Selling a business is one of the biggest financial decisions you’ll make. Getting the valuation right determines whether you walk away satisfied or leave money on the table.

At Unbroker, we’ve seen sellers make costly mistakes by guessing at their business value instead of using data-driven methods. This guide walks you through the proven approaches to valuation for sellers, the factors that move your price up or down, and how to prepare your business to command top dollar.

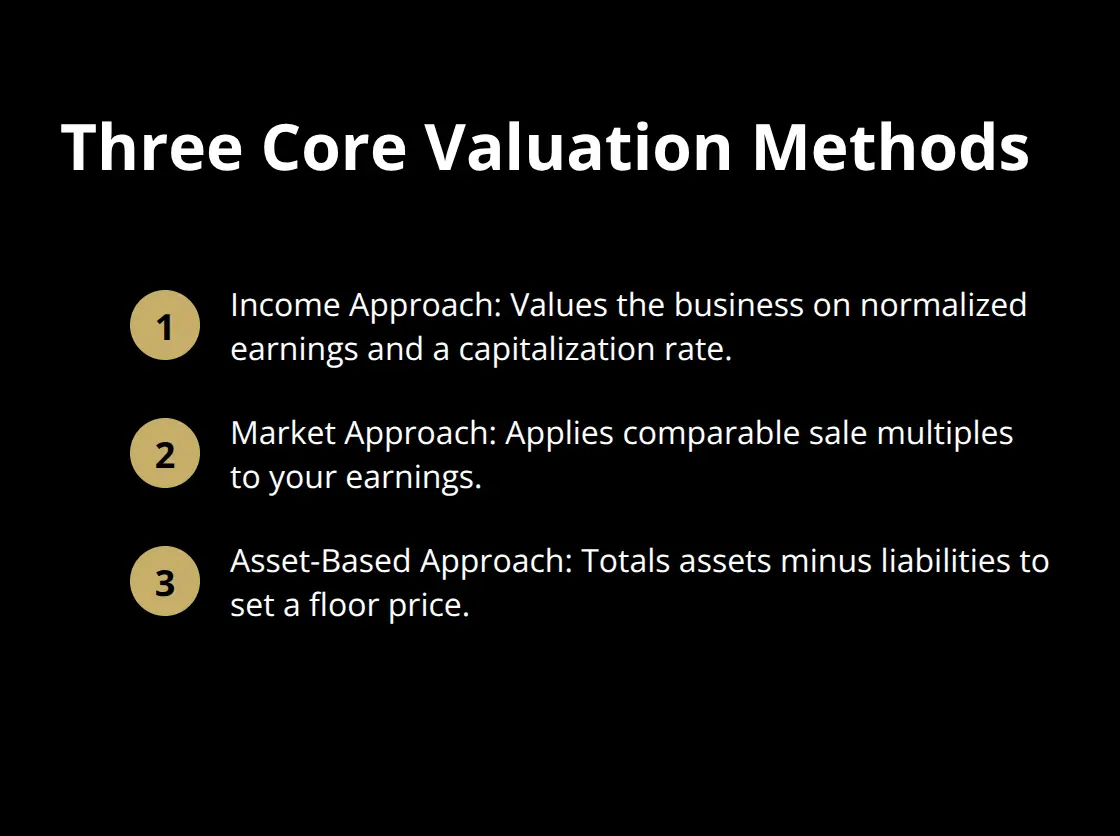

Understanding Business Valuation Methods

The Income Approach: What Your Business Earns

The income approach values your business based on what it can earn going forward. This method takes your net income, adds back owner compensation and one-time expenses, and divides by a capitalization rate to arrive at value. For example, if your business generates $100,000 in normalized annual earnings and the market cap rate for your industry is 20 percent, your income-based valuation would be $500,000. This approach works best for profitable businesses with predictable cash flows, and it’s what most buyers actually care about-they want to know what they’ll earn after taking over.

The Market Approach: What Similar Businesses Sold For

The market approach compares your business to recently sold companies in your industry and region, then adjusts for differences in size, location, and growth. If three similar businesses sold for 4 to 5 times earnings in the past year, you apply that multiple to your earnings to estimate value. This method grounds your price in real market data, not wishful thinking.

The Asset-Based Approach: Your Tangible Foundation

The asset-based approach calculates value by totaling your tangible and intangible assets, then subtracting liabilities. It provides a practical floor price, especially useful if your business isn’t highly profitable or if you own significant physical assets like equipment or real estate.

