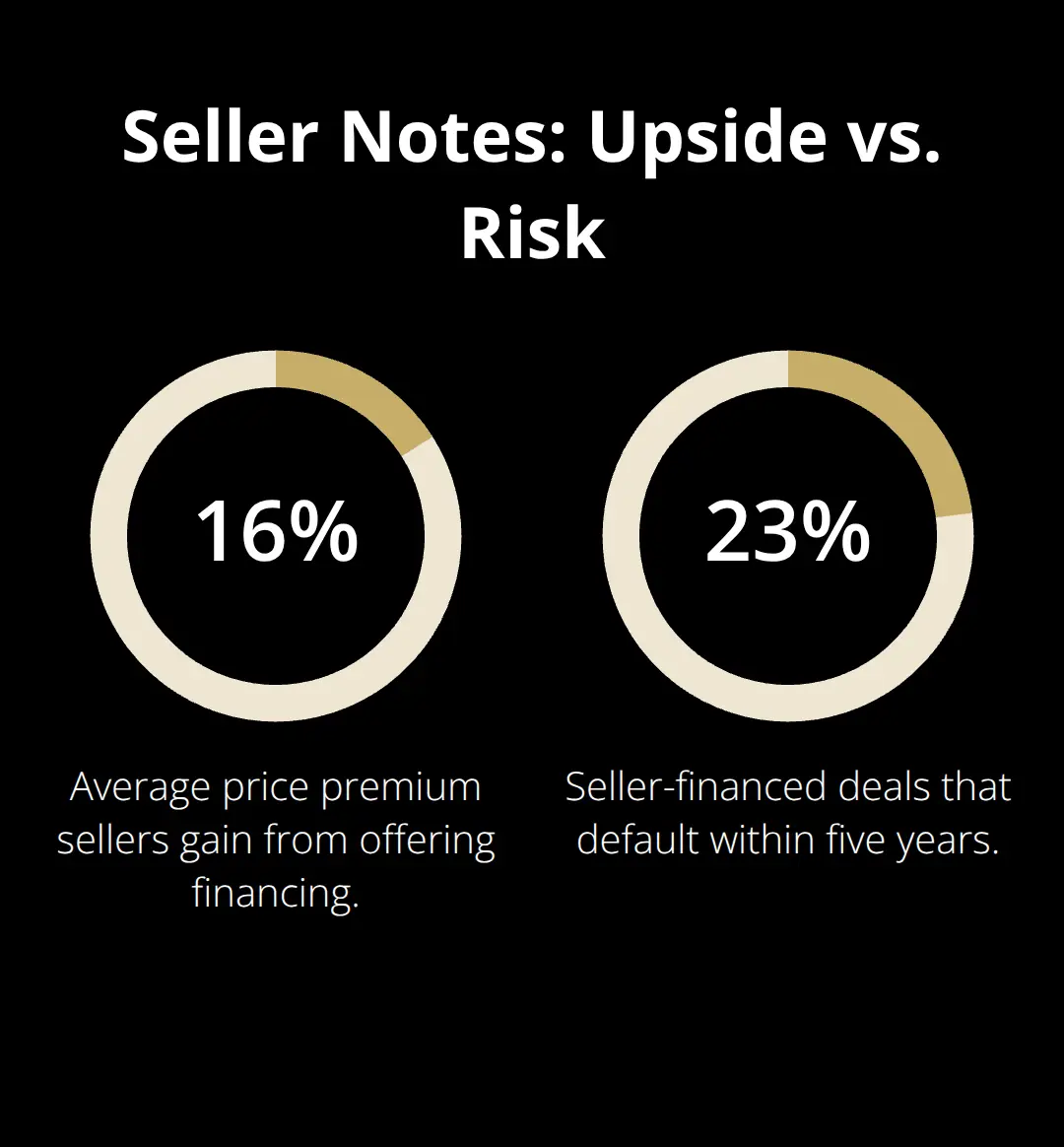

Selling your business through seller notes can generate higher sale prices and steady income streams. Yet 23% of seller-financed deals experience payment defaults within five years.

We at Unbroker see business owners wrestling with this decision daily. The potential rewards are significant, but the risks demand careful consideration before moving forward.

How Do Seller Financing Notes Actually Work

Seller financing transforms you from a business owner into a lender. Instead of receiving the full purchase price upfront, you accept a down payment and create a promissory note for the remaining amount. The buyer makes monthly payments with interest directly to you over an agreed timeframe (typically five to ten years).

Payment Structure and Interest Rates

Most seller financing deals require 30% to 50% down payment from buyers. Interest rates typically range from 4% to 8%, with seller notes usually structured over 3 to 6 years. A $500,000 business sale with $150,000 down creates substantial monthly payment obligations for buyers while generating steady income for sellers.

