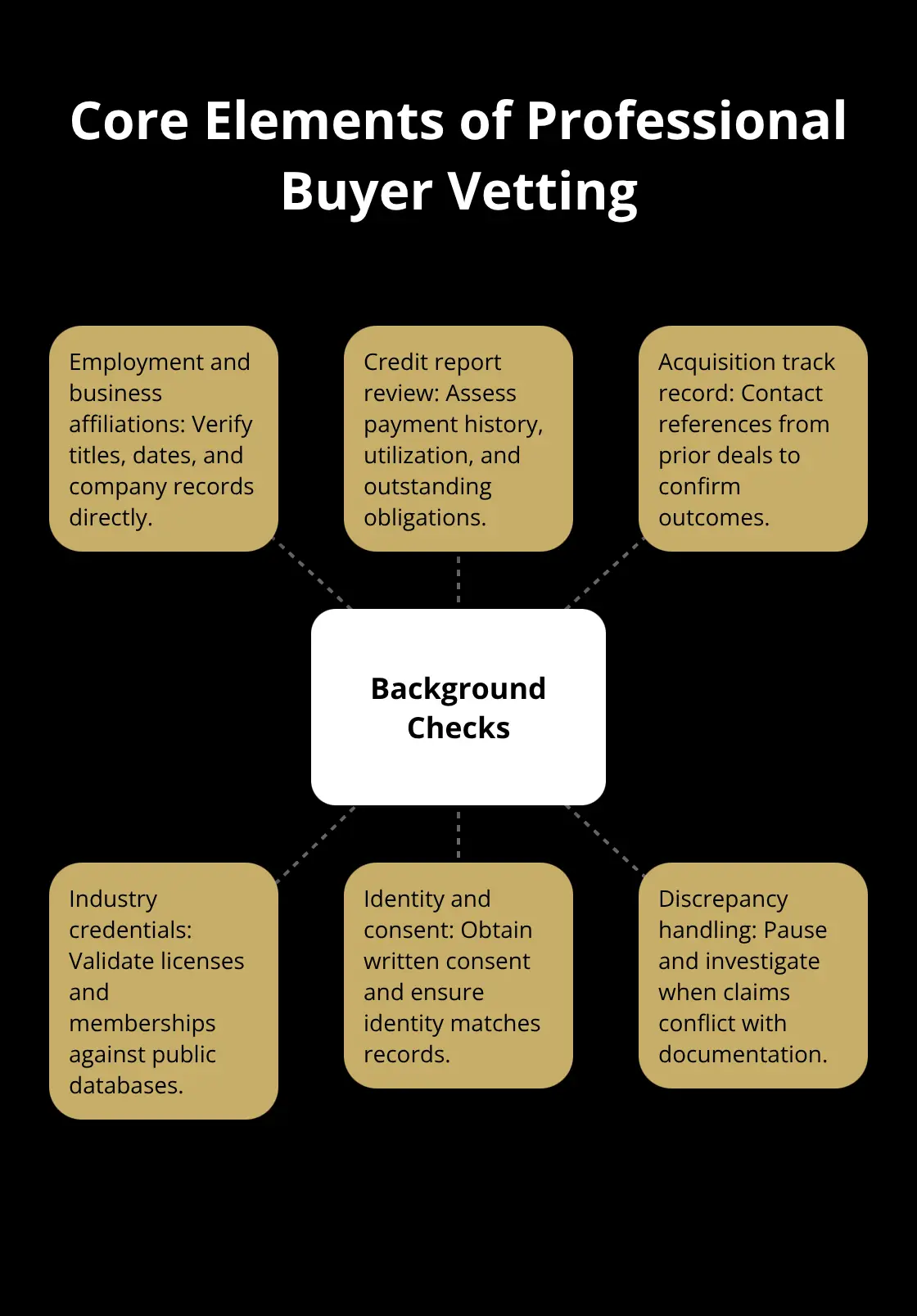

Professional background checks form the foundation of legitimate buyer vetting. You need more than a LinkedIn profile or a handshake. Run a comprehensive background check through services that verify employment history, business affiliations, and past acquisition experience. Credit reports reveal whether someone pays their obligations on time and how much existing debt they carry.

A buyer with a clean payment history demonstrates financial discipline. Those with recent late payments, collections, or bankruptcy filings present genuine risk, even if they claim to have cash available now. Credit bureaus like Equifax and Experian provide detailed reports, though you’ll need the buyer’s consent to pull them. Some buyers hesitate at this step, which itself signals a problem.

