Selling a business requires more than just listing it and hoping for buyers. At Unbroker, we know that DIY sale preparation separates successful exits from frustrating ones.

The difference comes down to documentation. Buyers want proof that your business is organized, profitable, and worth their investment.

This checklist walks you through the financial records, operational systems, and physical assets you need to gather before listing.

What Financial Records Do Buyers Actually Need?

The Three Areas Buyers Scrutinize

Buyers examine three areas when evaluating a business: how much money came in, how much went out, and what legal commitments exist. Your tax returns and profit and loss statements form the foundation of this conversation. Provide the last three to five years of filed tax returns alongside corresponding P&L statements. Buyers compare these documents to spot inconsistencies or red flags. If your P&L shows $500,000 in revenue but your tax return shows $400,000, that gap demands explanation.

Many business owners underreport revenue intentionally or unintentionally, which destroys buyer confidence immediately.

Verify Revenue Through Bank Statements

Your bank statements back up your financial claims. Pull 24 to 36 months of statements from every business account. Buyers trace cash flows through these statements to verify that revenue figures are real and that major expenses align with what you claimed. If you claim consistent monthly revenue but the statements show sporadic deposits, the story collapses. Organize these statements chronologically and flag any unusual transactions before showing them to buyers.

Contracts and Legal Agreements Shape Business Value

Contracts and legal agreements represent liabilities and opportunities. Gather employment agreements, vendor contracts, lease agreements, customer contracts, and any litigation history. A long-term customer contract worth $200,000 annually increases business value significantly. Conversely, a lease with five years remaining and escalating costs reduces it. Buyers need to see what obligations transfer to them and what revenue is locked in. Missing contracts or vague terms create uncertainty, and uncertain buyers walk away or demand discounts.

Organize Everything Professionally

Create a master document index listing every file, the date it covers, and where to find it. Use cloud storage like Google Drive or Dropbox rather than scattered email attachments or external hard drives. Buyers expect professional presentation, not a shoebox of receipts. If you’ve run your business informally without separating personal and business finances, now is the time to clean this up. Pull all business transactions for the past three years and categorize them properly. This takes time but prevents buyers from questioning your financial integrity.

Consider having an accountant review your P&L statements against tax returns to identify any discrepancies before listing. The cost of a few hours of accounting time is negligible compared to losing a buyer over unexplained numbers. If your business has seasonal revenue, prepare a narrative explaining these patterns. Buyers in your industry understand seasonality, but they need to see you understand it too. Document any one-time expenses that won’t recur post-sale (such as emergency equipment repairs or litigation costs). This context prevents buyers from assuming your normal operating expenses are higher than they actually are.

Move Forward to Operational Documentation

Your financial records tell buyers what your business earned. Now they want to see how you earned it. The systems, processes, and people behind those numbers determine whether a buyer can actually run the business after taking over.

