Most business owners have no idea what their company is actually worth. We at Unbroker see this constantly-entrepreneurs operate without a clear picture of their business valuation basics, which creates real problems when it’s time to sell or raise capital.

Getting your valuation right matters more than you think. The difference between an inflated estimate and a realistic one can cost you hundreds of thousands of dollars.

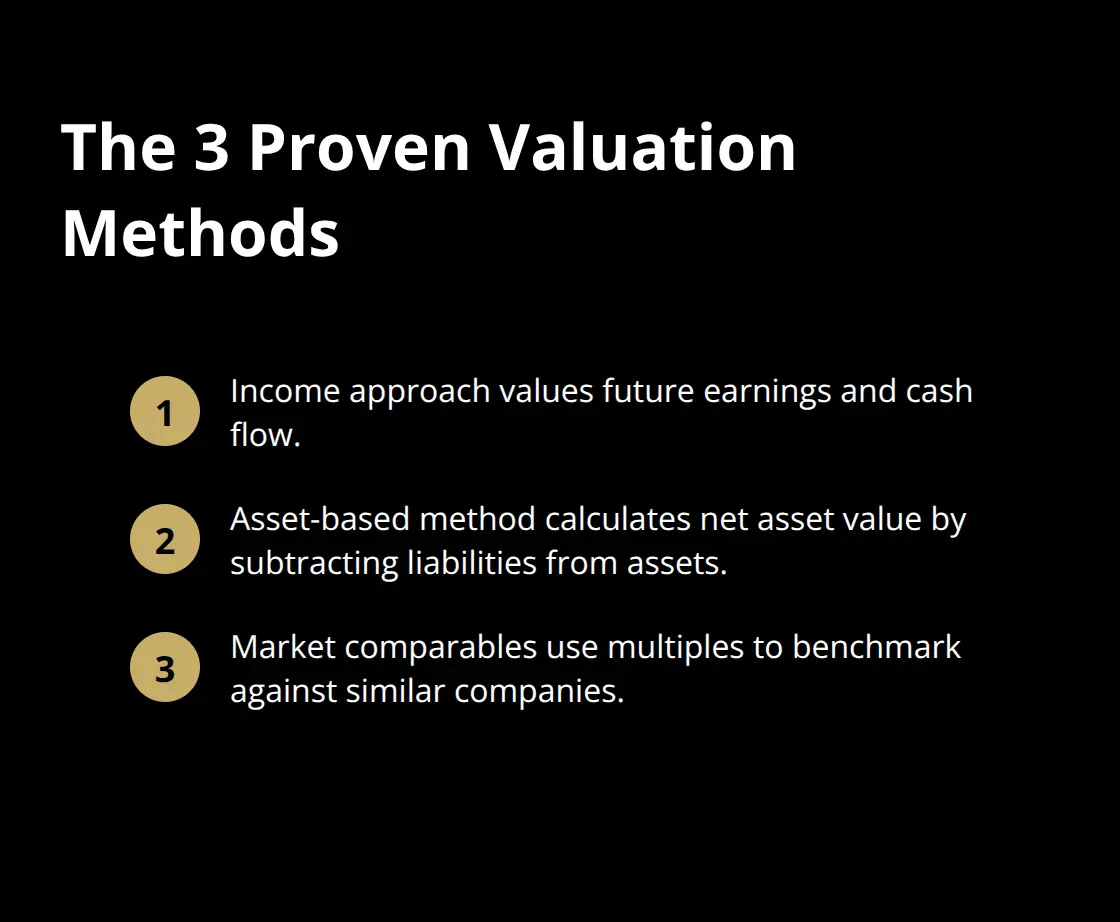

The Three Valuation Methods That Actually Work

Three distinct approaches determine what your business is worth, and each one tells a different story about your company. The income approach values your business based on future earnings and cash flow. The asset-based method involves calculating net asset value by subtracting liabilities from total assets. Market comparables evaluate financial metrics as ratios to compare different companies. Most business owners lean heavily on one method and ignore the others, which is a mistake. A realistic valuation pulls from all three because they serve different purposes depending on your situation and industry.

