Most business owners focus on revenue when pricing their company. That’s a mistake.

At Unbroker, we know that cash flow valuation is what actually determines what a business is worth. The money flowing through your business-and what remains after expenses-tells the real story of profitability.

How Cash Flow Actually Determines What Your Business Is Worth

Discounted cash flow analysis strips away accounting illusions and gets to what matters: the actual cash your business generates. This method values a company based on the present value of its future cash flows, adjusted for risk and time. A company generating $5 million in annual revenue but only $200,000 in free cash flow is worth far less than a competitor with $3 million in revenue and $800,000 in free cash flow. The difference lies in what remains after you pay operating expenses and reinvest in assets.

Free cash flow equals cash from operations minus capital expenditures, representing genuine profit that can fund debt repayment, dividends, or growth. When you apply a discount rate to these cash flows, you account for two realities: the time value of money and the risk that projected cash flows may not materialize. A pound today is worth more than a pound tomorrow because you can invest it now. If your business shows uncertain cash flows, investors demand a higher discount rate to compensate for that risk. For established businesses with stable cash flows, this method provides a more reliable valuation than revenue-based approaches alone.

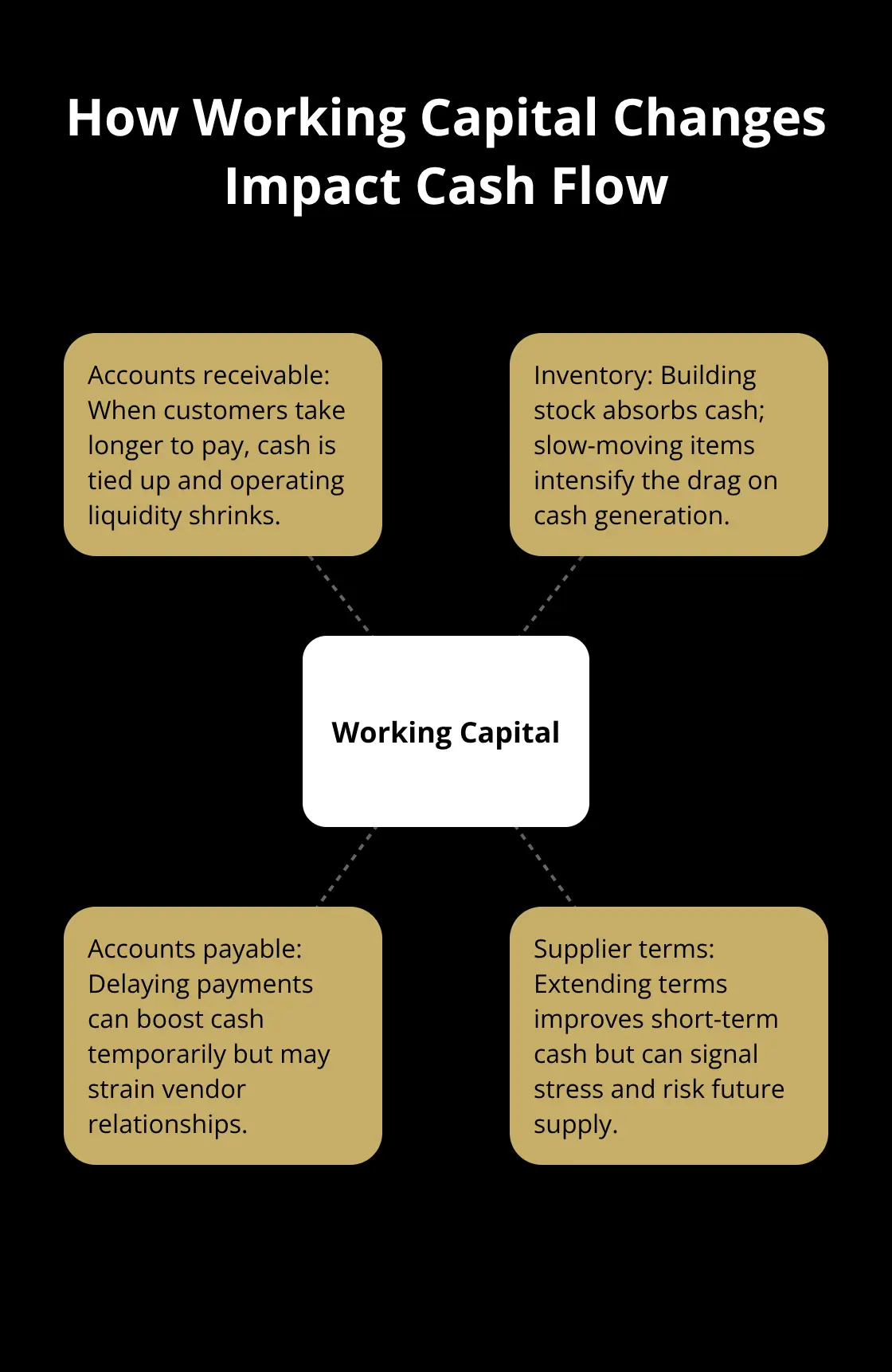

Why Working Capital Changes Distort Your Picture

Most business owners overlook how changes in receivables, inventory, and payables affect cash flow. A company growing rapidly might show increasing profits on paper while cash flow deteriorates because money gets tied up in inventory or customer credit. If your accounts receivable increase by $100,000 year-over-year, that’s $100,000 less cash available despite higher sales. Similarly, extending payment terms to suppliers improves cash position temporarily but signals potential vendor relationship stress.

You must monitor these working capital changes to reveal whether your business truly generates cash or simply shifts money around. A diverging trend where revenue rises while cash flow falls signals trouble that earnings reports mask. This pattern often indicates that inventory builds up, customers take longer to pay, or you accelerate capital spending without corresponding profit growth.

The Discount Rate Separates Realistic Valuations from Wishful Thinking