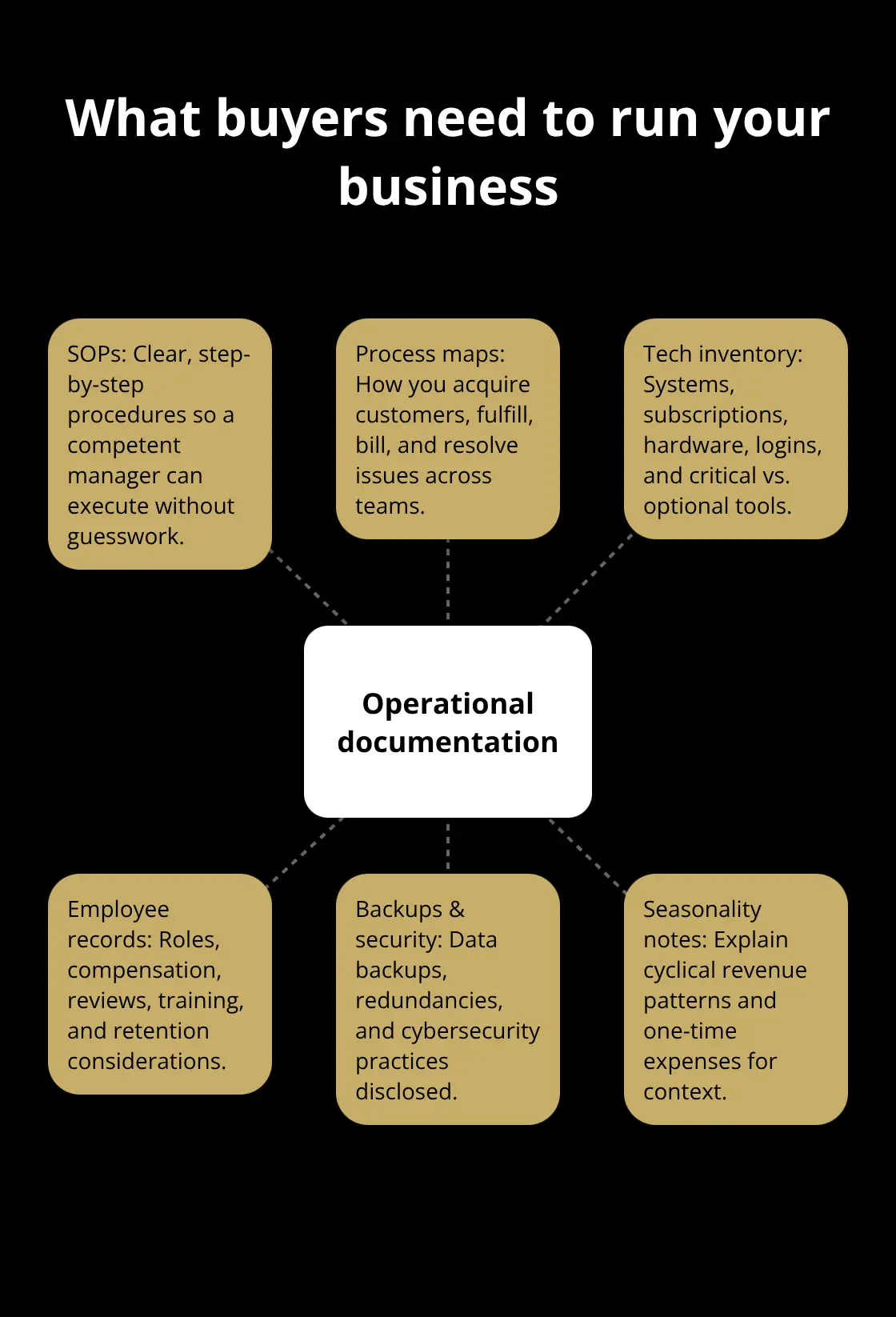

How to Document Operations So Buyers Actually Trust Your Business

Buyers want more than proof that your business made money. They want to understand exactly how it makes money and whether they can run it without you.

This means documenting your standard operating procedures, technology systems, and employee structure with enough detail that a competent manager could step in tomorrow.

Map Out Your Core Business Processes

Start by identifying your core business processes: how you acquire customers, deliver your product or service, handle billing, manage inventory, and resolve problems. Write these down step by step. If your process lives only in your head, it dies when you leave. Document each procedure in a single document or shared folder with clear titles, screenshots where relevant, and decision points.

For example, if your customer onboarding takes five steps, show exactly what happens at each step, who does it, how long it takes, and what tools are involved. Buyers scrutinize this because they’re calculating whether they need to hire additional staff or whether your existing team can handle the workload. If your processes are chaotic or undocumented, they’ll assume the worst and offer less.

Inventory Your Technology Infrastructure

Your technology infrastructure directly impacts business continuity and valuation. Create a complete technology infrastructure inventory of all software subscriptions, cloud services, hardware, and security systems your business uses. Store login credentials securely in a password manager like 1Password or Bitwarden. Document which tools are critical to daily operations and which are optional.

Include information about data backups, cybersecurity measures, and any integrations between systems. Buyers want to know whether your customer data is backed up, whether you have redundancy if a key system fails, and what happens to proprietary data after the sale. If you’re running on outdated or unsupported software, disclose it now rather than letting buyers discover it during due diligence.

Organize Your Employee Records and Retention Strategy

Gather your employee records, including job descriptions, compensation details, performance reviews, and any training documentation. Disclose your turnover rate and reasons employees have left. Buyers assess whether key employees will stay post-acquisition and what retention costs they’ll face.