Income Approach Reveals Your Real Earning Power

The income approach, particularly using earnings multiples, directly ties your company’s value to its profitability. If your business generates $300,000 in annual earnings and your industry typically trades at 4 times earnings, your valuation lands around $1.2 million. This method works well for established businesses with consistent profit records because it reflects what future owners care about most: cash they can actually take home.

Accuracy matters enormously here. Many owners inflate their earnings by removing legitimate business expenses or counting one-time gains as recurring revenue. Strip out owner compensation that exceeds market rate, unusual one-time sales, and non-recurring expenses before you calculate your valuation. The discounted cash flow method takes this further. You project your earnings over five to ten years, then reduce those future earnings to today’s dollars using a discount rate that reflects your business risk. Higher risk businesses receive higher discount rates, which lowers their present value. This approach requires honest forecasting, not wishful thinking about growth rates.

Asset-Based Valuation Grounds You in Reality

The asset-based method adds up your tangible assets like equipment, inventory, and real estate, then subtracts all liabilities. This approach works best for asset-heavy businesses like manufacturing or for liquidation scenarios where you need to know what everything is worth if sold separately. However, most service and software businesses are worth significantly more than their net assets because they generate ongoing revenue streams that don’t show up on a balance sheet.

Market Comparables Provide Concrete Data

Market comparables ground your valuation in reality. You examine what similar businesses actually sold for recently. If three comparable businesses in your industry sold within the last eighteen months at four to five times revenue, you have concrete data for positioning your valuation. Industry benchmarks vary dramatically. A SaaS business might sell for eight to twelve times EBITDA while a local service business might fetch two to three times annual revenue. Business brokers in your industry or M&A databases that track actual transaction prices provide this data.

Combining All Three Methods Prevents Overvaluation

The combination of all three methods prevents overvaluation. If your income approach suggests $2 million but your assets only support $800,000 and comparable sales show $1.4 million, you have a problem with your earnings projections or a business that’s overpriced relative to the market. This discrepancy signals that you need to revisit your assumptions before you move forward with a sale or financing round. Understanding which method applies most to your business type sets the stage for identifying the specific factors that actually move your valuation up or down.