Why One Method Isn’t Enough

Most sellers make the mistake of relying on a single method. Instead, use all three and weight them based on your situation. If you operate a service business with strong recurring revenue, the income approach should carry more weight. If your industry has active M&A activity with clear comparables, lean on the market approach. If you own a capital-intensive business or real estate alongside operations, the asset approach becomes more relevant.

IRS Revenue Ruling 59-60 explicitly recommends considering all three approaches rather than averaging them blindly. Professional valuators with credentials like ASA, AICPA, or NACVA reconcile these methods by documenting which approach best reflects your specific business and market conditions. This rigor matters because buyers will pressure you on price, and a defensible valuation backed by multiple methods gives you the confidence to hold your ground or justify a lower price if market conditions warrant it. With your valuation framework in place, the next step is understanding which factors actually move your price up or down.

Key Factors That Impact Your Business Valuation

Buyers pay for what your business will earn under their ownership, not what it produced last year. Three specific factors dominate every valuation conversation: revenue growth trajectory, customer retention strength, and whether your business operates independently of you.

Revenue Growth and Profit Stability

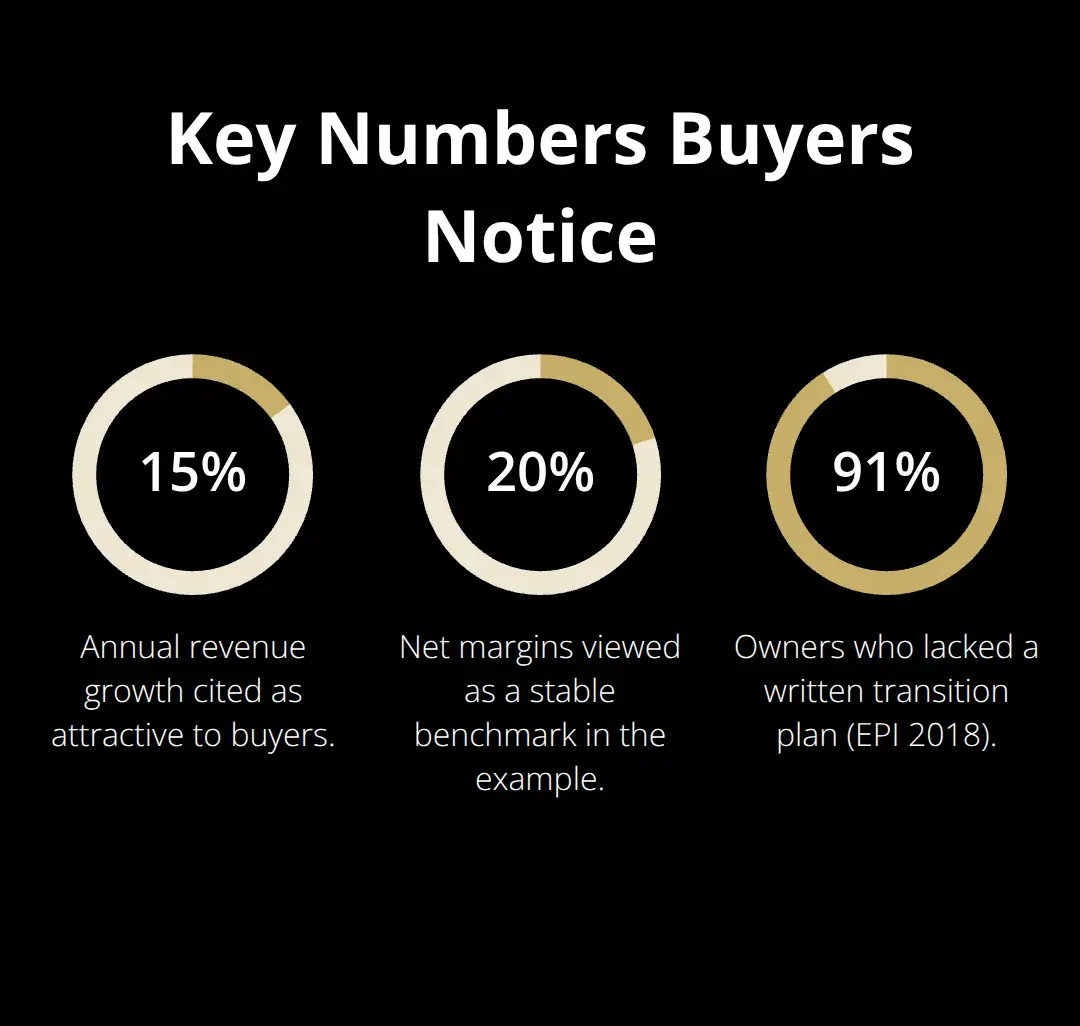

Revenue growth matters only when it’s real and sustainable. A business expanding 15 percent annually with stable 20 percent net margins attracts far higher multiples than one with flat revenue, regardless of current size. The Exit Planning Institute’s 2018 State of Owner Readiness report found that 91 percent of owners lacked a written action plan for transition, which signals to buyers that growth may stall post-sale.