Choosing the right discount rate determines whether your valuation reflects reality or fantasy. This rate reflects both the risk-free return you could earn elsewhere and the additional risk premium your business carries. A stable, mature business might use a 7–10 percent discount rate, while a volatile startup could justify 15–25 percent. Higher discount rates produce lower valuations because future cash flows are worth less in present-value terms.

Many business owners underestimate their risk and apply discount rates that are too low, inflating their valuation by 20–40 percent. You need honest assessment of competitive threats, customer concentration, and market conditions to get this right. When you sell a business, buyers will apply their own discount rate, and if it differs significantly from yours, you’ve found a pricing gap that explains negotiation friction.

How to Calculate Free Cash Flow from Your Financial Statements

You derive free cash flow from your cash flow statement using a straightforward formula: cash from operations minus capital expenditures. Start with net income, add back non-cash expenses (depreciation, amortization, stock-based compensation), and adjust for changes in working capital. Non-cash working capital changes include increases in accounts receivable, inventory, and accounts payable. If no cash flow statement exists, you can estimate capital expenditures by calculating the year-over-year change in property, plant, and equipment plus depreciation.

Positive free cash flow indicates your company can pay debts and fund growth or distributions. Negative free cash flow signals a potential external funding need and suggests your business consumes more cash than it generates. A stable positive free cash flow trend over four to five years predicts positive business performance more reliably than a single year of high cash flow. This multi-year perspective reveals whether your cash generation is sustainable or merely a temporary spike.

Now that you understand how cash flow determines your business’s true value, the next step involves calculating your historical cash flows and projecting future ones based on realistic market conditions.

Which Cash Flow Method Works Best for Your Business

Free Cash Flow to Firm: The Foundation for Comparing Different Capital Structures

The Free Cash Flow to Firm approach values your entire business by calculating cash available to all investors-debt holders and equity holders combined. This method starts with net operating profit after taxes, adds back non-cash expenses like depreciation and amortization, adjusts for working capital changes, and deducts capital expenditures. The resulting figure represents cash the business generates independent of its capital structure, making it ideal when you want to compare businesses with different debt levels.

