Most founders skip valuation until they need it. At Unbroker, we’ve seen this cost business owners millions when selling, raising capital, or planning succession.

Understanding business valuation basics isn’t just for exit planning. It shapes every major decision you make about growth, investment, and strategy.

What Actually Moves Your Business Valuation

Your revenue number sits at the center of every valuation conversation, but it tells only half the story. Investors and buyers scrutinize profitability far more than raw sales. A business generating $2 million in annual revenue with 40% net profit margins commands a dramatically different valuation than one with identical revenue but 5% margins. The reason is straightforward: profit determines what a buyer actually takes home.

Profitability and EBITDA Matter Most

When you prepare for valuation, calculate your EBITDA with precision. This metric removes accounting distortions and shows the true operational performance that buyers care about. Strip out owner compensation that exceeds market rates-if you pay yourself $500,000 annually when the role typically costs $150,000, that difference gets added back to earnings. This adjustment reveals the real earning power a new owner would inherit.

Growth Trajectory Reduces Risk

Growth trajectory matters intensely because it reduces perceived risk. A business growing 30% annually commands a higher multiple than a flat business with identical current profits. According to research from private equity firms, companies demonstrating consistent year-over-year revenue growth of 20% or more see valuation multiples increase compared to stagnant competitors.

Your market position directly influences these growth expectations. If you control 15% of a fragmented market with room to consolidate, buyers see expansion potential. If you fight for scraps in a saturated space, growth projections become skeptical.

Tangible and Intangible Assets Shape Value

Tangible and intangible assets reshape valuations in ways founders often underestimate. Proprietary technology, patents, customer lists, and brand recognition can add millions to your valuation if you document them properly. A software company with three issued patents and defensible IP typically attracts higher multiples than identical companies without patent protection.

