Selling your business without a broker means you’re responsible for preparing all the sale documents yourself. Getting this right matters-missing or incorrect paperwork can kill a deal or expose you to legal liability.

We at Unbroker have seen firsthand how many DIY sellers stumble on documentation. This guide walks you through the exact legal documents you need, how to organize them, and the mistakes that could cost you.

What Legal Documents You Must Prepare for a DIY Sale

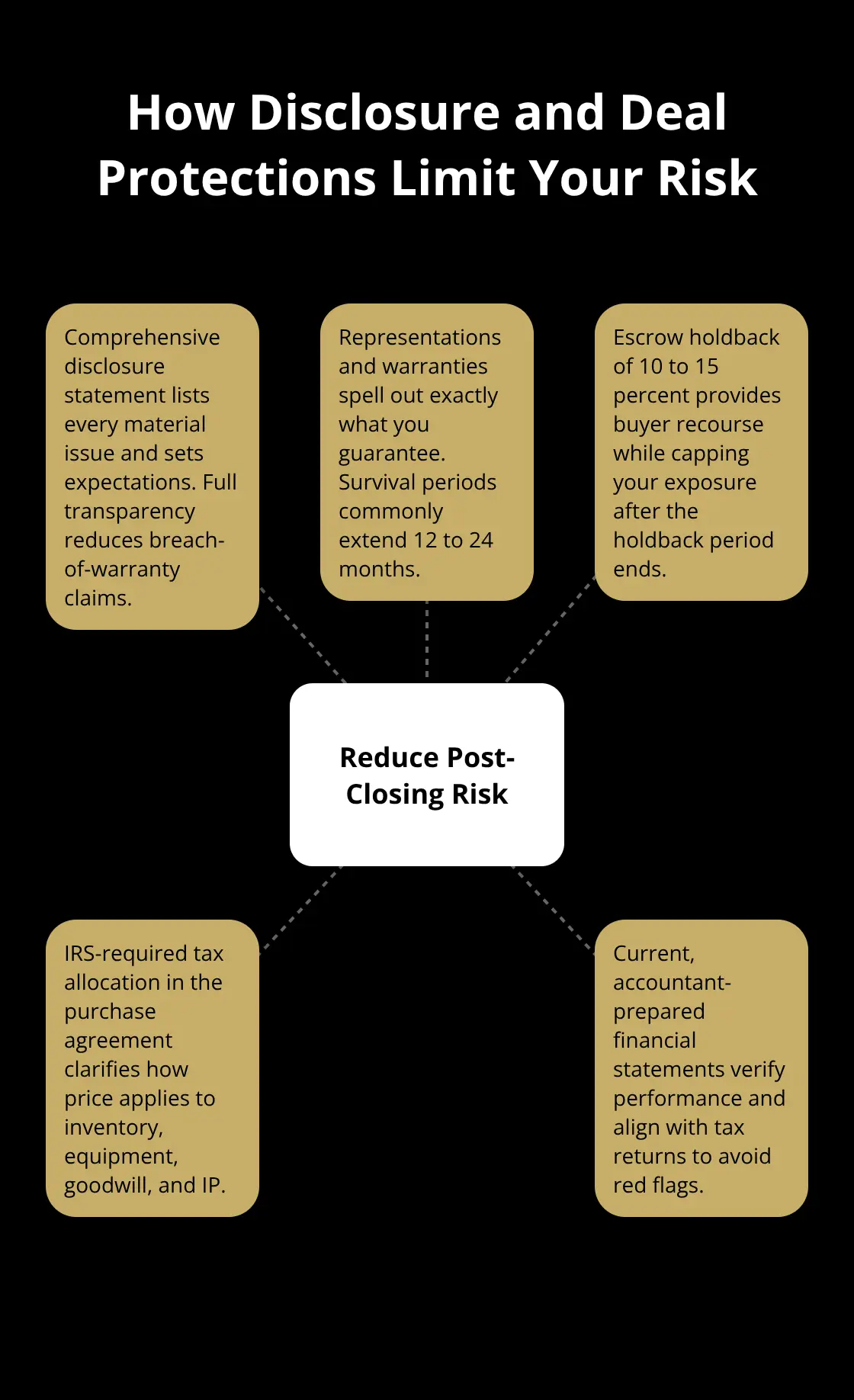

The purchase agreement forms your foundation, and it cannot be generic. This document must identify both parties with full legal names and addresses, specify the exact assets being transferred, and clearly state the purchase price and payment terms. The agreement must also include a tax allocation section that breaks down how the purchase price applies to different asset categories-this matters because the IRS requires it and gets specific about how you categorize inventory, equipment, goodwill, and intellectual property. Without proper allocation, you risk audits or disputes years after closing. Many DIY sellers use templates they find online, but those templates often miss critical details specific to your business type. If you sell a service business versus a product business, the asset mix looks completely different, and your agreement needs to reflect that reality.

