Selling your business is one of the biggest financial decisions you’ll make. But the real work often starts after the deal closes.

At Unbroker, we’ve seen countless business owners caught off guard by what comes next. A solid post-sale support plan removes the guesswork and keeps everything on track during the transition.

What Happens After You Sell Your Business

The first 30 to 90 days after closing are critical. During this period, you manage three simultaneous processes: establishing the new ownership structure, transferring legal and financial obligations correctly, and maintaining stability with your team and customers. Most sellers underestimate how much coordination this requires. The timeline typically breaks into two phases: the immediate handover (days 1-30) where you transfer access, passwords, customer lists, and operational procedures, and the transition period (days 31-90) where the new owner integrates systems and you answer questions. A detailed transition plan with specific dates, responsible parties, and deliverables prevents critical information from falling through the cracks. Sellers who skip this planning step often field urgent calls months after the deal closes because nobody documented how a key client relationship worked or where certain financial records were stored.

The Ownership Transfer Demands Your Full Attention

Legal documents and ownership transfer require precision. You must file articles of amendment with your state, update business licenses, transfer permits and certifications, and notify the IRS of the ownership change. This isn’t optional paperwork-missing deadlines can expose you to liability or create tax complications. Many sellers assume their accountant or the buyer’s lawyer will handle everything, but responsibility often falls between the cracks. You should maintain a checklist of every document that needs to transfer, verify completion, and keep copies for your records. The financial settlement piece requires careful attention: final working capital adjustments, earnout calculations, and tax escrow arrangements frequently generate disputes months after closing. A clear written agreement about how these will be resolved prevents misunderstandings that can damage your relationship with the buyer and potentially lead to legal action.

Communication Shapes Your Legacy and Protects Your Reputation

How you communicate the sale to employees and customers determines whether they stay with the new owner or leave. Employees need to hear directly from you that their jobs are secure and what changes to expect, ideally before rumors spread. A clear message about management continuity, any role changes, and how to reach leadership during transition eliminates anxiety. For customers, timing matters: inform key accounts personally before a public announcement, especially if contract terms or service delivery might change. Transparency about leadership transitions maintains trust. The new owner will appreciate customers who feel confident in the transition rather than confused or worried. Your reputation remains tied to how the business performs in those first months after you step back, which is why the next phase-addressing the specific challenges that emerge during handover-requires your immediate attention.

