Selling a service business requires more than just finding a buyer. The value of your company depends on specific metrics that buyers evaluate closely, from revenue stability to team capabilities.

At Unbroker, we’ve helped service business owners understand what actually moves the needle when it comes to valuation. This guide walks through the drivers that increase your worth and the strategies that position you for a successful sale.

What Actually Drives Value in a Service Business

EBITDA multiples are the primary valuation driver for service businesses, and higher EBITDA directly expands the multiple buyers will pay. This means that increasing your earnings before interest, taxes, depreciation, and amortization matters far more than simply growing revenue. A service business generating $500,000 in revenue with $100,000 in EBITDA will command a significantly higher valuation than one with $600,000 in revenue but only $60,000 in EBITDA. Revenue growth without profit growth disappoints buyers because it signals operational inefficiency or unsustainable practices. You should focus ruthlessly: cut unnecessary overhead, eliminate low-margin work, and reinvest profits into high-return activities. Track your EBITDA margin (EBITDA divided by revenue) monthly, not annually. If your margin sits below 20 percent, you have a profitability problem that will tank your valuation regardless of top-line growth.

Recurring Revenue Transforms Your Valuation

Recurring revenue is the single most valuable asset in a service business because it reduces buyer risk and improves valuation multiples. Businesses with 50 percent or more recurring revenue command substantially higher EBITDA multiples than those dependent on one-off projects. Long-term contracts, retainer agreements, and subscription-based service models all count as recurring revenue. You should shift toward annual service agreements or monthly retainers immediately if you currently operate on a project-by-project basis. This shift takes time, but it’s worth the effort because buyers will pay significantly more for predictable cash flows. A business with $1 million in annual recurring revenue at 30 percent EBITDA margin will be valued much higher than a similar business with the same revenue but only 10 percent recurring. Document your contract lengths and renewal rates carefully because buyers will verify this data during due diligence.

