Most business owners get their valuation wrong. We at Unbroker see it constantly-sellers either price themselves out of deals or leave money on the table because they didn’t validate their numbers properly.

The difference between an accurate valuation and a guessed one can cost you hundreds of thousands of dollars. These valuation accuracy tips will show you exactly which metrics matter and which mistakes to avoid before you sell.

What Happens When Your Valuation Is Wrong

Overpricing Kills Deals Fast

Overpricing your business stops deals before they start. When a seller’s asking price disconnects from market reality, serious buyers walk away immediately. The Exit Planning Institute found that 49% of business owners plan to exit within five years, which means competition for buyer attention is real. If your valuation sits above what comparable recent sales support, you waste months on tire-kickers while your best opportunities disappear.

Buyers talk to each other, and a business that sits overpriced for six months gets labeled as stale inventory. That reputation sticks, and when you finally adjust the price, new buyers assume something is broken underneath.

The cost runs deeper than just a lower final price. You lose months of time, face management distraction from running your company, and watch buyer confidence erode. Professional appraisers with ABV credentials through the AICPA typically charge $5,000 to $20,000 to prevent exactly this mistake, and that investment pays for itself many times over if it stops a failed listing.

Underpricing Costs You Hundreds of Thousands

Underpricing hurts differently but cuts deeper into your wallet. A business undervalued by just 10% on a $5 million sale costs you $500,000 in lost proceeds-money that should fund your retirement or next venture. Many sellers rely on rough revenue multiples without normalizing their earnings or understanding what drives value in their specific industry.