Buyers scrutinize your last three to five years of financials for trends, not just the headline number. If your revenue jumped 40 percent in year three but your profit margin compressed from 25 percent to 15 percent, that raises immediate concerns. Normalized earnings-what you’d actually earn in a typical year after removing one-time gains, personal expenses, and irregular spikes-determine what buyers calculate as your multiple. Wild swings or heavy owner discretionary spending force you to recast your financials before hitting the market. Clean records eliminate friction and strengthen your negotiating position.

Customer Concentration and Market Position

Customer concentration destroys valuation faster than almost anything else. A diversified customer base enhances value by reducing dependency risk. Buyers also evaluate whether your market position is defensible. Recurring revenue, long-term contracts, or switching costs that lock customers in reduce perceived risk and justify higher valuations. These structural advantages signal stability to potential acquirers and make your business worth substantially more than competitors without them.

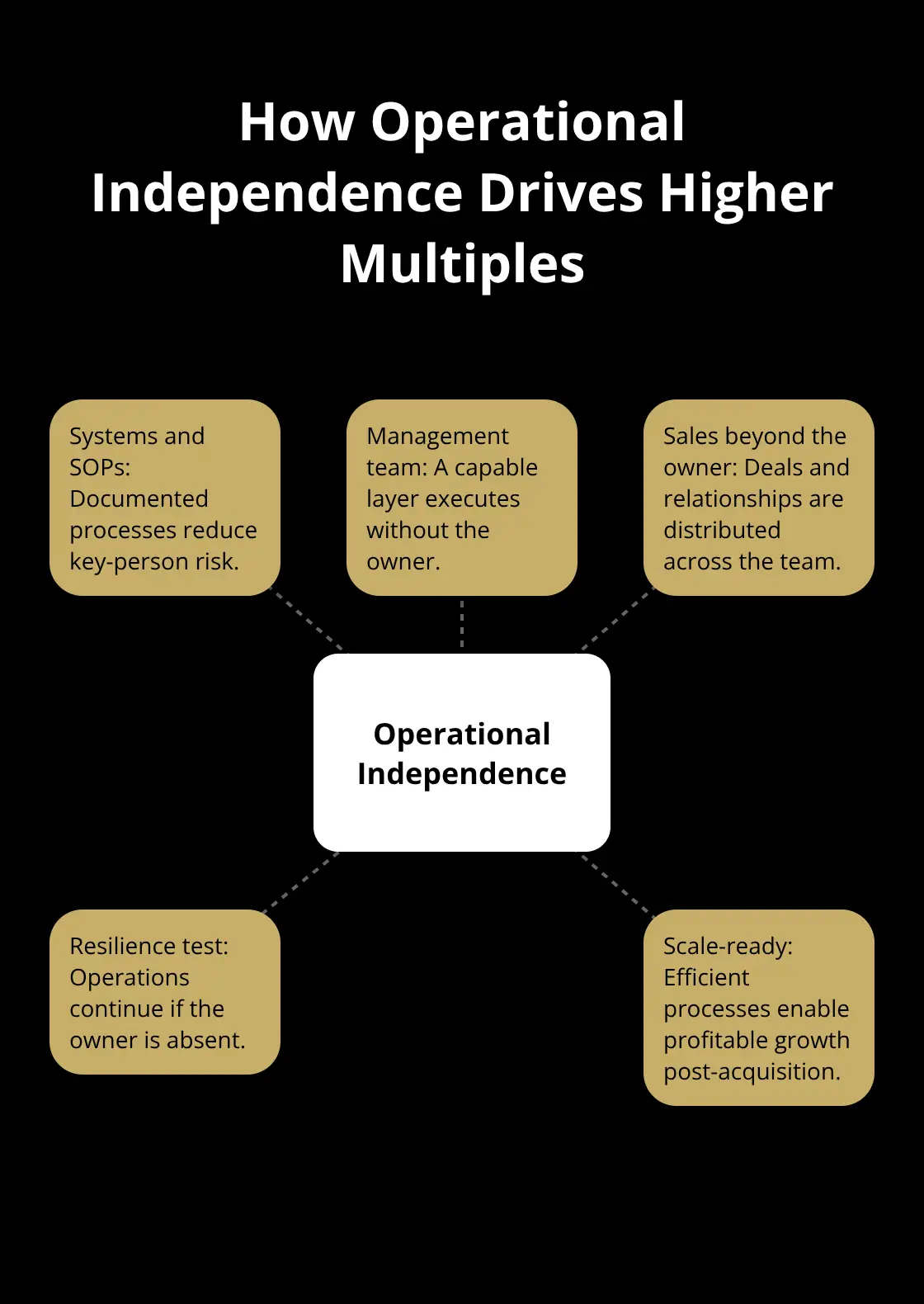

Operational Independence and Scalability

Operational efficiency and scalability determine whether a buyer can grow the business profitably after taking over. If your operation relies on you personally-you close all the deals, manage key relationships, handle hiring-the business is worth significantly less. Owner-dependent businesses often face significant valuation discounts during sales or appraisals because buyers perceive higher risks. If it doesn’t, buyers will either discount your valuation or demand you stay on post-sale, which complicates the deal and limits your exit options.

Systems, documented processes, and a capable management team that executes without your involvement separate businesses that sell for three times earnings from those that sell for six times earnings. Buyers test this ruthlessly during due diligence by asking whether operations would collapse if you disappeared tomorrow. The honest answer determines your price more than any other single factor.

This is why preparing your business for sale requires more than just assembling financial statements. You need to address the structural weaknesses that buyers will uncover and build the operational foundation that justifies a premium valuation.

Preparing Your Business for Maximum Valuation

Most sellers spend weeks agonizing over their asking price but only days preparing the actual business. This backwards approach costs money. Buyers will excavate your financials, operations, and customer relationships during due diligence. If you haven’t cleaned house first, you’ll either face steep discounts or kill the deal entirely when problems surface. The hard truth: 95 percent of sellers never reach peak valuation because they skip preparation. Start 12 to 24 months before your target sale date. This window gives you time to fix structural weaknesses without appearing desperate.

