Selling a business attracts tire-kickers and serious buyers alike. The difference between the two often costs you weeks of wasted time and thousands in legal fees.

At Unbroker, we’ve seen deals collapse because sellers didn’t vet buyers early enough. Using the right buyer vetting tools from day one separates genuine prospects from those who waste your time.

How to Identify Serious Buyers Early

Demand Proof of Funds First

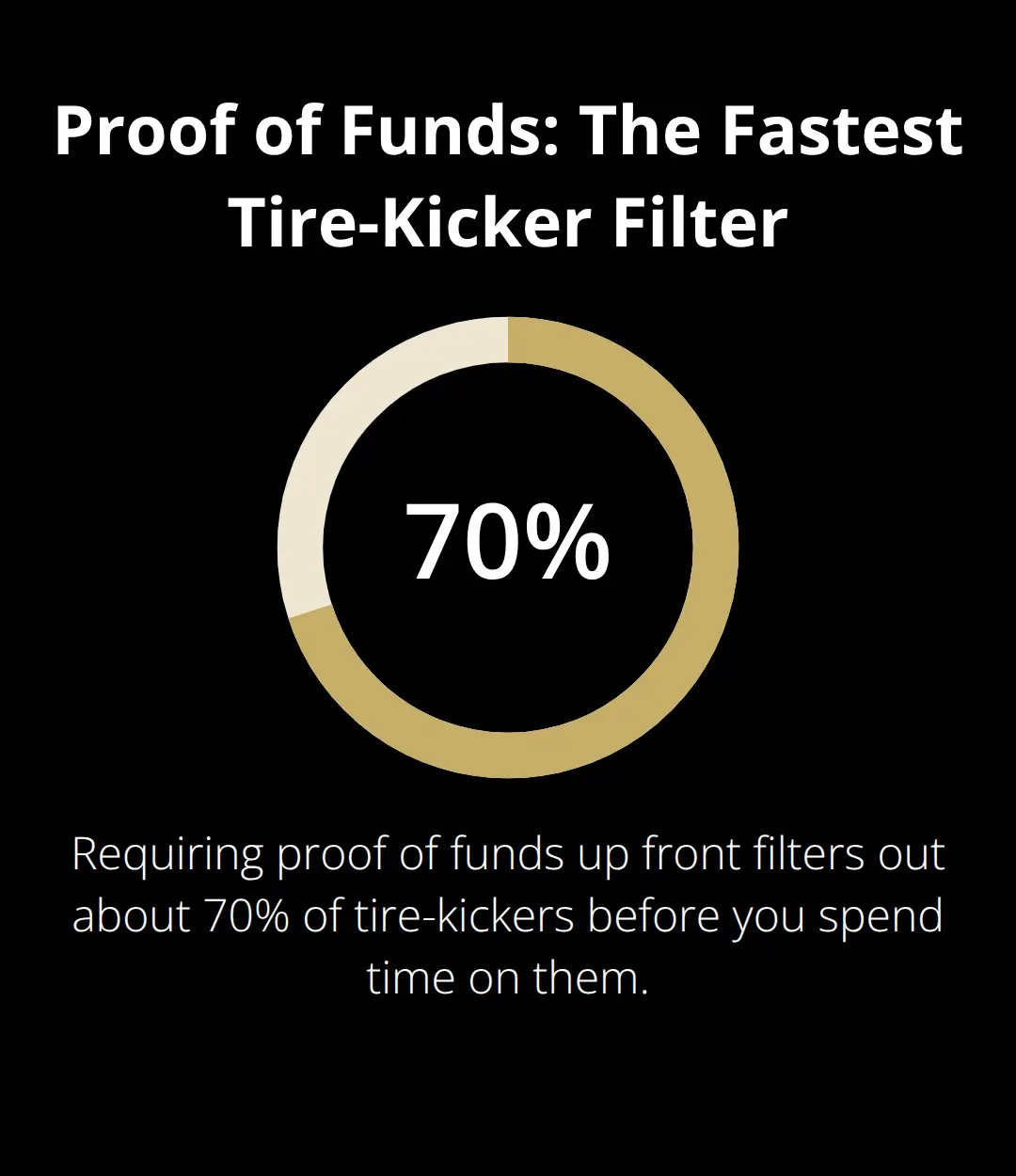

A serious buyer has cash or a pre-approval letter ready before your first conversation ends. This is non-negotiable. Bank statements or a formal pre-approval letter from a lender separates genuine prospects from dreamers. If a buyer hesitates or delays providing this documentation, treat it as a disqualifying signal and move on. Deals stall for months when sellers accept vague promises instead of cold financial proof. Require the buyer to submit to a credit check and provide bank statements or pre-approval upfront, not after weeks of negotiation. This single step eliminates roughly 70 percent of tire-kickers before you invest time in them.