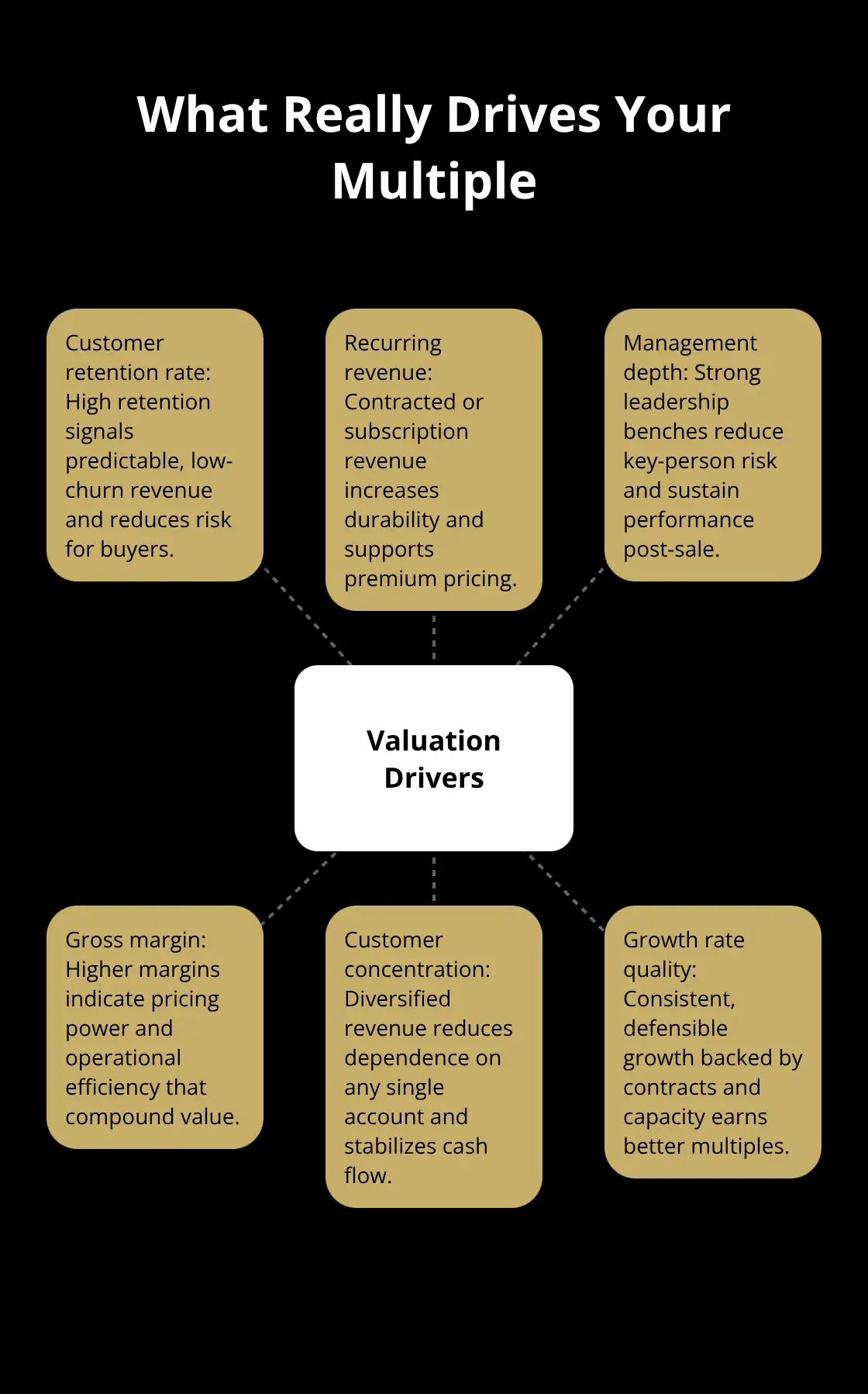

Customer retention rate, recurring revenue, and management depth matter far more to buyers than raw sales numbers, yet most sellers don’t measure these properly before going to market. When you enter negotiations with soft numbers instead of data-driven support, buyers anchor their offers low because they sense uncertainty.

Normalized EBITDA Reveals Your True Value

Normalized EBITDA calculation removes owner compensation, one-time expenses to reveal the true cash machine your business represents-and that number is what serious buyers pay for. The difference between guessing and validating your metrics typically shows up in the first offer: validated numbers attract bids within 5-15% of asking price, while unvalidated numbers trigger lowball offers 20-30% below your initial ask. That gap compounds when buyers sense they can negotiate you down further.

This is why understanding which specific metrics drive value in your industry-and how to measure them accurately-separates sellers who walk away satisfied from those who leave money on the table.

Which Metrics Actually Drive Your Sale Price

When business owners ask what their company is worth, the answer often comes back in the form of a multiple: “5x EBITDA,” “7x earnings,” or “1x revenue.” But these multiples sit at the surface of valuation and are blunt tools that miss what serious buyers really pay attention to. The multiple your business commands depends entirely on how predictable and durable your cash flows look, which means the raw multiple matters far less than what sits underneath it. A software company with $2 million in recurring annual revenue might sell for 8 times EBITDA, while a service business with identical EBITDA but lumpy, one-off contracts sells for 3 times. The difference isn’t the size of the business-it’s the stability buyers perceive.

Revenue Multiples Hide the Real Story

Revenue multiples alone tell you almost nothing. A $10 million revenue business could be worth $15 million or $3 million depending on gross margin, customer concentration, and growth rate. Buyers in your industry know this, which is why they immediately ask about customer retention rate, churn, and lifetime value. If you can’t answer these questions with real numbers, you’ve already lost negotiating power.

When you walk into negotiations, you need to know which metrics your industry values most and have concrete data to support each one.

Customer Retention and Lifetime Value Command Premium Prices

Customer retention rate above 90 percent signals that your revenue is sticky and predictable-this alone can justify a premium multiple. Lifetime value matters because it shows how much profit each customer generates over time. A customer acquired for $5,000 who stays five years and generates $50,000 in total margin is worth far more to a buyer than one who stays one year.

Calculate your lifetime value by taking average customer revenue, multiplying by gross margin, and then multiplying by average customer lifespan in years. If your retention rate is weak or your lifetime value falls below industry benchmarks, that becomes a drag on your valuation that no amount of revenue growth can offset.

Growth Trajectory Needs Real Support

Growth trajectory matters, but only when contracts, capacity, and historical performance support it. Buyers ignore projections that exceed your historical growth rate without clear justification. If you’ve grown 15 percent annually for five years but suddenly project 40 percent growth in your forecast, expect buyers to discount that aggressively.