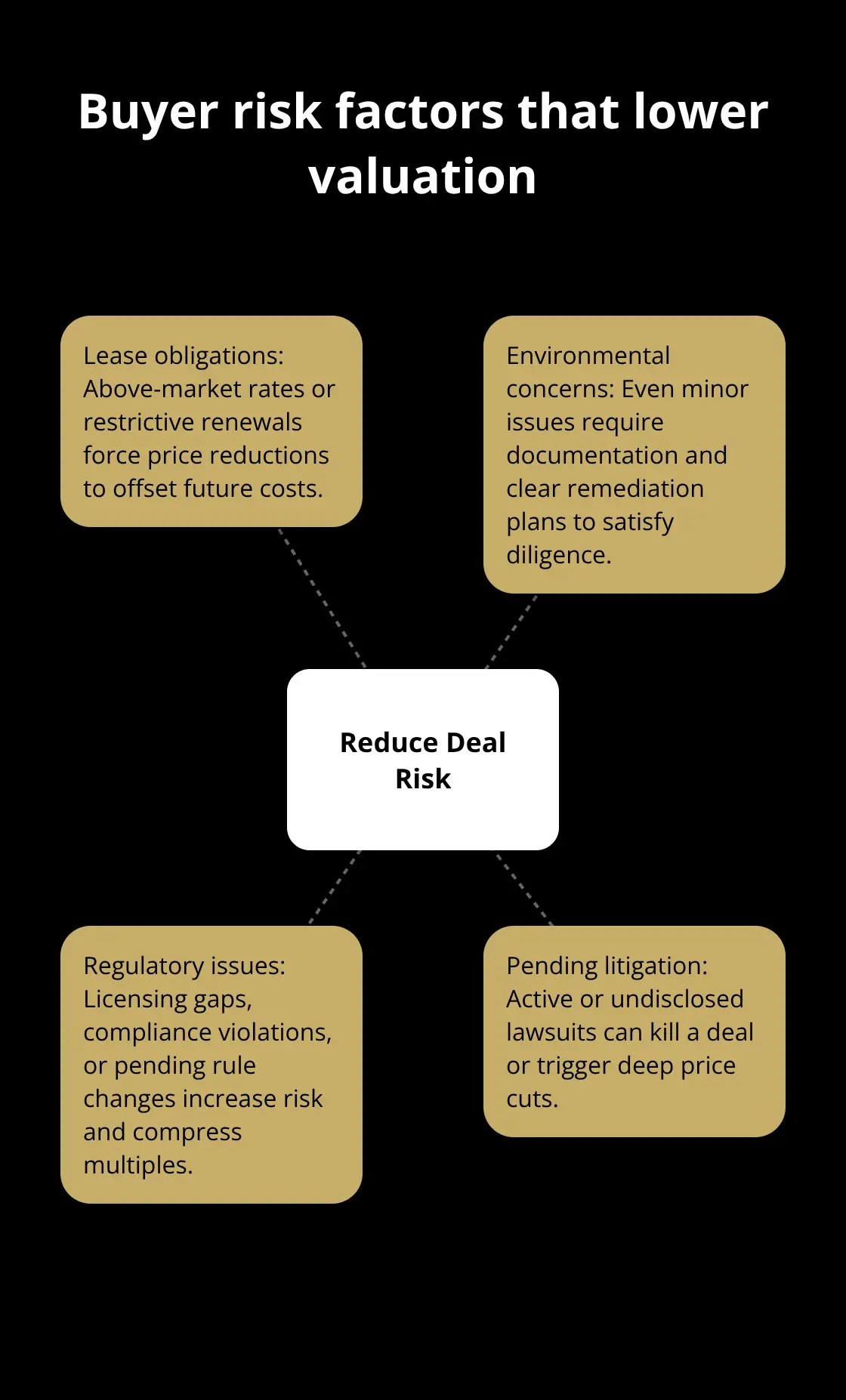

Conversely, liabilities drain value aggressively. Accumulated debt, pending litigation, lease obligations, and environmental issues all reduce what a buyer will pay. If your business carries $500,000 in outstanding debt, that amount comes directly off the sale price. The same applies to leases-a long-term lease with unfavorable rates becomes a liability that discounts valuation.

Conduct a Thorough Asset Audit

Conduct a thorough asset audit six months before any valuation or sale process. Document every patent, trademark, and software license. List customer contracts with renewal terms. Identify all liabilities, including off-balance-sheet obligations. This groundwork prevents nasty surprises during due diligence and strengthens your negotiating position.

Physical assets matter less in modern valuations than they did decades ago, but they still count. Real estate holdings, equipment, inventory, and working capital all contribute to enterprise value. However, quality matters more than quantity-outdated equipment sitting idle reduces valuation, while lean, productive assets increase it. Once you understand what drives your business value, the next step involves selecting the right method to calculate it.

