Buying a business doesn’t require a traditional SBA loan. We at Unbroker know that many buyers hit roadblocks with lengthy approval processes, strict requirements, and unexpected costs.

SBA loan alternatives exist, and some work faster and with fewer barriers. This guide covers seller financing, private investors, and other real funding sources that can get your acquisition done.

Seller Financing and Owner Carry-Back Options

Seller financing flips the traditional lending model on its head. Instead of approaching a bank or SBA lender, you negotiate directly with the business owner to fund part or all of the purchase price. The seller acts as your lender, and you repay them over an agreed timeframe with interest. This approach works because sellers often have strong incentives to close deals quickly and want certainty that their business transitions smoothly. A seller who finances part of the sale typically stays invested in the business’s success during the transition, which reduces your risk as a buyer. The mechanics are straightforward: you and the seller agree on a down payment amount (often 20–40% of the purchase price), and the seller finances the remainder. You sign a promissory note and possibly a security agreement, which gives the seller a legal claim to business assets or personal guarantees if you default. Closing happens in weeks rather than months because you bypass bank underwriting entirely.

How Seller Financing Works in Business Sales

Speed matters when you compete for acquisition targets or when market conditions shift rapidly. Seller financing accelerates the entire process because both parties can negotiate terms without waiting for bank approvals or SBA processing. You avoid the lengthy documentation requirements that traditional lenders demand. The seller and you control the timeline, not a loan committee. This flexibility attracts buyers who face credit challenges or who operate in industries that banks typically avoid. The business itself becomes the primary collateral, which means the seller retains a direct stake in your success. If the business performs well, the seller receives steady payments. If it struggles, the seller has recourse through the security agreement. This alignment of interests creates a partnership dynamic that traditional lending never achieves.

Why Sellers Agree to Finance

Sellers finance deals because they benefit significantly. First, seller financing expands the buyer pool. If you cannot qualify for traditional loans, you would never make an offer, so the seller loses a potential sale. Second, sellers often receive better overall returns than keeping cash in low-yield investments. A seller financing 60% of a $500,000 purchase at 6–7% interest earns solid returns while maintaining seller notes as assets. Third, seller financing reduces their tax liability in the year of sale through installment sale treatment, a major advantage for owners with large capital gains. The seller also avoids the uncertainty of finding a buyer through brokers or waiting months for bank approvals. From your perspective as a buyer, seller financing means lower closing costs, no SBA application fees, and flexibility on terms that banks would never offer. You also avoid personal guarantees in many cases, since the seller often accepts the business itself as collateral.

