Selling a business is one of the biggest financial decisions you’ll make. The difference between a rushed sale and a strategic one often comes down to preparation, pricing, and how effectively you market your company to the right buyers.

At Unbroker, we’ve seen firsthand how sellers who follow a structured approach consistently achieve higher valuations. This guide walks you through the essential steps to maximize your exit value.

Getting Your Business Ready to Sell

The first mistake most business owners make is assuming their financials are sale-ready when they’re not. Deloitte reports that 35.2% of M&A professionals expect increased due diligence scrutiny, which means buyers will examine your books harder than ever. Pull three years of financial records and due diligence requirements, profit and loss statements, and balance sheets. If your records are disorganized, budget $2,000 to $5,000 to reconcile them with a fractional CFO or accountant-this investment typically adds 10% to 15% to your final offer, making it worthwhile. Document every revenue stream and expense category separately so you can clearly show which items are recurring and sustainable versus one-off costs that won’t continue post-sale. Buyers care less about total revenue and much more about what actually sticks around and generates profit.

Build a Business That Doesn’t Need You

The second critical area is operational independence and management systems. If your business relies on you to function, buyers will either walk away or demand a steep discount. Spend the next 6 to 12 months deliberately building management systems that run without your direct involvement. Document standard operating procedures for your core processes, introduce your management team to key customers, and lock in multi-year contracts where possible. If a single customer represents more than 15% of your revenue, this is a major red flag. Diversify your customer base or at minimum show a clear plan to reduce that customer concentration risk before you list.

Reduce Dependency Across Your Operations

Similarly, diversify your suppliers and vendors so no single relationship creates dependency. Address any regulatory or compliance gaps now rather than during due diligence. Keep your business current with filings in your formation state and any other states where you operate, maintain an active registered agent, and obtain a certificate of good standing. These steps take weeks to complete but can prevent a buyer from walking away in the final stages when momentum matters most. With your financial records clean and your operations running independently, you’re positioned to move into the next phase: determining what your business is actually worth.

What Your Business Is Actually Worth

Valuation is where most sellers go wrong. They either pull a number from thin air, use an outdated rule-of-thumb multiple, or assume their revenue equals their value. The reality is harder: your business is worth what a buyer will pay for it, and that price depends on three concrete factors-what comparable businesses sold for, how much cash your business generates, and whether it can grow after you leave.

Calculate Your True Earnings

Start with the income approach, which works best for small operating businesses under $2 million in revenue. Take your net profit and add back owner compensation, one-time expenses, and non-recurring costs to calculate your Seller’s Discretionary Earnings (SDE). This shows a buyer what cash the business actually produces. For established firms with $2 million or more in revenue, use EBITDA (earnings before interest, taxes, depreciation, and amortization) instead. If your business is asset-heavy-manufacturing, equipment rental, real estate-factor in the asset-based value as a floor. A professional triangulation using all three methods costs $1,500 to $3,500 and gives you the credibility buyers demand. Without this investment, you negotiate blind.

Anchor Your Price to Market Data

Industry multiples anchor your price, but they vary dramatically by sector. The mistake is treating these as universal. A software company growing 20% annually commands the top of that range; one growing 5% sits at the bottom. Your job is to prove which tier you belong in. Pull three years of revenue and EBITDA data and show the trajectory. Document your customer contracts, pipeline, and market research to back up any growth claims-vague projections kill deals.

If you operate in Canada, finding true comparables is harder because private company sales rarely get disclosed. Statistics Canada publishes benchmarks by industry classification, but with hundreds of industry types, two similar-looking businesses can have vastly different profitability and risk profiles. Anchor your price with market data from reputable sources, not online calculators that oversimplify with a handful of inputs and ignore industry context, management quality, and economic conditions.