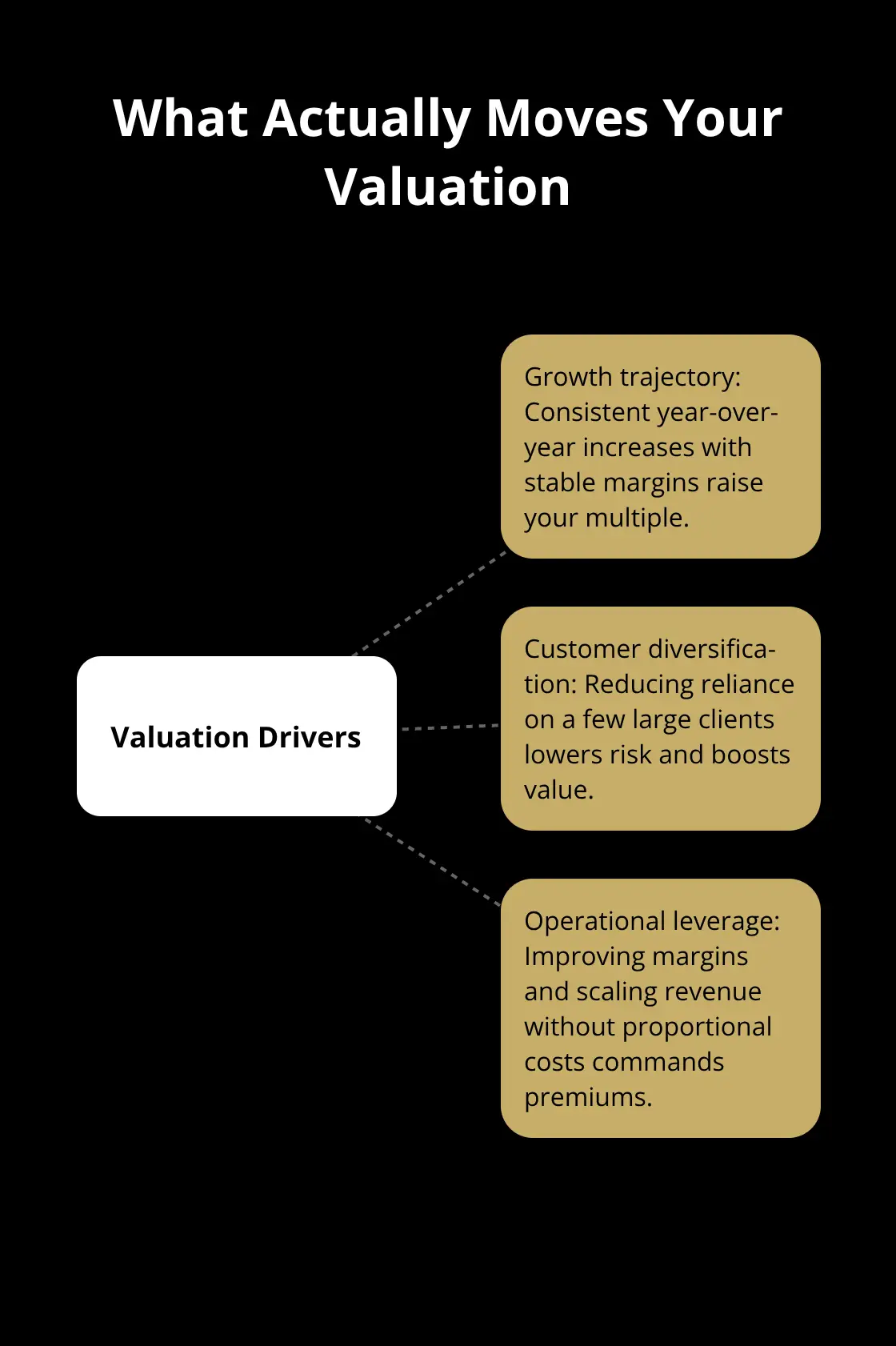

What Actually Moves Your Business Valuation

Revenue growth rates and profitability trends are the most direct levers for increasing what your business is worth, yet most owners focus on the wrong metrics. Your absolute revenue number matters far less than the consistency and trajectory of your profits. A business generating $500,000 in annual revenue with 40 percent profit margins is worth substantially more than a $2 million revenue business operating at 8 percent margins. Buyers care about cash flow, not top-line sales. If your revenue has grown 15 percent year-over-year for the past three years while maintaining stable profit margins, your valuation multiplier increases significantly.

Conversely, flat revenue for two consecutive years tanks your valuation even if profits remain unchanged. The reason is straightforward: buyers project future cash flows based on your trajectory. A stagnant business signals declining value regardless of current profitability.

Calculate your revenue growth rate over the past three to five years and compare it against industry benchmarks for your sector. SaaS companies typically show 20 to 40 percent annual growth rates at acquisition, while local service businesses might range from 5 to 15 percent. If you fall below your industry average, your earnings multiple compresses accordingly.

Customer Concentration Destroys Valuation

Customer concentration risk represents one of the most underestimated value killers in business valuations. If your top three customers represent more than 30 percent of annual revenue, most buyers immediately reduce their offer. A potential acquirer sees concentrated revenue as existential risk. Losing one major client could collapse profitability, which is unacceptable to someone paying a premium valuation multiple.

Diversify your customer base before pursuing a sale. If you operate with five major clients accounting for 80 percent of revenue, work aggressively to build relationships with 10 to 15 medium-sized clients over the next 12 to 18 months. This shift dramatically improves your valuation. Additionally, customer retention rates directly influence your multiple. A business retaining 85 to 90 percent of customers annually commands higher valuations than one with 60 to 70 percent retention. Calculate your annual customer churn rate by dividing lost customers by starting customers. Strong retention indicates predictable recurring revenue, which buyers value at premium multiples.

Operational Efficiency Multiplies Your Value

Operational leverage and scalability determine whether your business can grow without proportional cost increases. If your gross margin improves from 45 percent to 55 percent without corresponding revenue growth, that margin expansion directly translates to higher valuation multiples. Buyers pay premiums for businesses with operating leverage built in.