For a manufacturing company with $2 million in annual EBIT and $300,000 in annual depreciation, you add that depreciation back since it’s a non-cash expense, then subtract the $150,000 spent on equipment upgrades. This approach works particularly well when you’re selling to a strategic buyer who may refinance your debt or when comparing your valuation across different financing scenarios. The strength of this method lies in its focus on operational cash generation rather than accounting profits, which can hide true cash availability through aggressive depreciation schedules or unusual one-time items.

The Dividend Discount Model for Mature, Stable Businesses

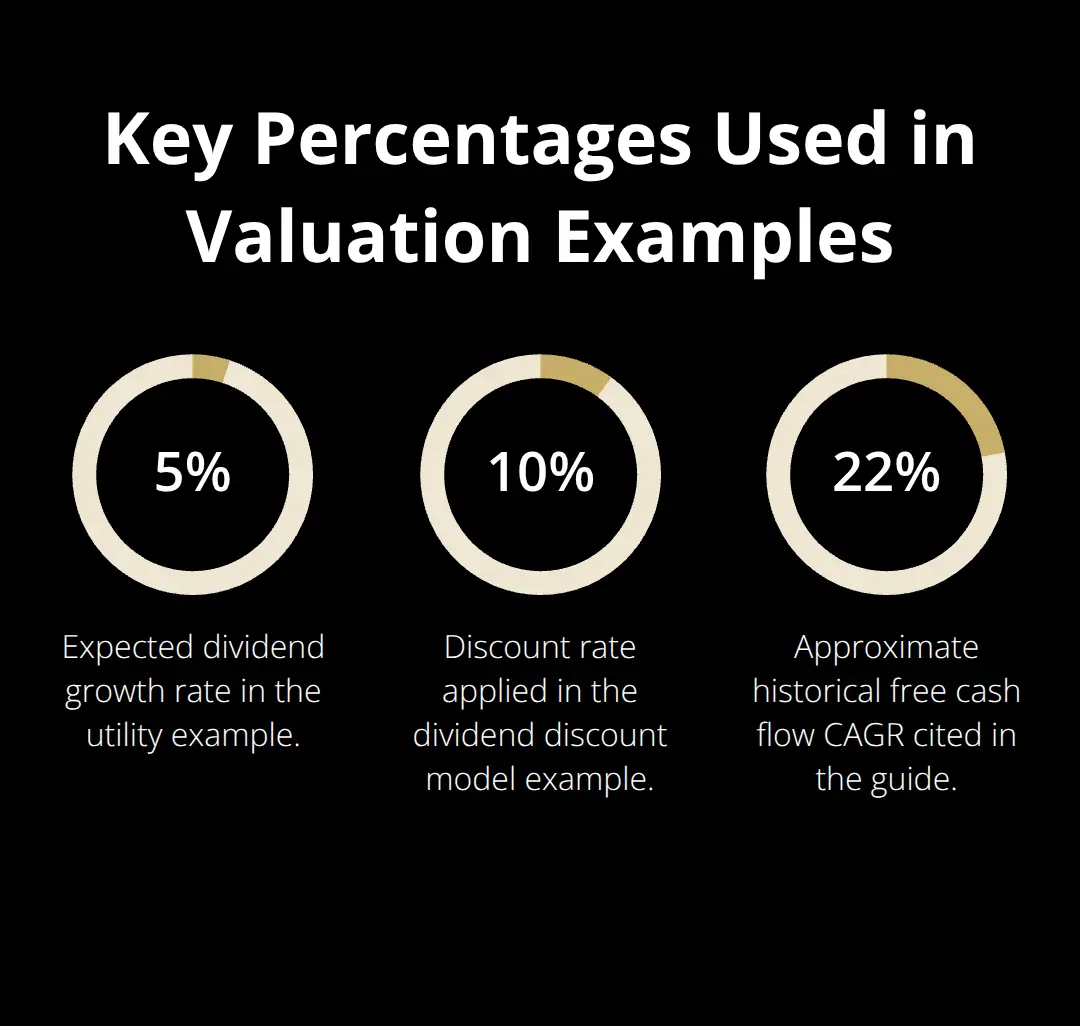

The Dividend Discount Model applies specifically to mature, profitable businesses that return cash to shareholders through consistent dividend payments. This method values a company based on the present value of expected future dividends, using the assumption that dividends reflect sustainable cash flows. A stable utility company paying $2 per share annually with a 5 percent expected growth rate and a 10 percent discount rate would be valued at approximately $42 per share using this formula.

