You’ve probably heard that business valuations depend on multiples. But here’s what most owners don’t realize: your valuation multiple can be significantly lower than industry benchmarks, and you might not know why.

At Unbroker, we’ve seen countless business owners shocked by their valuation numbers. The gap between what they expected and what buyers actually offer often comes down to specific, fixable issues.

What Moves Your Valuation Multiple Up or Down

The EV/EBITDA Framework

Your business multiple isn’t arbitrary. It’s shaped by concrete factors that buyers assess before making an offer. The enterprise value to EBITDA ratio, or EV/EBITDA, sits at the heart of most valuations. This metric captures what an acquirer would actually pay by accounting for your debt and cash position, not just your raw earnings. Dollar General, according to its SEC filings, had trailing EBITDA of 3 billion dollars, cash of 345 million, and debt of 14.25 billion-landing an EV/EBITDA around 18.2. That same company’s multiple shifts if debt changes or cash moves, even when EBITDA stays flat. This volatility matters because it shows that your multiple isn’t locked in; operational and financial decisions directly influence it. Buyers use this ratio because it levels the playing field across industries and regions, stripping away tax and capital structure noise that would otherwise distort comparisons.

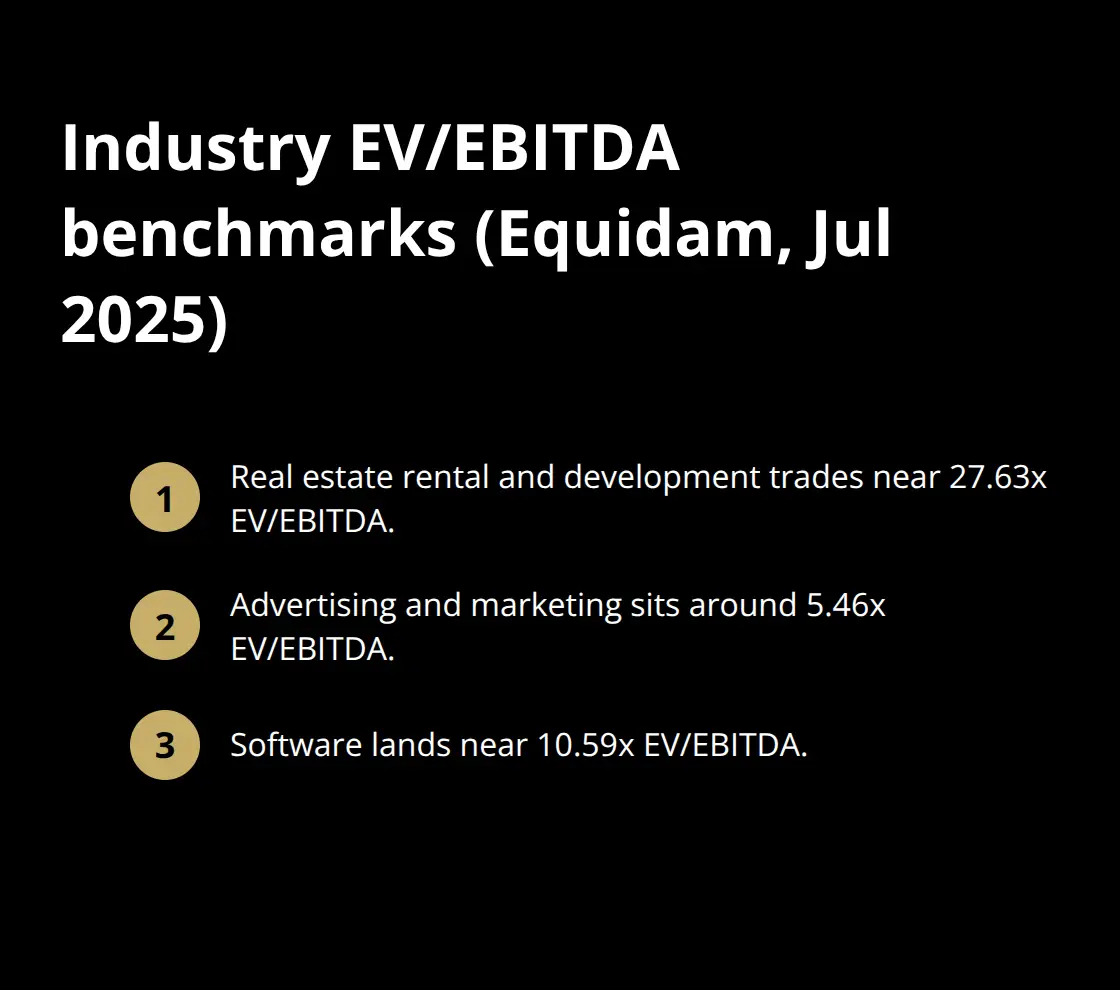

Industry Benchmarks Set Your Ceiling

Industry benchmarks set the ceiling for what you can realistically achieve. Real estate rental and development commands multiples near 27.63 according to analysis of over 30,000 public companies by Equidam as of July 2025, while advertising and marketing sits around 5.46. Software lands near 10.59.

These gaps exist because different sectors carry different risk profiles and growth trajectories. A real estate firm with long-term, cash-generating assets attracts premium valuations; a marketing agency faces tighter multiples due to client volatility and service-based revenue exposure. Your industry sets expectations, but your specific execution determines whether you land at the low end, middle, or top of that range.

What Buyers Actually Hunt For

Most buyers lean on adjusted EBITDA multiples when pricing acquisitions. They hunt for proof that your business sustains and grows profits without you, that your customer base won’t evaporate post-sale, and that your financial records actually reflect reality. A buyer won’t pay a premium multiple for a business that looks profitable only because the owner skipped taking a salary or buried personal expenses in the P&L. Clean financials, documented processes, and diversified revenue streams push your multiple upward. Weak management depth, customer concentration risk, or inconsistent growth projections pull it down hard. The specific issues that tank your valuation-inconsistent records, owner dependence, concentrated customers, outdated systems-are all fixable before you sell.

