Knowing what your business is worth isn’t just for selling or raising capital. It shapes strategic decisions, tax planning, and how you understand your company’s real position in the market.

At Unbroker, we’ve seen business owners make costly mistakes because they didn’t grasp the fundamentals of business valuation. This guide walks you through the core methods and concepts you need to value your business accurately.

What Business Valuation Actually Determines

Business valuation isn’t an abstract financial exercise. It answers a specific question: what would someone actually pay for your business right now, given what it generates, what it owns, and what risks it carries? The answer changes everything about how you operate. A business valued at $2 million versus $5 million tells you whether you’re sitting on hidden value or burning cash. Valuations drive real decisions about whether to sell, restructure, raise capital, or adjust your strategy. They also matter for tax purposes-the IRS requires documented valuations for gift and estate tax, ESOPs, and charitable donations. When disputes arise around ownership or dissenting shareholders want to exit, valuations determine who gets paid what. Courts use them to settle litigation claims. Accountants use them to assess goodwill impairment. If you plan an exit in three years, your valuation today tells you what work needs to happen to hit your target price.

Why timing shapes your valuation strategy

A valuation conducted too early wastes money on a number that won’t hold up in a year. A valuation conducted too late means you’re flying blind during critical years when small changes in profitability or customer concentration could shift your value by hundreds of thousands. Most business owners value their companies when they face a specific trigger-a potential sale, investment round, divorce settlement, or major restructuring. Smart operators, however, value annually or every two years to track whether their decisions actually move the needle. A valuation also exposes gaps. If your multiple sits at 4x EBITDA while competitors trade at 6x, that gap signals a specific problem: growth rate, customer concentration, market position, or operational risk. Fixing that problem is worth more than hoping a buyer overlooks it.

