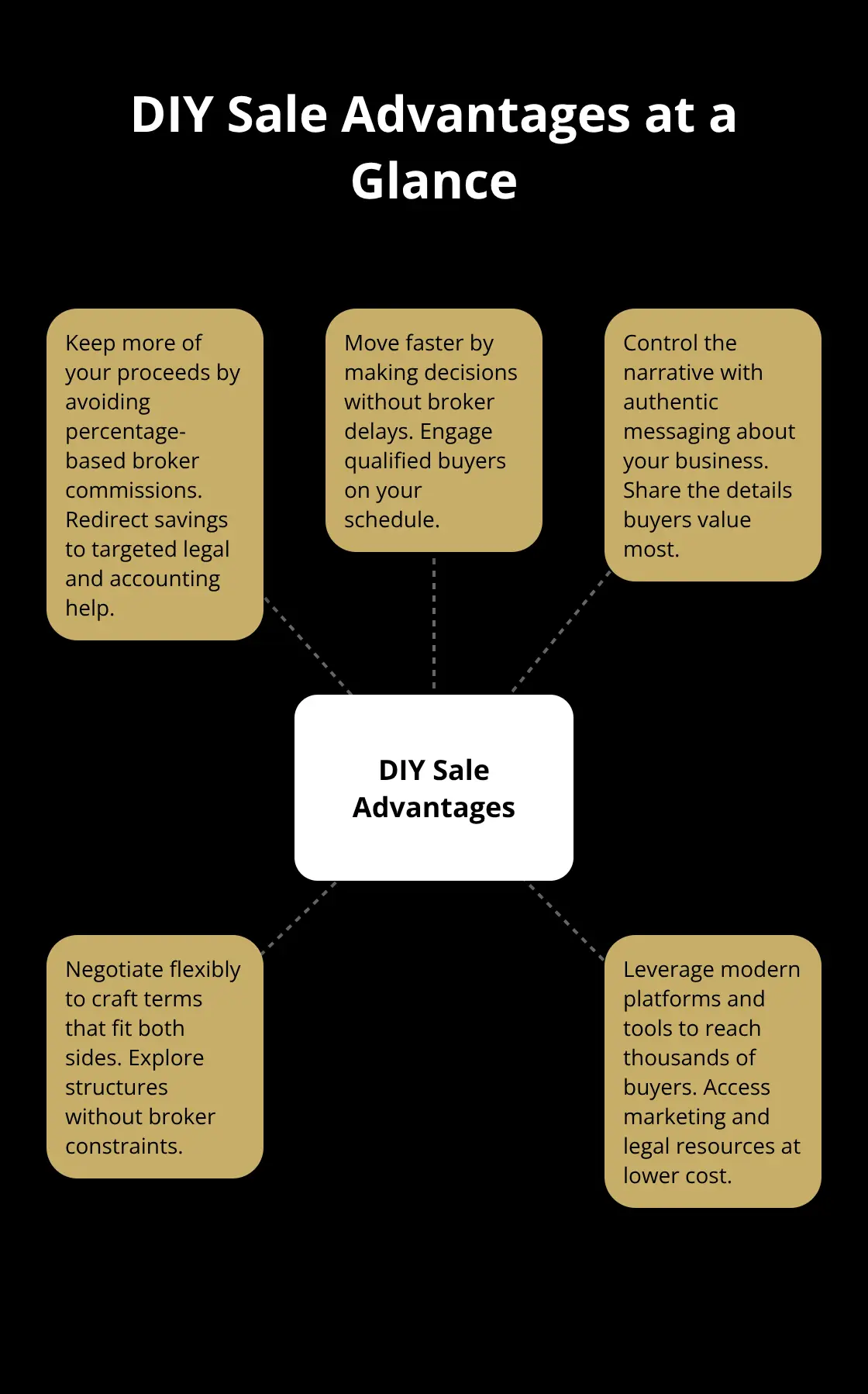

Selling your business without a broker is no longer a fringe strategy-it’s becoming mainstream. More business owners are taking control of their sales process and keeping more money in their pockets.

At Unbroker, we’ve seen firsthand how a do it yourself sale can work when you have the right approach. This guide walks you through every step, from preparing your financials to closing the deal.