Why Your Multiple Tanks When Buyers Look Closer

Messy Financials Kill Valuations Fast

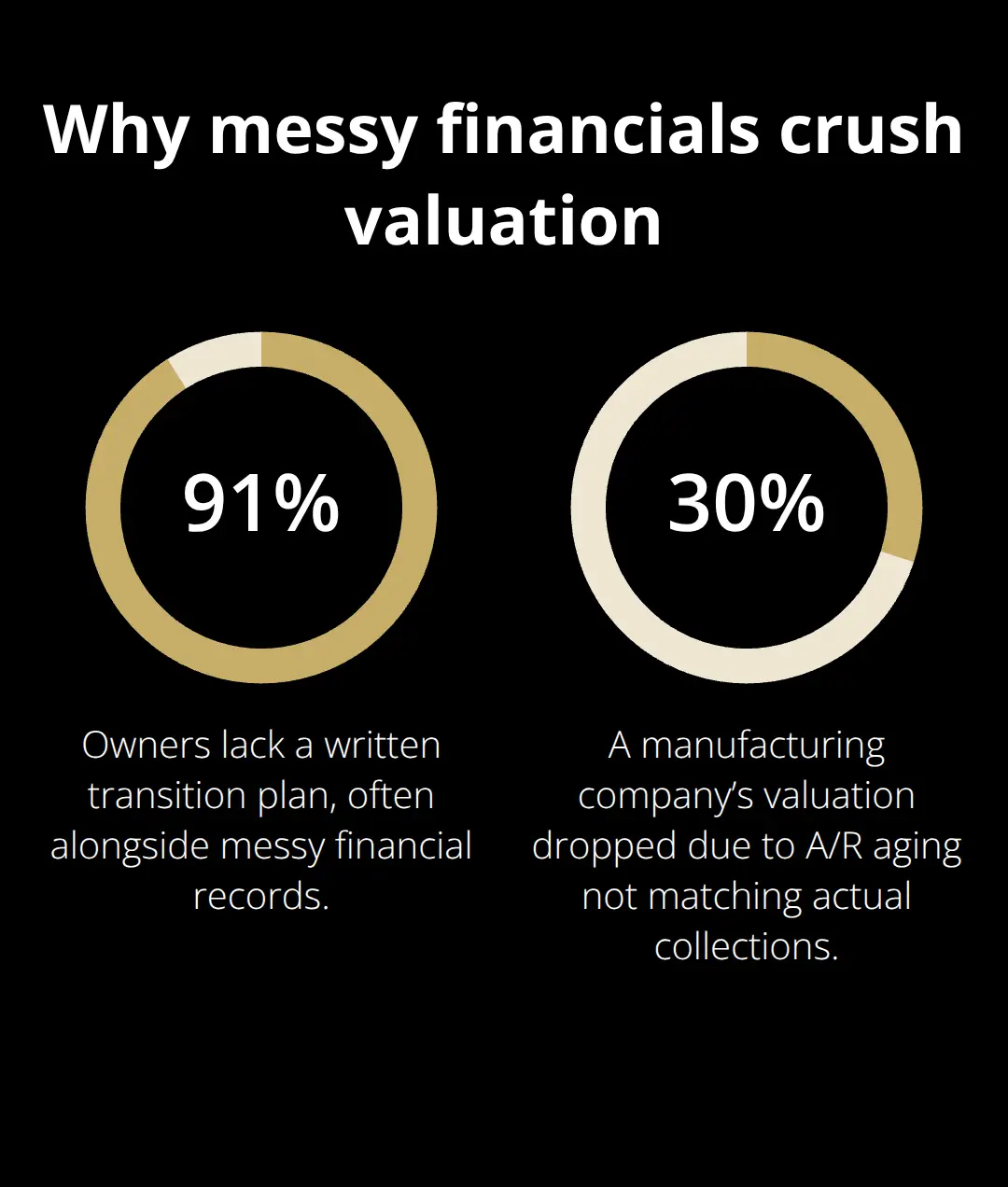

Messy financials are the silent killer of business valuations. When a buyer requests three years of clean income statements and balance sheets, and you hand over a folder of bank statements, expense receipts, and a spreadsheet you’ve been tinkering with for years, your multiple starts dropping immediately. The Exit Planning Institute found that 91% of business owners lack a written transition plan, and many haven’t cleaned up their financial records either. Buyers assume hidden problems when documentation is scattered.

Personal expenses buried in business accounts, inventory counts that don’t match physical stock, or missing sales records make a buyer nervous. That nervousness translates directly into a lower offer.

One manufacturing company had trailing twelve-month EBITDA around $2.5 million but saw its valuation hammered by 30% because accounts receivable aging reports didn’t align with actual collections. The buyer factored in extra risk and paid less. Get your financial statements audited or reviewed by a qualified accountant before you sell. Reconcile your balance sheet accounts monthly. Document every adjustment or non-recurring expense so buyers understand your true operating earnings. When your books are clean, buyers pay attention to your business fundamentals instead of hunting for red flags.

Flat or Declining Revenue Signals Weakness