Management Independence and Team Depth

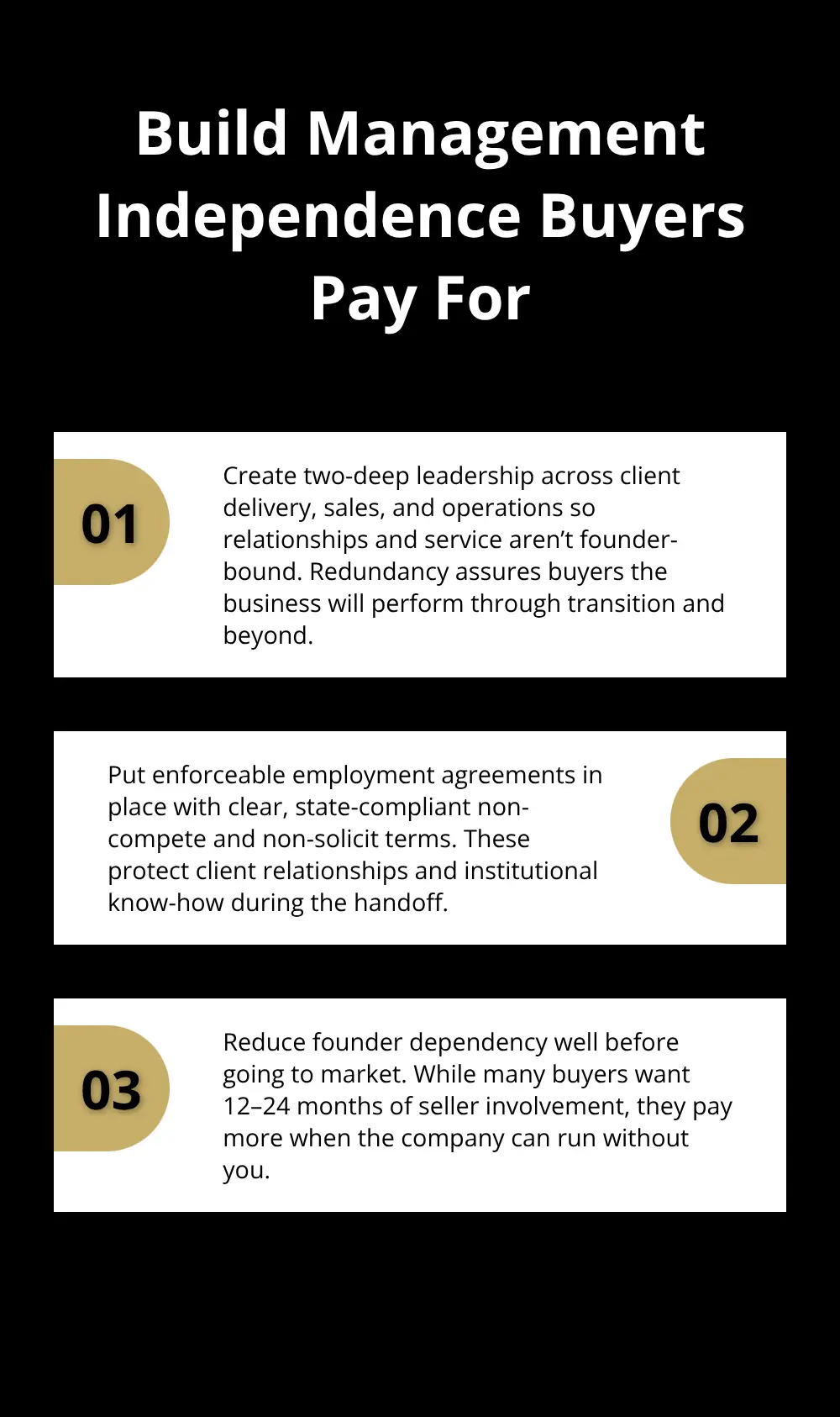

Buyers pay premiums for service businesses that don’t depend on the founder’s personal relationships or expertise. If your clients work with you because of your personal reputation, your valuation will suffer. You must build a management structure where key team members can own client relationships and deliver services independently. At minimum, establish two-deep leadership in essential functions (client delivery, sales, and operations). This redundancy signals to buyers that the business will survive your transition out. Employment agreements with non-compete clauses protect value during the handoff. Make sure these agreements are legally enforceable, geographically limited, and time-bound.

Management independence reduces the risk that losing one person cripples operations. Buyers often expect sellers to remain involved for 12 to 24 months post-sale anyway, but they’ll pay more if your business doesn’t need you to function.

Client Concentration and Relationship Risk

Buyers view concentrated client bases as a major red flag because losing one or two clients can devastate cash flows. If your top three clients represent more than 40 percent of revenue, you face a valuation discount that reflects this risk. You need to actively work toward a more balanced client portfolio where no single client exceeds 15 percent of revenue. This diversification takes deliberate effort-it means saying no to oversized deals that create dependency and yes to smaller, stable accounts that build resilience. Clients with long-term contracts and high switching costs (those locked into your systems or processes) are worth more to buyers than transactional relationships. Document these switching costs and contract terms clearly because they directly support your valuation during negotiations.

Prepare Your Business for the Buyer’s Microscope

Buyers conduct rigorous due diligence before committing to a service business acquisition, and they focus intensely on three areas: how your operations actually run, whether your revenue depends on a handful of clients, and whether your financial records withstand scrutiny. Most service business owners underestimate how much work this preparation phase requires, but the effort translates directly into valuation. A business with clear, documented systems commands higher multiples than one where processes exist only in the owner’s head. Similarly, a client base spread across multiple accounts with no single customer exceeding a certain threshold looks dramatically less risky than one where a few clients generate the majority of income. Clean financials that match your tax returns and show consistent profitability eliminate buyer hesitation and accelerate negotiations. Start this preparation work 12 to 18 months before you plan to sell because rushing these steps signals weakness and costs you money.

Map Out Your Operations in Writing

Your systems documentation must answer a specific question: can someone unfamiliar with your business replicate your delivery and client relationships without you? Write out your service delivery process step-by-step, including timelines, quality checkpoints, and client communication protocols. Capture your sales process, pricing methodology, and how you qualify prospects. Map out your financial close process, including how long it takes to invoice, collect payments, and reconcile accounts. List the software tools you use alongside the critical workflows they support. This documentation typically runs 20 to 40 pages and becomes invaluable during buyer onboarding post-sale. Buyers expect to see this level of operational clarity because it proves your business can function without you.