Build a Growth Narrative That Justifies Your Multiple

Your growth story matters as much as your multiple. A business showing consistent 15% annual growth with stable margins and recurring revenue justifies a higher valuation than a flat business, even if both hit the same EBITDA number today. Buyers pay for predictability and momentum, not just current earnings. Once you’ve established what your business is worth based on solid data and realistic growth projections, the next step is presenting that value to the right buyers in a way that makes them want to act.

How to Market Your Business to the Right Buyers

Most sellers waste months broadcasting their business to hundreds of tire-kickers instead of focusing on 50 qualified buyers who actually have capital and strategic intent. Targeted marketing to vetted prospects closes faster and at higher prices than spray-and-pray approaches that erode confidentiality and invite low-ball offers.

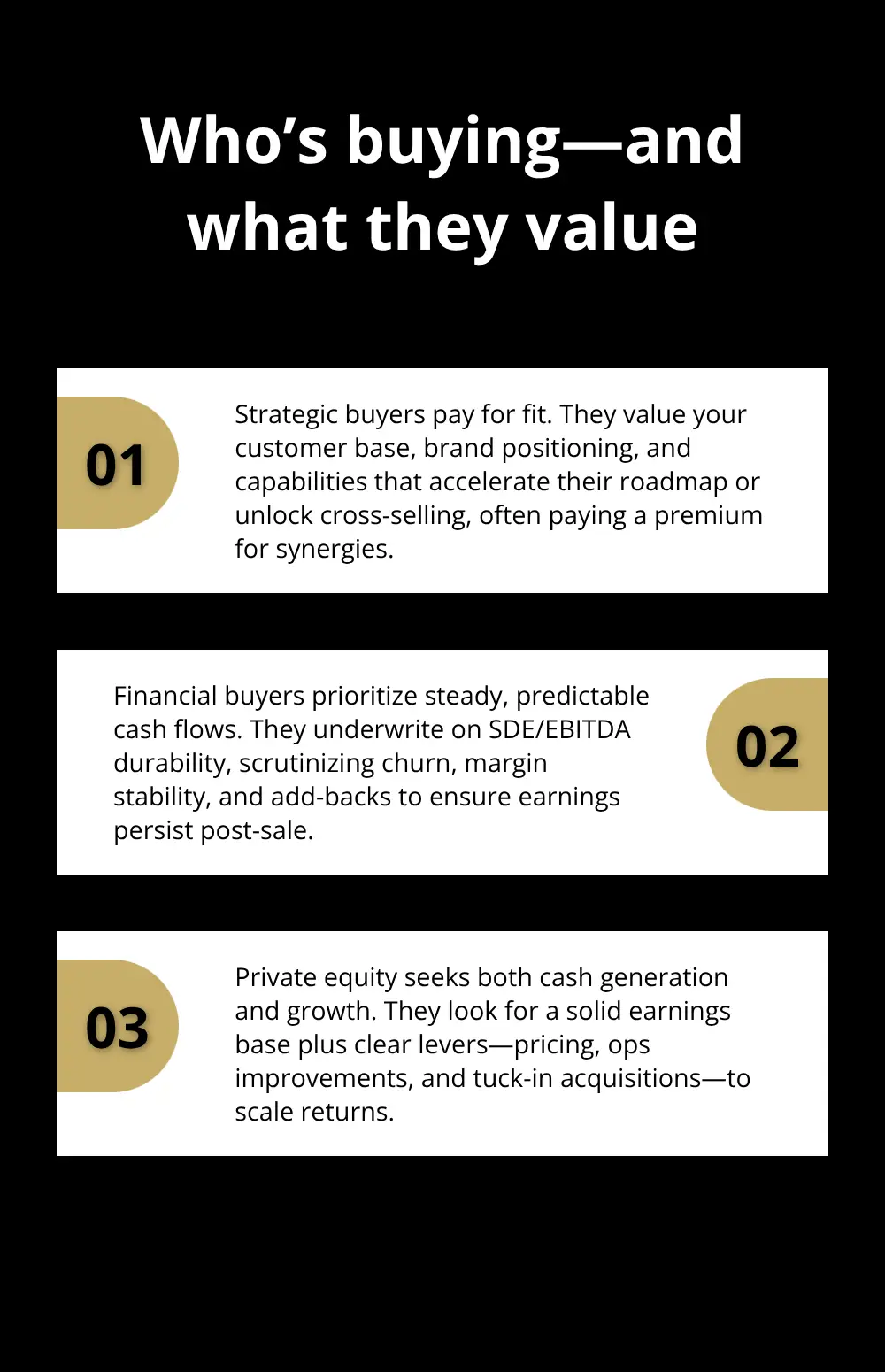

Define Your Ideal Buyer Profiles

A strategic buyer in your industry will pay a premium for your customer base and market position. A financial buyer focuses on metrics like a business’s EBITDA to assess cash flow stability and predictable earnings, so they care less about growth stories and more about whether your EBITDA will hold steady post-sale. Private equity firms sit somewhere in the middle, valuing both cash generation and growth potential.

