Business valuation isn’t magic-it’s built on concrete factors that buyers examine closely. At Unbroker, we’ve seen how understanding these valuation factors explained can transform how you prepare your business for sale.

Your revenue, profit margins, market position, and team quality all matter. We’ll walk through each driver so you know exactly what influences your business’s worth.

Financial Performance and Profitability

Revenue tells only part of the story. Buyers examining your financials want to see consistent growth over three to five years, not a single spike. A company growing 15% annually for five years signals market acceptance and scalability far better than one that jumped 40% once then flatlined. This consistency matters because buyers project future cash flows based on historical patterns. If your revenue has been erratic, expect them to apply a lower multiple or demand a discount.

Growth Quality Matters More Than Growth Speed

Growth in high-margin products or services amplifies your value more than growth in low-margin offerings. A SaaS company growing subscription revenue at 20% annually with 70% gross margins commands a higher valuation than a services firm growing at 20% with 40% margins. The difference lies in what each dollar of revenue actually produces for the owner.

Cash flow is where theory meets reality. Many business owners focus on profit on paper while ignoring actual cash movement. A profitable company that ties up cash in inventory or extends payment terms to customers looks less attractive to buyers than one converting profits into usable cash quickly. Your operating margins matter too. If your gross margin sits at 45% but your net margin is only 8%, buyers will question your cost structure and operational efficiency. They’ll scrutinize whether your overhead can be reduced post-acquisition or whether those costs are locked in.

The Economics of Your Customer Base

Customer acquisition cost relative to lifetime value determines whether your business is genuinely profitable. If you spend $5,000 acquiring a customer who generates $6,000 in total revenue over their relationship, that equation fails. Buyers model this carefully. They want to see that your cost to acquire a customer recovers within 12 to 18 months through repeat purchases or long-term contracts.

Subscription businesses have an advantage here because recurring revenue makes lifetime value predictable. A software company with customers paying $200 monthly who stay for an average of four years has a lifetime value of $9,600 per customer. That justifies higher acquisition spending and commands higher valuations.