Common Post-Sale Challenges Business Owners Face

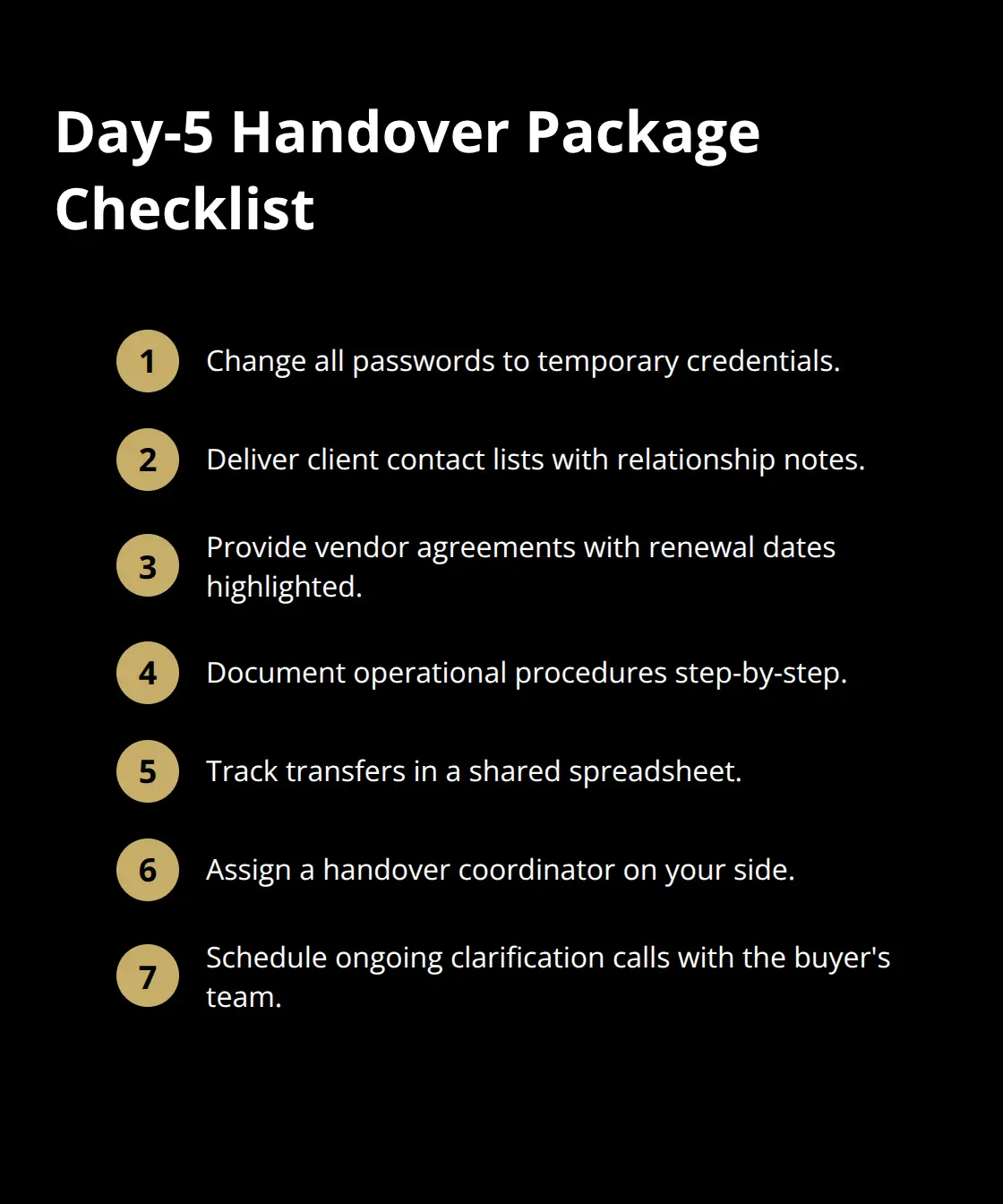

The handover phase exposes gaps that didn’t matter when you owned the business. The buyer expects complete access to everything-customer contracts, vendor relationships, financial records, software logins, operational procedures-within days, not weeks. Most sellers never documented critical processes because they lived in their heads. You knew how to handle the top three clients, but nobody else did. You knew the supplier who gives better terms if you call on Thursdays, but that knowledge existed only with you. The buyer will demand this information in writing, and the longer you delay, the more frustrated they become. Set a hard deadline of day five to deliver a complete handover package: every password changed to temporary ones, every client contact list with relationship notes, every vendor agreement with renewal dates highlighted, and every operational procedure documented step-by-step. Use a shared spreadsheet to track what’s been transferred and what’s still pending. This prevents the buyer from chasing you for missing pieces three months later. Assign one person on your side as the handover coordinator-not yourself, because you’re emotionally drained and prone to forgetting details.

That coordinator owns the checklist and follows up daily with the buyer’s team to confirm receipt and understanding. Plan for ongoing clarification calls where the buyer’s team asks how things actually worked and why certain decisions were made.

Buyer Questions Reveal Hidden Problems

The buyer will ask questions you didn’t anticipate because they see the business through a different lens. They’ll want to know why customer retention dropped in Q3 two years ago, why a key employee left suddenly, or why margins compressed in a specific product line. These questions feel like accusations, but they’re usually just due diligence they should have done before closing. Your job is to answer factually without defensiveness. Prepare a detailed Q&A document before closing that covers the last three years of performance, including any setbacks and how you handled them. When the buyer asks why a customer left, you state exactly what happened, not a sanitized version. This builds credibility and prevents them from discovering something worse later and feeling deceived. Some buyer concerns will be about changes they want to make immediately. They might want to renegotiate supplier contracts, shift the sales approach, or cut costs in operations. You have limited leverage here once the deal closes, so don’t waste energy fighting these decisions. Your job is to explain how the current approach works and what risks they face if they change it. Then step back. They own the business now. If they ignore your advice and it fails, that’s their problem.