Revenue that flatlines or declines signals weakness that multiples cannot hide. A business growing 5% annually in a sector where peers average 12% will trade at a significant discount. Declining revenue in a stable industry raises immediate questions about competitive position and market share loss. The Exit Planning Institute reports that consistent historic and projected growth commands premium multiples, while one-off revenue spikes get ignored or discounted heavily.

Recurring revenue growth matters far more than one-off contracts. A software company with $500,000 in annual recurring revenue growing 15% year-over-year attracts buyers willing to pay 10 to 12 times EBITDA. The same company with $500,000 in revenue that jumped 40% last year due to one project, then fell back to 5% growth, trades at 6 to 8 times EBITDA instead.

Owner Dependence Erodes Value Rapidly

Owner dependence erodes multiple faster than almost anything else. When the business cannot function without you, buyers see a job for hire, not an asset they can own. If you are the top salesperson, the operations manager, and the technical expert keeping clients happy, a buyer inherits massive risk post-acquisition. They’ll demand a lower multiple or tie part of the payment to your continued involvement under an earn-out. Build systems and hire managers who can run things without you now, not after you sell.

Customer Concentration Creates Valuation Drag

A concentrated customer base-where one client represents more than 10% of revenue or your top three customers exceed 50% of sales-creates valuation drag that’s hard to overcome. Buyers know that losing one or two customers tanks your cash flow. They price that risk into their offer by reducing the multiple they’ll pay. Expand your customer base deliberately. Try to diversify before you approach buyers.

