Selling your business without a broker means keeping more money in your pocket. At Unbroker, we’ve worked with hundreds of business owners who’ve successfully navigated this path on their own terms.

This guide covers the small business sale tips that actually work. You’ll learn how to prepare your business, price it right, and close the deal while protecting yourself every step of the way.

Get Your Business Ready to Sell

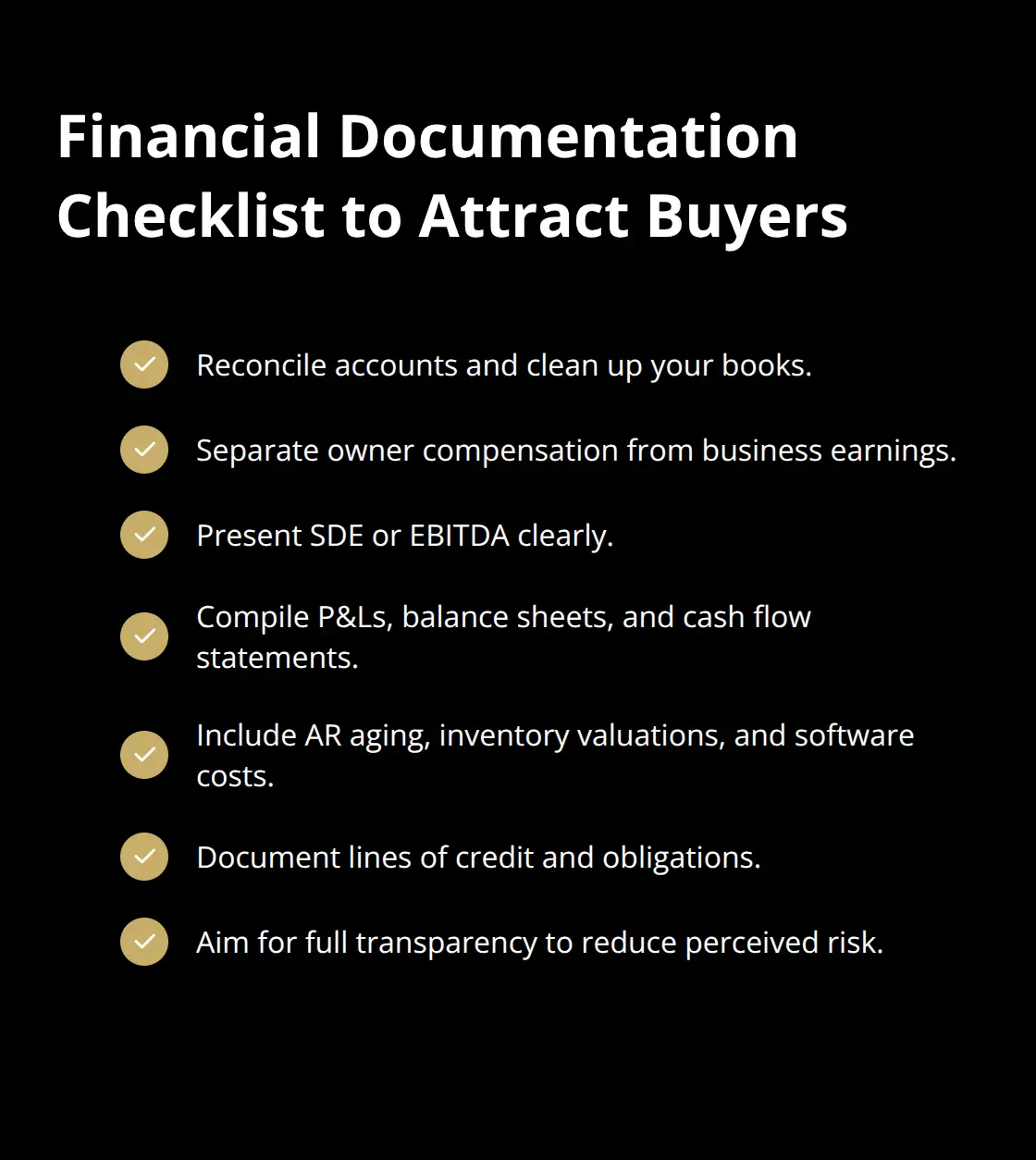

Your financial records and tax returns are the first thing buyers examine. You need at least three years of tax returns, profit-and-loss statements, balance sheets, and cash flow statements to prove your business is profitable. Many sellers present messy books, which immediately signals to buyers that something is wrong. Work with a small-business accountant to reconcile accounts, document all income streams, and clearly separate owner compensation from actual business earnings. Present your Seller’s Discretionary Earnings or EBITDA, depending on your business size, so buyers see the true earning potential.