Why Retention Reveals True Business Health

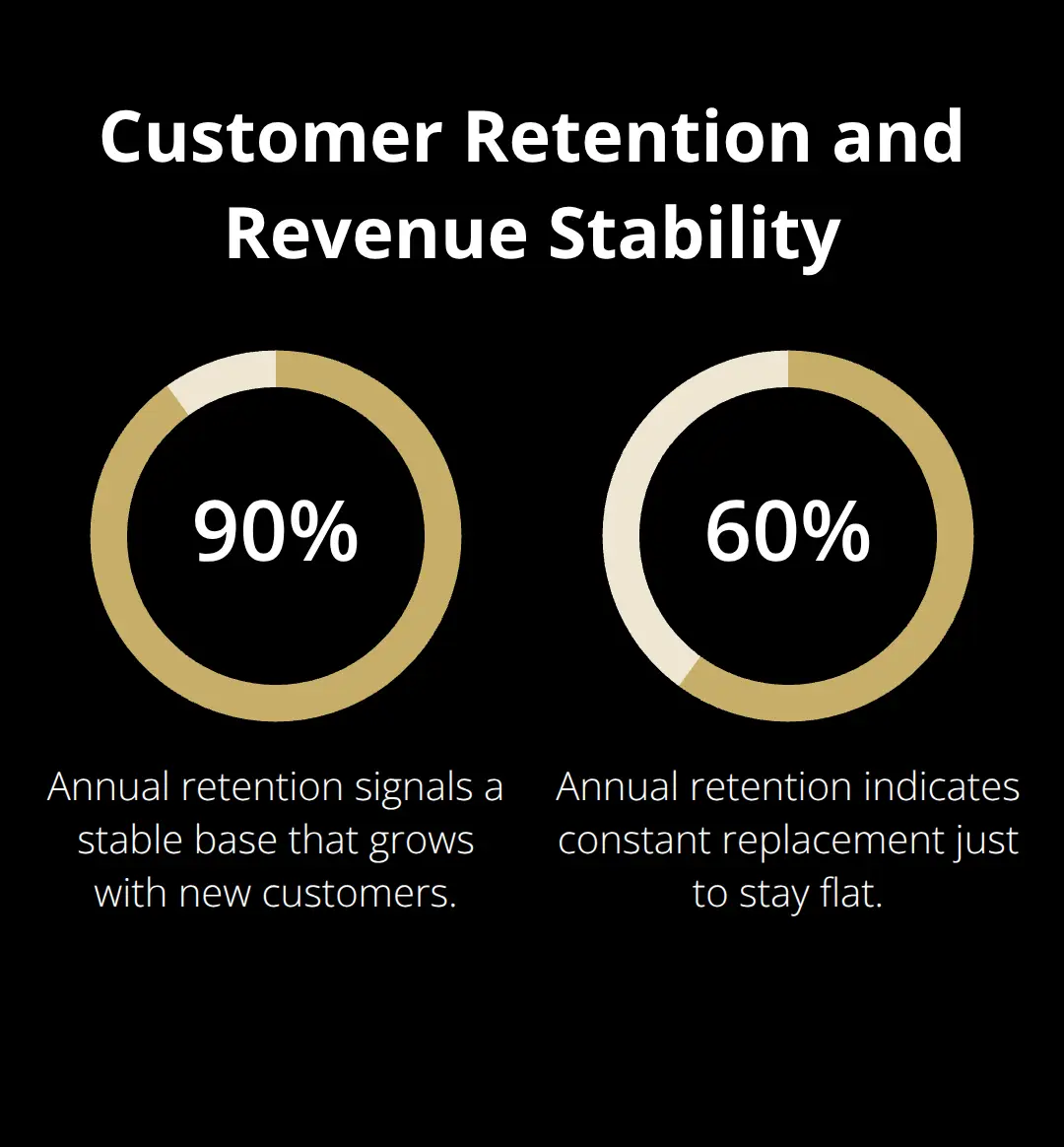

Customer retention rates reveal business quality more honestly than acquisition metrics alone. A 90% annual retention rate means your revenue base is stable and grows incrementally through new customers. A 60% retention rate means you constantly replace lost customers just to maintain flat revenue.

Buyers heavily penalize low retention because it signals either a poor product, weak customer relationships, or fierce competitive pressure.

Track these numbers ruthlessly before putting your business on the market. If your retention is weak, fix it first rather than hoping buyers overlook the problem. Strong retention combined with healthy margins and consistent growth creates the financial foundation that buyers value most. These metrics also set the stage for how your market position and competitive advantages will influence the final valuation.

Market Position Shapes What Buyers Will Pay

Your market position determines whether a buyer sees your business as a commodity or an asset worth a premium. Brand strength matters far more than most owners realize. A company with recognized brand identity can charge higher prices than competitors offering identical products or services. This pricing power flows directly into margins, which we covered earlier, but it also signals to buyers that your customer relationships are defensible. If customers choose you over cheaper alternatives, that choice reflects brand trust, not just habit. Buyers value this because they inherit that trust when they acquire your business.

Market Share in Growth Industries

Market share in a growing industry amplifies your valuation significantly. A company holding market share in an expanding market looks far more attractive than one holding share of a stagnant market. Growth trajectory matters because it suggests you can maintain or expand share without fighting harder just to stay even. Your positioning within that industry context matters equally. Being a market leader in a declining industry still attracts less valuation interest than being a strong number-two player in a high-growth sector where you can scale rapidly.

Competitive Differentiation and Your Moat

Competitive differentiation determines whether that market share is secure or constantly under threat. If your competitive advantage comes from proprietary technology, exclusive supplier relationships, or a unique service model that competitors cannot easily replicate, buyers assign higher multiples to your earnings. Conversely, if competitors can copy your offering within months, expect a valuation discount. The strength of your moat-whether through patents, customer switching costs, network effects, or operational excellence-directly influences how confident buyers feel about future cash flows.

A manufacturing company with proprietary processes that cut production costs significantly below industry average has a defensible advantage. A retail business competing solely on location or price has minimal protection. These differences shape how buyers model your future performance and what they’ll pay today.

Industry Growth and Valuation Multiples

Industry growth outlook shapes valuation multiples across entire sectors. Technology and healthcare businesses typically command higher multiples than mature industries like manufacturing or distribution because buyers expect stronger future cash flows. Strong financial performance signals competitive strength to buyers, while companies with weaker margins struggle to attract premium valuations.