Ask About Past Acquisitions and Deal Patterns

In your first qualifying call, ask specific questions about previous business purchases: How many businesses have they bought? How long did those deals take? Can they reference their lender or attorney? Serious buyers answer these questions directly and often volunteer details about their timeline, motivation, and deal structure. They discuss payment terms, deposit amounts, and how funds will transfer. They ask about title type, legal compliance, and due diligence steps. Vague answers, shifting preferences, or reluctance to discuss past deals signal low commitment.

Watch Communication Behavior and Third-Party Involvement

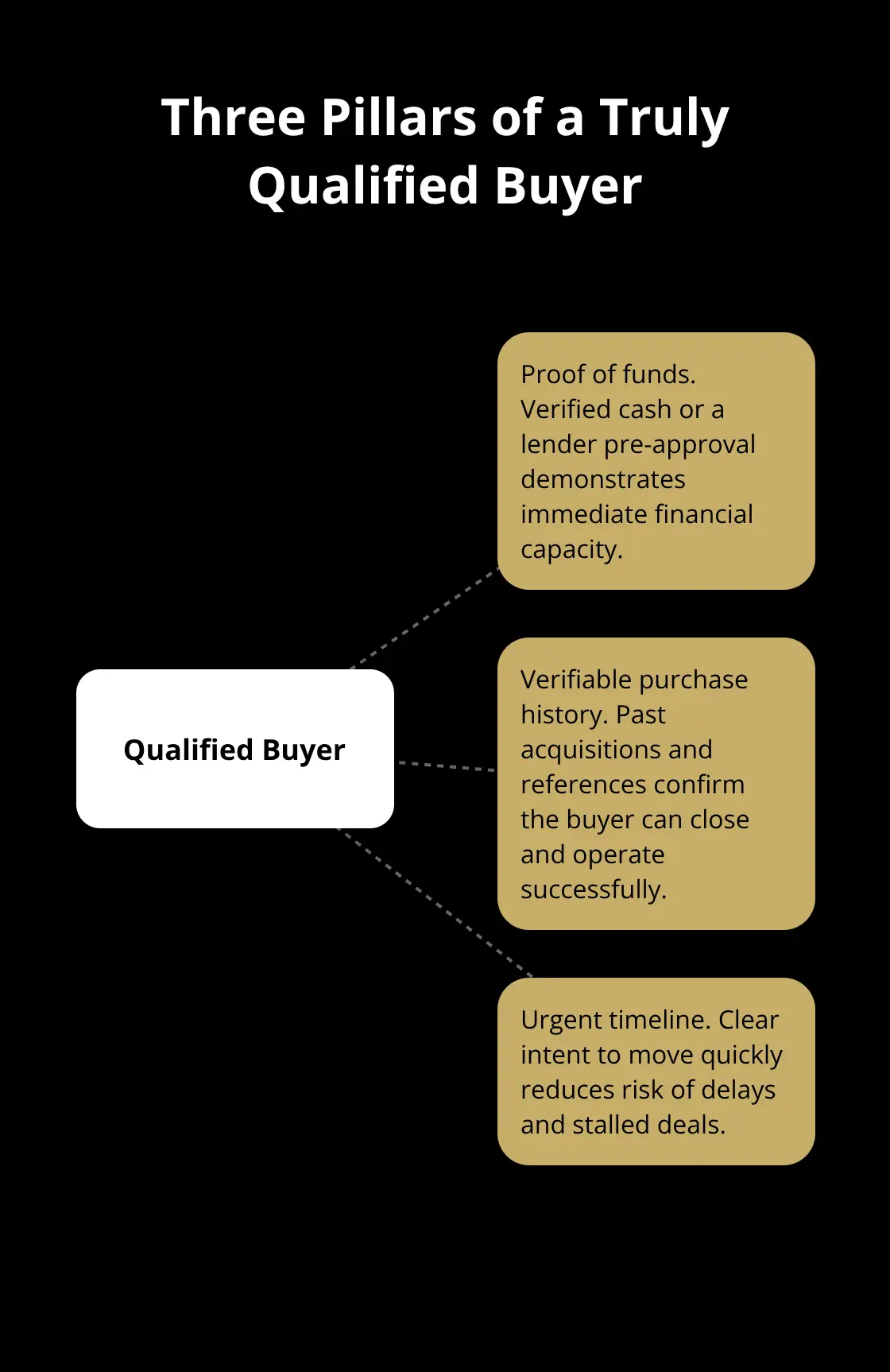

Communication cadence reveals intent faster than words alone. Genuine prospects reply within 24 hours, schedule site visits without cancellations, and involve third parties like spouses, lawyers, or accountants early. Someone who goes silent for days, reschedules repeatedly, or avoids bringing advisors is not ready to close. Background screeners, employers and lenders can verify employment and income data, confirming they can handle the financial obligation. A truly qualified buyer combines proof of funds, verifiable purchase history, and urgent timeline-all three pillars matter. If you see only one or two, the buyer likely lacks the commitment to move forward quickly. The next section covers the tools and strategies that automate this screening process and help you scale your vetting without losing accuracy.