Why More Sellers Are Going It Alone

Business owners who sell without a broker save substantial money upfront. Traditional brokers typically charge between 8% and 10% of the sale price, which on a $500,000 business sale means $40,000-50,000 in fees. A DIY approach eliminates this cost entirely, or reduces it dramatically if you use a platform that charges a flat fee instead of a percentage. The financial incentive is real and measurable.

Beyond commissions, brokers often charge additional fees for marketing, legal work, and administrative tasks that stack up quickly. When you handle the sale yourself, you control which services you actually need and which ones you can skip or address independently. This cost difference matters most for smaller business sales where broker fees consume a larger percentage of your profit. A business selling for $250,000 loses $20,000-25,000 to traditional brokers, making the DIY path significantly more attractive financially.

You Keep More of What You Earn

The financial advantage translates directly to your bottom line. If your business is worth $1 million and a broker takes 10%, you lose $100,000. That same $100,000 stays in your pocket when you manage the sale yourself. This isn’t theoretical-it’s the difference between funding your next venture or padding your retirement.

The money you save can cover professional services where they actually matter, like having a lawyer review contracts or hiring an accountant to prepare tax documentation. You’re not sacrificing quality; you’re redirecting money away from middlemen and toward services that directly protect your interests. Many sellers find they can afford better legal and accounting support when they eliminate broker commissions entirely.

Control Means Faster Decisions and Better Terms

When you sell your business yourself, you make every decision without waiting for broker approval or negotiation. You choose which buyers to engage with, what information to share, and when to move forward. This speed matters because broker-led sales often involve multiple layers of approval, internal discussions, and delays that stretch timelines unnecessarily.

You respond to serious buyers immediately rather than waiting for your broker to coordinate. You also control the narrative around your business. Instead of a broker’s generic description, you craft messaging that highlights what makes your company special. You decide which aspects matter most to potential buyers and emphasize those directly.

This direct communication often leads to better-aligned deals because buyers understand your business on your terms, not through a broker’s filtered perspective.

You can also negotiate more flexibly. If a buyer wants to structure the deal differently or needs custom terms, you can explore options without broker constraints. This flexibility often leads to deals that work better for both parties and close more smoothly.

Modern Platforms Eliminate the Broker Advantage

The traditional broker advantage was access to buyer networks and marketing reach. That gap has closed dramatically. Online platforms now connect sellers directly to thousands of qualified buyers. You can list your business on multiple platforms simultaneously, reaching far more potential buyers than most individual brokers could access.

Professional marketing tools that once required broker expertise are now available to everyone. You can create compelling listings with professional photos, detailed descriptions, and financial summaries without hiring anyone. Some platforms provide templates for legal documents, confidentiality agreements, and term sheets that once required expensive attorney time. AI-driven matching systems now identify interested buyers more efficiently than traditional broker outreach.

The technology advantage that brokers once controlled is now democratized. You have access to the same buyer networks, marketing tools, and legal resources that brokers use, often at a fraction of the cost. With these tools in place, you’re ready to prepare your business for the market-starting with the financial records and documentation that buyers will scrutinize most carefully.