Beyond raw numbers, gather software costs, accounts receivable aging reports, inventory valuations, and any lines of credit your business carries. Buyers want transparency here because they’re evaluating risk.

Show Revenue Durability Across Multiple Customers

Diversifying your customer base matters significantly. If one client represents more than 20 percent of revenue, buyers will discount your valuation because they see customer concentration risk and valuation discount. Start documenting your customer breakdown now so you can show revenue durability across multiple segments. This single metric often determines whether a buyer views your business as stable or fragile.

Document How Your Business Actually Works

Standard operating procedures documentation separate a business worth buying from a lifestyle business tied entirely to you. Write down exactly how you handle customer onboarding, order fulfillment, employee management, vendor relationships, and quality control. Buyers care deeply about this because they want to run your business without constant phone calls to you. Create simple, step-by-step documents for your core processes-not lengthy manuals, just practical guides that someone new could follow. If you’ve been doing everything yourself, delegate some tasks now to test whether your systems actually work when you’re not involved. This also reveals which processes are fragile and need strengthening before listing.

Fix Deal-Breakers Before Listing

Unresolved legal issues, pending compliance violations, aging equipment, outdated technology, or customer complaints become deal-breakers during due diligence. If your website looks like it hasn’t been updated since 2015, buyers assume your entire operation is neglected. Invest in a professional refresh of your online presence because buyers often form first impressions digitally. Check that all contracts with customers, suppliers, and employees are actually assignable to a new owner-many agreements contain clauses that terminate if ownership changes, which can tank the deal’s value. These fixes take time, so address them now rather than scrambling later.

With your business in solid shape, you’re ready to determine what it’s actually worth.