This approach fails dramatically for high-growth companies or businesses that reinvest all profits rather than distribute them, making it unsuitable for startups or expansion-phase firms. You should only apply this method when your business has a long track record of stable, predictable dividend payments and operates in a mature industry with limited growth prospects.

Comparable Company Analysis: Benchmarking Against Similar Firms

Comparable Company Analysis uses cash flow multiples to benchmark your business against similar firms by comparing enterprise value to free cash flow, typically expressed as an EV/FCF multiple. If comparable businesses in your industry trade at 8 times free cash flow and your company generates $500,000 in annual free cash flow, your valuation would land near $4 million. This method requires finding truly comparable companies with similar growth rates, profitability, and risk profiles-a challenge for niche businesses or those with unique competitive advantages.

The critical limitation is that market multiples change rapidly; the 8x multiple from last year may compress to 6x this year if interest rates rise or investor sentiment shifts toward different sectors. You must update these multiples quarterly rather than relying on stale benchmarks from industry reports published twelve months ago. A divergence between your valuation using comparable multiples and your valuation using discounted cash flow signals that either your discount rate assumptions need adjustment or the comparable companies don’t truly match your business profile.

Now that you understand which method fits your situation, the next step involves calculating your historical cash flows and projecting future ones based on realistic market conditions.