Financial statements reveal what buyers actually need to see

You need financial statements for business sale including balance sheets, bank statements, tax returns, and cash flow statements. Buyers want to see revenue trends, profitability patterns, and whether your business actually generates the cash you claim. The SBA emphasizes that financial statements should be current and verified-ideally prepared by an accountant rather than cobbled together from QuickBooks exports. Tax returns matter equally because they verify legitimacy and show what you actually reported to the IRS, not what you wish you’d reported. Many sellers get tripped up here because their books don’t match their tax returns, which immediately raises red flags for buyers. If you’ve run cash deals or had off-the-books income, now is the time to reconcile those discrepancies or disclose them clearly. Buyers will uncover inconsistencies during due diligence anyway, and transparency here prevents deal collapse later. One practical step: have your accountant prepare a detailed reconciliation document that explains any gaps between your accounting records and tax filings.

Disclosure documents protect you from post-closing liability

Your disclosure statement must list every material fact that could influence a buyer’s decision-outstanding lawsuits, contract disputes, customer concentration issues, equipment needing replacement, lease renewal challenges, or regulatory compliance issues. Material means anything that would change the buyer’s valuation or decision to purchase. Many sellers think they can downplay problems or hope the buyer doesn’t notice, but that strategy backfires. If you fail to disclose and the buyer discovers issues after closing, they can sue for breach of representations and warranties, and those lawsuits happen years later when you’ve already spent the money. The legal standard for what constitutes disclosure is broad, so err on the side of over-disclosure.

If you’re uncertain whether something qualifies as material, include it. Your representations and warranties section should specify exactly what you’re guaranteeing about the business-that you own the assets free and clear, that contracts are valid and transferable, that there are no hidden liabilities, and that financial statements are accurate. These guarantees typically survive closing for 12 to 24 months, meaning the buyer can still sue if they find problems within that window. Structure your deal to include an escrow holdback of 10 to 15 percent of the purchase price, held by a neutral third party for that period. This gives the buyer recourse if they discover undisclosed issues and protects you from frivolous claims once the holdback period expires.

What comes next in your documentation process

With your core legal documents in place, you now face the practical challenge of organizing everything in a way that buyers can actually review. The next section walks you through how to conduct a thorough document audit, identify gaps before they become problems, and create a centralized repository that speeds up due diligence.

How to Organize Your Documents Before Buyers Start Asking Questions

Now that you understand what documents you need, the real work begins: getting them into shape and organizing them so buyers can actually review them without drowning in chaos. Most DIY sellers treat document organization as an afterthought, but this step determines whether your sale moves forward smoothly or stalls while buyers wait for scattered files.

Conduct a thorough document audit

Start by auditing everything you currently have. Go through your filing system, accounting software, email archives, and physical files to identify what exists and what’s missing. Create a checklist against the core documents we outlined: purchase agreement, financial statements for the past three to five years, tax returns, disclosure documents, employment contracts, client and supplier agreements, lease documents, intellectual property registrations, and any litigation records.

For each document, note whether you have it, whether it’s current, and whether it needs updating. This audit typically takes two to three weeks if you do it carefully, but rushing through it creates blind spots that emerge during due diligence. Many DIY sellers discover missing contracts or outdated agreements only when a buyer asks for them, which kills momentum and raises questions about what else you’re hiding.

Fix gaps before showing documents to buyers

Once you’ve identified gaps, decide what you can fix yourself and what requires professional help. If your financial statements are incomplete or your accounting records don’t match your tax returns, hire an accountant to reconcile them before showing anything to buyers. If you’re missing client contracts or have verbal agreements that were never documented, work with a lawyer to create written confirmations or amendment letters that clarify the terms.

These fixes take time but cost far less than losing a deal because documents don’t support your claims. You want buyers to see a business that operates with clear documentation and transparent record-keeping, not one that scrambles to explain missing paperwork.