Craft separate messaging for each type. For a strategic buyer, emphasize how your customer relationships, proprietary processes, and market access accelerate their expansion plans. For a financial buyer, highlight recurring revenue, customer retention rates, and management depth that prove the business runs without you. For PE, show both the cash foundation and the runway to hit higher margins through operational improvements.

Screen Buyers and Protect Confidentiality

Screen buyers early and aggressively. Before sharing detailed financials, ask about their capital sources, deal timeline, and strategic fit. Require proof of funds for serious contenders. This single step cuts deal fatigue by eliminating window-shoppers and keeps your sale process moving.

Market your business through multiple channels depending on your sector. A software company benefits from tech-focused platforms; a manufacturing business reaches industrial buyers on specialized databases. Avoid generic online marketplaces that attract mostly browsers. Online business-for-sale marketplaces connect you to a broad buyer network while maintaining confidentiality through NDAs and structured data rooms.

Tell a Compelling Story With Numbers

Your business profile must tell a story, not recite facts. Lead with your competitive advantage: a customer base that spans three industries, a patent-protected process, recurring subscription revenue, or a management team that runs operations. Back every claim with numbers.

Instead of saying you have strong customer relationships, state that your top 10 customers represent 40% of revenue and have been with you for an average of 8 years. Instead of claiming market leadership, cite your market share percentage or growth rate relative to industry benchmarks. Buyers respond to specifics because specifics reduce perceived risk.