Navigate the Selling Process Without a Broker

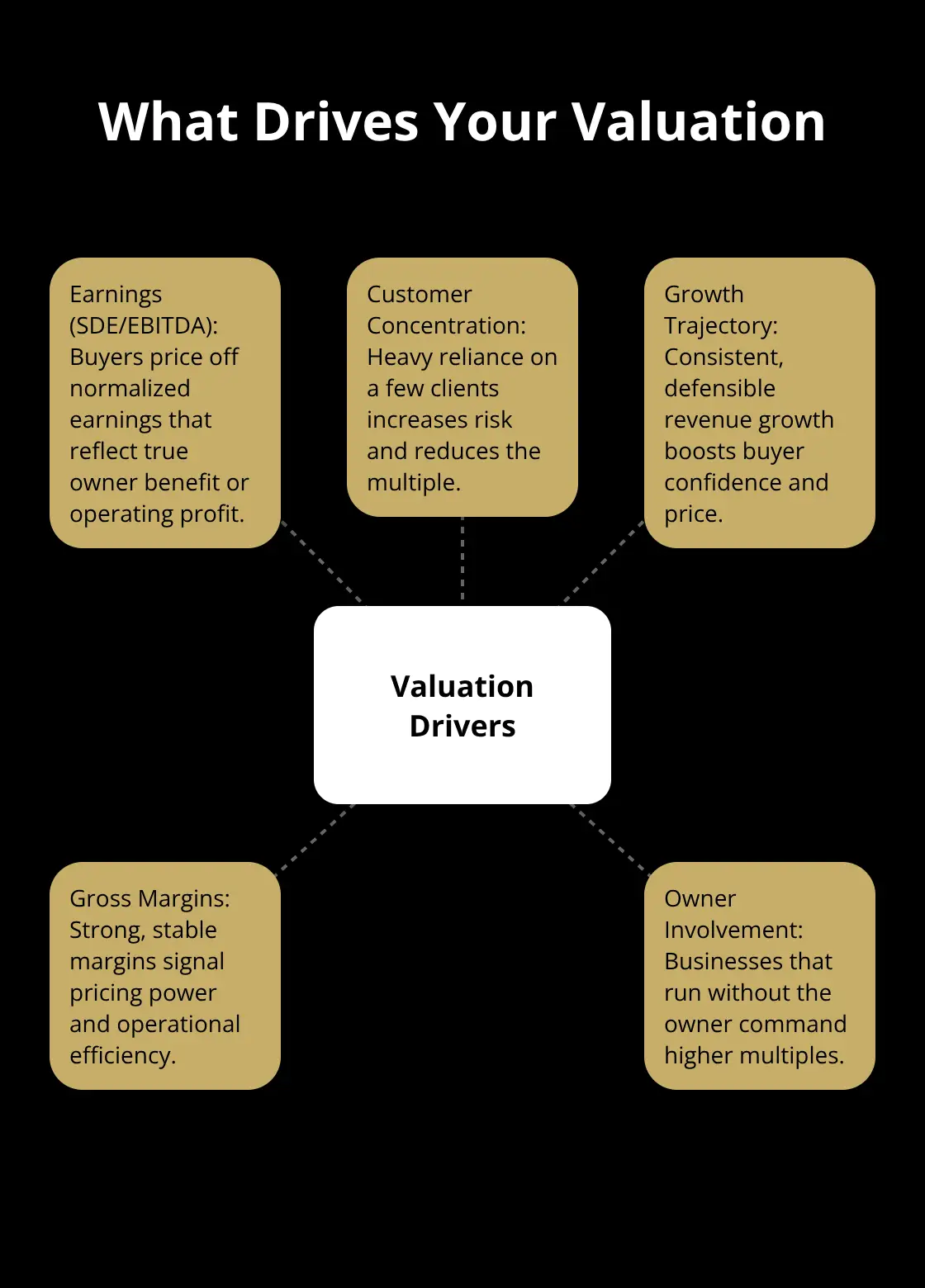

Getting your valuation right separates sellers who walk away satisfied from those who leave money on the table or fail to attract serious buyers. Most small business owners guess at their price based on revenue multiples they’ve heard or what they think sounds reasonable. This approach fails consistently because it ignores what actually determines a business’s worth.

Your valuation depends on several concrete factors: your Seller’s Discretionary Earnings (SDE) or EBITDA, your customer concentration, your revenue growth trajectory, the strength of your gross margins, and how much owner involvement the business requires. A business generating $100,000 in SDE with one customer representing 40 percent of revenue sells for far less than an identical business with revenue spread across fifty customers. Similarly, a business where you personally handle all client relationships commands a lower multiple than one with documented systems and a trained management team ready to operate without you.

Calculate Your Realistic Asking Price

Start with your realistic SDE or EBITDA using three years of historical data, then apply a multiple that reflects your specific risk factors. For most small businesses, common multiples are two to four times SDE depending on these variables. Marketplaces like Empire Flippers publish valuation data showing what actually sold and at what multiples, giving you real market comparisons rather than guesses. Use multiple valuation approaches-asset-based, income-based, and market comps-then triangulate toward a realistic asking price.

Price too high and you’ll waste months with tire-kickers who aren’t serious; price too low and you’ll regret the decision for years.

Identify and Reach Your Ideal Buyer

Direct marketing requires identifying who actually wants to buy your business, then reaching them where they pay attention. Your ideal buyer has specific characteristics: they understand your industry, they have capital or access to financing, and they’re actively looking to acquire rather than passively browsing. This means targeting them through industry-specific channels rather than general business marketplaces.

If you run a service business, reach out to complementary service providers who could expand their offerings by acquiring you. If you operate in a niche, connect with industry associations, trade publications, and online communities where potential buyers congregate. Email outreach works better than cold calls when you’re selling a business because buyers need time to absorb information and run numbers.

Research each prospect thoroughly, then send a brief, specific email explaining why your business would benefit them specifically. Mention concrete details: your customer base, your recurring revenue percentage, your margins, and why acquiring you makes strategic sense for their operation. A generic email to fifty prospects generates far fewer leads than a personalized email to five genuinely qualified prospects. Post on industry-specific platforms and consider placing your business on marketplaces where serious buyers already search, understanding that each channel reaches different buyer profiles. Track which channels produce actual inquiries versus noise so you can focus energy where it works.

Negotiate From a Position of Strength

Negotiations favor the side with better information and stronger alternatives. If you have multiple interested buyers, you hold leverage; if you’re desperate to sell, buyers sense it immediately and lowball you. Start negotiations with a clear minimum price you’ll accept and walk away from offers below that threshold-this discipline prevents emotional decisions that undermine your financial outcome.