Assess your competitive position honestly before valuation discussions begin. If you lack meaningful differentiation, consider what you can build or acquire in the next 12-24 months to strengthen your moat. Buyers respond to businesses that have durable advantages, not just temporary market success. This foundation of competitive strength directly influences how operational factors-your management team, customer relationships, and assets-will affect your final valuation.

Operational and Asset-Based Factors

Your management team represents the biggest operational risk in any business sale. Buyers don’t just assess your current financial performance-they evaluate whether the business survives and thrives after you step back. If your company depends entirely on you making decisions, closing deals, or managing key relationships, that concentration creates massive valuation risk. A private equity group conducting due diligence will stress-test whether your operations function without your daily involvement. If the answer is no, they’ll apply a significant discount or walk away entirely.

Documented processes, capable second-in-command leadership, and clear decision-making authority outside your hands matter far more than most owners acknowledge. A management team with documented tenure, relevant industry experience, and proven ability to execute without micromanagement commands higher valuations than a business where the owner is the only person who understands critical functions.

Team Composition and Professional Maturity

Buyers examine your org chart with the same scrutiny they apply to your financials. A company with a CFO who can explain cash flow dynamics, an operations manager who owns process improvement, and a sales leader with a track record in your industry signals professional maturity. These roles indicate the business has moved beyond founder-dependent operations. Conversely, a team of long-time loyalists without formal credentials or external experience raises red flags about whether they can adapt to new ownership or integrate with an acquirer’s systems.

Document your team’s accomplishments explicitly. If your VP of Operations reduced production costs by 18% over three years, that’s a concrete asset. If your sales director built a repeatable process that generates qualified leads at a predictable cost, that process survives ownership transition and justifies higher valuation multiples. Buyers pay premiums for businesses where key talent signs employment agreements extending beyond closing. If your top three people will stay and perform under new ownership, that dramatically reduces perceived risk and increases what a buyer will offer.

Customer Relationships and Concentration Risk

Customer concentration risk cuts both ways operationally. It forces buyers to tighten terms, lower valuation multiples, and observe your customer relationships more closely. More importantly, it signals that customer relationships depend on your personal involvement. Buyers fear that when you exit, that customer follows you.