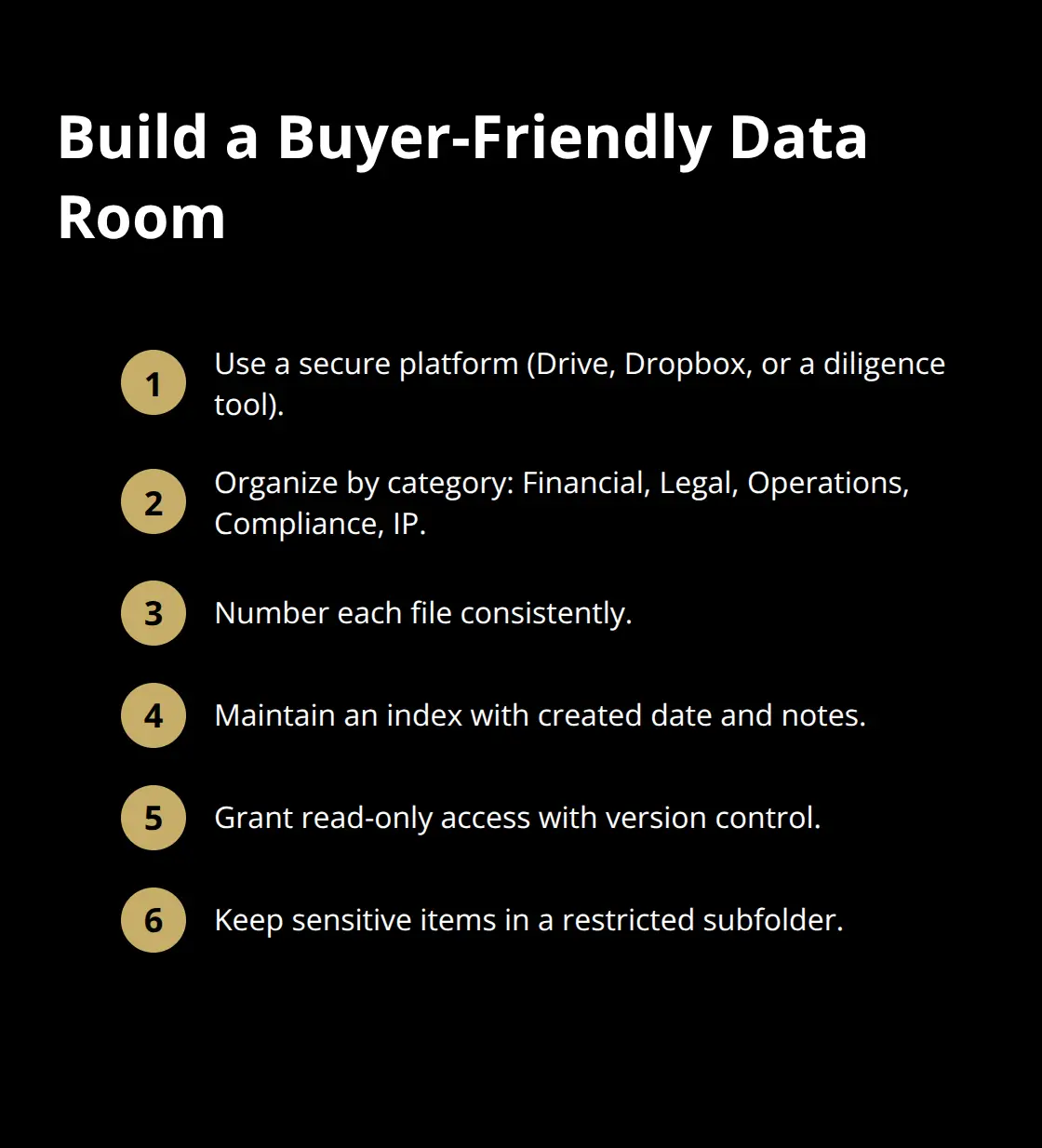

Organize documents in a centralized repository

Create a centralized document repository, either as a secure virtual data room using Google Drive, Dropbox, or a dedicated due diligence platform, organized into clear categories: Financial Documents, Legal Agreements, Operational Materials, Compliance Records, and Intellectual Property. Number each document and create an index that lists what’s included, when it was created, and any relevant notes.

