Getting your broker license opens doors to a lucrative career in financial services. The path requires specific education, passing exams, and navigating regulatory requirements-but it’s entirely achievable with the right roadmap.

At Unbroker, we’ve guided countless professionals through this journey. This guide walks you through each step to become a licensed broker, from initial qualifications through launching your brokerage business.

What Qualifications Do You Actually Need to Become a Broker

California sets the bar higher than most states, and for good reason. To become a broker in California, you must be at least 18 years old and either live in the state or follow specific out-of-state guidance from the Department of Real Estate. The real requirement that stops most people is experience: you need two years of full-time licensed salesperson work within the last five years, or equivalent unlicensed real estate experience, or a four-year degree with a real estate major or minor. The DRE enforces these requirements strictly.

Education Requirements That Matter

The education component is non-negotiable. You must complete eight college-level courses before you sit for the broker exam, and each course must run at least 45 hours and count as three semester units or four quarter units. These courses cover Real Estate Practice, Legal Aspects of Real Estate, Real Estate Finance, Real Estate Appraisal, Real Estate Economics or Accounting, plus three additional courses from a specified list. As of January 1, 2024, the Real Estate Practice course must include implicit bias and fair housing content with an interactive, participatory component-not just a checkbox exercise.

Institutions must be accredited by the Western Association of Schools and Colleges or recognized by the U.S. Department of Education, or approved by the California Real Estate Commissioner. If you studied abroad, foreign credentials require evaluation by a DRE-approved evaluation service before the DRE will accept them. California State Bar members skip the coursework requirement but still must show two years of full-time salesperson experience within the last five years.

The Exam and Timeline Reality

Passing the broker exam is your ticket, but timing matters enormously. You must complete courses before you schedule the exam, and the DRE manages all licensing tasks through their eLicensing system where you can self-schedule exams and print certificates. Processing times vary, so you should check current timelines on the DRE website to prevent costly delays. After you pass the exam, you submit a license application for DRE approval-this isn’t instant.

The entire process typically takes six months to a year depending on how quickly you complete coursework and how fast the DRE processes your application. Military servicemembers and their spouses have access to DRE assistance programs that can accelerate certain steps. Out-of-state applicants face additional complexity and should review DRE guidance specific to their situation early.

What Your License Is Actually Worth

The U.S. Bureau of Labor Statistics reports that as of May 2024, brokers earned $72,280 annually, making the investment in licensing worthwhile. Once licensed, you’ll need to maintain continuing education requirements-these do not substitute for initial coursework and vary by state, so you should plan for ongoing compliance costs and time commitments throughout your career. With your license in hand, you’re ready to move from meeting regulatory requirements to the practical work of building a real brokerage business that generates revenue and serves clients effectively.

Your Roadmap From Coursework to Licensure

Map Out Your Study Timeline Realistically

The eight required courses demand at least 360 hours of study time since each course runs a minimum of 45 hours. If you work full-time while studying, plan for four to six months of sustained effort to finish all coursework. The California Department of Real Estate requires you to complete all courses before you schedule your broker exam, so no shortcuts exist here. Most candidates underestimate how long coursework actually takes and fall behind schedule as a result. Start your courses with a clear calendar showing when you’ll finish each one, then add two weeks of buffer time before you schedule your exam.