Reduce Client Concentration Over Time

Client diversification requires deliberate action over months or years. Reduce your reliance on any one customer so that your largest customer accounts for less than 15% of your revenue. Start by identifying which existing clients could expand their spending (upsells within current accounts) versus which new markets or service lines could attract fresh clients. Set a specific target and timeline for reducing concentration among your largest clients. This shift means turning away some large project opportunities that deepen dependency and accepting smaller, stable retainer clients instead. Track your client concentration monthly using a simple spreadsheet showing each client’s revenue contribution and contract renewal dates. Buyers will scrutinize this data during due diligence, so accuracy matters.

Establish Monthly Financial Close Cycles

Monthly financial reporting helps small businesses track cash flow, spot issues early, and make data-driven decisions. If your accounting currently happens once a year, switch to monthly close cycles immediately. Buyers will compare your financial statements to your tax returns, and discrepancies raise red flags that tank valuations. Normalize your financials by removing one-time expenses and personal costs run through the business, such as excessive owner compensation, vehicle expenses, or club memberships. These adjustments show what sustainable, transferable earnings actually look like. Store all client contracts in a centralized location and verify that non-compete agreements are in place for key team members.

Formalize Employment Agreements and Contracts

If you lack formal employment agreements, draft them now with legal counsel who specializes in your state’s requirements. Vague or unenforceable non-competes provide zero protection and signal to buyers that your team could walk out and start a competing firm. Documentation completeness matters more than perfection; buyers expect to find gaps, but a well-organized file structure demonstrates operational discipline and reduces their due diligence workload. The stronger your contractual foundation, the more confidence buyers place in your ability to retain key talent and client relationships through the transition.