Tools That Actually Separate Serious Buyers From Pretenders

Run Background Checks Before Your First Call

Employment verification, credit history, and past business affiliations tell you whether this buyer has closed deals before or is shopping for their first acquisition. Contact employers directly, verify titles through Chamber of Commerce databases, and pull credit reports from Equifax or Experian with the buyer’s consent. A buyer who refuses background verification signals that something doesn’t add up. Tax returns and bank statements should align with stated assets and income. If a buyer claims $500,000 in liquid capital but their bank statement shows $50,000, you’ve caught a lie before signing anything. This step takes 48 hours and saves you weeks of wasted negotiation with someone who can’t actually close. Inconsistent employment dates, acquisition timelines, or funding sources warrant deeper investigation before you proceed.

Create a Standardized Proof-of-Funds Checklist

Treat proof of funds as a gating requirement, not a suggestion. Bank statements covering the past 60 days that clearly show available liquid funds matching the claimed purchase price work best. A pre-approval letter from a reputable lender stating creditworthiness, income, and debt-to-income ratio is equally valid. This isn’t paperwork theater-it’s the difference between a buyer who closes in 30 days and one who disappears in month three. Many sellers skip this because they fear losing a prospect, but that fear costs thousands in legal fees and lost time. When you impose financial gatekeeping early, you attract only buyers serious enough to gather documents upfront. Serious prospects understand that vetting protects the deal’s integrity and accelerates closing.