Payment terms should include late fees, typically 5% of overdue amounts, and acceleration clauses that make the full balance due after 60 days of non-payment.

Security Measures That Protect Sellers

Smart sellers file UCC-1 statements to provide notice to interested parties that they have a security interest in the debtor’s personal property. Personal guarantees from buyers add another protection layer, making them personally liable for the debt. The promissory note should include step-down provisions that reduce your collateral requirements as the buyer demonstrates reliable payment history.

Include specific default remedies that allow you to reclaim business assets and operations if payments stop. Professional legal documentation costs $2,000 to $5,000 but prevents costly disputes later.

Documentation Requirements

The promissory note serves as your primary legal protection. This document must specify payment amounts, due dates, interest rates, and default consequences. Include detailed asset descriptions that secure the loan and establish your rights to business inventory, equipment, and customer lists.

Professional attorneys draft comprehensive agreements that withstand legal challenges. These documents protect your interests while establishing clear expectations for both parties throughout the repayment period.

Why Seller Financing Delivers Better Returns

Seller financing consistently delivers superior financial outcomes compared to all-cash transactions. Business owners who accept seller notes receive an average of 86% of their asking price, while cash-only deals typically close at 70% according to industry data from the International Business Brokers Association. This 16% price premium translates to substantial additional income on million-dollar business sales.

Premium Prices Through Creative Deal Structure

The finance component allows you to command higher valuations because buyers view seller-backed deals as lower risk investments. When you offer finance terms, buyers interpret this as confidence in your business fundamentals and future performance. Seller promissory notes typically have specific conditions including full standby requirements for SBA loan terms and maximum equity limits of 50% of total transaction value. A $300,000 seller note at competitive interest rates creates substantial annual income over the loan term while the principal balance decreases.

Tax Benefits and Payment Control

Seller finance enables installment sale treatment under IRS regulations, which spreads capital gains taxes across multiple years instead of creating a massive tax burden in the sale year. This tax deferral strategy often saves business owners 15% to 20% in total tax liability (depending on their income bracket). Monthly payment streams provide predictable cash flow that many sellers prefer over lump-sum distributions that require immediate reinvestment decisions.

Market Access and Competitive Advantage

Approximately 70% of business sales involve seller finance because most qualified buyers lack sufficient cash reserves for complete acquisitions. Traditional financing options remain challenging for many buyers, which creates finance gaps that seller notes fill effectively. Your willingness to provide finance attracts serious buyers who might otherwise pursue competitor businesses that offer similar terms.

These substantial benefits come with corresponding risks that every business owner must evaluate carefully before committing to seller finance arrangements.

What Are the Real Risks of Seller Financing

Seller financing exposes business owners to significant financial risks that many underestimate. While specific default rates for seller-financed business transactions vary, corporate defaults have reached concerning levels with 81 defaults year-to-date, nearly matching the five-year average. When buyers stop payments, sellers must navigate complex legal proceedings while business values potentially decline during extended recovery periods.

Payment Default and Collection Challenges

Buyer defaults trigger expensive legal processes that consume 15% to 25% of the outstanding loan balance in attorney fees and court costs. Research shows that 60% of businesses face cash flow issues annually, which makes payment interruptions common during economic stress periods. Sellers must prepare to reclaim business operations, which requires immediate management attention and often reveals deteriorated conditions that reduce asset values.

Personal guarantees provide limited protection when buyers declare bankruptcy or dissolve business entities to avoid obligations. Collection efforts often stretch across multiple years while legal costs accumulate and business assets depreciate. Contract negotiations represent the biggest risk area where inexperienced sellers make costly mistakes.

Economic Downturns and Asset Devaluation

Market conditions directly impact your ability to recover funds through asset liquidation or business resale. The 2008 financial crisis created severe economic stress as financial market conditions deteriorated sharply, which left sellers with collateral worth significantly less than outstanding loan balances. Economic downturns also increase buyer default rates as revenue declines make monthly payments unaffordable.

Sellers who hold notes during market corrections often accept substantial losses rather than pursue lengthy foreclosure processes that yield minimal recoveries. Asset values fluctuate with market conditions, but loan balances remain fixed at original amounts.