Schedule Your Exam and Prepare Strategically

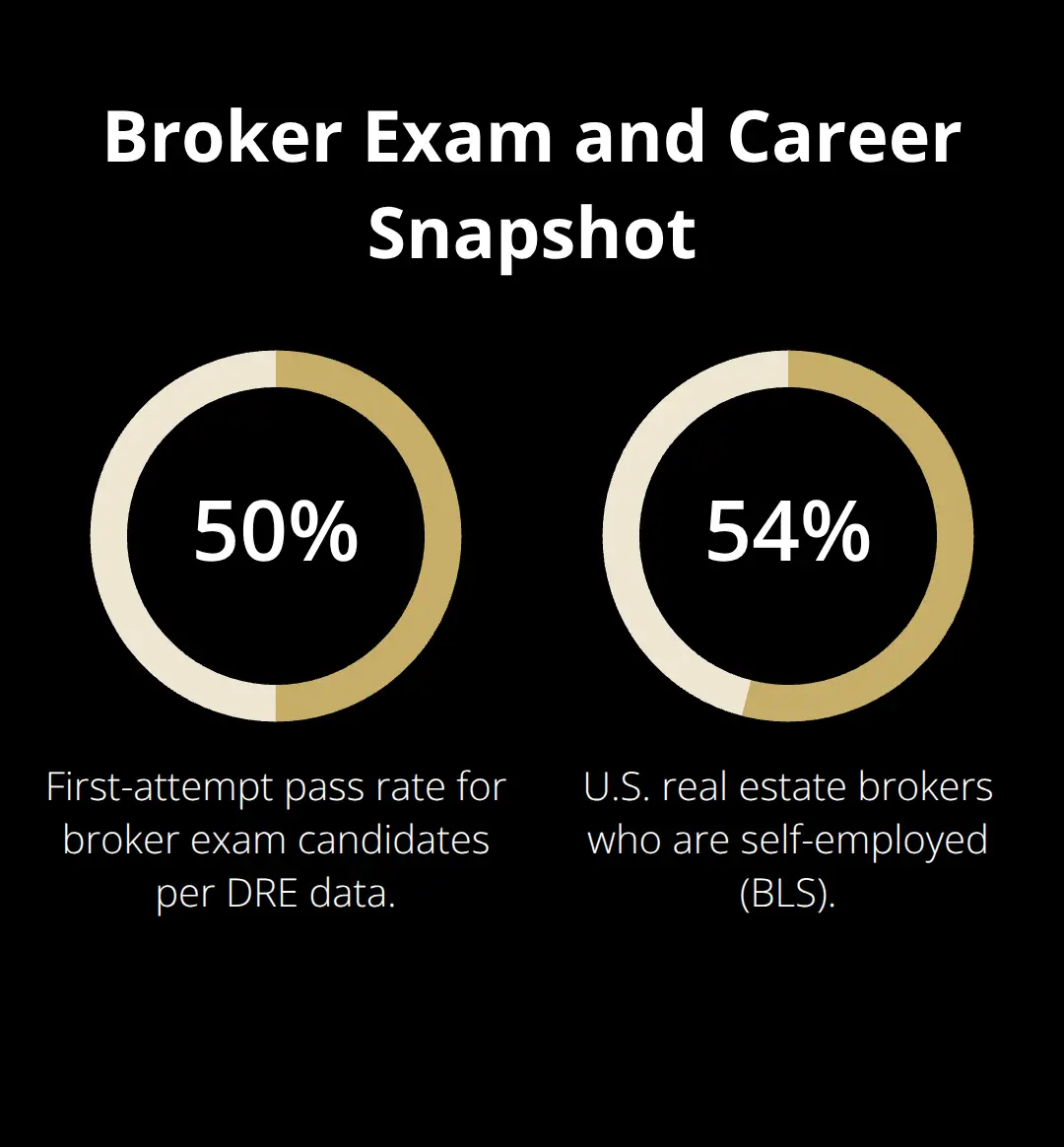

Once courses are complete, use the DRE’s eLicensing system to self-schedule your exam immediately-don’t wait for someone else to book it for you. The exam covers real estate law, practice standards, trust account management, and fair housing rules through multiple-choice questions that test practical knowledge, not theoretical concepts. Pass rates hover around 50 percent on first attempts according to DRE data, so treat exam prep seriously. Many candidates fail because they rush through study materials without working through practice questions repeatedly.

Spend your final two weeks taking full-length practice exams under timed conditions to build speed and accuracy before test day.