Common Business Valuation Methods

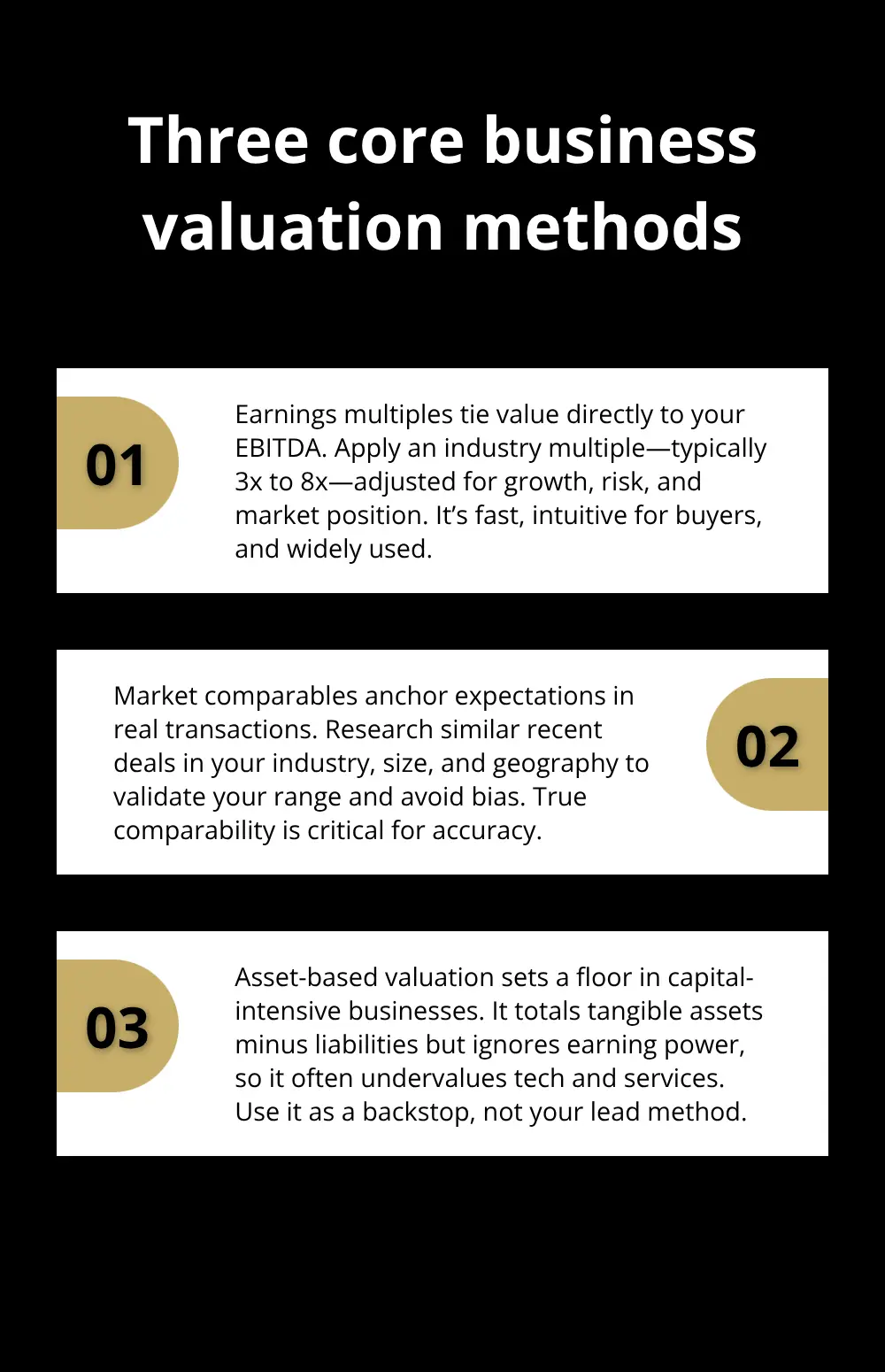

Earnings Multiples: The Founder’s Primary Tool

The earnings multiple approach remains the most practical method for founders because it directly ties valuation to what your business actually generates. Take your EBITDA figure and multiply it by an industry-specific multiple, typically ranging from 3x to 8x depending on your sector, growth rate, and market position. Software-as-a-service companies consistently command 6x to 8x multiples due to recurring revenue predictability, while manufacturing businesses typically sit at 3x to 5x multiples. The multiple itself reflects risk and growth potential-a high-growth SaaS company at 40% annual expansion might justify 8x multiples, whereas a flat manufacturing business warrants 3x. This method works because buyers already understand it; when you present a $5 million EBITDA business valued at 6x, they immediately calculate the $30 million price without confusion.

The weakness emerges when your EBITDA fluctuates wildly or when you operate in an emerging sector without established multiples. In those cases, you need secondary validation.

Market Comparables: Anchoring Your Valuation in Reality

Market comparables provide that validation by showing what similar businesses actually sold for recently. Research recent acquisitions of comparable companies in your industry, geography, and size using sources like Crunchbase or industry databases. If three similar software companies sold in the past eighteen months at 5.5x to 6.5x revenue multiples, and your revenue sits at $8 million with 35% growth, you anchor your valuation range realistically between $44 million and $52 million.

The critical mistake founders make is selecting comparables that aren’t truly similar-comparing your high-growth SaaS business to a declining legacy software company skews the analysis entirely. Spend time verifying that your comparables match your business model, stage, and market conditions. This rigor prevents you from overvaluing or undervaluing your company based on flawed benchmarks.