Outdated Systems Scare Away Modern Buyers

Outdated systems and technology scare away modern buyers. If your operations run on spreadsheets, your inventory system is a filing cabinet, or your customer data lives in disconnected databases, a buyer assumes integration costs and operational inefficiency. Modern infrastructure, cloud-based systems, and documented processes add perceived value and justify a higher multiple. These operational improvements position your business as acquisition-ready and signal that you’ve invested in scalability. When you address these five issues-messy records, weak growth, owner dependence, customer concentration, and outdated technology-you move from a discount valuation to one that reflects your business’s true potential.

How to Fix Your Valuation Before Buyers Come Calling

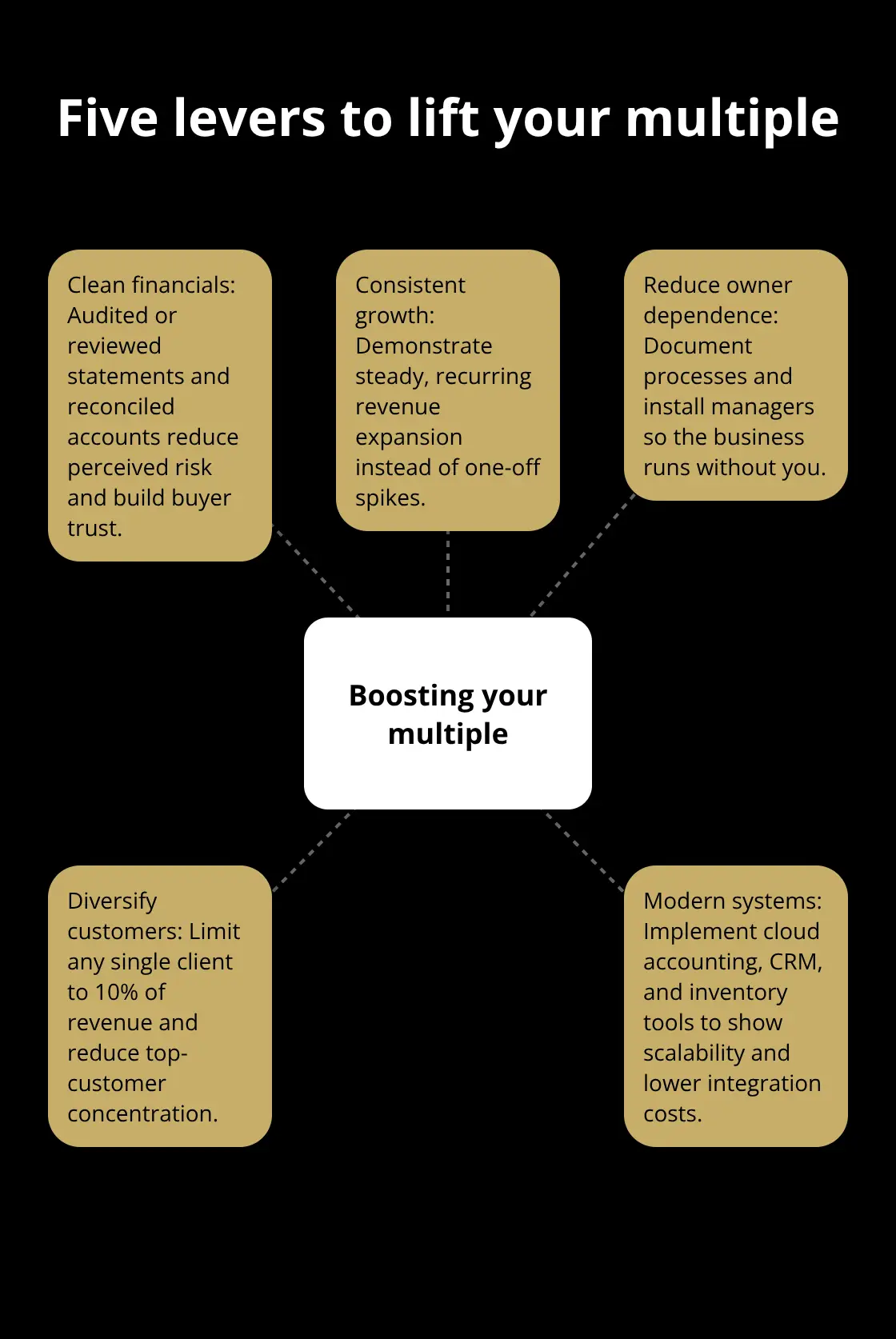

Start with your financial records because nothing else matters if your books don’t tell a credible story. Hire a qualified accountant to audit or review your last three years of statements, then reconcile every balance sheet account monthly going forward. This means matching accounts receivable aging reports to actual collections, ensuring inventory counts align with physical stock, and removing every personal expense from your business accounts. Clean financial records with audited or reviewed statements enhance valuation and build buyer confidence. Document every non-recurring expense separately so your true operating earnings become obvious. When your financials are clean, buyers focus on your business fundamentals instead of hunting for red flags.

Demonstrate Consistent Revenue Growth

Revenue growth matters more than you think because one-off spikes don’t move the needle. A business growing 15% annually in a sector where peers average 8% commands a meaningful multiple premium. Recurring revenue growth matters far more than project-based wins that vanish after completion. A software company with $500,000 in annual recurring revenue trades at higher multiples than the same company with volatile revenue. Focus on building predictable, subscription-based revenue streams before you sell. If you’re service-based, convert one-time clients into annual retainers. If you sell products, develop a maintenance or subscription component. Buyers pay premiums for predictable cash flows because those reduce their acquisition risk.

Build Systems That Function Without You

Owner dependence tanks valuations faster than almost anything else. When the business cannot function without you, buyers see a job for hire, not an asset they can own. Hire managers for sales, operations, and technical functions, then document every critical process in writing. Create an organizational chart showing who runs what, establish non-compete and confidentiality agreements with key employees, and implement succession plans for critical roles. Reducing owner dependence boosts your company’s value and improves buyer confidence. If they see a one-person show, they either walk away or demand a significant discount and tie payment to your earn-out.