Earnout Payments Require Precise Language

The most dangerous buyer concerns involve earnout payments. If your deal includes an earnout-where you receive additional payment based on future performance-the buyer controls the outcome. If they’re running the business poorly and your earnout depends on hitting revenue targets, you face a real problem. This is why earnout clauses need specific, measurable definitions written into the purchase agreement before closing. Revenue is either hit or it isn’t. EBITDA is calculated using specific accounting methods. Avoid vague language like improved performance or reasonable efforts because the buyer will interpret it in their favor. The purchase agreement should specify exactly how working capital gets calculated-which assets count, which don’t, and what valuation method applies. Don’t let this be negotiated casually. Get a CPA involved before you sign anything.

Tax Settlements Create Surprises Months Later

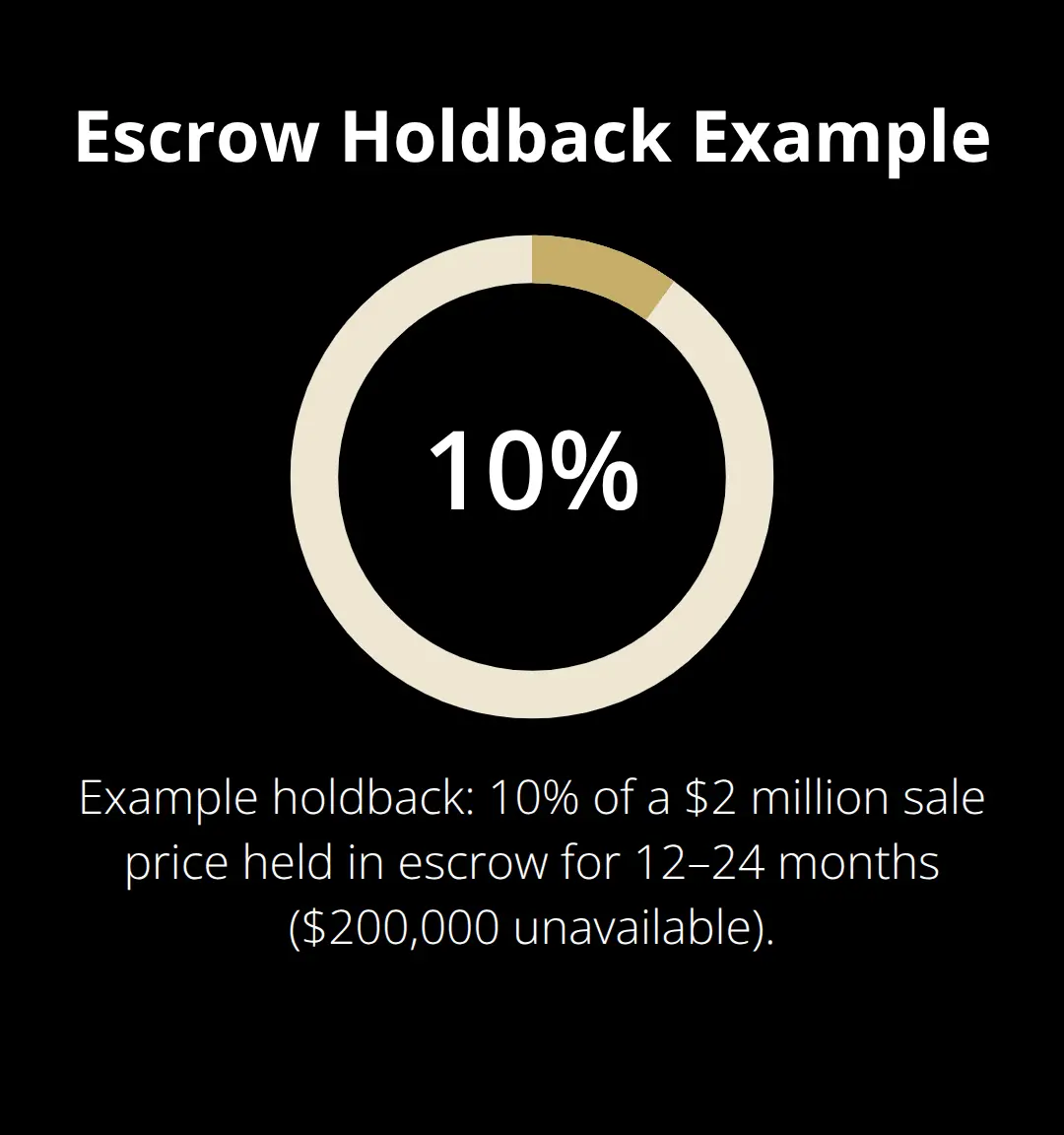

Tax implications don’t disappear at closing-they multiply. The IRS views business sales differently than you do, and the buyer’s accountant will have different opinions than yours about how to structure the deal for tax purposes. Working capital adjustments typically happen after closing when the buyer’s accountant reconciles what you said inventory and receivables were worth versus what they actually are. If you claimed inventory was worth $200,000 but it was really worth $150,000, you owe the buyer $50,000. This surprises sellers who thought the deal was done. Escrow accounts hold back a portion of the purchase price to cover potential disputes and tax adjustments. Many sellers don’t understand how much money sits in escrow or when they’ll actually get it.

If 10% of the sale price goes into escrow and your deal is $2 million, that’s $200,000 sitting unavailable for 12 to 24 months. You need that money for your personal plans after the sale, so escrow amounts matter significantly. Negotiate the smallest escrow amount possible and the shortest holdback period the buyer will accept. Capital gains taxes hit differently depending on whether the sale qualifies as a stock sale or asset sale, and the buyer often prefers asset sales for their tax benefits while you prefer stock sales for yours. These conflicting interests require negotiation upfront, not confusion later. If you have employees with deferred compensation or severance agreements, those obligations transfer to the new owner, but the buyer might not honor them the way you would. Clarify in writing what happens to employee benefits and severance before closing so there are no surprises when the buyer lays someone off immediately after taking over.

Who Actually Handles Post-Sale Issues When Problems Emerge

Most business sellers assume the buyer’s team will figure things out after closing, but that’s naive. The buyer stays busy integrating systems, managing operations, and making changes. They’re not thinking about explaining historical decisions or resolving disputes fairly. You need someone in your corner who understands both your interests and the legal landscape of post-sale obligations.