Submit Your Application With Complete Documentation

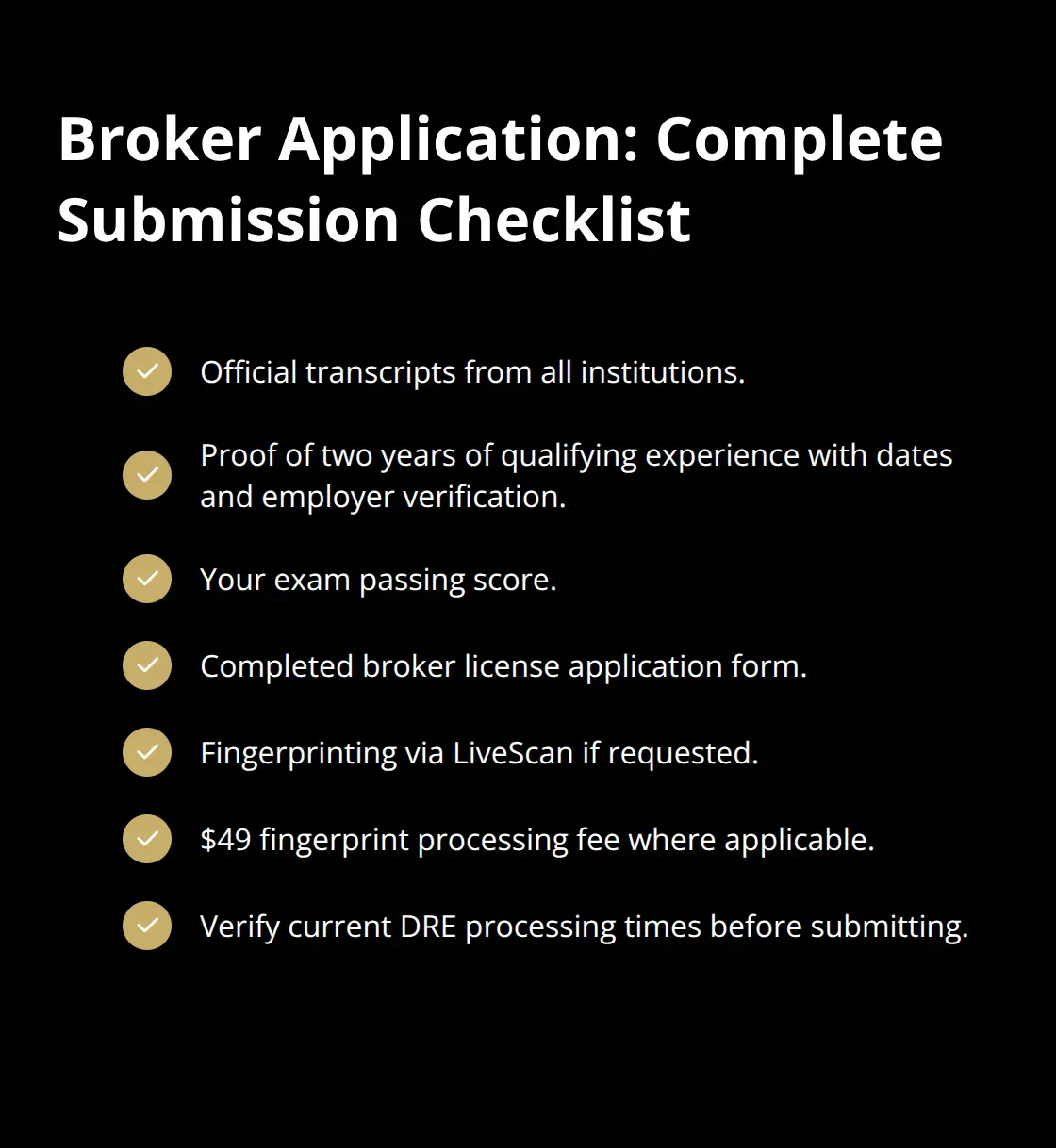

After you pass the exam, submit your broker license application to the DRE for approval-this is where patience becomes critical. Check DRE processing times for broker applications to understand current approval timelines. Incomplete applications get rejected and sent back, costing you another month of waiting. Submit everything the DRE requests the first time: official transcripts from all institutions, proof of your two years of qualifying experience with dates and employer verification, your exam passing score, and a completed application form. The background check component varies by application; the DRE may request fingerprinting through LiveScan, which involves a $49 fingerprint processing fee.

Handle Background Checks and Out-of-State Complications

If you have any prior legal issues or licensing violations, disclose them immediately-hiding problems guarantees denial. Out-of-state applicants need additional documentation proving they meet California’s specific requirements, so budget an extra two to four weeks for your timeline if you’re applying from another state. Once the DRE approves your application, you’ll receive your broker license certificate via the eLicensing system, and you’re officially licensed to operate a real estate brokerage in California. With your license secured, you now shift focus from regulatory compliance to the business side-establishing your brokerage structure, building your operational framework, and creating systems that attract clients and agents to your firm.