Examine your cost structure ruthlessly. Are you spending 25 to 30 percent of revenue on personnel? Are overhead costs declining as a percentage of sales? Businesses showing improving unit economics attract acquisition interest at substantially higher multiples than those with flat or deteriorating margins. Scalability matters equally. A business requiring proportional headcount increases to grow revenue is less valuable than one where revenue can scale with minimal additional costs. Software and digital service businesses command higher multiples specifically because they scale without linear cost increases. If your business model requires hiring one new employee for every $150,000 in additional revenue, that’s a 1:1 cost-to-revenue ratio that limits your valuation. Restructure toward models where one additional employee generates $300,000 or more in new revenue.

These three factors-growth trajectory, customer diversification, and operational leverage-form the foundation of what buyers actually pay for. Understanding how each one moves your multiple sets the stage for the next critical reality: the mistakes that tank valuations even when these fundamentals look solid.

Common Mistakes Business Owners Make When Valuing Their Companies

Overestimating Growth Without Evidence

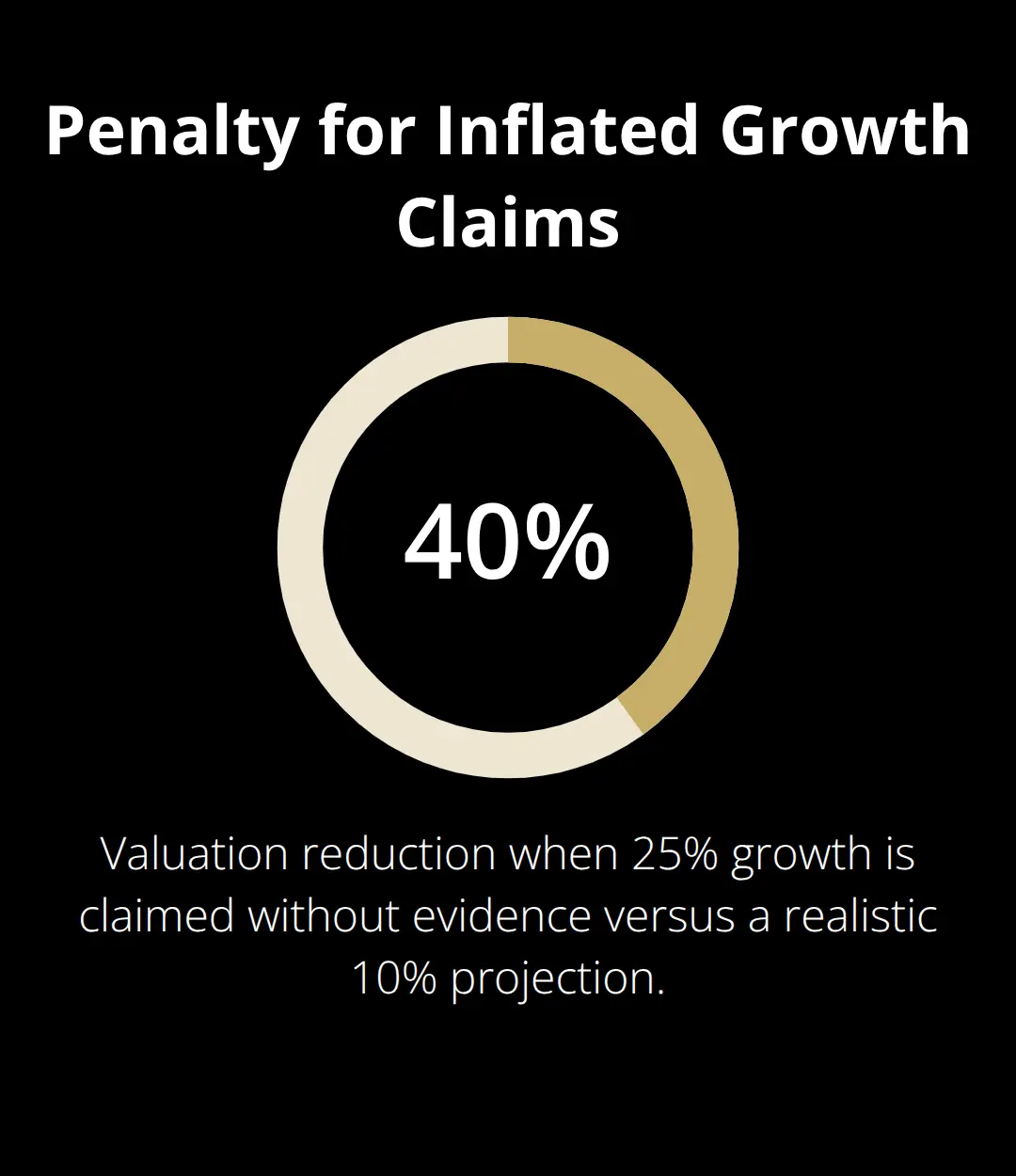

Most business owners make one fatal mistake when valuing their companies: they project growth rates that have no basis in reality. An owner shows historical revenue data that grew 8 percent annually over five years, then confidently projects 25 percent growth for the next three years without explaining what changes. Buyers see this immediately and discount your valuation accordingly.

If your industry typically grows at 6 to 10 percent annually and you claim 30 percent growth without a specific, executable strategy to capture new market share, acquisition professionals apply a lower multiple to your earnings. The discount can be brutal. A business with realistic 10 percent growth projections might trade at 5 times EBITDA while the same business claiming 25 percent growth without justification trades at 3 times EBITDA-a 40 percent valuation reduction from pure overconfidence.

Ground your growth assumptions in concrete facts: specific contracts already signed, documented market expansion plans with timelines, or quantified competitive advantages that competitors cannot replicate. Vague statements about market opportunity or team capability don’t move the needle with serious buyers.

Economic Cycles and Market Conditions

Economic cycles and market conditions destroy valuations when owners ignore them entirely. If you sell during a sector downturn, your valuation multiple compresses regardless of your company’s strength. Buyers see timing as critical to their returns.