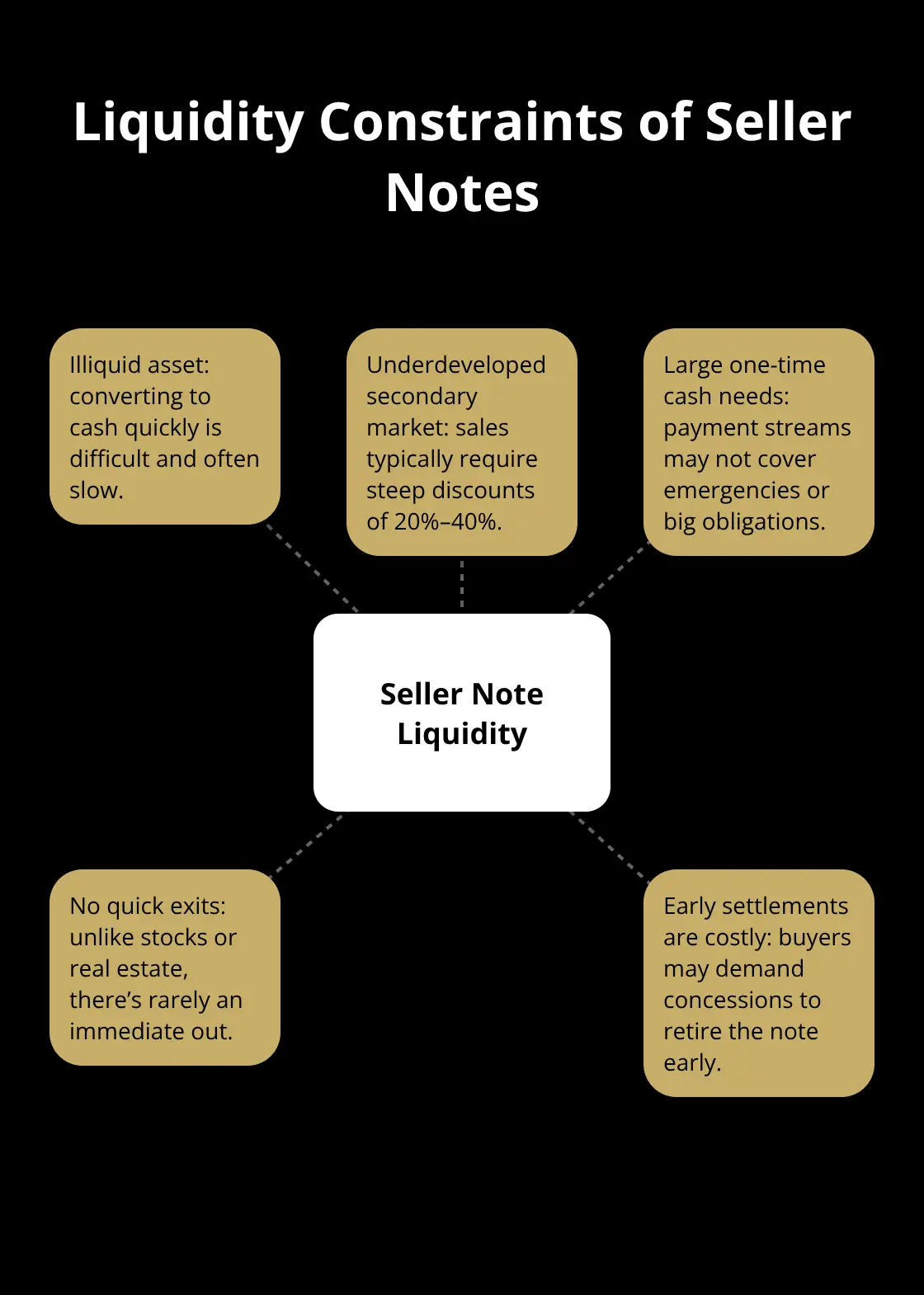

Liquidity Constraints and Cash Flow Impact

Seller notes create illiquid assets that cannot be easily converted to cash when unexpected expenses arise. The secondary market for business seller notes remains underdeveloped, which means most sellers cannot sell their payment streams without accepting significant discounts (20% to 40% below face value). Monthly payment dependence becomes problematic when sellers need large cash amounts for medical emergencies, investment opportunities, or family obligations.

Unlike stock portfolios or real estate, seller notes offer no quick exit strategies during financial emergencies. Sellers must wait for scheduled payments or negotiate costly early settlement agreements with buyers.

Final Thoughts

Seller notes present a complex financial decision that requires careful evaluation of your risk tolerance and cash flow needs. The 16% price premium and tax advantages make seller notes attractive, but the 23% default rate within five years creates substantial exposure that many business owners cannot afford. Your decision should center on immediate cash requirements, ability to manage collection risks, and comfort with illiquid investments.

Business owners who need full proceeds for retirement or new ventures should avoid seller notes despite the higher sale prices. Those with strong financial cushions and collection experience may find the steady income streams worthwhile. Risk-averse sellers have alternatives that provide certainty without payment default exposure (all-cash transactions deliver immediate liquidity at lower prices but eliminate collection risks entirely).

Strategic buyers often pay premium prices for businesses that complement their operations, which creates competitive situations that approach seller-financed valuations. We at Unbroker help business owners evaluate all exit strategies through our transparent platform that connects sellers with qualified buyers while providing expert guidance throughout the transaction process. Whether you choose seller notes or pursue cash transactions, professional support helps maximize your sale proceeds while minimizing unnecessary risks.