Sellers waste thousands of dollars every year chasing leads that never convert. At Unbroker, we’ve seen firsthand how the wrong buyer qualification platform can drain your pipeline and your budget.

A buyer qualification platform filters out tire-kickers before they waste your time. The right system separates serious buyers from those who aren’t ready to move forward.

Why Qualification Filters Save Money and Time

Unqualified leads cost real money. According to ATTOM Data Solutions, 66 percent of home buyers need mortgage financing, which means one-third of your lead pool likely lacks pre-approval or financial readiness. Without proper screening, agents spend hours showing properties to buyers who can’t actually qualify for a loan. That’s not just wasted showings-it’s lost opportunity cost.

A buyer without pre-approval creates friction at every stage: inspections get ordered, appraisals get scheduled, and offers get made, only for the lender to reject them weeks later. Filtering happens upfront or it happens expensively downstream.

Pre-Approval Separates Real Buyers from Window Shoppers

The simplest filter is a pre-approval letter. A qualified buyer has already spoken to a lender, provided documentation, and received written confirmation of their borrowing capacity. That means nearly one-third of your incoming leads face genuine barriers to mortgage approval. Ask early whether a buyer has pre-approval. If they haven’t, connect them to a lender for a quick consultation before you schedule a single showing. This isn’t about being rude-it’s about respecting everyone’s time. A buyer who completes pre-approval moves from prospect to qualified buyer, and your conversion rate jumps dramatically.

Speed Kills Uncertainty in the Sales Cycle

Qualification platforms automate this vetting in real time. Instead of manually phone-calling leads to ask about finances, a platform captures essential details upfront through screening questions. Real-time notifications alert you when a buyer’s profile matches your listings, and automated follow-ups keep prospects engaged without manual effort. The result is faster pipeline movement and lower administrative burden. Buyers appreciate it too-24/7 availability means they don’t wait for an agent to call back. Instant property matching reduces overwhelm by sending curated suggestions rather than dumping the entire MLS feed on someone. When a serious buyer enters the system, your team knows it immediately and can focus energy where it counts.

What Happens When You Skip Qualification

Poor qualification wastes weeks and compounds costs. Without upfront vetting, agents show homes to buyers who lack financing, motivation, or urgency. Each unqualified showing consumes time that could go toward serious prospects. The lender eventually discovers issues that should have surfaced in the first conversation. Appraisals fail, inspections reveal problems, and offers collapse because the buyer never had real capacity to close. These downstream failures cost far more than a five-minute pre-approval conversation would have cost upfront. When you control the timeline and filter which buyers you interact with, you avoid becoming a passenger in your own sales process.

The next step is identifying which platform features actually deliver this efficiency.