Asset-Based Valuation: A Safety Floor, Not a Primary Method

Asset-based valuation rarely drives modern business valuations unless you operate in capital-intensive industries like real estate, manufacturing, or equipment leasing. This method adds up tangible assets minus liabilities, but ignores earning power entirely, producing artificially low numbers for most tech and service businesses.

However, if your business owns significant real estate, proprietary equipment, or inventory, asset value serves as a valuation floor-your business shouldn’t sell below what the assets alone are worth. Use earnings multiples as your primary method, validate with market comparables, and reference asset value only to confirm you’re not underpricing physical holdings. Once you’ve selected your valuation method and calculated a realistic range, the next critical step involves preparing your business to withstand the scrutiny that buyers and investors will apply.

Getting Your Business Ready for Valuation

Organize Financial Records with Precision

Before any valuation conversation happens, your financial records must be bulletproof. Buyers and investors spend weeks examining every document you provide, looking for inconsistencies, hidden liabilities, or accounting red flags. Start by collecting your financial statements from the past three years-tax returns, bank statements, profit and loss statements, and balance sheets. If your accounting has been sloppy-mixing personal and business expenses, recording transactions informally-hire an accountant to reconcile everything before a buyer sees it. The cost of this cleanup, typically $2,000 to $8,000 depending on complexity, pays for itself many times over because buyers won’t discount your valuation for messy books if the numbers reconcile cleanly.

Document the source of every revenue stream with absolute clarity. If 40% of your income comes from three major clients, show contracts proving those relationships are real and renewable. Vague revenue explanations tank valuations faster than anything else. Separate owner compensation from operational expenses with surgical precision. If you’ve paid yourself irregularly or taken personal loans from the business, normalize these numbers now. A buyer needs to see what the business actually generates for an owner operating it professionally.

Identify and Resolve Outstanding Issues

Beyond financials, identify every liability and obligation that could surprise a buyer during due diligence. Pull your credit report, review all lease agreements, check for pending litigation or regulatory issues, and list any environmental concerns. If your business faces a lawsuit, disclose it early rather than hoping it disappears-undisclosed liabilities can kill a deal or slash the final price dramatically.

Lease agreements deserve special attention because unfavorable terms become significant liabilities. If you operate under a lease with rates well above market rates or restrictive renewal terms, a buyer will demand a price reduction to offset that burden. Environmental concerns, even minor ones, require documentation and remediation plans. Regulatory issues in your industry (licensing requirements, compliance violations, or pending rule changes) all factor into buyer risk assessments and valuation adjustments.

Secure Professional Valuation Assessment

Get a professional valuation assessment from a qualified business appraiser who holds credentials like the American Society of Appraisers designation. This typically costs $3,000 to $10,000 but provides the independent third-party validation that serious buyers demand. The appraiser will apply multiple valuation methods to your specific situation, stress-test your financial projections, and identify which factors most influence your valuation. They’ll also catch issues you missed.

More importantly, their report becomes your shield during negotiations-when a buyer questions your valuation, pointing to a professional assessment deflects emotional arguments and anchors discussions in methodology. The appraiser’s credentials and methodology carry weight that your own calculations cannot match, no matter how accurate they are. This independent perspective strengthens your negotiating position substantially and prevents buyers from anchoring on artificially low opening offers.

Final Thoughts

Understanding business valuation basics transforms how you approach growth, fundraising, and exit planning. The metrics that drive your valuation today-profitability margins, growth trajectory, asset quality, and liability management-shape every strategic decision you make right now. When you grasp how buyers and investors actually calculate value, you stop making decisions that inadvertently tank your company’s worth.

Earnings multiples give you a practical framework for understanding what your business generates, while market comparables ground your expectations in real transactions. Asset-based approaches provide safety floors, and professional appraisals deliver the credibility that serious buyers demand. Using multiple methods simultaneously prevents the dangerous mistake of relying on a single number that might be wildly off.

Your next steps depend on where you stand. If you’re not planning an exit soon, audit your financial records anyway and identify liabilities that could surprise buyers later. We at Unbroker help founders navigate the selling process with transparent, low-cost options that eliminate the traditional brokerage fees that drain value.