Market position determines whether you’re a commodity or a defensible business. Strong market position means you have pricing power, customer switching costs, or a reputation that makes you harder to replace. Weak market position means you compete mainly on price and lose customers easily to competitors.

Market Position Separates Defensible Businesses from Commodities

Document your market position with concrete evidence: customer testimonials, repeat business rates, or industry rankings if they exist. Without this foundation, your valuation rests on assumptions rather than facts, and assumptions are what kill deals. The metrics that matter most vary by industry, which is why your next step involves identifying which specific drivers apply to your business and then validating each one with hard data before you approach potential buyers.

Common Valuation Mistakes Sellers Make

Most sellers price their business by grabbing a multiple from an online article or asking a friend what they sold for. This approach fails because comparable sales data without context is worthless. A software business that sold for 6x EBITDA tells you nothing if it had $10 million in annual recurring revenue while yours has $2 million. Buyers know this gap, and they’ll use your vague comparable to anchor their offer low.

Finding Comparables That Actually Match Your Business

The real work involves finding comparables that actually match your business by identifying 5–15 recent transactions in your industry, within your size range, with similar growth and customer profiles. If you can’t find three to five legitimate comparable sales that match these criteria, stop relying on multiples altogether. Instead, work backward from what buyers in your space typically pay for specific metrics: customer acquisition cost, retention rate, gross margin.

A manufacturing business sold last year for 4.2x EBITDA but had 60% gross margin and a 95% customer retention rate. If your margins sit at 40% and retention at 80%, that 4.2x multiple doesn’t apply to you. This is where most sellers fail-they anchor to a number without understanding what conditions made that number possible. Spend time talking to industry peers, asking advisors what recent deals closed for, and documenting the specific characteristics that drove each sale price. Without this foundation, your valuation is guesswork dressed up as analysis.

Intangible Assets Require Documented Evidence

Sellers love to inflate their valuations by adding a premium for brand reputation, customer relationships, or proprietary processes. The problem is buyers don’t pay for intangible assets require documented evidence without documented evidence. Saying your brand is strong means nothing-showing that customers specifically chose you over competitors with documented testimonials, case studies, or retention data means everything.

Proprietary processes only matter if they create measurable competitive advantages: faster delivery, lower costs, or higher margins. If your process simply describes how you work but doesn’t produce results competitors can’t match, it adds zero value. You must prove that your intangible assets translate into real financial performance that buyers can verify.

One-Time Revenue and Expenses Distort True Earnings

One-time revenue spikes or unusual expenses distort your true earning power and tank your valuation if left unaddressed. A business that brought in a $500,000 contract from a major customer that won’t repeat looks like it grew 40% when normalized EBITDA adjustments remove one-time costs and discretionary spending to show only 10% growth. Buyers see the spike, assume it’s gone, and discount your valuation accordingly.

Document every adjustment you make to normalize earnings: owner compensation paid above or below market rates, personal expenses run through the business, one-time legal settlements, or a customer win that won’t repeat. List each adjustment with dollar amounts and clear justification. If you can’t defend an adjustment, remove it.

Buyers will spend weeks stress-testing your normalized numbers, and unsupported adjustments become red flags that kill deal momentum faster than almost anything else.

Final Thoughts

Accurate valuations attract serious offers within days because buyers recognize they’re looking at real numbers, not inflated projections. When you walk into negotiations with normalized EBITDA, documented customer retention rates, and comparable sales that actually match your business, you’ve already won half the battle. Buyers spend weeks validating your numbers anyway, so showing up with clean, defensible data means they spend that time confirming what you’ve already proven rather than hunting for hidden problems.

The valuation accuracy tips covered here work because they force you to think like a buyer. What would make you confident enough to write a check? What metrics would you demand to see? What adjustments would you question? Answer those questions before you sell, and you’ll negotiate from strength instead of desperation (this shift in perspective changes everything about how buyers perceive your business).

Start today by calculating your normalized EBITDA, pulling together your customer retention data, and identifying five comparable sales in your industry. If you need support navigating the sale process itself, Unbroker offers transparent options designed to eliminate high brokerage fees while giving you access to a vast buyer network and expert guidance. Your numbers are ready-validate them and move forward.