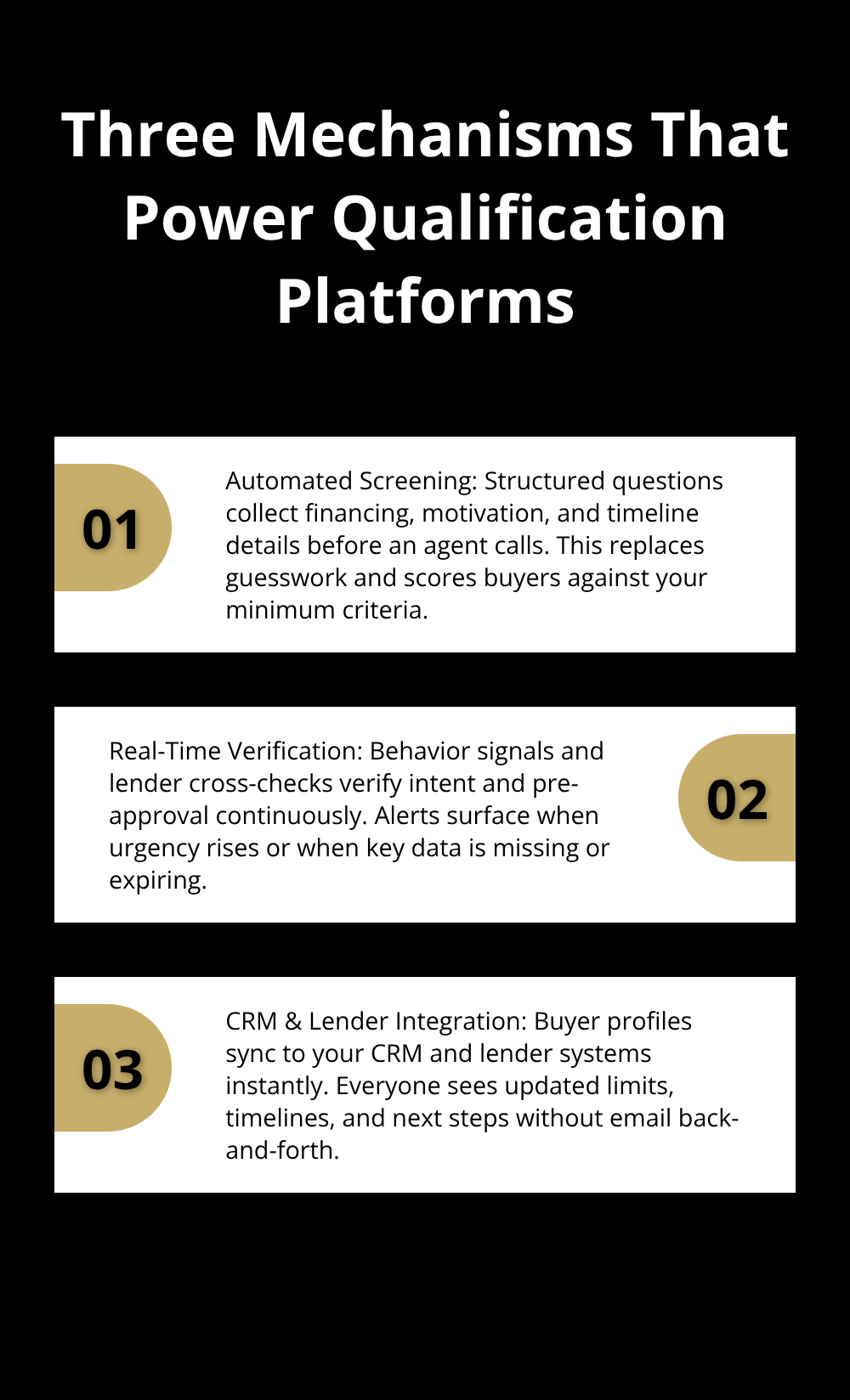

How Buyer Qualification Platforms Work Behind the Scenes

A buyer qualification platform operates through three interconnected mechanisms that work together to filter serious buyers from tire-kickers. First, the system captures buyer information through structured screening questions early in the interaction. Instead of relying on agents to manually probe finances, motivation, and timeline, the platform asks specific questions upfront: Have you been pre-approved? What’s your budget? When do you need to move?

These responses populate a buyer profile that the platform uses to score readiness. According to real estate data, 66 percent of buyers need mortgage financing, so asking about pre-approval status immediately segments your pipeline into two groups-those with lending confirmation and those without. The platform doesn’t judge; it simply surfaces the difference so agents can triage accordingly.

Automated Screening Captures What Manual Calls Miss

Structured screening questions replace phone tag and guesswork. When a buyer enters the platform, they answer targeted questions about financial readiness, motivation, and timeline before an agent ever picks up the phone. This upfront data collection accomplishes two things: it qualifies the buyer instantly, and it gives agents context before the first conversation. A buyer who has already stated their budget and pre-approval status arrives at a showing prepared, not defensive. The platform scores each response and flags buyers who meet your minimum criteria (pre-approval confirmed, realistic timeline, genuine motivation). Agents see this score immediately and know whether to prioritize the lead or nurture it for later. This eliminates the common mistake of treating all leads equally-a platform-qualified buyer receives different attention than a curious browser.

Real-Time Verification Replaces Manual Follow-Up

Real-time verification happens automatically once a buyer enters the system. The platform monitors buyer activity-property views, email opens, scheduling patterns-and flags when behavior signals serious intent or red flags. If a buyer goes silent for two weeks, an automated follow-up goes out without agent intervention. If a buyer schedules multiple showings in a single day, your team receives an alert to prioritize that lead. The platform also validates pre-approval status by cross-referencing lender information when the buyer provides it, reducing the risk of fake or outdated approvals. This continuous verification means you never chase ghosts; you always work with current, verified data. Agents spend time on buyers whose profiles match their current inventory and motivation level, not on prospects who disappeared weeks ago or never qualified in the first place.

Integration Keeps Lenders and Agents Aligned

The most powerful feature is integration with your existing CRM and lender networks. When a buyer profile is created in the qualification platform, that data flows directly into your CRM so nothing falls through the cracks. Lenders can access qualified leads instantly and provide real-time pre-approval updates back into the system. If a lender approves a buyer for $350,000, that information syncs immediately, and agents see it without manual email chains. This eliminates the common scenario where an agent shows homes outside the buyer’s actual range or wastes time on contingencies the lender already rejected. Modern platforms also include automated assignment workflows, meaning a newly qualified buyer routes to the right agent based on geography, availability, or specialization. The collaboration between lender and agent becomes visible and tracked, so both parties know the buyer’s status at every stage and can coordinate showings and document collection efficiently.

Understanding how these mechanisms work together sets the stage for identifying which specific features actually move qualified buyers through your pipeline faster.

What Platform Features Actually Filter Qualified Buyers

The difference between a mediocre qualification platform and an effective one comes down to three specific capabilities that work together to separate serious buyers from noise. First, the platform must filter based on concrete financial data, not just buyer intent. A platform that asks whether someone has pre-approval but doesn’t verify it against actual lender records is guessing. The best platforms cross-reference pre-approval claims with lender databases or require buyers to upload documentation upfront. This matters because roughly 16 percent of Americans have serious credit delinquencies according to FICO, meaning many leads will claim readiness without actual proof.