Structuring Terms That Protect Both Sides

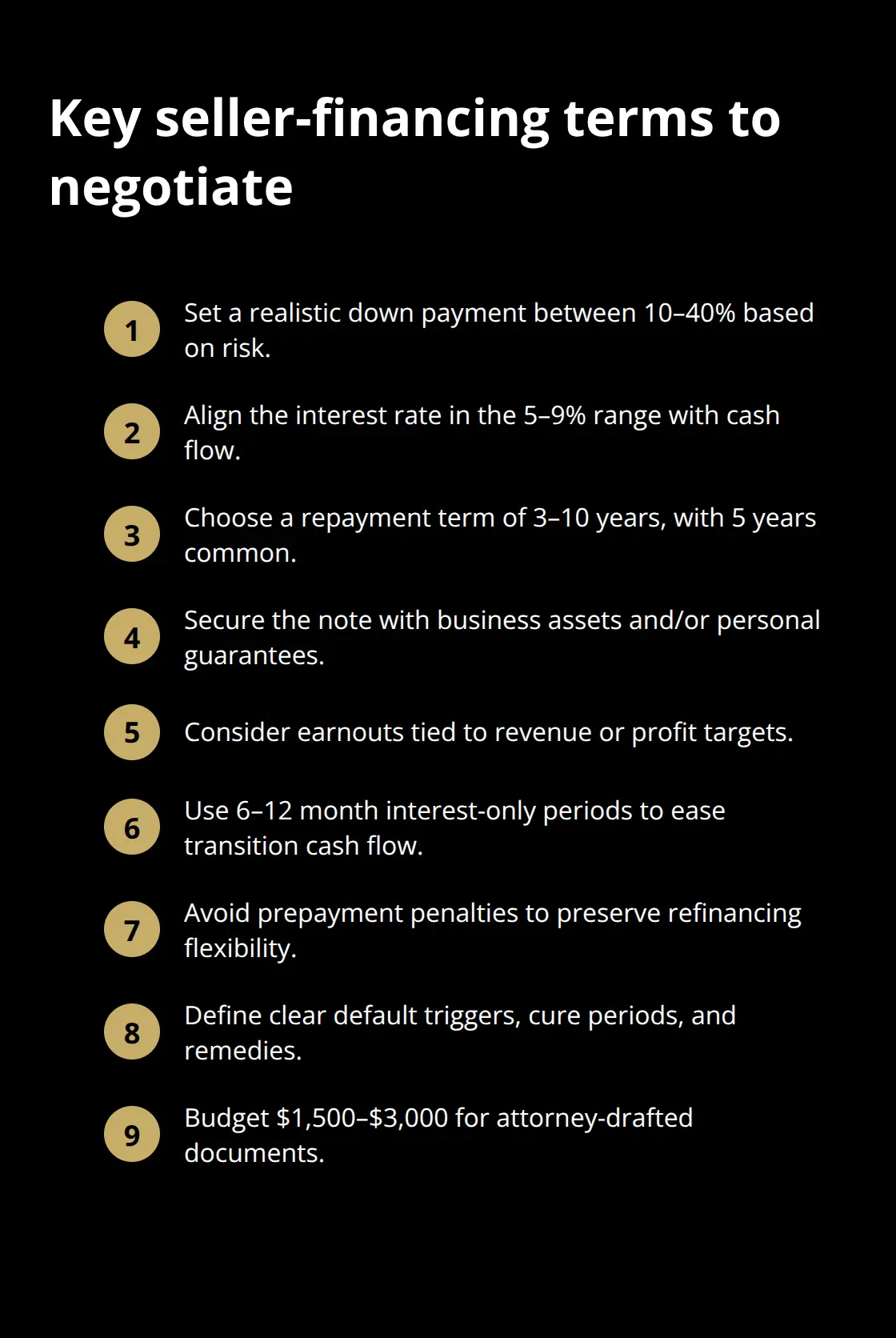

Terms matter enormously in seller financing, and both parties can negotiate them fully. Down payments typically range from 10–40% depending on your financial strength and the seller’s confidence. Interest rates on seller-financed deals usually fall between 5–9%, often lower than conventional business loans but higher than the seller’s cost of capital. Repayment periods vary from 3 to 10 years, though 5 years is common for smaller acquisitions. A critical detail is whether the note is secured by business assets, personal guarantees, or both.

Unsecured seller notes are rare and only happen with highly credible buyers. Most sellers require a security interest in equipment, inventory, and accounts receivable. Some deals include earnout provisions where part of the payment depends on the business hitting revenue or profit targets post-acquisition. This protects both parties: the seller sees proof the business performs, and you avoid overpaying for a declining operation. Interest-only periods of 6–12 months can ease your cash flow during the transition phase before principal payments begin. You should also negotiate whether prepayment penalties exist. Avoiding prepayment penalties gives you flexibility to refinance into a bank loan later if your credit improves or the business performs exceptionally well. Default provisions matter too. Define what constitutes default, the notice period before acceleration, and whether the seller can reclaim assets or force a sale of the business. Working with a business attorney to draft the promissory note costs $1,500–$3,000 but protects both parties and prevents disputes later.

Advantages for Both Buyers and Sellers

Seller financing works best when the purchase price aligns with the business’s cash flow, meaning your revenue covers debt service comfortably from day one. This structure ensures you can sustain operations while repaying the seller. The seller benefits from a steady income stream that often exceeds what they would earn from passive investments. You benefit from terms that a traditional lender would never offer-flexible repayment schedules, lower interest rates, and the ability to negotiate around your specific business cycle. Unlike SBA loans, which impose rigid requirements and lengthy approval timelines, seller financing adapts to your situation. The business itself demonstrates its viability through existing revenue, which both parties can verify. This transparency builds confidence on both sides and accelerates the deal. When you move forward with seller financing, you eliminate the uncertainty that plagues traditional lending. The next step involves exploring how private equity and angel investors can complement or replace seller financing for larger acquisitions.