Assemble and Recast Your Financial Records

Your first task is assembling financial documentation that tells a coherent story. Collect three to five years of profit and loss statements, tax returns, cash flow statements, and a detailed balance sheet showing all assets and liabilities. These documents form the foundation of every valuation conversation. More importantly, recast your financials by removing one-time purchases, owner discretionary spending, and non-operational expenses. If you spent $50,000 last year on a personal vehicle, a country club membership, or a one-time facility upgrade, add it back to net income. Buyers care about normalized earnings, not what you personally extracted. Clean, recasted financials eliminate friction and let buyers focus on what your business actually earns rather than questioning your accounting.

Build Systems That Operate Without You

Many sellers fail to address owner dependence head-on. If your business collapses without you, take concrete steps to change that reality. Hire or promote a capable operations manager. Document your sales processes and key customer relationships so they survive your exit. Create standard operating procedures for critical functions. Buyers test whether operations function independently through specific questions during due diligence: Can your team execute without your involvement? Do customers have relationships with your business or just with you? Is there a management layer between you and daily operations? Honest answers to these questions determine whether you receive a three-times-earnings multiple or a six-times-earnings multiple. Businesses that command premium valuations have systems, documented playbooks, and capable teams that run independently.

Final Thoughts

You now have a framework for valuing your business with confidence. The income approach, market approach, and asset-based approach give you multiple data points to defend your asking price. Revenue growth, customer retention, and operational independence determine whether buyers see your business as a three-times-earnings opportunity or a six-times-earnings one.

Preparation separates sellers who reach peak valuation from those who leave money on the table. Start 12 to 24 months before your target sale date so you have time to assemble financial records, recast them to show normalized earnings, and build systems that operate without you. Buyers will scrutinize everything during due diligence, and a well-prepared business commands premium multiples while a rushed one faces steep discounts.

When you’re ready to move forward with valuation for sellers, we at Unbroker help you navigate the entire journey with transparent pricing and expert support through our Full Service Business Sale option or our Assisted Business Sale, both of which include access to a vast buyer network and premium marketing tools to protect your interests.