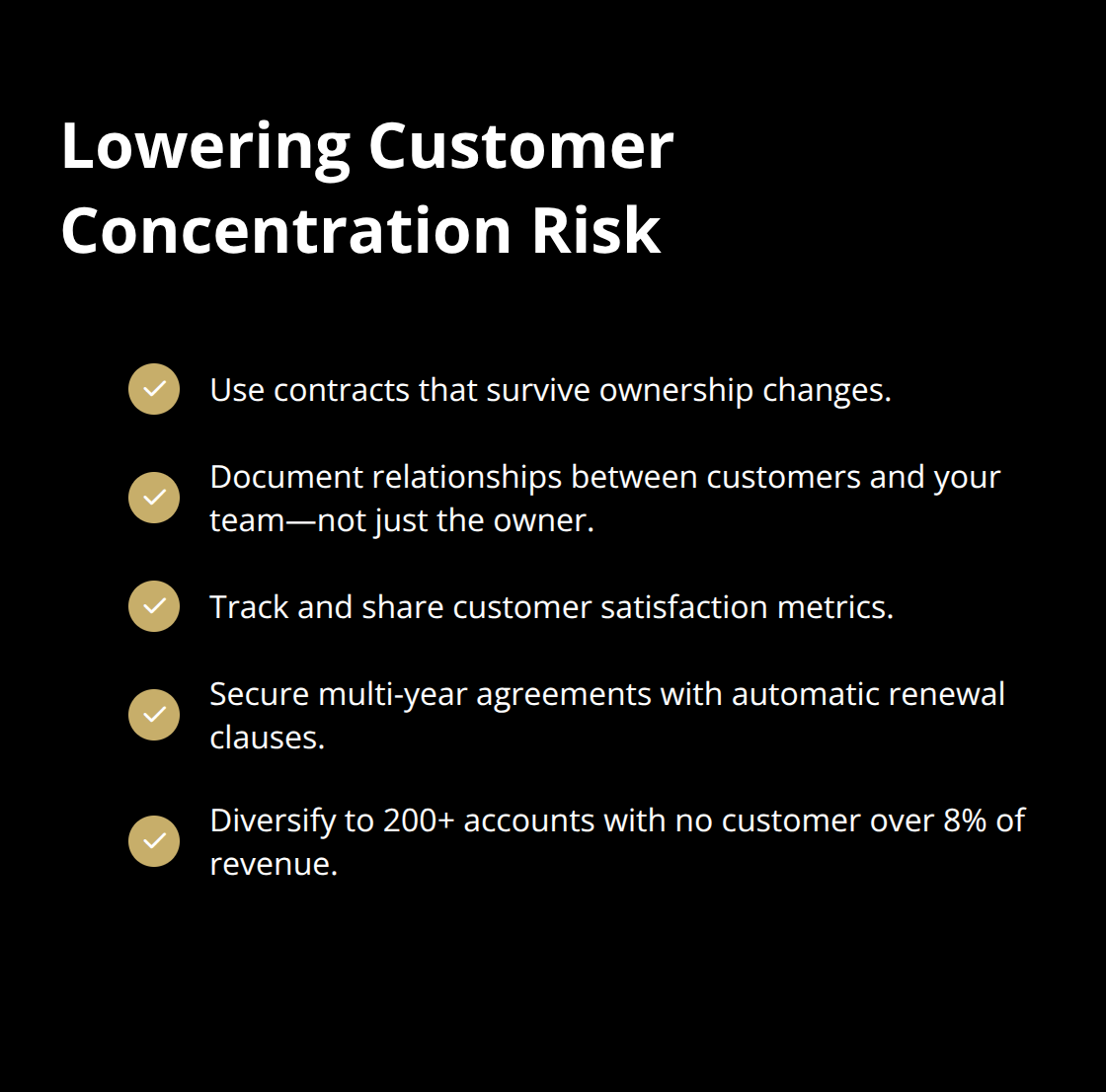

Combat this through formal contracts that survive ownership change, documented relationships between the customer and your team rather than just you, and demonstrated satisfaction metrics. If your top ten customers have multi-year contracts with automatic renewal clauses and your operations team manages those accounts directly, concentration risk drops substantially and valuation improves. A customer base that spans 200+ accounts with no single customer exceeding 8% of revenue looks far more stable, even if total revenue is identical.

This diversification means your business survives individual customer loss without operational disruption.

Intellectual Property and Proprietary Systems

Proprietary technology, software, or processes function as operational assets that directly impact margins and scalability. A manufacturing company with in-house software that optimizes production scheduling saves money every single day that software runs. A services firm with proprietary methodologies that standardize delivery and reduce labor costs compounds that advantage with every new client engagement.

Document what you own. If you’ve developed custom software, file provisional patents if applicable. If you’ve built unique processes, create written operating manuals that codify that knowledge. If you hold trade secrets, protect them through confidentiality agreements with employees. Buyers conduct IP searches and review licensing arrangements. If your competitive advantage rests on technology you’ve licensed from a third party, that advantage walks away if licensing terms change post-acquisition. Owned intellectual property that you can transfer cleanly to a new owner significantly strengthens valuation and deal certainty.

Physical Assets and Operational Value

Physical assets matter less than most owners assume, but they matter strategically. A manufacturing business with specialized equipment that took years to master commands valuation based on that equipment’s productive capacity and replacement cost. A service business with minimal physical assets focuses valuation entirely on people, processes, and customer relationships. Assess what’s actually driving your margins and cash flow, then ensure those assets are documented, owned outright where possible, and clearly transferable in a transaction.

Final Thoughts

Buyers will stress-test your financial performance, competitive position, and operational stability against each valuation factor. They model your cash flows under different scenarios, benchmark your margins against competitors, and evaluate whether your team executes without you. They scrutinize customer concentration, verify your intellectual property ownership, and assess whether your competitive advantages hold up or fade quickly.

Preparing your business for sale means addressing these factors systematically before the sale process starts. Document your financial trends across three to five years, strengthen your management team with employment agreements extending past closing, and diversify your customer base if concentration risk exists. Formalize your processes and intellectual property so they transfer cleanly to new ownership, and build your competitive moat through patents, exclusive relationships, or operational excellence that competitors cannot replicate.

The gap between what you think your business is worth and what a buyer will actually pay often comes down to how thoroughly you address valuation factors explained in this post. Owners who strengthen their financial performance, market position, and operational foundation command higher multiples and attract more serious buyers-and we at Unbroker help you navigate this process with transparent guidance and access to qualified buyers.