Legitimate purchasers expect credit verification and move forward without resistance. Verify their stated professional background directly by calling their employer and speaking with references from previous business acquisitions they’ve completed. Confirm their industry credentials against public records and chamber of commerce databases. Inconsistencies between what they claim and what records show indicate either carelessness or dishonesty-both disqualifying traits.

Proof of Funds Separates Qualified Buyers from Dreamers

Proof of funds requirements separate qualified buyers from those with unrealistic expectations. Before you share detailed financial information, require documentation showing the buyer has actual capital available at closing. Bank statements from the past 60 days prove liquid assets far more convincingly than verbal claims.

Pre-approval letters from lenders confirm that financial institutions have already validated their creditworthiness and lending capacity. SBA loans, conventional bank financing, and portfolio lenders all issue pre-approval letters that specify exactly how much money the buyer can borrow and under what terms. Ask to see the full pre-approval, not just a summary.

A buyer claiming available capital should produce bank statements showing exactly that amount in accessible accounts. Real estate holdings, retirement accounts, or business equity don’t count as proof of funds unless they’re documented and immediately accessible. This distinction matters because it separates buyers who can actually close from those whose capital remains locked away.

Non-Disclosure Agreements Protect Your Competitive Position

Non-disclosure agreements protect your competitive position and operational secrets. Require every potential buyer to sign an NDA before you reveal revenue figures, customer lists, employee names, supplier relationships, or any operational details that competitors could weaponize.

The agreement should specify that the buyer cannot share information with third parties without written consent, cannot use the information to compete directly, and faces financial penalties for breach. Many sellers skip this step because they want to move quickly, but this decision costs far more than the time it takes to execute a document.

Reference templates exist through legal document services, and customization for your specific situation costs a few hundred dollars through a business attorney. Enforce the NDA by documenting exactly what information you shared and when. If a buyer later shares your data inappropriately, you have clear evidence of breach and grounds for legal action.

With your vetting tools in place and serious buyers identified, the next critical step involves structuring the actual sale terms and understanding what deal structure works best for your specific situation.

Red Flags That Stop Deals Cold

Inconsistencies Reveal What Buyers Won’t Say Directly

Inconsistencies in a buyer’s story surface quickly when you ask the right questions and document everything. A buyer who claims $500,000 in liquid capital but then mentions pending real estate sales, delayed inheritance, or business equity payouts has not actually proven access to funds. Another states their employer is ABC Corporation, yet LinkedIn shows they left that company eight months ago. They explain the gap with vague references to consulting work that produces no verifiable contracts or references. These inconsistencies don’t always mean deception, but they do mean you lack confidence in their statements. Verify every material claim independently by calling their stated employer and confirming employment dates. Request bank statements from recent months. Ask for the name and contact information of their lender and follow up directly rather than accepting their word that pre-approval exists.

When inconsistencies emerge, slow down the process and demand clarity. Serious buyers provide explanations with documentation. Those who grow defensive or change their story again signal trouble and warrant immediate disqualification.

Resistance to Financial Documentation Masks Real Problems

Unwillingness to share financial documentation stands as perhaps the clearest warning sign that a buyer lacks the resources they claim. A legitimate purchaser expects these requests because they understand that thorough vetting protects both sides. When a buyer resists providing bank statements, tax returns, or pre-approval letters, they signal either that the funds don’t exist or that they’re hiding something about their financial position. No legitimate reason exists for a qualified buyer to refuse these standard requests.

The resistance itself becomes the disqualifying factor. Move on to the next prospect rather than waste time negotiating with someone unwilling to prove their capacity.