If three of your five employees have left in the past year, that’s a red flag you need to address. Provide evidence that your remaining team is stable and that critical knowledge isn’t concentrated in one or two people. This operational transparency removes doubt and positions your business as professionally managed.

Present Your Documentation Professionally

Organize all operational documentation in a centralized location (cloud storage like Google Drive or Dropbox works well). Create a master index that lists every file, what it covers, and where to find it. Buyers expect professional presentation, not scattered files across multiple platforms. If your business has evolved over time, include notes explaining how processes have changed and why current systems work better than previous ones.

Your operational documentation now shows buyers how your business actually functions. Organizing legal documents and operational records removes friction during the sale process and demonstrates that you’ve prepared professionally for this transition.

What Assets and Intellectual Property Drive Business Value

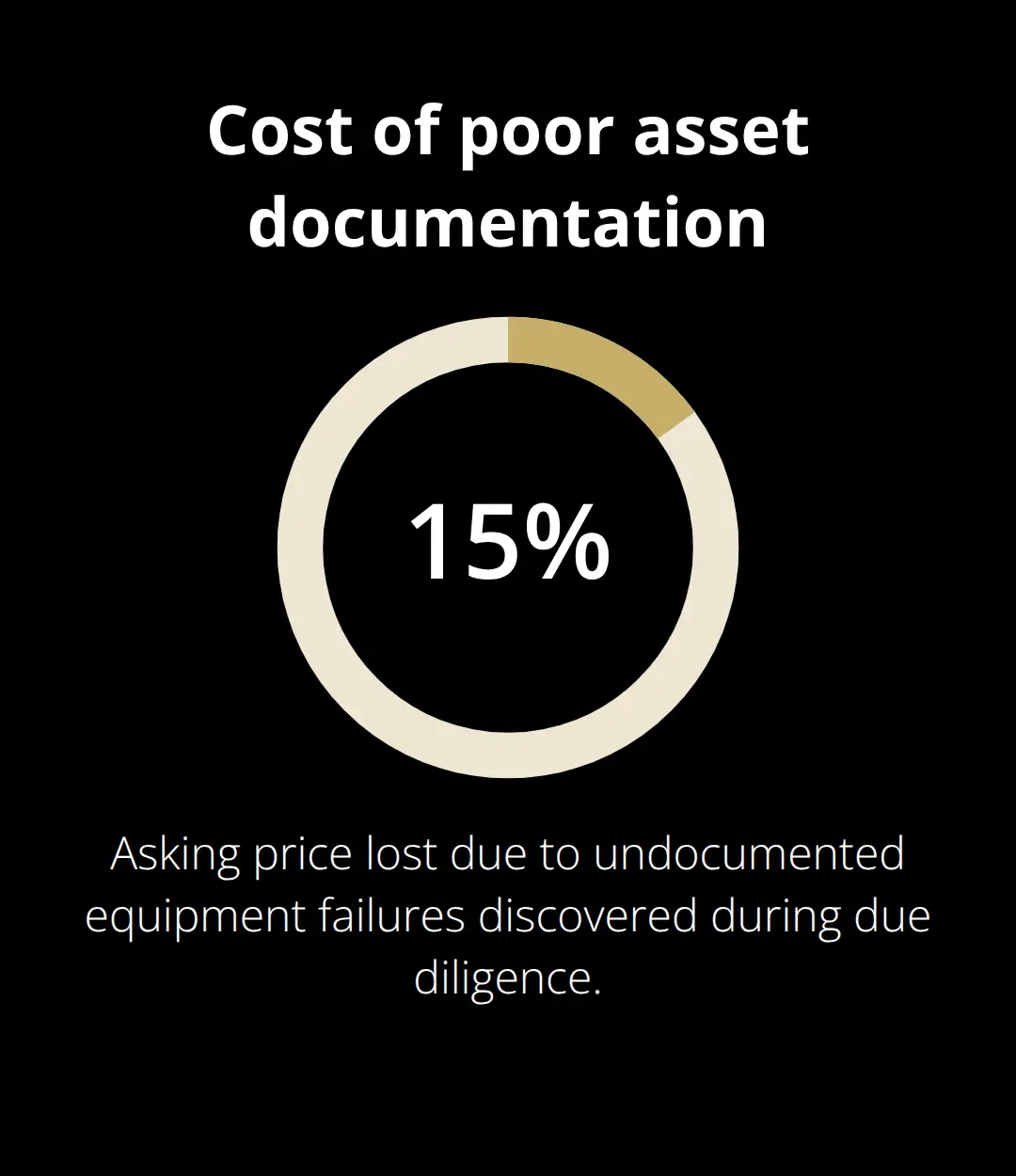

Buyers assess physical assets and intellectual property alongside your financial statements and operational systems. Equipment that breaks down six months after purchase becomes the new owner’s problem, which is why detailed asset documentation separates confident buyers from skeptical ones.

Document Equipment and Inventory Thoroughly

Create a complete equipment and inventory list that includes the purchase date, original cost, current condition, maintenance history, and replacement value for every item your business relies on. If you operate a service business with vehicles, list each one with mileage, service records, and any outstanding loans. If you manufacture products, inventory raw materials, work-in-progress items, and finished goods with current market values.

Buyers calculate whether they’re acquiring functional assets or inheriting expensive repairs. Missing or incomplete records force them to assume the worst and devalue your business accordingly. One manufacturing business lost 15 percent of its asking price because the buyer discovered undocumented equipment failures during due diligence that should have been disclosed upfront.

Assess Facility Condition and Lease Terms

Your facility itself matters equally. Document every maintenance record, repair receipt, and upgrade you’ve made over the past five years. Include information about HVAC systems, electrical panels, plumbing, roofing condition, and any structural work. Buyers assess whether the facility will support operations immediately or whether they’ll face unexpected capital expenses.

If your lease has renewal terms or escalation clauses, disclose these now. A lease that doubles in cost in two years significantly impacts the business valuation and buyer enthusiasm. Transparency about facility obligations removes surprises during the sale process.

Protect and Document Intellectual Property