How standards of value affect your outcome

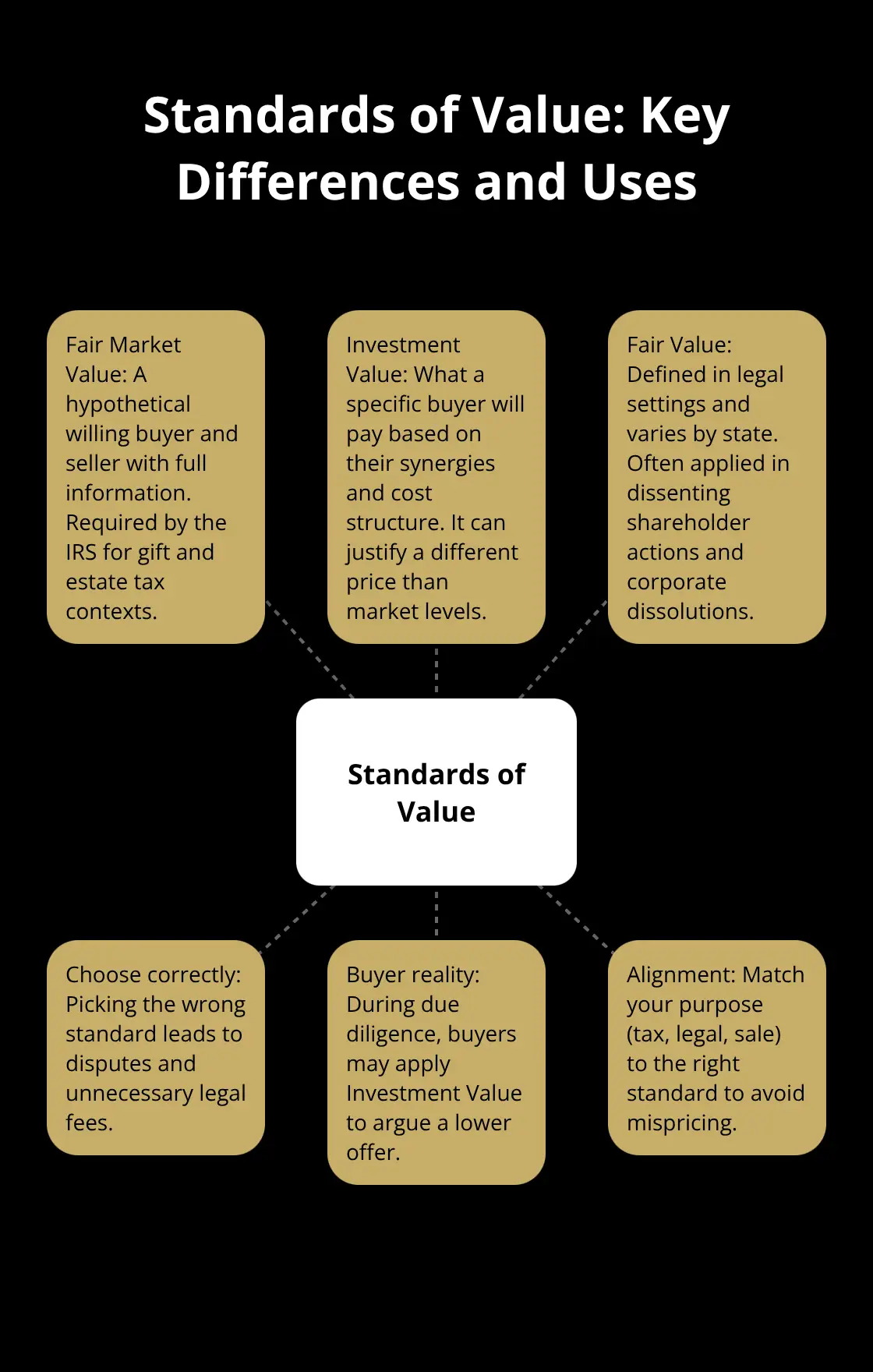

The standard of value matters more than most owners realize. Fair Market Value assumes a hypothetical willing buyer and seller with full information. Investment Value reflects what a specific buyer will pay based on combined benefits.

Fair Value in legal contexts varies by state and applies in dissenting shareholder actions or corporate dissolutions. Choosing the wrong standard leads to disputes and wasted legal fees. The IRS requires Fair Market Value for gift and estate tax situations. A buyer conducting due diligence may apply Investment Value to justify a lower offer based on their specific cost structure. Understanding which standard applies to your situation prevents costly misalignment between what you think your business is worth and what a court or tax authority will accept.

What comes next in the valuation process

The three core approaches-income, asset-based, and market comparison-each reveal different aspects of your business’s true value. Which method you choose depends on your industry, your financial stability, and the purpose of the valuation itself. Understanding how these approaches work and when to apply them is what separates owners who negotiate from a position of strength from those who accept whatever offer lands on their desk.

How Each Valuation Method Works in Practice

The Income Approach: Translating Profits Into Price

The income approach values your business based on what it actually generates in cash. This method applies an earnings multiple to your EBITDA or net income, translating profit into a present-day price. If your business produces $500,000 in EBITDA and comparable companies in your industry trade at 5x EBITDA, your enterprise value sits around $2.5 million. The multiple itself reflects market expectations about growth, risk, and competitive position.

A software company might command 12x EBITDA while a local service business trades at 3x, not because one is better managed, but because investors expect faster growth and lower customer churn in software. The discount rate and growth assumptions matter enormously here. Small changes in your assumed growth rate or the cost of capital can swing your valuation by hundreds of thousands of dollars. If you project 3% growth instead of 5%, your value drops significantly.

The strength of this approach lies in its direct connection to cash generation. Buyers care about what they can extract from the business, and the income approach speaks their language. The weakness is its sensitivity to assumptions. You must defend your projections with historical performance and market data, not wishful thinking.