What Your Service Business Is Actually Worth

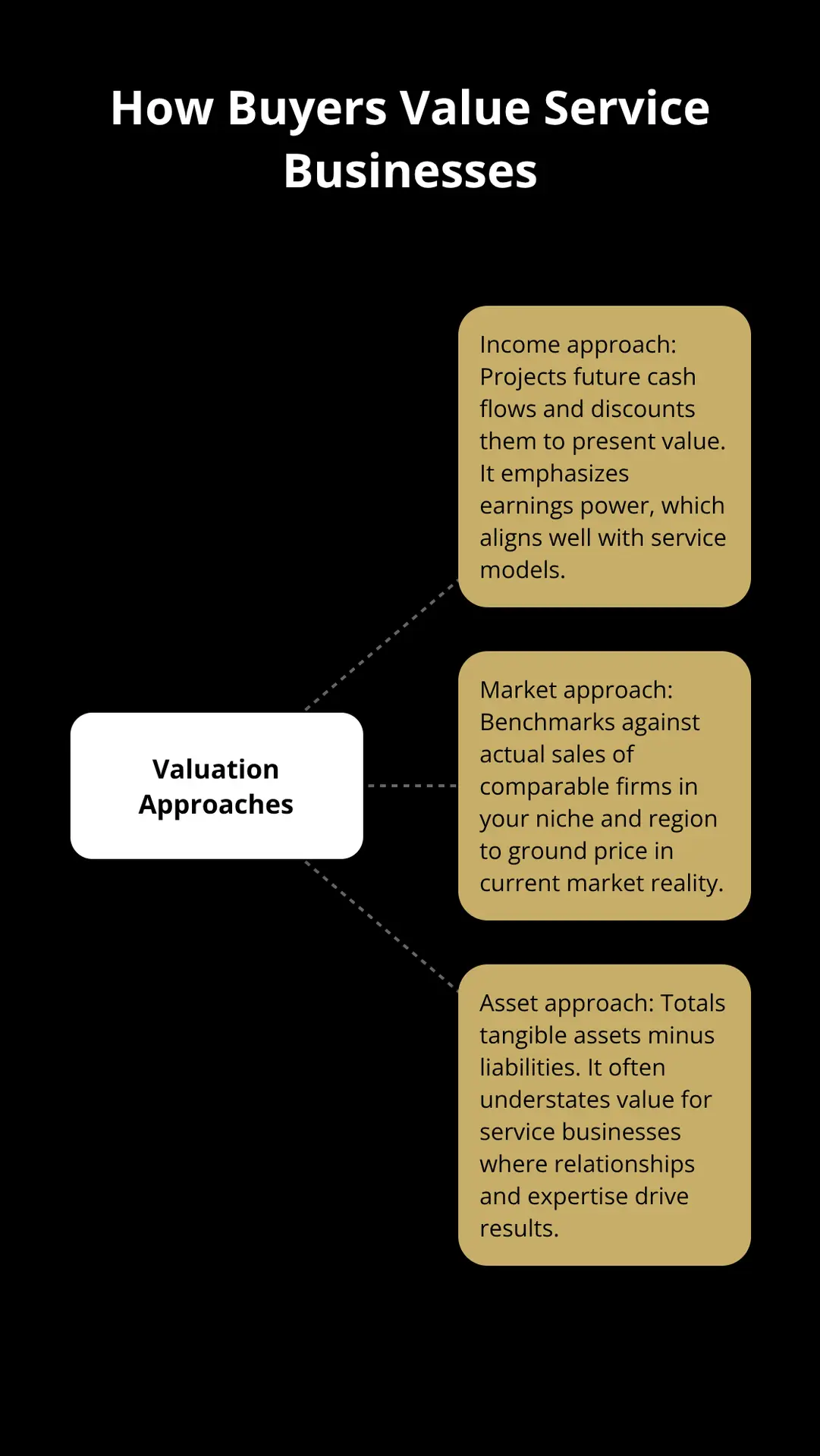

Most service business owners price their companies based on gut feeling or a conversation with one broker, then wonder why they leave money on the table during negotiations. Valuation requires understanding three distinct approaches that buyers use, and each one tells a different story about your business’s worth. The income approach projects your future cash flows and converts them into present value, which works well for service businesses because it focuses on earnings power rather than tangible assets. The market approach benchmarks your business against recent sales of comparable firms in your industry and region, though finding truly comparable transactions takes professional databases like DealStats or PitchBook that most owners don’t access. The asset approach totals your tangible assets (equipment, software licenses, client databases) minus liabilities, but this method typically undervalues service businesses because relationships and expertise matter far more than physical things. Most service business valuations rely heavily on the income approach because it directly answers what buyers care about: how much cash will this business generate for me after I take over?