When a buyer raises an objection about price, don’t immediately discount; instead, ask what specific concerns drive their resistance. They might worry about customer retention, key employee departures, or integration challenges. Address those concerns with concrete evidence from your documentation rather than reducing your asking price. A buyer who questions whether customers will stay might be satisfied by showing long-term contracts or recurring subscription agreements. One concerned about key employees might want to see your systems documentation proving the business doesn’t depend on individuals.

Separate price discussions from other terms. A buyer might accept your full asking price if you offer seller financing for part of the purchase or agree to a transition period where you’re available for questions. These creative structures preserve your valuation while addressing their cash flow concerns. Document every conversation and send written summaries confirming what was discussed and what the next steps are. This prevents misunderstandings and creates a clear record if disputes arise later.

Negotiations typically extend four to eight weeks, so patience and consistency matter more than aggressive tactics. Once you’ve reached agreement on price and terms, you’ll move into the critical phase where legal protections and buyer verification become essential to closing the deal successfully.

Protect Yourself During the Transaction

The moment a buyer shows serious interest, you shift from marketing mode into protection mode. This is where most sellers without brokers stumble because they lack the legal framework to safeguard themselves.

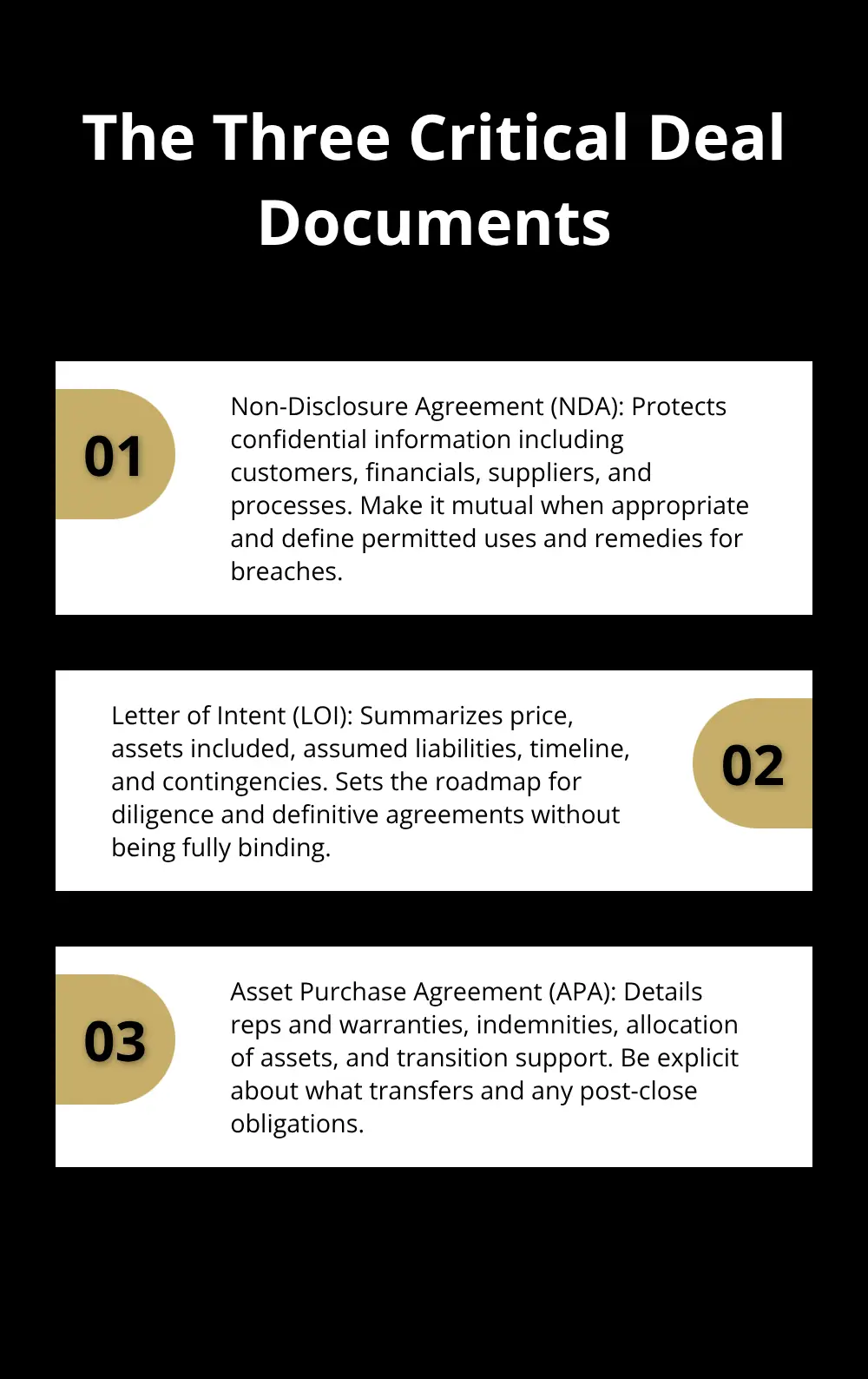

You need three critical documents before any buyer accesses your financials or operational details: a non-disclosure agreement that legally binds them to confidentiality, a letter of intent that outlines the basic terms both parties agree to pursue, and an asset purchase agreement that specifies exactly what’s being sold and on what terms.

These aren’t optional formalities. Without an NDA, a buyer who decides not to proceed can use your customer list or operational knowledge to compete against you directly. Without an LOI, you waste weeks negotiating with someone who disappears when they realize they can’t secure financing. Without a purchase agreement, you end up in disputes about what was actually promised. SCORE and the Small Business Administration both emphasize that you must prepare these documents before serious negotiations begin, not scramble them together at the last moment when emotions run high and you’re desperate to close.

Use Legal Templates and Documentation

An NDA should cover all proprietary information including customer data, financial performance, supplier relationships, and operational processes. Your LOI should specify the purchase price, what assets transfer, what liabilities the buyer assumes, the timeline for closing, and any contingencies like financing approval or customer retention milestones. The purchase agreement goes further, detailing representations and warranties you’re making about the business, indemnification clauses that protect you if hidden problems surface after closing, and transition support obligations.

Professional-grade templates save you thousands in attorney fees while ensuring solid protection. Many online resources provide these documents at reasonable cost, and some platforms offer them as part of their service offerings.

Verify Buyer Credibility and Financing