Diversify Your Customer Base

A concentrated customer base-where one client represents more than 10% of revenue or your top three customers exceed 50% of sales-creates valuation drag that’s hard to overcome. Buyers know that losing one or two customers tanks your cash flow. They price that risk into their offer by reducing the multiple they’ll pay. Expand your customer base deliberately. Try to cap any single customer at no more than 10% of revenue and ensure your top three customers don’t exceed 50% of total sales. This requires deliberate action: launch new products, enter adjacent markets, or hire business development staff focused specifically on new customer acquisition. Concentrated revenue is a major valuation killer, so treat customer diversification as a core business priority, not a nice-to-have.

Invest in Modern Technology and Infrastructure

Outdated technology signals operational inefficiency to buyers. Replace spreadsheet-based inventory management with proper software, migrate customer data into a centralized CRM, and move financial records to cloud accounting platforms. These upgrades cost money upfront but justify higher multiples by demonstrating scalability and reducing integration costs for the buyer.

A business running on modern systems closes faster and at better terms because buyers see an acquisition-ready operation rather than a legacy mess requiring expensive overhauls. Start these improvements 12 to 24 months before you plan to sell because buyers can tell the difference between infrastructure installed yesterday and systems that have been running smoothly for years.

Final Thoughts

Your valuation multiple depends on factors you control. Clean financial records, consistent revenue growth, systems that operate without you, a diversified customer base, and modern technology all push your multiple upward. Messy books, flat revenue, owner dependence, concentrated customers, and outdated systems pull it down.

Start now, not when you approach the market. Cleaning up your financials takes time, and building management depth takes longer. Diversifying your customer base requires deliberate effort over months, while upgrading your technology infrastructure needs 12 to 24 months to prove stability to buyers-the owners who command premium valuations started these improvements years in advance.

We at Unbroker help business owners sell at fair valuations without the traditional brokerage fees that eat into your proceeds. Our platform connects you with qualified buyers while providing the tools, templates, and guidance you need to strengthen your position before negotiating, and whether you choose hands-off selling or want expert support while maintaining control, we eliminate the guesswork and keep more money in your pocket. Visit Unbroker to explore your options and see how transparent, low-cost selling works.