EBITDA Multiples: The Core Valuation Driver

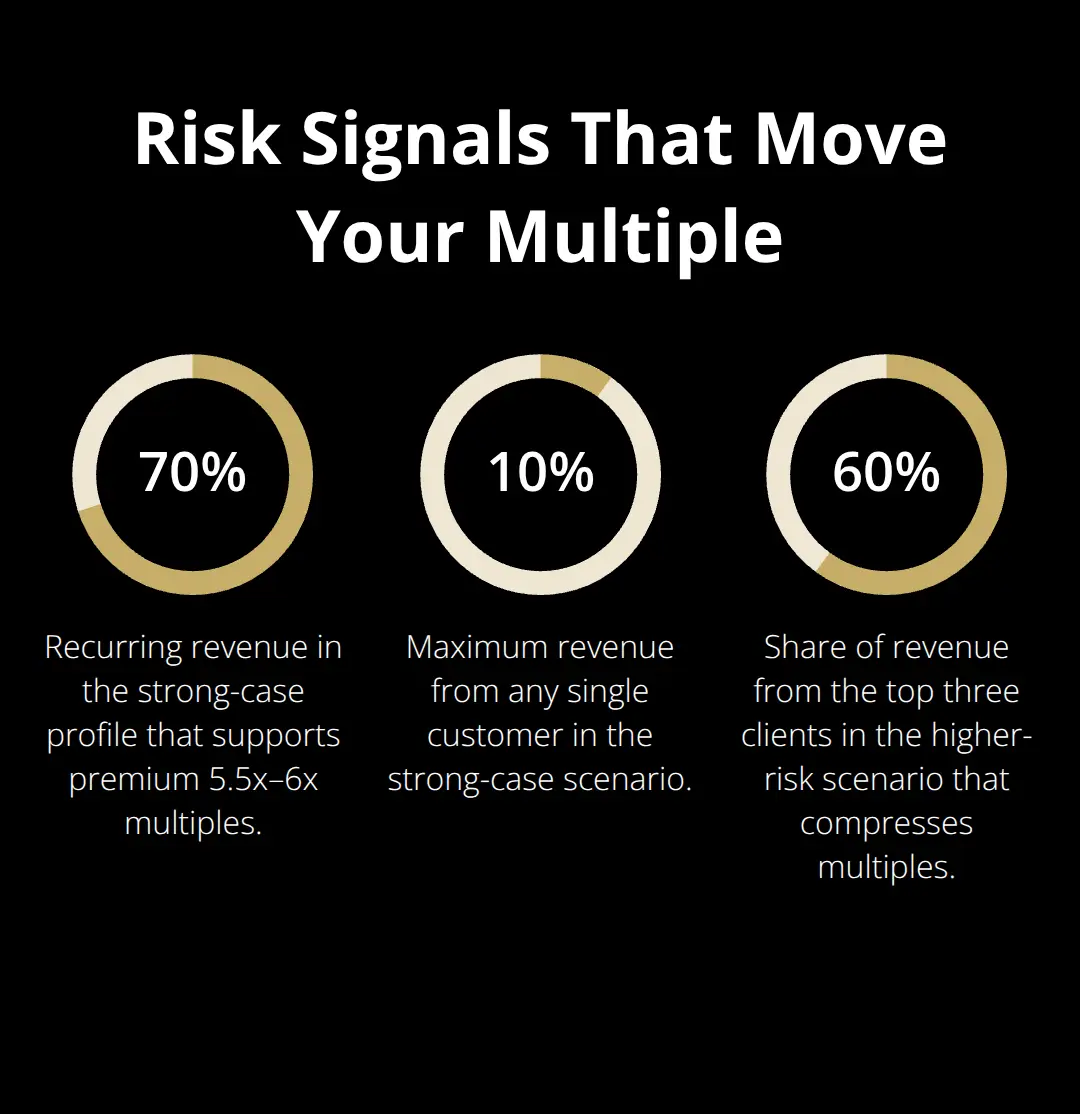

EBITDA multiples form the backbone of service business pricing, and understanding how multiples work prevents you from accepting lowball offers. A business generating $200,000 in EBITDA might sell for $800,000 to $1,200,000 depending on the multiple buyers assign, which typically ranges from 4x to 6x EBITDA for stable service businesses. The multiple depends directly on risk: lower risk equals higher multiples. A service business with 70 percent recurring revenue and diversified client base where no customer exceeds 10 percent of revenue, and a management team that functions without the founder commands a 5.5x to 6x multiple. The same business with 20 percent recurring revenue, three clients generating 60 percent of revenue, and heavy owner dependence might only fetch 3x to 4x EBITDA.

This difference represents hundreds of thousands of dollars.

To calculate your valuation range, multiply your normalized EBITDA by 4, 5, and 6 to see the low, mid, and high scenarios. Normalized EBITDA means you remove one-time costs, excessive owner compensation, and personal expenses run through the business to show what a new owner will actually earn. If you paid yourself $150,000 in salary but a replacement manager costs $80,000, you add back $70,000 to your EBITDA figure. Buyers will normalize your financials anyway during due diligence, so doing it yourself first demonstrates sophistication and accelerates negotiations.

Your EBITDA margin (EBITDA divided by revenue expressed as a percentage) also influences the multiple you receive. Service businesses with margins above 25 percent typically command premium multiples within their risk category because high margins signal operational excellence and pricing power. Margins below 15 percent raise questions about scalability and often result in multiple compression. If your margins sit below 20 percent, improving them before sale matters more than growing revenue because each percentage point improvement can add $50,000 to $100,000 in valuation for a $1 million revenue business.