Getting Your Business Ready to Sell

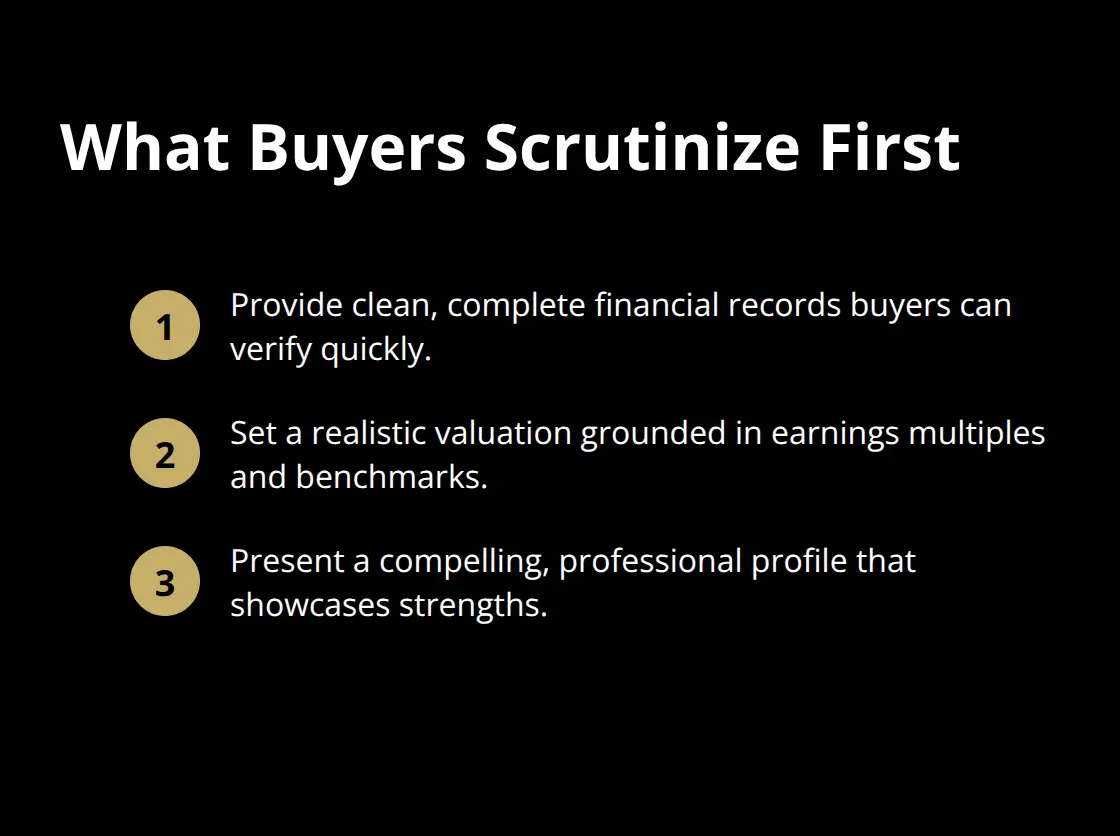

Buyers scrutinize three things before making an offer: your financial records, your business valuation, and your presentation. These three elements determine whether you attract serious buyers or waste months fielding lowball offers from unqualified prospects.

Organize Your Financial Records

Start with your financials because they’re non-negotiable. Most buyers want at least three years of tax returns, profit-and-loss statements, balance sheets, and cash flow statements. If your records are disorganized, consolidate everything into a single folder organized by year within two weeks. Missing or incomplete financials kill deals faster than anything else.

Buyers assume the worst when they can’t access clean data, and that assumption costs you money. If you’ve run your business informally without detailed records, hire an accountant now to reconstruct the last three years. This costs $1,500–3,000 but prevents buyers from walking away entirely.

Document everything that affects profitability: customer contracts, supplier agreements, lease terms, employee agreements, and any pending legal issues. Buyers need to understand what stays with the business and what leaves with you. Include details about your biggest customers and whether their contracts transfer to the new owner. If three customers represent 40% of your revenue, disclose that upfront rather than letting a buyer discover it during due diligence and renegotiate the price downward.

Value Your Business Accurately

Valuation is where most DIY sellers go wrong. They either overestimate what their business is worth or underestimate it so badly they leave six figures on the table. The most common approach uses multiples of earnings: multiply your annual profit by a number between 2 and 3.3 depending on your industry and growth rate.

A software-as-a-service business with recurring revenue might command a higher multiple, while a service business with inconsistent clients might warrant a lower one. If your business generates $200,000 in annual profit and trades at a 2.57x multiple, your valuation is $514,000. Use industry benchmarks to validate your number. The SBA provides data on typical valuations by industry, and sites like Flippa track actual sale prices for digital businesses. Get a second opinion from comparable businesses that sold recently in your market. If you’re off by 20%, you’ll either scare away qualified buyers with an inflated price or leave money on the table.

Create a Compelling Business Profile

Once you’ve calculated valuation, create a business profile that tells your story. Most DIY sellers write boring descriptions that sound like they copied them from a template. Write something that explains why your business matters and why someone should care.

Describe your competitive advantage in concrete terms: you’ve built a customer base that stays with you, you’ve created systems that run without your constant involvement, or you’ve developed a product that competitors can’t easily replicate. Quantify what makes you different. If your customer retention rate is 85% when the industry average is 60%, state that. If your business runs on 35% margins when competitors operate at 20%, highlight it. Buyers respond to specifics, not vague claims about quality or market position.

