Selling your business without a broker is possible, but you need the right tools and knowledge. We at Unbroker have created this DIY sellers toolkit to guide you through every step of the process.

From preparing financial documents to closing the deal, this guide covers the templates, strategies, and tactics you’ll need to succeed.

Essential Documents and Templates for DIY Business Sales

Selling a business without a broker means you handle the paperwork that typically gets filtered through a middleman. Most buyers won’t even look at your business seriously until they see three specific document types, and missing any one of them kills deals fast.

Financial Statements: The Foundation Buyers Verify

Buyers demand at least two to three years of tax returns, profit and loss statements, and balance sheets to verify your numbers. Their accountants and lenders will request these anyway, so prepare them early. Many DIY sellers make the mistake of cleaning up their financials before showing them to buyers, which creates red flags. Show your actual historical documents instead. If your numbers are messy, buyers assume you’re hiding something worse.

Organize your financial documents into a single folder before you list your business, including tax returns, bank statements, profit and loss statements, and accounts receivable aging reports. Include utility bills, lease agreements, and supplier contracts that show your true operating costs. Buyers verify everything anyway, so complete transparency accelerates the process. Most DIY sellers underestimate how much time document gathering takes-set aside two weeks minimum to pull together clean, organized financials. If your bookkeeping is chaotic, hire an accountant for a few hours to organize the last three years.

This investment pays for itself by speeding up due diligence and preventing price negotiations based on confusion.

Confidentiality Agreements: Protect Competitive Secrets

Confidentiality agreements serve a specific purpose: they protect your business information from competitors who might pose as buyers. Your agreement should specify what information qualifies as confidential, how long the obligation lasts, and what happens if someone violates it. Include a return or destruction clause that requires buyers to return all documents if they don’t move forward.

This step matters most if you operate in a competitive market where a leaked customer list or pricing structure damages your value. Many sellers skip this step and regret it when a competitor gains access to sensitive data. Draft an NDA that prevents anyone viewing your financials from using that information against you or sharing it publicly.

Purchase Agreements: Where Legal Details Matter

Purchase agreements and term sheets spell out exactly what’s being sold, the price, payment terms, and contingencies. A weak purchase agreement leads to disputes during closing or even post-sale claims. Address the items that sink most DIY deals: inventory valuation, customer contract assumptions, and employee transition responsibilities. State whether the buyer assumes existing leases or renegotiates them. Clarify which liabilities transfer and which stay with you.

Include specifics like which assets transfer, whether you stay on as a consultant, and how disputes get resolved. Many DIY sellers use generic templates from online sources, which often miss industry-specific details or state requirements. Your agreement needs to address non-compete clauses, earnest money deposits, and what happens if the buyer’s financing falls through. Consider having a local business attorney review your templates before using them ($200 to $400 typically covers a two-hour consultation and catches gaps that generic templates miss). The difference between a vague agreement and a detailed one often determines whether a deal closes smoothly or falls apart in the final weeks.

With your documents in place, you’re ready to position your business in front of qualified buyers-which means creating a listing that actually captures their attention and demonstrates clear value.

How to Get Your Business in Front of Qualified Buyers

Your financial documents are organized and your legal agreements are locked down. Now comes the part that actually generates offers: positioning your business where serious buyers actually look. Most DIY sellers make a critical mistake here-they treat their business listing like a classified ad instead of a sales document. A weak listing kills deals before they start. Your listing needs to answer the one question every buyer asks first: why should I care about this business over the dozens of others available right now?