Second, the platform needs to surface buyer information in a format agents can act on immediately. This means showing pre-approval amounts, down payment sources, debt-to-income ratios, and timeline certainty in a single dashboard view rather than burying details in email threads or scattered notes. Third, the platform should match buyers to inventory based on what they can actually afford and what genuinely interests them, not just what’s listed. AI-driven matching learns from buyer behavior-properties viewed, time spent on listings, filter adjustments-and refines recommendations over time. These algorithms improve accuracy as they gather more data, meaning early matches are rough but later suggestions become highly personalized.

Filtering That Stops Wasted Showings Before They Start

A platform without robust filtering is just a lead capture tool. Real filtering requires the platform to establish minimum qualification thresholds and enforce them automatically. Set your thresholds clearly: pre-approval confirmed yes or no, timeline within 90 days or longer, debt-to-income ratio below 43 percent. When a buyer’s profile fails to meet these thresholds, the platform routes them to a nurture sequence rather than assigning them to an agent for immediate showing. This is where most platforms fail-they treat all leads as urgent when only a fraction actually qualify. The platform should also filter for motivation signals beyond finances. A buyer who schedules three property viewings in one week and opens every property alert shows urgency. A buyer who browses sporadically over six months shows curiosity, not commitment. Platforms that track engagement patterns and surface motivation indicators help agents focus on buyers exhibiting active intent. Some platforms allow you to customize screening questions to match your specific market and buyer profile, which means you control what data triggers a qualified buyer flag. If your market demands 20 percent down payments, a platform that flags pre-approval without verifying down payment source wastes everyone’s time. The filtering must be specific to your business, not generic.

Buyer Information That Agents Can Act On Immediately

Transparency in buyer information means agents see everything they need to make decisions without hunting through attachments or old emails. When a buyer enters the system, their profile should display pre-approval amount, lender contact information, down payment confirmation, timeline, and motivation summary in one view. Some platforms surface red flags-a buyer whose pre-approval expires in 30 days, or a buyer whose debt-to-income ratio leaves minimal room for the new mortgage payment. These alerts prevent agents from spending weeks on a buyer who falls out of qualification mid-process. The platform should also log all buyer interactions in one place, so when an agent picks up the conversation, they know what questions have already been answered and what concerns the buyer raised. This eliminates the frustration of asking a buyer about their timeline twice or forgetting they mentioned a job relocation. Transparency also means showing agents the source of buyer data-whether pre-approval came directly from the lender, whether it was self-reported, or whether it’s pending verification. This context matters because a lender-verified pre-approval carries different weight than a buyer’s claim. Platforms that integrate directly with lender systems provide the highest confidence data, while platforms that rely on buyer self-reporting require follow-up verification.

AI-Driven Matching That Learns Buyer Preferences

AI-driven matching transforms how platforms connect buyers to properties. The system tracks which listings buyers view, how long they spend on each property, and which filters they adjust repeatedly. Over time, the algorithm identifies patterns in buyer behavior and surfaces properties that match those preferences before the buyer even asks. A buyer who consistently views homes in a specific neighborhood with three bedrooms and a garage receives recommendations aligned with that pattern, not random MLS listings. The platform becomes smarter with each interaction, meaning recommendations improve as the buyer spends more time in the system. This personalization reduces overwhelm-buyers see curated suggestions instead of hundreds of irrelevant options. Agents benefit too because they understand what genuinely interests each buyer and can have more productive conversations about property fit. The most effective platforms combine AI matching with human oversight, allowing agents to adjust recommendations when they spot patterns the algorithm missed or when market conditions shift rapidly.

Final Thoughts

A buyer qualification platform transforms how you compete by filtering qualified prospects upfront and eliminating the downstream costs that drain most real estate operations. When your lender and agent teams stay aligned through integrated systems, appraisal failures and financing surprises drop dramatically, and buyers move through your process faster because everyone has the same information at the same time. That speed translates directly to revenue, and the ROI compounds quickly-a single avoided showing on an unqualified buyer saves two hours of agent time, which multiplies across your team into hundreds of recovered hours annually.

Start by auditing your current process to identify where a buyer qualification platform creates immediate value. Ask yourself how many showings end without an offer, how many offers collapse due to financing issues that should have surfaced earlier, and how many leads go silent because follow-up happens manually instead of automatically. Look for platforms that verify pre-approval directly with lenders rather than accepting buyer claims, demand integration with your CRM so data flows seamlessly between agents and lenders, and test AI-driven matching to see whether personalized recommendations increase buyer engagement compared to generic MLS feeds.

Define your minimum qualification thresholds, then find a platform that enforces them automatically through structured screening and real-time verification. At Unbroker, we understand that efficiency and transparency drive results-whether you’re selling homes or businesses, the principle remains the same: filter for qualified prospects, eliminate friction, and close faster.