Verification happens simultaneously with documentation because a buyer’s ability to actually pay matters more than their enthusiasm. Before you reveal sensitive information, request proof of funds showing they have cash or committed financing for the purchase price. This single step eliminates tire-kickers and time-wasters instantly. A legitimate buyer expects this request and responds quickly with bank statements or a pre-approval letter from their lender. Someone who hesitates or gets defensive about providing proof of funds probably can’t actually afford your business.

Maintain Confidentiality Throughout the Process

During the entire selling process, maintain strict confidentiality by revealing your business identity only to qualified buyers who’ve signed the NDA. Many sellers make the mistake of discussing their sale broadly with employees, vendors, or industry contacts, which leads to rumors that damage business value or create panic among your team. Key employees often leave when they hear the business is being sold, and vendors may demand payment terms changes or price increases if they think new ownership is coming.

Restrict information to a need-to-know basis until you’ve signed a purchase agreement and are ready for transition planning. When you do involve employees, frame the sale positively and explain why the buyer is a good fit for the business and their roles.

Address Change-of-Control Clauses in Contracts

Contracts with customers, suppliers, and employees deserve special attention because many contain change-of-control clauses that terminate automatically when ownership transfers. Review every significant agreement now to identify which ones require buyer consent or renegotiation before closing. If a contract terminates upon sale, that revenue disappears from your valuation and the deal’s attractiveness declines dramatically.

Some sellers renegotiate these agreements proactively with customers before listing, converting them to longer-term contracts that survive the ownership change. This removes a major deal risk and increases your asking price because the buyer inherits stable, protected revenue streams.

Final Thoughts

Selling your business without a broker works when you approach it systematically, and the small business sale tips that actually deliver results share one common thread: preparation beats improvisation every time. Successful sellers spend weeks getting their financials clean, their processes documented, and their legal protections in place before they contact a buyer. They price realistically using actual market data rather than guesses, verify buyer credibility before revealing sensitive information, and negotiate from strength by understanding their business’s true value.

The path forward depends on how much support you want along the way. If you handle everything yourself, you’ll need solid legal templates, realistic pricing benchmarks, and discipline around confidentiality. If you want expert guidance without paying traditional broker commissions, Unbroker provides transparent options designed specifically for DIY sellers, offering legal document templates, negotiation assistance, and access to qualified buyers through AI-driven processes.

Your next step is deciding your timeline. If you sell within the next six months, start organizing your financial records and documentation immediately. If you plan further ahead, use this time to strengthen your business by diversifying customers, improving margins, and building systems that operate without you.