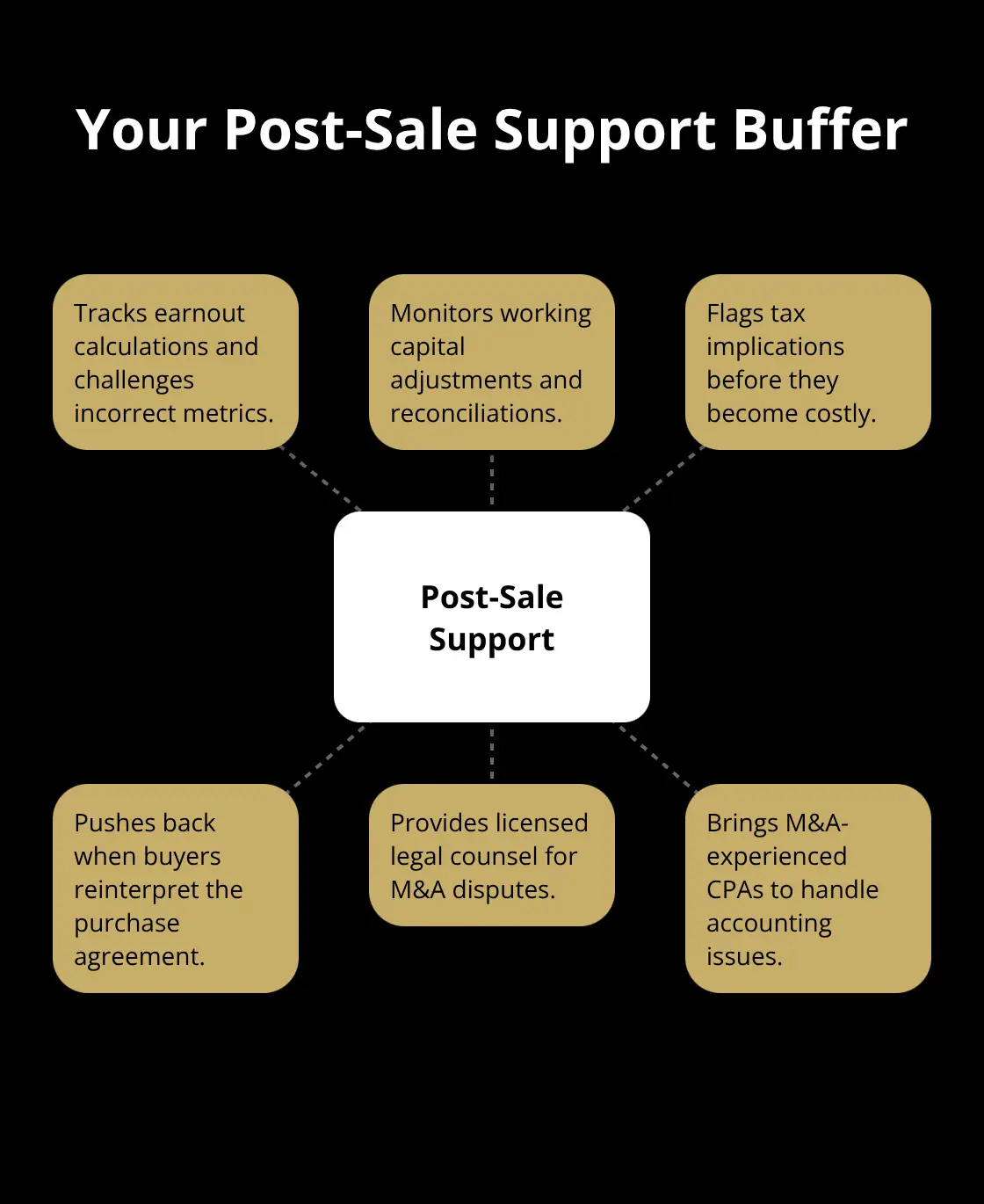

The right post-sale support provider acts as your buffer between buyer demands and your peace of mind. They track earnout calculations, monitor working capital adjustments, flag tax implications before they become expensive surprises, and push back when the buyer tries to reinterpret the purchase agreement in their favor.

Industry-Specific Experience Protects You From Hidden Landmines

This person or firm should have deep experience with business sales in your industry because every sector has different landmines. A provider who has closed 50 software company sales understands recurring revenue, customer concentration risk, and SaaS-specific working capital issues. That same provider might be useless for a manufacturing sale where inventory valuation and equipment condition matter more. Start by asking potential providers how many transactions they’ve closed in your specific industry and what percentage involved earnouts or working capital adjustments. If they can’t give you concrete numbers, keep looking. Experience matters more than marketing promises because post-sale disputes cost real money. One earnout dispute that drags into litigation costs $50,000 to $150,000 in legal fees alone, making an experienced advisor worth their weight in gold.