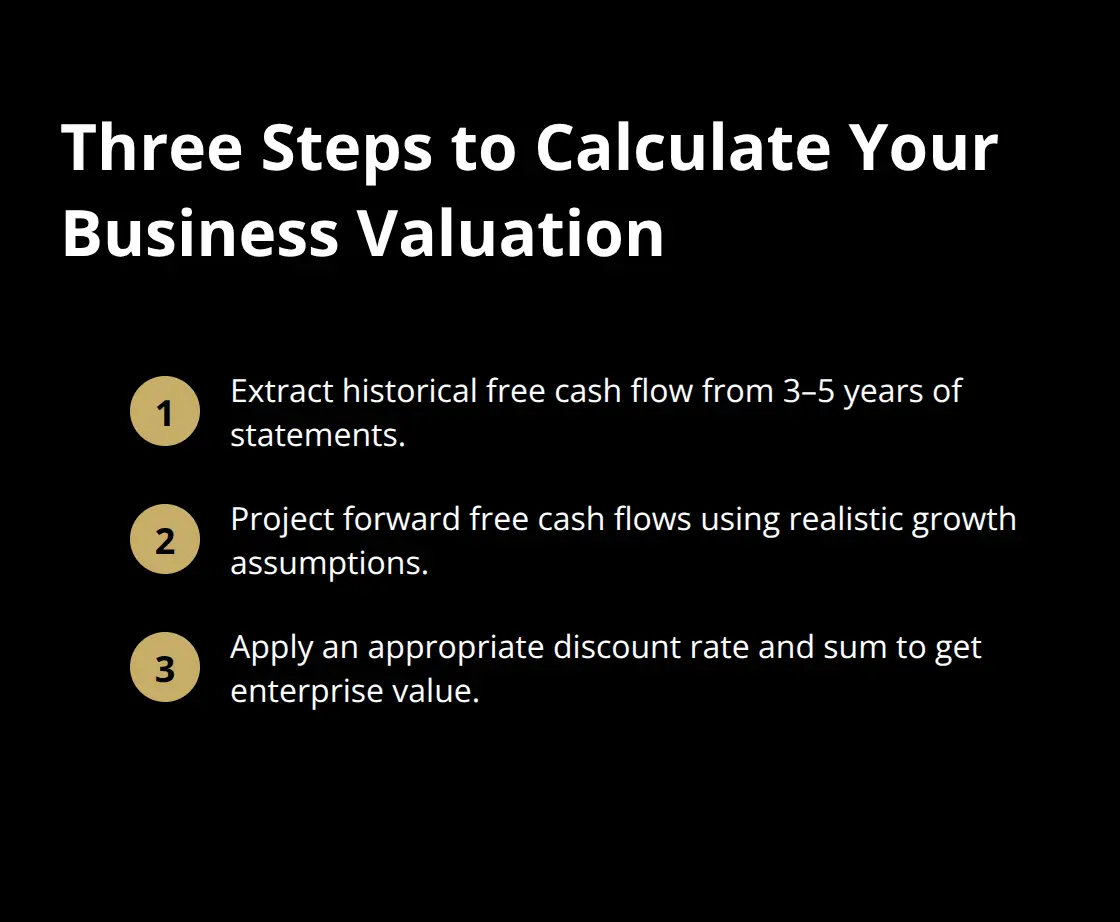

How to Calculate Your Business Valuation in Three Steps

Extract Historical Cash Flows from Your Financial Statements

Start by pulling your actual cash flows from the past three to five years of financial statements. Take your cash flow statement and calculate free cash flow for each year: cash from operations minus capital expenditures, adjusted for any unusual one-time items that won’t repeat. Most business owners make the mistake of using net income instead, which inflates value through accounting tricks like aggressive depreciation or deferred revenue recognition. If your business generated $600,000 in operating cash flow last year but spent $150,000 on equipment, your free cash flow was $450,000-not the $520,000 net income your accountant reported.

Once you have three to five years of historical free cash flow, calculate your average growth rate. If free cash flow grew from $300,000 to $450,000 over three years, your compound annual growth rate reached approximately 22 percent. This historical rate serves as your baseline, though you’ll adjust it downward for future projections because most businesses can’t sustain their early growth rates indefinitely.

Project Forward Cash Flows with Realistic Market Assumptions

Projecting forward requires honest assessment of market conditions, not wishful thinking. A manufacturing business with 22 percent historical growth won’t maintain that rate if the industry is consolidating or customer concentration is rising. Try using a conservative forward growth rate of 3–6 percent for mature businesses and 8–15 percent for growing firms with expanding market share. If your business serves a declining industry or faces new competition, reduce your projection further.

Once you’ve settled on a realistic forward growth rate, project your free cash flow five to ten years ahead using that rate. This projection forms the foundation for everything that follows in your valuation calculation.

Apply the Discount Rate to Convert Future Cash Flows to Present Value

Apply a discount rate to convert these future cash flows into today’s dollars, and this rate is where most valuations fail. A discount rate of 7–10 percent suits stable, established businesses with consistent cash flows and minimal competitive threats. Growing businesses or those with customer concentration risk should use 12–18 percent. Startup or highly volatile businesses warrant 20–25 percent or higher (the discount rate reflects both what you could earn in a risk-free investment and the additional return you demand for bearing business risk).

Once you multiply each year’s projected free cash flow by its discount factor and sum the results, you arrive at your enterprise value. This number represents what your business is truly worth based on profit streams, not revenue or asset values.

Final Thoughts

Cash flow valuation strips away accounting fiction and focuses on what actually matters: the money your business generates and retains. Revenue figures mislead, profit margins hide the truth, but free cash flow reveals whether your business can sustain itself, pay obligations, and fund growth. When you apply a realistic discount rate to your projected cash flows, you arrive at a valuation that reflects genuine economic value rather than wishful thinking or industry gossip.

Using this method when you sell your business gives you negotiating power because you walk into conversations with a defensible valuation based on documented cash flows, realistic growth assumptions, and transparent discount rate logic. Buyers respect this approach since they use the same framework internally, and when they propose a lower offer, you can point to specific cash flow projections and explain why your discount rate reflects your business’s actual risk profile. This clarity eliminates vague arguments about market conditions or comparable sales that may not actually be comparable.

Unbroker offers modern business sale services with low-cost options, no hidden fees, and access to a vast buyer network that helps you turn your valuation into an actual sale at the right price. Whether you choose full-service or assisted selling, you get premium marketing tools and negotiation support throughout the process.