Building Your Brokerage Business

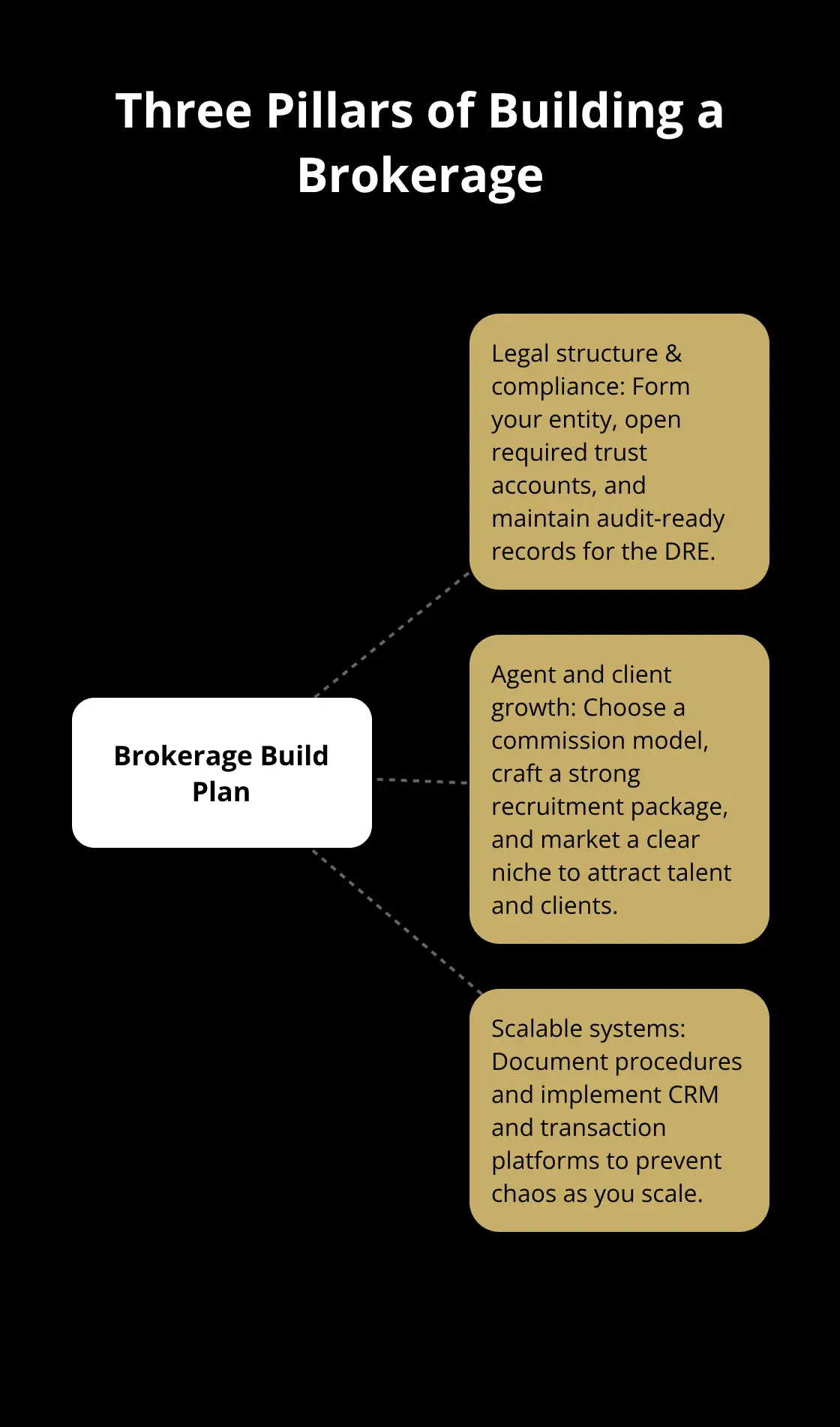

Your broker license is a credential, not a business. The jump from licensed individual to actual brokerage owner requires three parallel tracks: establishing a legal structure that protects your personal assets and meets state compliance rules, building systems that attract both agents and clients consistently, and creating operational processes that scale without you working 80-hour weeks. Most new brokers fail because they focus only on getting licensed and ignore the business fundamentals that separate sustainable firms from short-lived ventures.