The Asset-Based Approach: What You Own Minus What You Owe

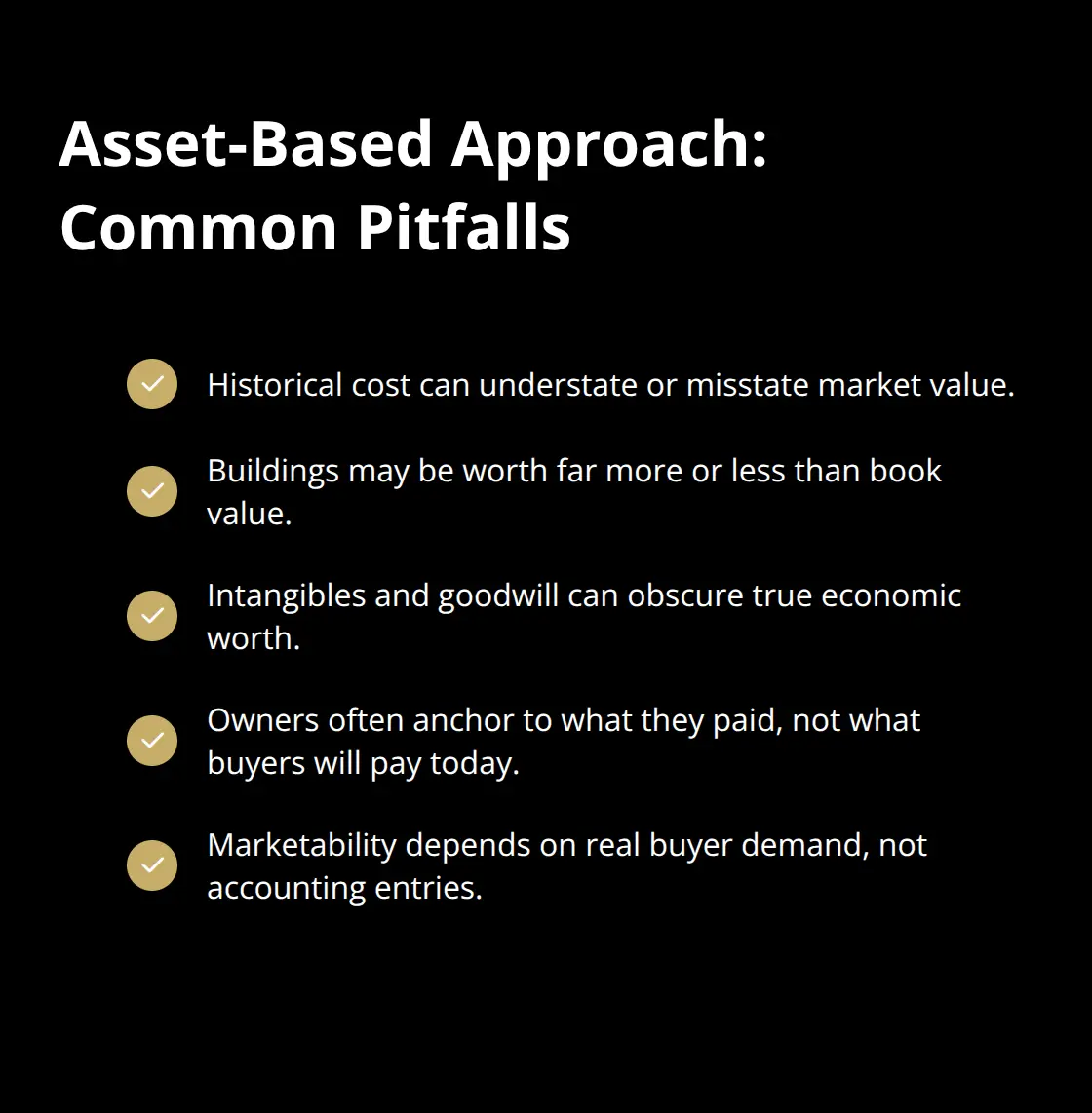

The asset-based approach values what your company owns minus what it owes. This method works well for asset-heavy businesses like manufacturing, real estate, or equipment rental where tangible assets drive value. It fails badly for service firms, software companies, or businesses where most value sits in customer relationships and brand.

Book value from your balance sheet rarely reflects true value because accounting uses historical cost, not market price. A building purchased ten years ago appears on your books at its original price, not its current market worth. Goodwill and intangible assets muddy the picture further. Most owners overestimate asset value because they anchor to what they paid, not what someone would actually buy those assets for today.

The Market Comparison Approach: What Real Buyers Actually Pay

The market comparison approach looks at what buyers recently paid for similar businesses in your industry. If three comparable companies sold in the past eighteen months at 4.2x, 4.8x, and 5.1x EBITDA, you have concrete market data instead of guesses.