Market Comparables Ground Your Price in Reality

Market comparables show what actual buyers paid for similar businesses recently. Professional appraisers search transaction databases for service businesses in your niche, region, and size range, then extract the multiples paid to derive a realistic range for your company. A plumbing service business in Denver selling for $1.2 million with $240,000 in EBITDA (5x multiple) provides a relevant data point if you run a similar plumbing business in the same market. The problem is that most owners never see these comparables because brokers treat valuation data as proprietary. This opacity works against you.

Request that any broker or appraiser show you the actual comparable transactions they used, including company size, revenue, EBITDA, multiple paid, and any adjustments made for differences. Comparables typically span the past 24 to 36 months because older deals reflect different market conditions and interest rates. Geographic location affects multiples significantly: service businesses in major metropolitan areas often command 10 to 20 percent premiums over similar businesses in smaller markets because buyer competition is fiercer. Size matters too: larger service businesses with $2 million or more in EBITDA typically command higher multiples than smaller ones because they offer more scale and lower per-transaction risk to buyers.

Growth Trajectories and Risk Adjustments Shape Your Multiple

Buyers pay premiums for service businesses that show clear growth trajectories, but you must prove growth is achievable with real data rather than projections. A business with 15 percent year-over-year revenue growth over the past three years deserves a higher multiple than one with flat revenue because growth demonstrates market acceptance and operational capability. Document your growth drivers explicitly: are you winning market share, expanding into new service lines, or selling more to existing clients? Each story carries different weight with buyers.

A documented plan to expand into adjacent services with a specific timeline and resource allocation adds 0.5x to 1x to your multiple because it shows how a buyer can drive returns post-acquisition. Conversely, market headwinds and industry consolidation pressure work against you. If your industry is contracting or facing disruption, expect multiple compression of 1x or more regardless of your company’s performance. Technology adoption and automation capability also factor heavily: a service business that invested in tools to improve efficiency and reduce labor dependency commands higher multiples than one still operating manually.

Three years of consistent, positive performance strengthens buyer confidence and valuation significantly. If you grew revenue 10 percent annually for three straight years while maintaining or improving margins, you occupy a strong negotiating position. Conversely, a business that was flat for two years then grew 20 percent in year three raises questions about sustainability. Buyers typically discount growth that appears temporary or dependent on one large client win.

Customer Concentration Directly Reduces Your Multiple

Customer concentration risk directly reduces your multiple: each percentage point of revenue from your largest client above 15 percent typically costs you 0.1x to 0.2x on your multiple. A business where the top client represents 25 percent of revenue instead of 15 percent might see a multiple compression of 1x or more, which translates to $200,000 to $400,000 in lost valuation for a $1 million EBITDA business. Work backward from your target valuation to understand what adjustments matter most: if you want to hit 5.5x EBITDA, identify whether you need to reduce customer concentration, improve margins, document growth plans, or build management depth.

Final Thoughts

Selling a service business requires you to focus on three core drivers: increasing your EBITDA and margins, reducing customer concentration, and documenting your operations thoroughly. These improvements compound over time, and the work you invest now translates directly into thousands of dollars at closing. A business that raises its EBITDA margin from 18 percent to 25 percent while shrinking its largest customer from 30 percent to 12 percent of revenue might see valuation jump from $600,000 to $900,000 or higher, depending on market conditions and growth trajectory.

You should start your preparation 12 to 18 months before you plan to sell a service business. Map your operations in writing, formalize employment agreements with non-compete clauses, and establish monthly financial close cycles. Normalize your EBITDA by removing one-time expenses and personal costs, track your customer concentration deliberately, and shift toward recurring revenue models. These steps take discipline, but they eliminate buyer hesitation and accelerate negotiations when you move forward.

When you’re ready to sell, you need a partner who understands valuation, handles confidentiality seriously, and connects you with qualified buyers. We at Unbroker built our platform specifically for business owners who want transparent pricing and no hidden fees. Get started with a clear valuation of your business today and explore your options with our Full Service Business Sale or Assisted Business Sale options.