Include details about your team, your growth trajectory over the past three years, and your revenue sources. If you’ve grown 15% annually, show that progression. If you have recurring revenue contracts worth $X per year, quantify that security. Your profile should answer the question every buyer asks: why is this business worth purchasing instead of starting from scratch?

With your financials organized, valuation set, and profile written, you’re ready to market your business and attract qualified buyers who understand exactly what they’re purchasing.

How to Find Buyers and Close the Deal

List Your Business Across Multiple Platforms

The difference between a successful DIY sale and a failed one comes down to reaching the right buyers and negotiating confidently. Most DIY sellers list their business on one or two platforms and wonder why serious offers don’t materialize. You need a multi-channel approach that puts your business in front of qualified buyers across different networks simultaneously.

Start with platforms that specialize in business sales, not just general marketplaces. Digital business sale marketplaces connect sellers with thousands of vetted buyers and provide tools to manage inquiries without exposing your identity prematurely. List simultaneously on industry-specific platforms relevant to your business type-if you run a digital agency, platforms like Flippa attract serious tech buyers. Each platform has different buyer demographics, so multiple listings dramatically increase your odds of finding someone ready to move quickly.

Tailor Your Listing to Each Platform

Create separate listing descriptions for each platform rather than copying the same text everywhere. A buyer on one marketplace expects different messaging than one browsing an industry forum or LinkedIn group. Tailor each description to the platform’s audience and the types of buyers most active there.