This structure allows buyers to navigate your materials efficiently without asking you to hunt for things repeatedly. The goal is to present yourself as organized and transparent, which directly influences how buyers perceive business quality.

Have a lawyer review your complete package

Finally, have a lawyer review your complete documentation package before you share it with any potential buyer. They’ll spot missing provisions in contracts, identify disclosure gaps, flag outdated agreements that need renewal, and ensure your representations and warranties language actually protects you. This review typically costs $1,500 to $3,000 but prevents costly mistakes.

A lawyer can also ensure your asset allocation in the purchase agreement aligns with how your accountant structured your financial records, eliminating inconsistencies that trigger buyer scrutiny. With your documents organized and vetted, you’re ready to move into the next critical phase: identifying and avoiding the common mistakes that derail DIY sales.

What Kills DIY Sales: Three Document Mistakes You Cannot Afford to Make

Incomplete financial records destroy buyer confidence instantly

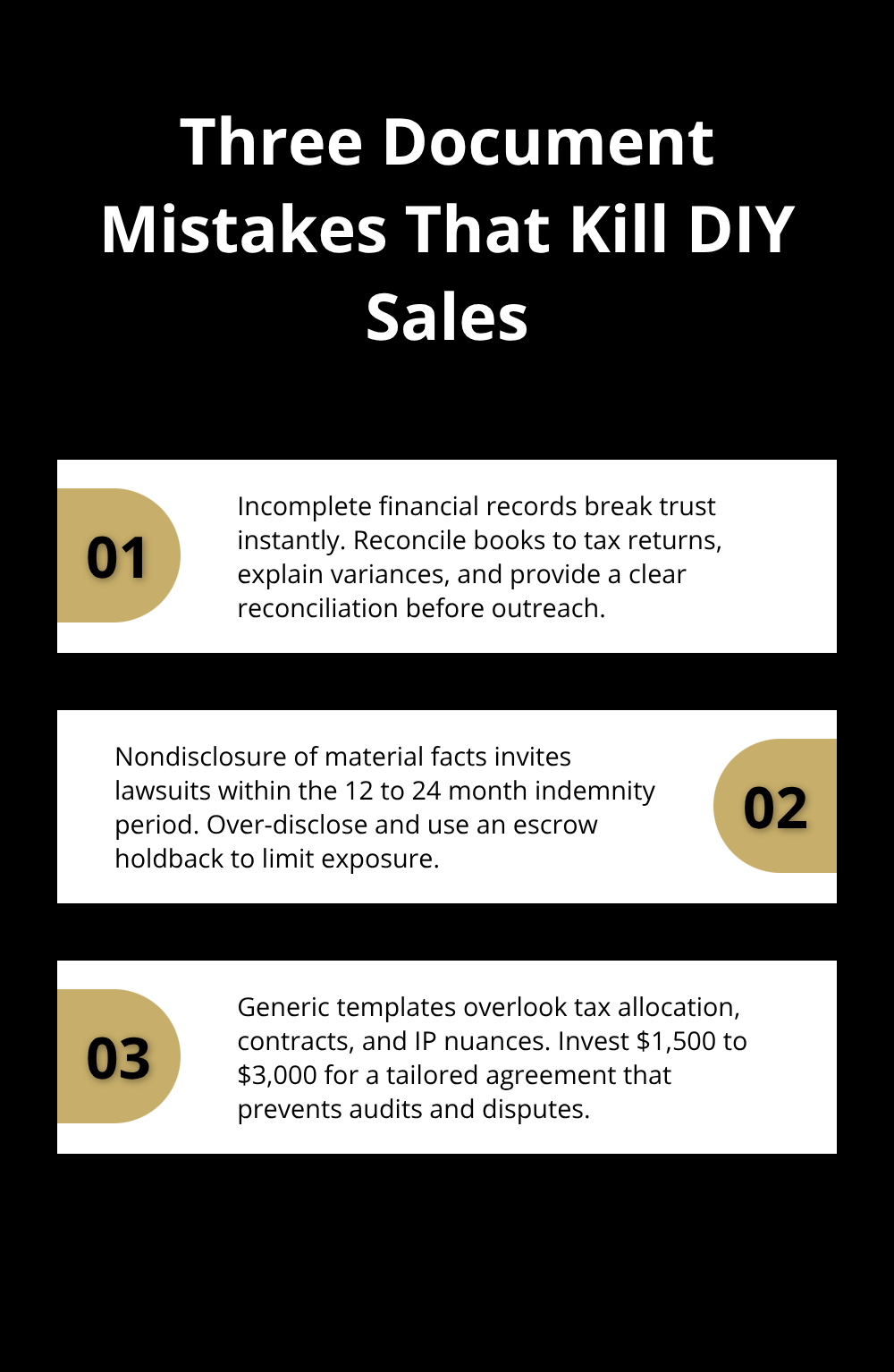

Incomplete financial records are the number one reason DIY sales collapse before closing. Your QuickBooks data tells only part of the story. Buyers demand bank statements, invoices, receipts, and tax returns to ensure they match. If your accounting software shows $500,000 in revenue but your bank deposits only show $450,000, that gap destroys credibility instantly. Most buyers hire a CPA or accountant to help them perform financial due diligence. Reconcile your books to your tax returns at least three months before approaching buyers. If you reported $400,000 in revenue on your 2023 tax return but your current books show $500,000, that discrepancy needs explanation before any buyer sees it. Create a detailed reconciliation document that explains timing differences, one-time adjustments, or accounting method changes.

Buyers will assume the worst if you cannot explain the gap.

Missing customer contracts or supplier agreements also tank deals because buyers cannot assess business continuity. If 40 percent of your revenue comes from three customers with only verbal agreements, that creates massive risk. Document those relationships now, even if it means creating a written confirmation letter with your customers stating terms and renewal expectations. Do not wait until a buyer asks for contracts you do not have.

Nondisclosure of material facts exposes you to years of legal liability

Material facts are anything that affects valuation or the buyer’s decision to purchase, and courts define that broadly. Outstanding lawsuits, pending lease renewals, equipment requiring replacement within 12 months, customer concentration risk where one client represents over 20 percent of revenue, or regulatory compliance issues all qualify as material. Many sellers rationalize that a buyer will discover these issues anyway, so why mention them early. That logic is backwards. If you disclose upfront, you control the narrative and can explain context. If a buyer discovers undisclosed issues after closing, they file a breach of warranty claim within the 12 to 24 month indemnity period, and now you defend yourself in litigation years after you thought the deal was done. Courts have awarded damages exceeding the purchase price when sellers concealed material facts.