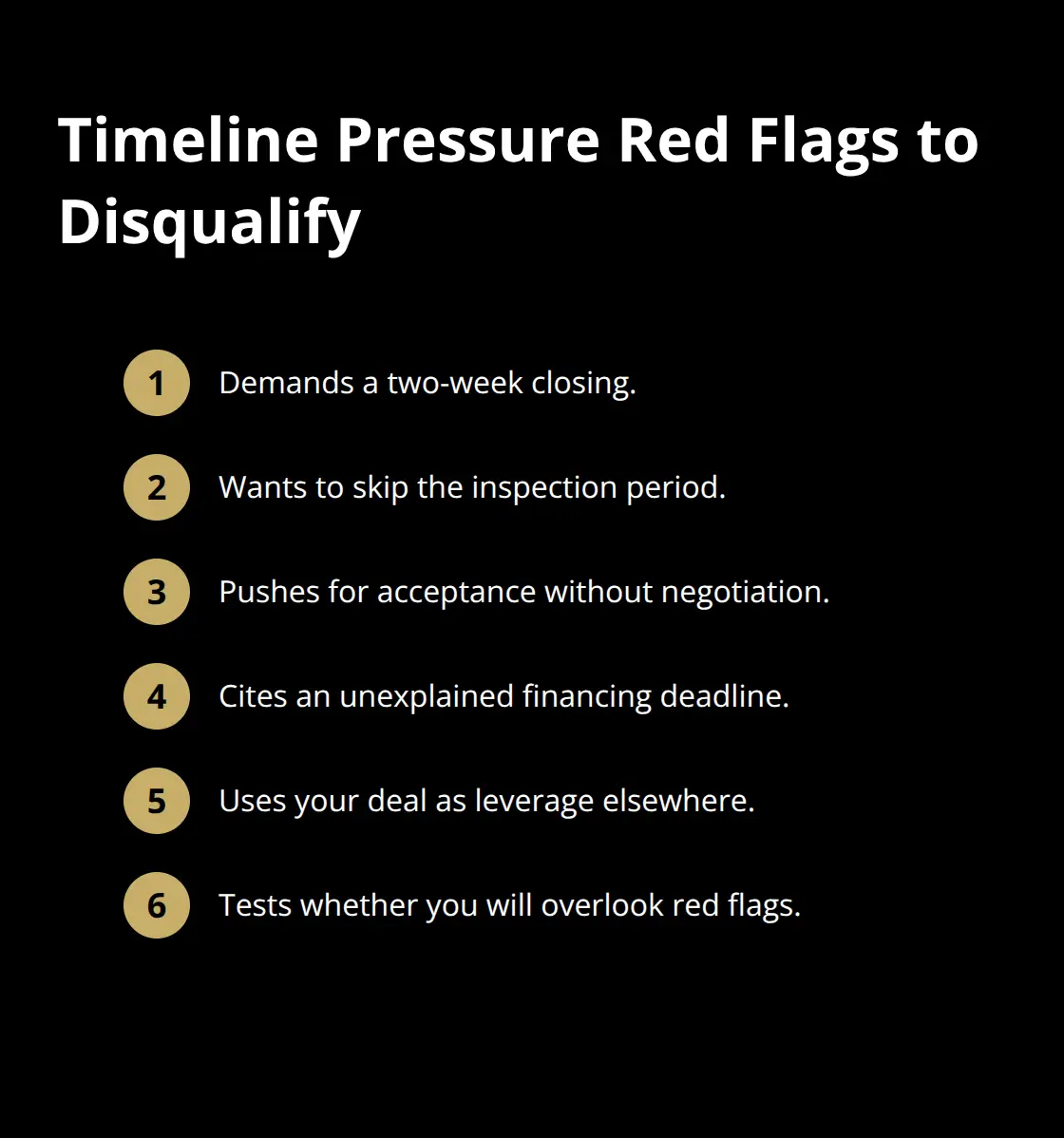

Timeline Pressure Indicates Hidden Constraints

Pressure to expedite the sale process often masks genuine problems on the buyer’s side. A buyer who insists on closing within two weeks, wants to skip the inspection period, or pushes you to accept their offer without negotiation typically faces a constraint you don’t know about. Maybe their financing falls through if they don’t close by a specific date. Maybe they’re using your business as leverage in another deal. Maybe they’re testing whether you’re desperate enough to overlook red flags.

Serious buyers understand that proper vetting takes time and actually respect sellers who refuse to rush. Treat timeline pressure as a disqualifying factor unless the buyer provides a documented business reason that makes sense for both parties. Trust your instincts-when something feels wrong, it usually is.

Final Thoughts

Buyer vetting tools and rigorous screening separate successful sales from deals that collapse mid-process. The time you invest now in verifying financial capacity, checking backgrounds, and enforcing confidentiality agreements pays dividends when you reach closing with a qualified, serious buyer who actually has the funds to complete the transaction. Thorough buyer assessment protects three critical areas of your sale: it eliminates wasted time chasing prospects who lack genuine purchasing power, it safeguards your confidential business information from competitors, and it dramatically increases the probability that you actually receive payment at closing.

The vetting process you establish now becomes your competitive advantage. Qualified buyers respect sellers who demand proof of funds, require background checks, and enforce non-disclosure agreements because these steps signal that you’re serious and organized. Buyers without legitimate resources disappear quickly when faced with real documentation requirements, leaving you free to focus on prospects who can actually close.

Moving forward with confidence means trusting the red flags you’ve learned to recognize-inconsistencies in a buyer’s story, resistance to financial documentation, and pressure to expedite the timeline all warrant immediate disqualification. We at Unbroker understand that selling a business involves far more than finding a buyer, which is why our Assisted Business Sale service provides expert support to help you navigate negotiations and maintain control of your sale timeline while keeping costs transparent and low.