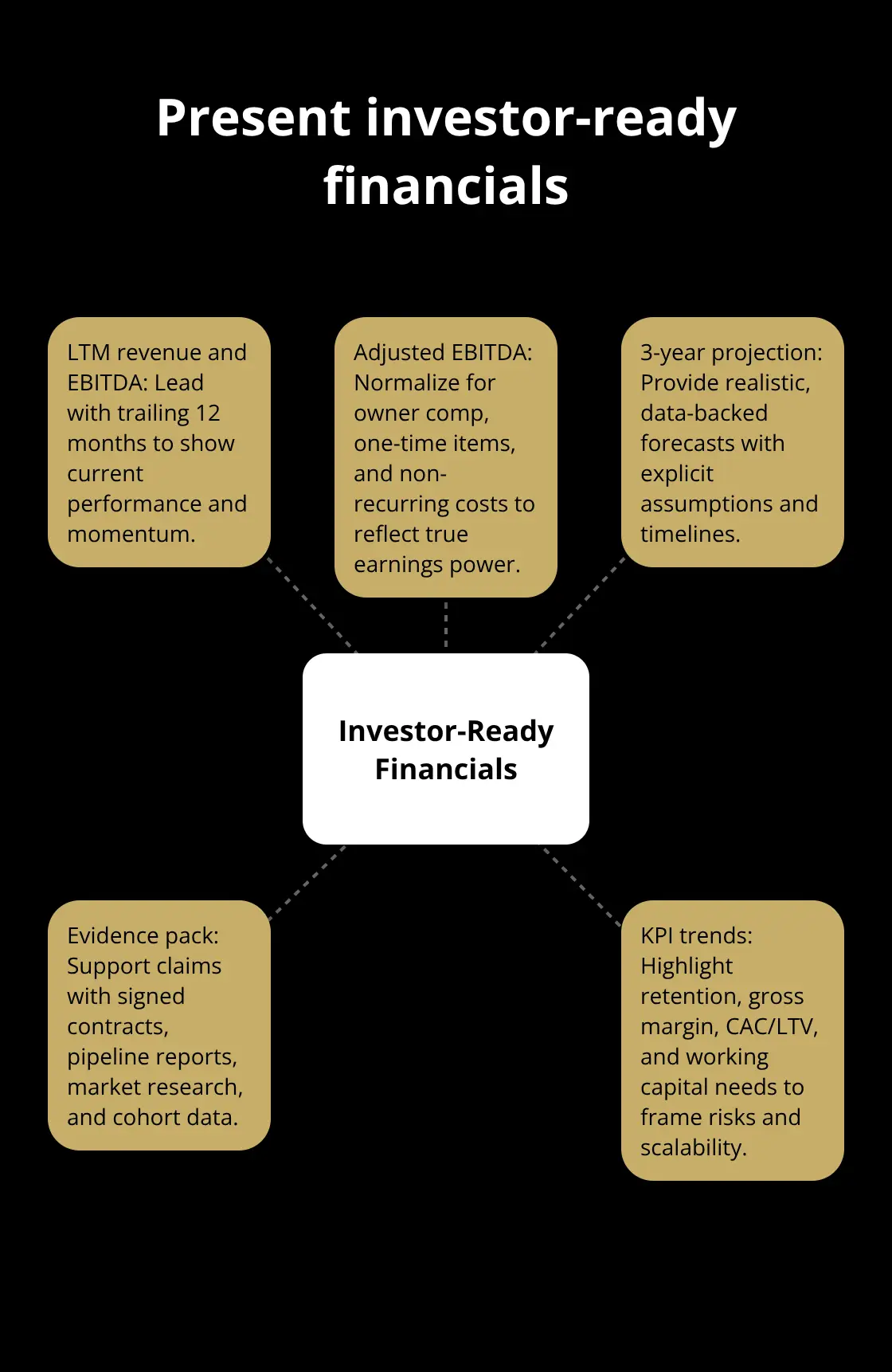

Present Concrete Financial Data and Projections

Present your last 12 months of revenue and EBITDA prominently, along with your adjusted EBITDA that normalizes add-backs like owner compensation or one-time costs. Include a three-year growth projection backed by signed customer contracts, pipeline data, or market research, not speculation.

The more concrete your investment story, the faster buyers move to offer stage.

Final Thoughts

Selling a business requires discipline across three areas: preparation, pricing, and marketing. Most sellers stumble because they skip one or treat it as optional. The owners who maximize exit value execute all three methodically, and they invest 12 to 24 months in the process rather than rushing to close. This timeline isn’t wasted time-every month you spend strengthening operations, documenting processes, and building a credible valuation story translates directly into higher offers and smoother closings.

Assemble your deal team early: an M&A attorney, a CPA, and ideally an M&A advisor who understands your industry. These professionals pay for themselves by structuring the deal correctly and protecting you during negotiations. They also help you navigate the complexities of tax optimization, earnout structures, and post-closing obligations that most sellers overlook. When you sell a business with the right advisors in place, you avoid costly mistakes that erode your final proceeds.

We at Unbroker built a platform to simplify this entire process with transparent, low-cost options and no hidden fees. You gain access to confidential buyer networks, legal templates, and negotiation support that fit your situation without the traditional brokerage markup. Your exit is too important to leave to chance-follow the framework in this guide, invest in the right advisors, and you’ll position yourself to sell at a price that reflects your business’s true value.