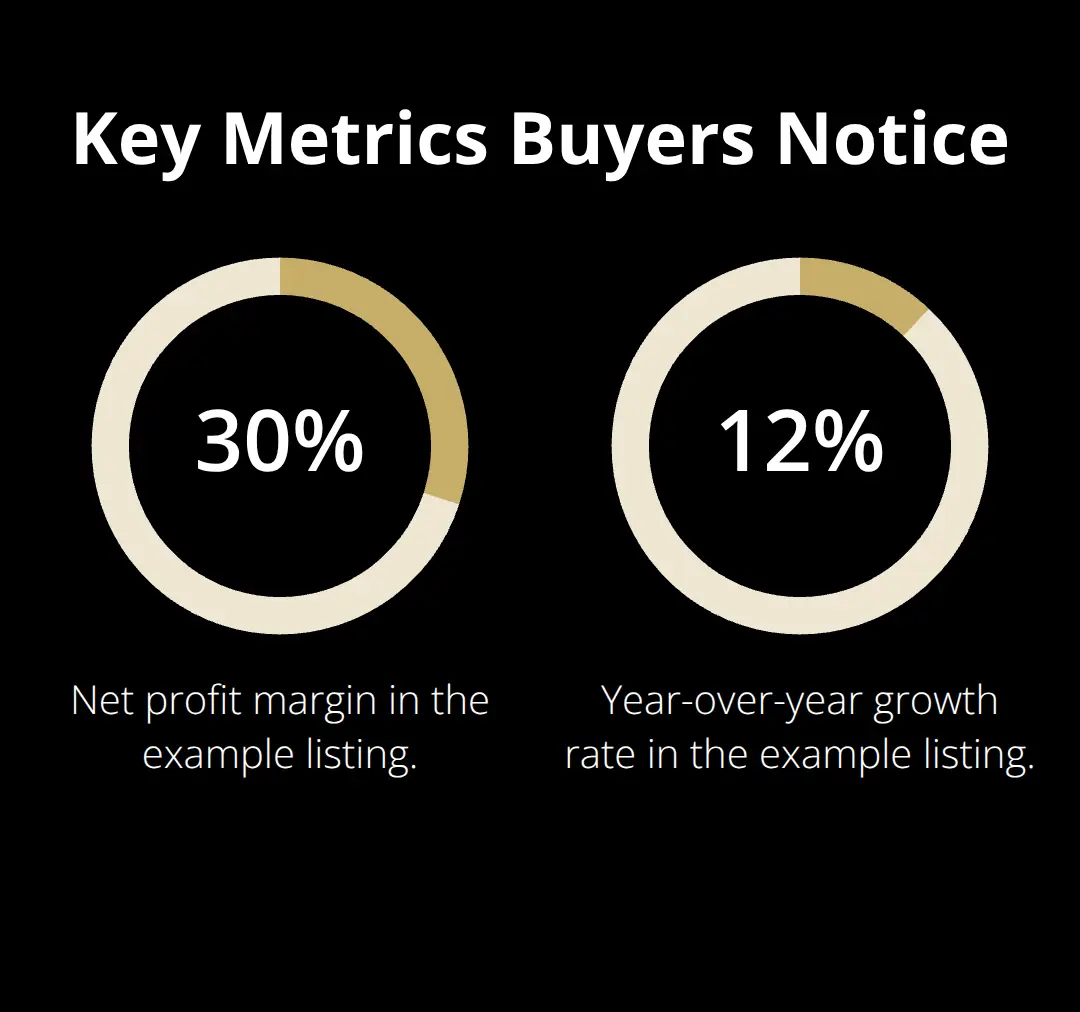

Include specific financial metrics in every listing: your annual revenue, profit margin, growth rate over the past three years, and customer acquisition cost. Buyers skip vague descriptions instantly. They want numbers that tell them whether your business fits their investment criteria. If your business generates $500,000 in annual revenue with 30% net margins and you’ve grown 12% year-over-year, state those facts prominently.

Add high-quality photos of your workspace, team, or products depending on your business type. Poor presentation kills deals before conversations even start.

Screen Buyers and Move Toward Serious Offers

Once inquiries arrive, your negotiation approach determines whether you achieve fair terms or face pressure to accept lowball offers. Screen buyers early by asking about their funding status, timeline, and why they’re interested in your specific business. Unqualified buyers waste your time-focus only on those with money ready and realistic expectations about valuation.

When a serious buyer appears, move quickly to a non-disclosure agreement before sharing detailed financials. This protects your business confidentiality and signals professionalism. Present your asking price confidently based on the valuation work you completed earlier. Don’t apologize for your price or treat it as a negotiation starting point. Buyers expect anchoring-they’ll make lower offers regardless of your initial ask, but starting too low leaves money on the table permanently.

Justify Your Price With Data

If a buyer’s offer falls below your acceptable range, explain your valuation methodology clearly. Walk them through your profit calculations, comparable sales in your industry, and growth trajectory. Data-backed justification often moves buyers closer to your price. When disagreements arise over valuation, suggest bringing in a neutral third-party appraiser rather than debating endlessly. This costs $1,500–3,000 but breaks deadlocks and demonstrates you’re serious about fair pricing.

Negotiate non-financial terms aggressively when buyers won’t meet your price. Extended payment terms, earnouts tied to performance, or seller financing can add significant value beyond the headline purchase price. If a buyer offers $450,000 when you want $500,000 but will finance 20% of the purchase over two years at 5% interest, you’ve effectively increased your return substantially.

Document Everything and Secure Legal Review

Document every offer and counteroffer in writing immediately, even informal discussions. Verbal agreements create confusion and disputes. Use email confirmations to establish clear records of what each party agreed to. When you’re close to agreement, hire a business attorney to review the purchase agreement before signing. This typically costs $2,000–4,000 but prevents costly mistakes in contract language that could haunt you after closing. Many DIY sellers skip legal review to save money and regret it when disputes arise post-sale over representations they made or obligations they unknowingly accepted.

Final Thoughts

A do-it-yourself sale works when you approach it systematically. You organize your financials, value your business accurately, create a compelling profile, and market across multiple platforms. You screen buyers carefully, negotiate confidently, and document everything in writing. These steps separate successful DIY sellers from those who struggle and settle for less than their business deserves.

The financial advantage remains your strongest motivator-saving $40,000 to $100,000 in broker commissions funds your next chapter. Success requires discipline, though. You must resist accepting the first offer that arrives, even when negotiations feel exhausting. You must hire professional help where it matters most: legal review before signing, accounting support if your records are weak, and valuation validation from industry benchmarks (these targeted expenses protect far more money than they cost).

Some sellers discover during the process that they lack time or confidence to negotiate effectively. If you reach that point, Unbroker offers assisted options designed for sellers who want expert guidance without traditional broker fees. You maintain control while accessing negotiation assistance and qualified buyers-making your do-it-yourself sale strategy work exactly as you intended.