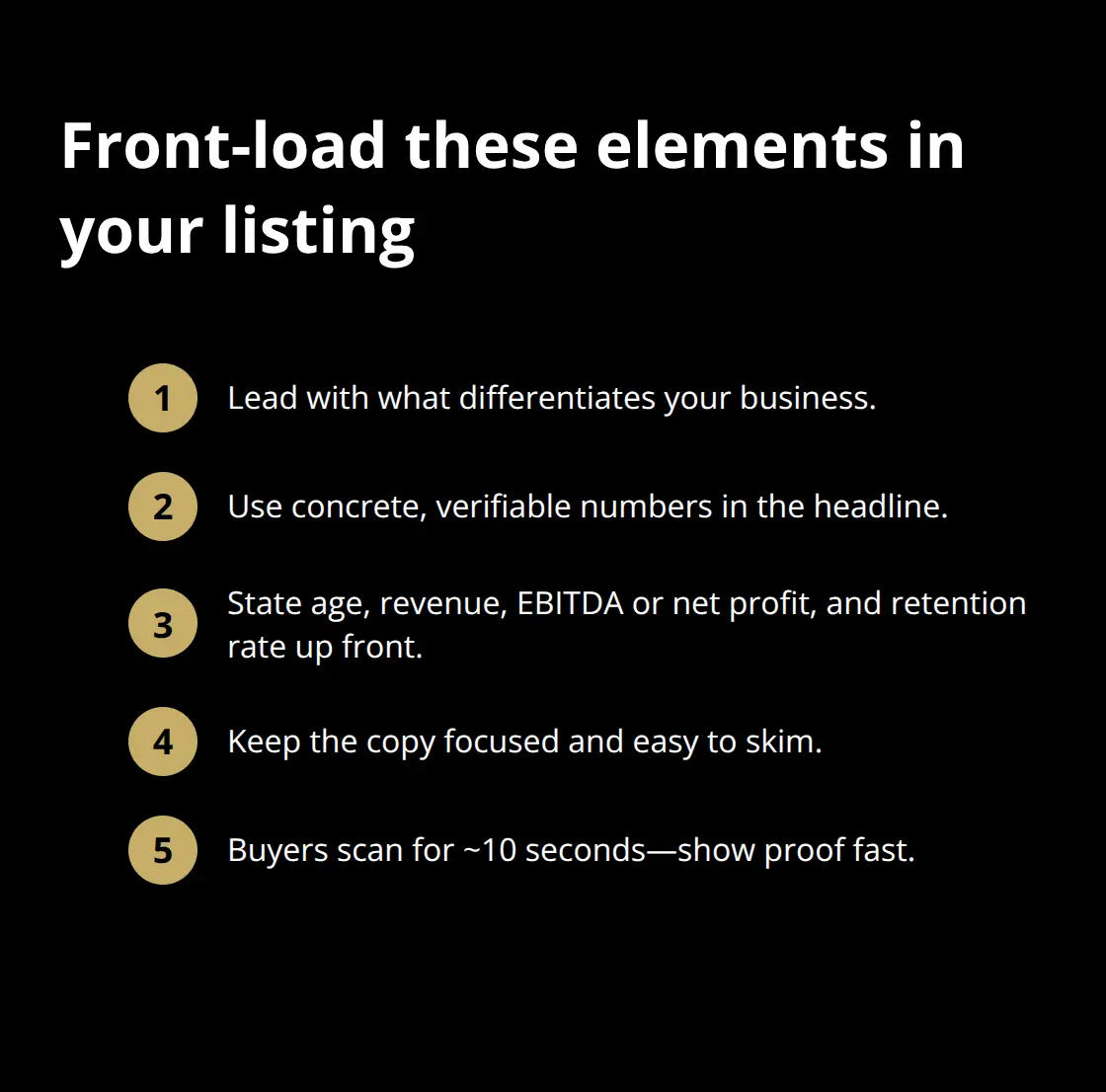

Write a Headline That Stops Scrollers

Lead with what makes your business different, not generic descriptors. Instead of “Business for Sale in [City],” try “Established HVAC Service with 200+ Recurring Residential Contracts” or “Profitable Ecommerce Brand Generating $85K Monthly Revenue.” Include your actual numbers because they filter serious buyers from tire-kickers. Add the business age, current revenue, EBITDA or net profit, and customer retention rate in the first paragraph. Buyers scan listings for 10 seconds before deciding whether to dig deeper, so front-load the metrics that prove viability.

Structure Your Listing for Maximum Impact

Your listing should run 400 to 600 words and cover what the business does, why customers stick around, what systems are already in place, and what a new owner would inherit. Mention any recurring revenue and long-term contracts because these reduce buyer risk. Include 8 to 12 high-quality photos that show your operation, customer-facing spaces, and team-visuals matter because they build confidence that this business is real and professional.

Post on Multiple Platforms and Networks

Post your listing on major platforms like BizBuySell, Flippa for digital businesses, or industry-specific marketplaces depending on your business type. Each platform reaches different buyer pools, so don’t limit yourself to one. Add your listing to LinkedIn and relevant industry forums where potential acquirers actually search. Many buyers start their search on Google or industry boards before hitting marketplace sites, so make sure your business appears when they search keywords related to your industry and location. Maximize your listing exposure by understanding which channels attract serious buyers in your sector.

Reach Out to Your Network Directly

Leverage your existing network by sending a confidential sell sheet directly to people who might know qualified buyers-past customers, suppliers, or business peers who’ve mentioned expansion plans. This personal outreach often generates serious inquiries faster than public listings because these leads come with context and credibility. When building your outreach list, prioritize strategic buyers in your industry who have shown acquisition interest, competitors looking to expand, and financial buyers seeking cash-flowing businesses. Research who acquired similar businesses in your space over the last two years and contact them directly. Send a one-page summary highlighting your business strengths, revenue, and growth trajectory without revealing sensitive details until they sign your NDA.