Create a comprehensive disclosure document that lists every potential issue, then have your lawyer review it. If you are uncertain whether something qualifies as material, include it. Over-disclosure protects you far more than under-disclosure. Structure your deal with a 10 to 15 percent escrow holdback. This gives the buyer recourse for discovered issues and provides you a clear cutoff date when liability ends.

Generic templates fail to protect your specific business situation

Generic templates do not reflect your actual business. A template designed for a retail store will not work for a service business, and neither will handle your specific customer contracts, lease arrangements, or intellectual property correctly. The tax allocation section matters enormously here. If you sell equipment worth $100,000 and goodwill worth $400,000, the IRS requires this breakdown in your agreement. A generic template often omits this entirely or uses vague language that invites IRS scrutiny.

Spend $1,500 to $3,000 having a lawyer customize your purchase agreement to your specific situation. That investment prevents audits, disputes, and deal delays that cost far more. A lawyer will also ensure your representations and warranties section actually protects you by including proper carve-outs and survival periods. Without these protections, you could face claims years after closing for issues that existed before you sold.

Final Thoughts

Your sale documents form the backbone of a successful DIY business sale, and getting them right protects you from post-closing liability while establishing credibility with potential buyers. Audit what you currently have, identify gaps, and fix them before you approach any buyer-reconcile your financial records, document all customer and supplier relationships, and create a comprehensive disclosure statement. Have a lawyer review your complete package before you share anything with prospects, as this upfront investment prevents far costlier problems later.

We at Unbroker understand that handling a business sale alone feels overwhelming, which is why we offer an Assisted Business Sale service at $99 per month for DIY sellers who want expert guidance on documentation, negotiation, and legal templates. Our Full Service Business Sale option works for sellers who prefer hands-off selling, and both services include access to legal document templates, negotiation assistance, and a network of qualified buyers. Visit Unbroker to explore how we can support your sale while keeping costs transparent and fees low.

The businesses that sell successfully are the ones where sellers prepare thoroughly and stay organized throughout the process. You now have the roadmap to handle your sale documents with confidence and move forward without unnecessary delays or legal complications.