This approach requires recent, comparable transactions. A sale from five years ago tells you nothing about today’s market. Size matters too. A $50 million acquisition of a competitor carries more weight than a $2 million deal. Adjustments for differences in growth rate, customer concentration, profitability, and financing terms are essential. A buyer paying 6x EBITDA for a company with 40% year-over-year growth justifies a different multiple than one growing 5% annually.

The market approach answers the question every owner wants answered: what will a real buyer actually pay right now? Understanding which method fits your situation-and often, using all three to triangulate value-determines whether you negotiate from strength or accept whatever offer arrives first.

What Really Moves Your Business Value

Growth Rate Dominates Everything Else

Growth rate premium in valuation multiples is the single biggest value driver, and it overshadows almost everything else. A business expanding at 20% annually commands multiples three to four times higher than one expanding at 3%. Tesla traded at 36x EBITDA in 2016 while Ford sat at 15x and GM at 6x, not because Tesla operated more efficiently, but because investors priced in explosive growth. That growth premium persists until the market believes growth will slow.

The gap between your growth rate and your industry’s average growth rate determines whether you command a premium or a discount. If your industry averages 5% growth and you expand at 12%, that spread is worth money. If you both expand at 5%, your multiple converges with competitors.

Profitability and Margin Trends Matter More Than Raw Profit

Profitability matters, but only as a foundation. A business can expand fast and still destroy value if it bleeds cash. What matters is whether your growth produces actual earnings or just revenue. A SaaS company expanding at 50% annually while maintaining 20% net margins generates real cash that justifies a premium multiple. A contractor expanding at 40% while operating at 2% margins takes on risk without reward.

Margin expansion and operational leverage matter more than absolute profit levels. A business that improves margins by 300 basis points year-over-year signals operational discipline ahead. A business with flat or declining margins despite revenue expansion raises red flags about cost control and competitive pressure. Buyers explicitly model margin expansion into their acquisition decisions, so a clear path to better margins directly increases what they’ll pay.