The Service Package Must Cover Your Specific Risks

A generic post-sale support plan won’t protect you. If your deal includes an earnout, the provider must specialize in earnout disputes and have language templates that prevent the buyer from gaming revenue calculations. If your sale involved significant working capital adjustments, they need a CPA network ready to challenge the buyer’s accounting if it’s wrong. If you’re concerned about tax implications, they should have tax attorneys who understand M&A structures and can review the purchase agreement before you sign. Request a detailed breakdown of what each service package includes and ask directly whether it covers your specific situation. Some providers offer basic document review but won’t attend buyer meetings or defend your position during disputes. Others provide comprehensive support but charge $10,000 to $25,000 upfront, which might be excessive if your deal is relatively straightforward.

Pricing for post-sale support varies wildly depending on whether the provider charges hourly rates, flat fees, or contingency arrangements. Hourly rates typically run $250 to $500 per hour for experienced M&A attorneys, which adds up quickly if disputes drag on. Flat-fee arrangements cost $5,000 to $20,000 but only make sense if you know exactly what support you’ll need. Contingency arrangements, where the provider takes a percentage of disputed amounts they recover, align incentives but often exclude routine support like earnout monitoring. Ask whether the fee covers ongoing communication with the buyer or only responds to specific disputes. If the buyer asks you a question about working capital adjustments in month three after closing and your provider charges hourly to answer that question, you’ll face a bill just to get clarification.

Verify They Have Real Legal and Tax Firepower

This is where many sellers get burned. A post-sale support provider who is really just a business consultant with no legal credentials can’t defend you in disputes or negotiate with the buyer’s attorney. You need someone licensed to practice law in your state who specializes in M&A transactions, not general corporate law. Ask directly whether the provider has in-house legal counsel or contracts with specific law firms. If they contract with firms, get the names and verify those firms actually exist and have M&A experience. Some providers name-drop prestigious law firms without actual relationships, which leaves you without legal backup when you need it.

The same applies to tax expertise. Working capital adjustments and earnout calculations require someone who understands both business accounting and tax law. A CPA who handles general bookkeeping won’t catch the subtle issues that cost you thousands. Your provider should have access to CPAs with M&A experience who have handled working capital disputes specifically. Ask for references from past clients who dealt with earnout or working capital disputes, not just satisfied sellers who had smooth closings. A smooth closing tells you nothing about whether your provider will fight for you when things get complicated. The provider who helped you through an earnout dispute where the buyer tried to manipulate EBITDA calculations is the one worth paying for.

Continuity Matters More Than You Think

Verify that whoever provides legal and tax support stays available during the post-sale period, not just during the sale itself. Many firms front-load their team during the transaction but disappear afterward. You need continuity with someone who understands your deal and can pick up a phone when month 14 of a 24-month escrow period brings a dispute you didn’t anticipate. The provider who knows your specific earnout language, your working capital adjustment methodology, and your tax structure can resolve issues fast. A new provider brought in months later has to relearn everything, which costs you time and money. This is why you should ask potential providers about their post-sale availability and response times before you sign anything. If they won’t commit to specific availability windows or charge premium rates for post-sale calls, that tells you they don’t prioritize post-sale support. The best providers treat post-sale work as core to their business, not an afterthought.

Final Thoughts

Selling your business demands more than just closing a deal. The 90 days after signing expose gaps in documentation, trigger buyer questions you didn’t anticipate, and create financial disputes that linger for months. A solid post-sale support plan protects you from these predictable problems by ensuring someone monitors earnout calculations, flags working capital disputes before they become expensive, and pushes back when the buyer tries to reinterpret terms in their favor.

Professional post-sale support matters because the buyer controls the business after closing. They set the pace for answering your questions, they interpret ambiguous contract language in their favor, and they manage the financial metrics that determine your earnout payments. An experienced advisor levels the playing field by ensuring the buyer honors the terms you negotiated and catches problems early when they remain fixable.

Your next step is straightforward: review your purchase agreement and identify your specific risks (earnouts, working capital adjustments, tax implications), then find a provider with concrete experience handling those exact issues in your industry. Ask for references from sellers who faced disputes, not just smooth closings, and verify they have licensed legal counsel and experienced CPAs available during the post-sale period. Visit Unbroker to explore how we support your business sale from start to finish with transparent pricing and no hidden fees.