Setting Up Your Legal Structure and Compliance Foundation

Start with your business structure immediately. You can operate as a sole proprietorship, LLC, S-corp, or C-corp, and your choice directly impacts taxes, liability protection, and ongoing paperwork. An LLC protects your personal assets if a client sues and costs roughly $500 to $1,500 to establish depending on your state, making it the most common choice for new brokers. You’ll need a separate business bank account for client funds and trust account management-this isn’t optional, it’s a regulatory requirement that the California Department of Real Estate audits regularly. Open this account within your first week of licensure and never mix personal and client money. Errors and commingling of funds trigger license suspension or revocation.

Obtain errors and omissions insurance immediately, and general liability coverage for your office operations. These insurance policies aren’t luxury items; they’re mandatory protection against the lawsuits that inevitably arise in real estate transactions. Set up a compliance calendar tracking state continuing education deadlines, trust account reconciliation schedules, and annual licensing renewals to prevent missing critical dates that could cost your license.

Attracting Agents and Building Revenue Streams

Your first revenue comes from recruiting agents to work under your license, not from transactions you personally close. Decide early whether you’ll operate a traditional commission split (typically 80/20 or 70/30 in your favor), a flat-fee model where agents pay monthly desk fees, or a hybrid approach combining both. The National Association of Realtors notes that independent brokerages control a significant portion of the market nationwide, meaning there’s room to compete against mega-brokerages by offering personalized support and lower overhead costs.

Create a recruitment package showing your agent value proposition: what training you provide, transaction support, technology access, and commission structure. Attend local real estate networking events and reach out directly to agents at competing brokerages who might be dissatisfied with their current firm. Build a professional brokerage website immediately-this is your first client acquisition tool and agents evaluate your firm through it before applying. Your website should clearly state your commission splits, specialties, and contact information.

For client acquisition, decide your initial niche: residential sales, commercial properties, buyer representation, or a specific geographic area. Specialization lets you build expertise and market positioning faster than trying to serve everyone equally. Invest $3,000 to $8,000 in initial marketing covering website development, business cards, and targeted digital advertising to agents and clients in your chosen niche.

Creating Systems That Actually Work

Document your operational processes before you hire your first agent. Create written procedures for listing intake, transaction timelines, document handling, and client communication standards. This prevents chaos as you grow and makes onboarding new agents faster. Implement a customer relationship management system like HubSpot or Salesforce to track leads, manage transactions, and automate follow-ups-these tools cost $50 to $300 monthly and eliminate the chaos of spreadsheets and scattered notes.

Establish a transaction management platform such as Dotloop or Ziplogix for contract management and e-signature workflows, which costs $100 to $500 monthly depending on transaction volume. Most brokers underestimate how much time they’ll spend on compliance and administrative work; budget 30 percent of your time for these tasks even after you’ve hired administrative support. Schedule your first Code of Ethics and Fair Housing training within your initial three-month period-this is mandatory and must be completed within the appropriate three-year cycle to maintain your license.

Set specific performance metrics for your first year: how many agents you’ll recruit, average transaction volume per agent, and average commission per deal. The U.S. Bureau of Labor Statistics reports that about 54 percent of real estate brokers are self-employed, meaning your profit depends directly on how efficiently you operate.

Final Thoughts

Becoming a licensed broker requires sustained effort across education, examination, and business fundamentals, but the payoff justifies the work. You’ve now seen the complete path: completing eight college-level courses, passing the broker exam, submitting your application to the DRE, and then shifting into the harder work of actually building a profitable brokerage. Most people stop after they become licensed brokers and wonder why their business stalls-the credential alone generates zero revenue.

Your real competitive advantage comes from the systems you build, the agents you recruit, and the clients you serve consistently. The brokers earning $72,280 annually aren’t just licensed; they’ve created operational frameworks that scale beyond their personal effort. They document processes, invest in technology, and build recruitment pipelines that bring agents and clients to their firm automatically (this is where your focus belongs after you receive your license).

Start your compliance calendar immediately and never miss a continuing education deadline. Track your trust account reconciliation monthly, not annually. Build your brokerage website before you recruit your first agent, and if you plan to sell your brokerage eventually, document everything from day one so clean financial records and clear operational procedures make your firm attractive to buyers.