Customer Concentration and Recurring Revenue Shape Risk

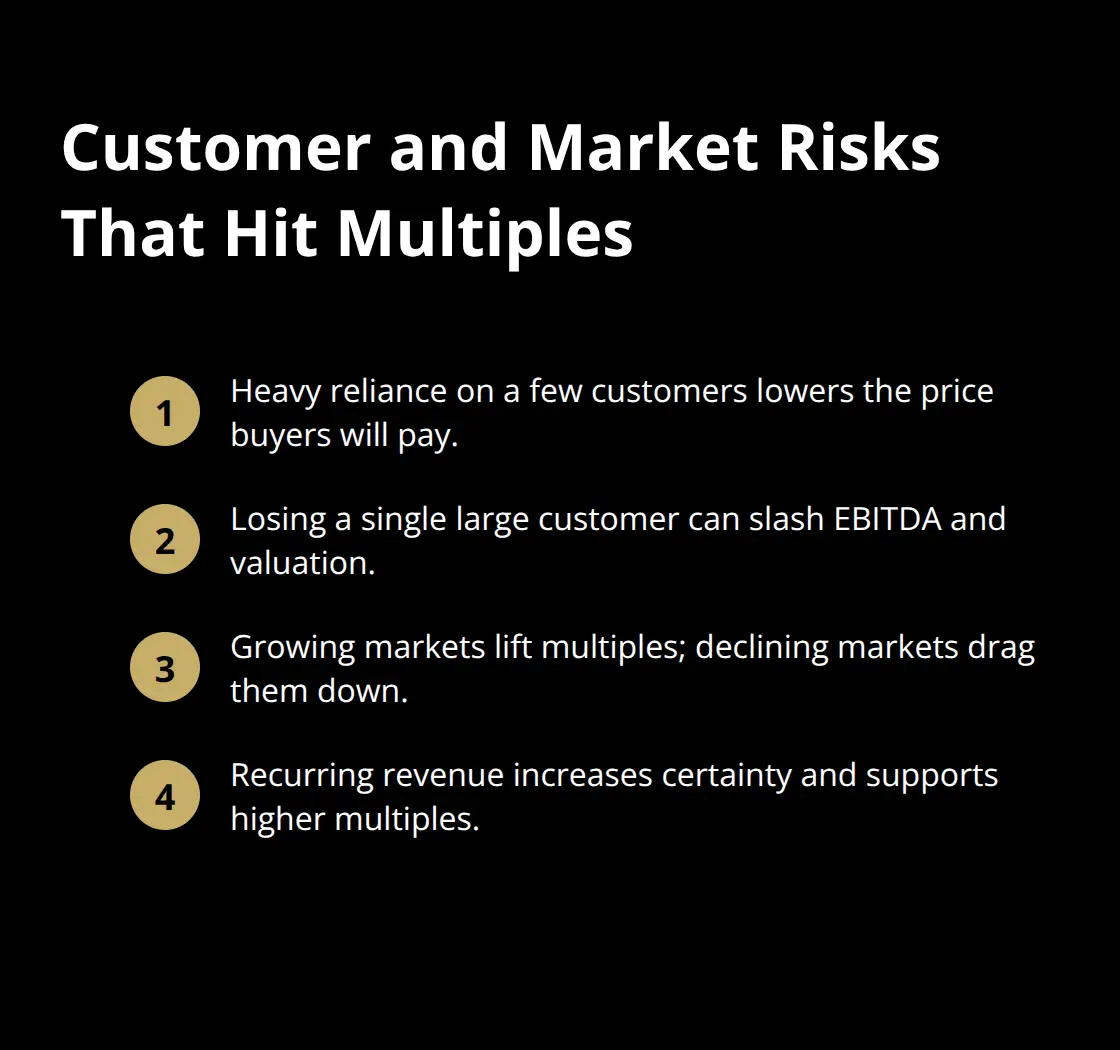

Industry position and customer concentration determine risk, and risk directly reduces your multiple. A business operating in a expanding market segment with tailwinds from secular trends commands higher multiples than one in a declining industry. But this advantage evaporates if you depend on three customers for 60% of revenue. Concentration risk is the fastest way to kill valuation multiples.

A buyer acquiring a business where one customer represents 30% of revenue demands a steep discount because losing that customer cuts EBITDA by 30%.

Recurring revenue valuation multiples fundamentally change valuation math. In 2025, typical SaaS valuation multiples on an ARR basis range from 2.5X to 6X, depending heavily on growth rate, customer durability, and deal structure. Recurring revenue reduces uncertainty and allows buyers to project cash flows with confidence. That certainty translates directly into higher multiples.

Unit Economics and Customer Quality Reveal Sustainability

Customer acquisition cost relative to lifetime value reveals whether your expansion is sustainable or borrowed time. If you spend $5,000 to acquire a customer who generates $8,000 in lifetime value, that’s healthy unit economics. If you spend $5,000 to acquire a customer worth $4,500, your expansion is temporary. Sophisticated buyers model this carefully and adjust their offers accordingly.

The quality of your customer base matters more than the size. Ten customers generating $100,000 each in annual value is stronger than 200 customers generating $5,000 each. Large, stable customers reduce churn risk and make projections more defensible. Geographic concentration also impacts value. A business concentrated in one region or one country faces regulatory, economic, and market risks that a geographically diversified business avoids. Diversification, whether geographic or customer-based, commands a valuation premium because it reduces the odds that a single event destroys the business.

Final Thoughts

Business valuation basics rest on three pillars: what your business generates in cash, what it owns, and what comparable businesses actually sell for. The income approach translates your profits into a market price using earnings multiples. The asset-based approach works when tangible assets drive value. The market comparison approach grounds your valuation in real transactions. Most owners benefit from using all three methods to triangulate value rather than relying on a single number.

Choosing the right approach depends on your industry and your reason for valuing. A software company with strong recurring revenue and minimal physical assets leans toward the income approach, while a manufacturing business with significant equipment and real estate may weight the asset-based approach more heavily. Tax authorities require Fair Market Value, but a potential buyer may apply Investment Value based on their specific synergies. Understanding which standard applies prevents disputes later.

Growth rate, profitability, customer concentration, and recurring revenue determine whether you negotiate from strength or accept whatever offer arrives. We at Unbroker help business owners navigate the sale process with transparent pricing and expert support, giving you access to a vast buyer network and premium marketing tools without the hidden fees traditional brokers charge. Start your valuation journey with Unbroker and understand your business’s true market value before you enter negotiations.