Interest rates matter equally. When the Federal Reserve raises rates, buyer financing becomes expensive, which reduces how much they’ll pay for your business. A buyer financing a $2 million acquisition at 5 percent interest pays roughly $95,000 annually in debt service. At 8 percent interest, that same acquisition costs $160,000 annually, which means they reduce their offer to stay within acceptable debt-to-cash-flow ratios.

Failing to Address Owner Dependency

Owner dependency represents the silent valuation killer that surprises most entrepreneurs. If your business generates $500,000 in annual profit but you personally close 70 percent of sales, manage the largest client relationships, and handle all strategic decisions, buyers view your company as dependent on you. The moment you leave, revenue drops.

Acquisition professionals reduce valuations significantly when owner dependency is high. The only solution is documenting which revenue is truly repeatable without you. Transition your largest clients to other team members over the 6 to 12 months before approaching buyers. Build documented systems and processes that show the business runs without your daily involvement. If you cannot demonstrate that your business generates predictable revenue independent of your personal effort, buyers will pay accordingly-which means accepting a significantly lower offer.

Final Thoughts

An accurate valuation forms the foundation for every major business decision you’ll make, whether you’re selling, raising capital, or planning succession. The business valuation basics we’ve covered-income approach, asset-based methods, and market comparables-provide the framework to understand what drives your value. Honest assessment of your financials, realistic growth projections, and a clear-eyed view of your competitive position separate owners who maximize their exit from those who leave money on the table.

If you plan to sell within the next 12 to 24 months, commission a professional valuation from a qualified appraiser. This investment typically costs between $3,000 and $10,000 but provides defensible documentation that strengthens negotiations with buyers and lenders. Valuators bring objectivity you cannot provide yourself-they spot inflated assumptions, identify undervalued assets, and present findings in formats that buyers and lenders actually trust.

We at Unbroker work with business owners at every stage of the valuation and sale process. Our platform provides transparent pricing, expert support, and access to qualified buyers without the inflated fees traditional brokers charge. Your business represents years of work and financial investment, so valuing it accurately ensures you receive what it’s actually worth.