Design Your Initial Qualifying Call to Test Real Commitment

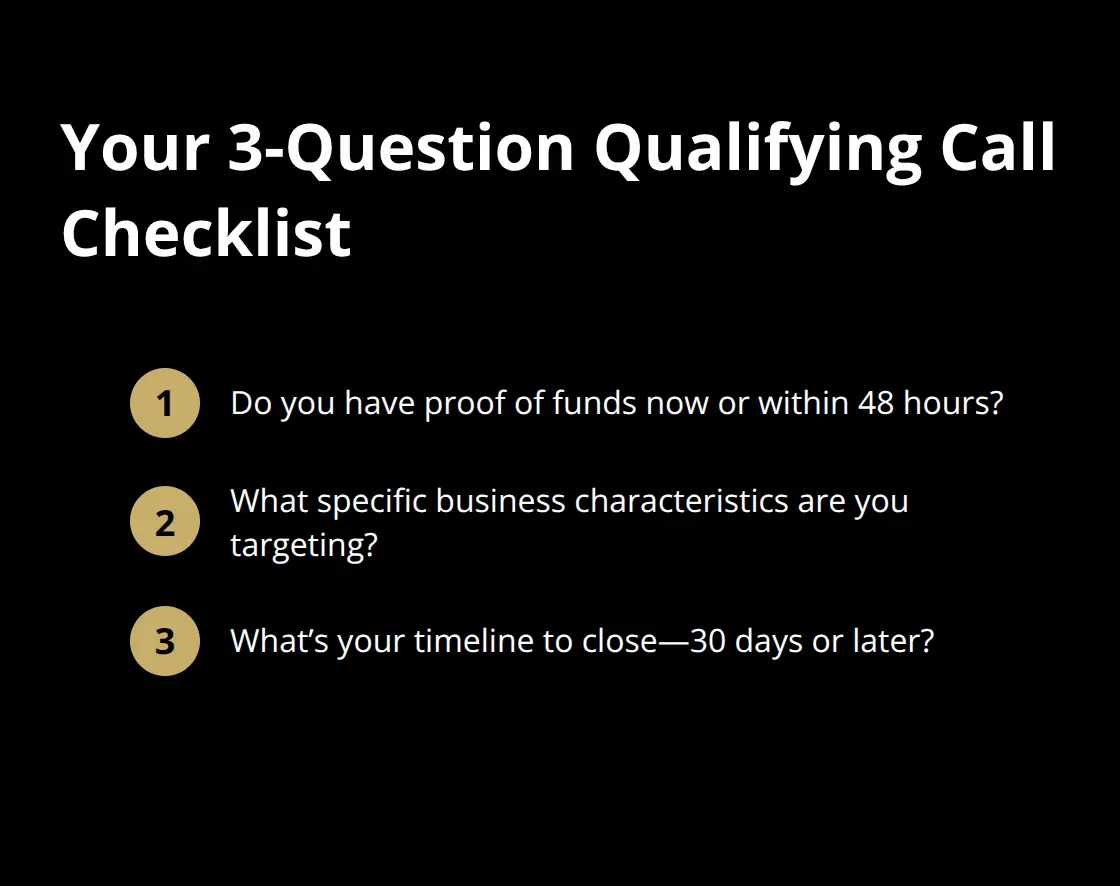

Ask three things in your first conversation and listen carefully to how the buyer answers. First, do they have proof of funds ready or can they obtain it within 48 hours? Second, what specific business characteristics are they seeking, and can they articulate them with precision? Third, what drives their timeline-are they closing in 30 days or “sometime next year”?

Vague responses signal low intent. A serious buyer answers all three directly and often volunteers additional detail about their financing structure, past acquisitions, and how they plan to operate the business post-purchase. They ask about legal compliance, title documentation, and due diligence steps. They mention involving a lawyer or accountant. Buyers who dodge these questions, claim urgency without proof of funds, or shift their criteria mid-call waste your time. Document every call and track which buyers advance through your qualification gates. Over time, you’ll see patterns in who actually closes versus who fades away.

The buyers who pass these three screening layers move into your active pipeline. The next chapter covers the red flags that should disqualify a prospect immediately, protecting you from deals that collapse mid-process.

Red Flags That Disqualify a Buyer Immediately

Unrealistic Offers Reveal Desperation Tactics

A buyer who low-balls your asking price by a significant margin on the first offer isn’t negotiating-they’re testing whether you’re desperate. Serious buyers research market comparables and make reasonable opening offers within 10 to 15 percent of asking price. They reference local data or recent sales to justify their number.

A buyer who claims your business is worth half what you’re asking but can’t cite a single comparable deal or market report is either uninformed or trying to manipulate you into panic-selling. Walk away. Similarly, a buyer who keeps shifting their negotiation position-first they want seller financing, then they demand a 90-day earnout, then they want you to stay on for two years-signals they lack a clear strategy or decision-making authority.

Each new demand wastes weeks and suggests they haven’t thought through their acquisition plan. Realistic negotiators make one or two reasonable counteroffers and then either commit or move on. If someone keeps changing terms after you’ve already made concessions, they’re stalling or testing your resolve, not closing.

Missing Financial Documentation Signals Trouble

A buyer who dodges your requests for financial documentation is disqualifying. You ask for a bank statement; they offer a vague promise to provide one next week. You request a pre-approval letter; they claim their lender is reviewing it but never follow up. You ask for a credit check; they refuse on privacy grounds.

These aren’t reasonable objections-they’re disqualifying signals. A genuinely qualified buyer understands that proof of funds accelerates the deal and removes doubt. Someone who resists this step either lacks the money or has something to hide. The moment a buyer avoids financial transparency, treat them as unqualified and redirect your energy toward prospects who meet your standards.

Vague Business Experience Reveals Fabricated Track Records

When you ask how many businesses they’ve purchased, a serious buyer gives you a number and names or details about those deals. They discuss what went well, what they’d do differently, and how they plan to run your business. A buyer who gives vague answers like “I’ve done a few deals” or “I’ve been in business a long time” without specifics is either lying about their track record or hasn’t actually closed a significant acquisition.

Verify their claims directly with past sellers, their accountant, or their lender. If they refuse to provide references or claim confidentiality prevents them from naming past deals, that’s a red flag worth acting on. Trust your instinct-if something feels off about their story, it probably is. Buyers with legitimate experience welcome verification because it proves their credibility and strengthens their position in negotiations.

Final Thoughts

Vetting buyers early eliminates months of wasted negotiation with prospects who can’t actually close. The three screening layers covered in this post-proof of funds, purchase history verification, and communication patterns-filter out roughly 70 percent of tire-kickers before you invest significant time. A single disqualifying red flag, whether missing financial documentation or vague business experience, saves you from deals that collapse mid-process and cost thousands in legal fees.

Serious buyers move faster, negotiate in good faith, and close on schedule. When you implement a standardized vetting process using buyer vetting tools and direct verification methods, you attract only prospects with genuine intent and financial capacity. This shifts your energy from chasing unqualified leads to closing deals with buyers who are ready to move.

Start by creating a proof-of-funds checklist and a qualifying call script that tests commitment on three fronts: financial readiness, specific acquisition criteria, and timeline urgency. If you’re selling a business and want expert guidance through the vetting and negotiation process, we at Unbroker offer the Assisted Business Sale service, which provides negotiation support and sale-timeline guidance with a satisfaction guarantee.