Patents, trademarks, copyrights, proprietary software, customer lists, and trade secrets often represent your business’s most valuable components, yet many owners underestimate their importance during sale preparation. If your business holds patents, gather the patent numbers, filing dates, jurisdictions where they’re protected, and any licensing agreements. Trademark registrations should include the registered mark, classes of goods or services covered, and renewal dates.

Proprietary software or processes need clear documentation showing what makes them unique and how they generate competitive advantage. Customer lists with contact information, purchase history, and contract terms demonstrate recurring revenue potential. Many business owners store this information haphazardly across different locations and formats, which creates red flags during buyer evaluation.

Establish Clear Ownership and Consolidate Records

Organize intellectual property in a secure location with clear ownership documentation. If you’ve developed proprietary methods or software internally, document the development timeline and any employee involvement to establish clear ownership. Buyers want certainty that they’re acquiring assets free from disputes or third-party claims.

Missing or ambiguous intellectual property documentation can kill deals entirely because buyers refuse to assume legal risk. One software company lost a six-figure deal because it couldn’t prove ownership of its core algorithm after a former contractor raised claims. Consolidate all asset and intellectual property documentation in your centralized storage system alongside financial and operational records. Create a separate section clearly labeled with ownership certificates, maintenance records, and valuation assessments. This comprehensive asset inventory removes ambiguity and positions your business as thoroughly prepared for transition.

Final Thoughts

Your DIY sale preparation work removes the obstacles that slow down deals and reduce valuations. Buyers move faster when they access consistent financial records, clear operational documentation, and verified asset inventories without chasing you for missing information. They offer higher prices when they see a professionally managed business rather than one held together by knowledge that exists only in your head, and they close with confidence instead of walking away due to unanswered questions.

The documentation you’ve gathered also protects you after the sale closes. Clear records of your financial performance, operational systems, and asset condition prevent disputes with buyers who might later claim equipment wasn’t in the condition you represented. Your maintenance records and financial statements create an audit trail that proves exactly what you claimed during negotiations.

Your preparation work is complete, and now you’re ready to present this documentation to potential buyers in a way that builds confidence. We at Unbroker help business owners navigate this final stage with transparent, straightforward tools designed to connect you with serious buyers while eliminating unnecessary fees.