Measure What Works and Adjust

Track which channels generate the most qualified inquiries so you can adjust your marketing spend accordingly. If a platform costs money to list, measure whether the leads justify the expense before continuing. Most DIY sellers find that a combination of free marketplace listings plus targeted outreach to their network produces 60 to 70 percent of serious offers. Once qualified buyers start responding to your listing, you’ll face a new challenge: separating genuine interest from casual inquiries and moving serious prospects toward an actual offer.

How Buyers Think and What Actually Closes Deals

Most DIY sellers enter negotiations thinking the price is what matters most. It isn’t. Serious buyers care about three things in this order: certainty of closing, timing, and then price. A buyer offering $5,000 less but with cash and no contingencies beats a higher offer dependent on financing and a home inspection every single time. Understanding what actually drives buyer decisions changes how you negotiate.

What Different Buyer Types Actually Want

Strategic buyers acquiring competitors want to know exactly how customers will react post-sale and whether key team members will stay. Financial buyers focused on cash flow want proof that revenue won’t drop after the transition. First-time business buyers worry about operational complexity and whether they can run the business without your constant involvement. Your negotiation approach needs to match the buyer type sitting across from you.

Ask qualifying questions early: Are they using their own capital or seeking financing? Have they owned a business before? What timeline works for their situation? These answers tell you what concessions matter and which ones don’t. A buyer desperate to close in 30 days might accept a higher price to skip extended due diligence. A buyer with months to spare will grind you on details and price because they have leverage.

Evaluating Multiple Offers on Real Terms

When multiple offers arrive simultaneously, your instinct might be to auction upward. Resist it. Instead, evaluate each offer across five dimensions: purchase price, earnest money deposit amount, financing contingencies, timeline to close, and seller financing or earnest money holdback. A $500,000 cash offer with a 30-day close beats a $520,000 offer contingent on the buyer securing a Small Business Administration loan in 60 days roughly 70 percent of the time based on actual deal velocity data.

Set a deadline for best and final offers, typically 48 to 72 hours, then rank offers by closing probability rather than raw price. Communicate your decision in writing with specifics: you’re moving forward with an offer that includes these terms because they reduce execution risk. If your top choice falls through, you have a ranked backup ready. Never negotiate with two buyers simultaneously at the final stage because one will withdraw and you’ll lose leverage.

Strategic Counteroffers That Move Deals Forward

During counteroffers, move only one variable at a time. If a buyer requests a lower price and an extended closing timeline simultaneously, counter with the lower price but tighter timeline, forcing them to prioritize what actually matters. Most deals stall because sellers try to win every point instead of trading strategically. Give ground on timeline if the buyer raises their offer. Concede on earnest money if they remove inspection contingencies. Track every counteroffer in writing with clear deadlines, typically 24 hours for a response.

Managing the Final Stretch to Closing

The period between signed agreement and final closing determines whether deals actually complete. Document everything in writing. If a buyer requests to delay closing because their financing hasn’t cleared, that delay needs to be formally amended with new dates and any adjusted terms. Assign a specific person to manage closing logistics: coordinate with the buyer’s lender, your accountant, the attorney handling paperwork, and the title company.

Most DIY sellers lose deals in the final 30 days because communication breaks down and surprises emerge. Schedule a weekly call with all parties involved so issues surface early rather than at closing. Request the buyer’s loan approval letter within 14 days of agreement signing so you know their financing is real. If they can’t produce it, the deal has problems. Require a final walkthrough 48 hours before closing to confirm the buyer hasn’t changed their mind about the condition or inventory.

Set specific expectations about what the buyer can and cannot remove or modify before the sale closes. Many deals collapse because a buyer starts treating the business as theirs before closing and makes operational changes that tank the deal value. Maintain control until money transfers and documents sign. Your final check should verify that the buyer’s accountant has reviewed all financial documents without requesting major adjustments, which signals they’re comfortable with the numbers.

Final Thoughts

Selling your business without a broker works when you follow a structured process and stay disciplined through closing. The DIY sellers toolkit covers three areas that separate successful sales from failed ones: organizing your documents so buyers trust your numbers, positioning your business where qualified buyers actually search, and negotiating on terms that reduce your risk instead of chasing the highest price. Most DIY sellers underestimate how much time document preparation takes, so start there first.

Buyers won’t move forward without clean financial statements, a solid purchase agreement, and confidentiality protection. Your listing and marketing strategy determine how many qualified offers you receive, and a weak listing generates tire-kickers while a strong one attracts multiple serious buyers competing for your business. During negotiations, price ranks third behind closing certainty and timeline-a lower cash offer that closes in 30 days beats a higher offer dependent on financing every time.

The final stretch to closing determines whether deals actually complete, so document everything in writing and schedule regular calls with all parties to verify the buyer’s financing is real. If managing this process alone feels overwhelming, explore Unbroker’s Assisted Business Sale service, which provides expert guidance for DIY sellers who want professional help without paying traditional broker fees.