Beyond Banks: Private Capital and Asset-Based Paths

Angel Investors and Private Equity Fill Financing Gaps

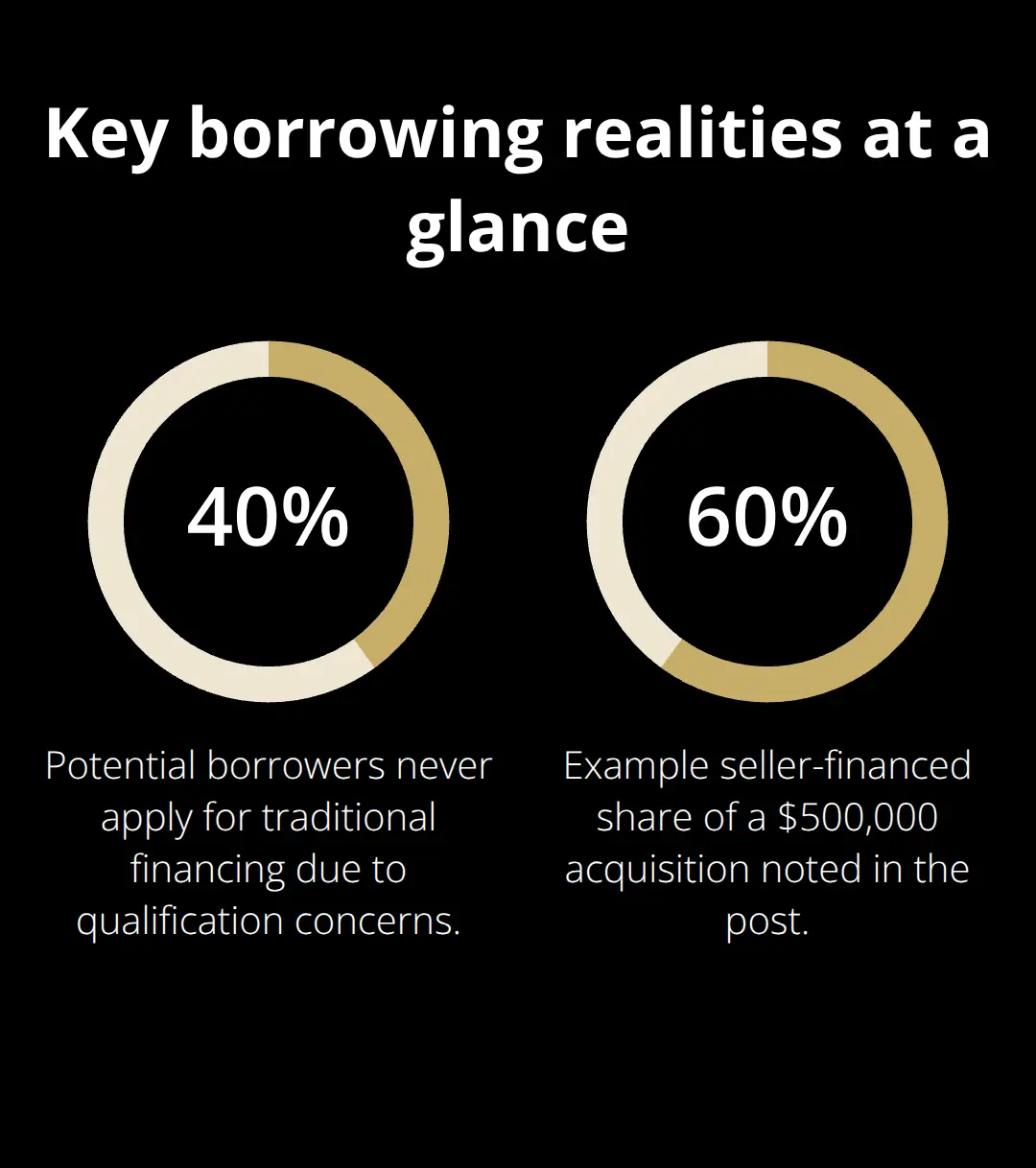

When seller financing covers part of your acquisition but you need additional capital, private equity investors and angel networks fill the gap effectively. Angel investors typically write checks between $25,000 and $100,000 per deal, though some syndicate larger rounds. Unlike banks that scrutinize credit scores and tax returns obsessively, angels evaluate the business’s revenue trajectory, your management experience, and the industry’s growth potential. A January 2025 Treasury analysis found that 40% of potential borrowers never apply for traditional financing, often because they know they won’t qualify, yet many of these same buyers attract private capital by demonstrating strong operational fundamentals.

Angel networks operate regionally through organizations that vet entrepreneurs and facilitate introductions. The equity trade-off is real: you surrender ownership stake, typically 10–30% for early-stage acquisitions, but you gain mentorship, industry connections, and patient capital that doesn’t demand repayment within five years. Crowdfunding platforms like Wefunder and SeedInvest let you raise capital from dispersed investors without relying on a single wealthy backer, though success depends entirely on your ability to articulate the acquisition’s value proposition and build audience engagement. The global crowdfunding market is projected to exceed $28 billion by 2028, underscoring its legitimacy as a funding channel for business acquisitions.

Equipment Financing Secures Hard Assets Separately

Asset-based lending and equipment financing represent a completely different approach that works when your acquisition includes tangible assets like machinery, inventory, or real estate. Lenders in this category care far less about your personal credit or business history because the equipment itself secures the loan. National Funding approves borrowers with credit scores as low as 475 and offers equipment financing up to $150,000 with no collateral required beyond the equipment itself. SBG Funding delivers same-day funding for equipment loans running 1–10 years, requiring only $10,000 monthly revenue and six months in business.

This matters for acquisitions because equipment-heavy businesses like manufacturing, construction, or automotive service shops can finance the hard assets separately from the purchase price, reducing the amount you need from seller financing or equity investors. The equipment becomes the primary collateral, which means lenders approve faster and charge lower rates than they would for unsecured business loans.

Invoice Factoring Converts Receivables to Cash

Invoice financing and factoring work similarly: if the business you’re acquiring has unpaid customer invoices, you convert those receivables into immediate cash by factoring them at a typical rate of 1% to 5% of the invoice value per month. BlueVine approves factoring applications within 24 hours for businesses with just three months in operation and a minimum FICO of 530. This approach proves particularly valuable when you acquire a service business with strong recurring revenue but slow-paying corporate clients.

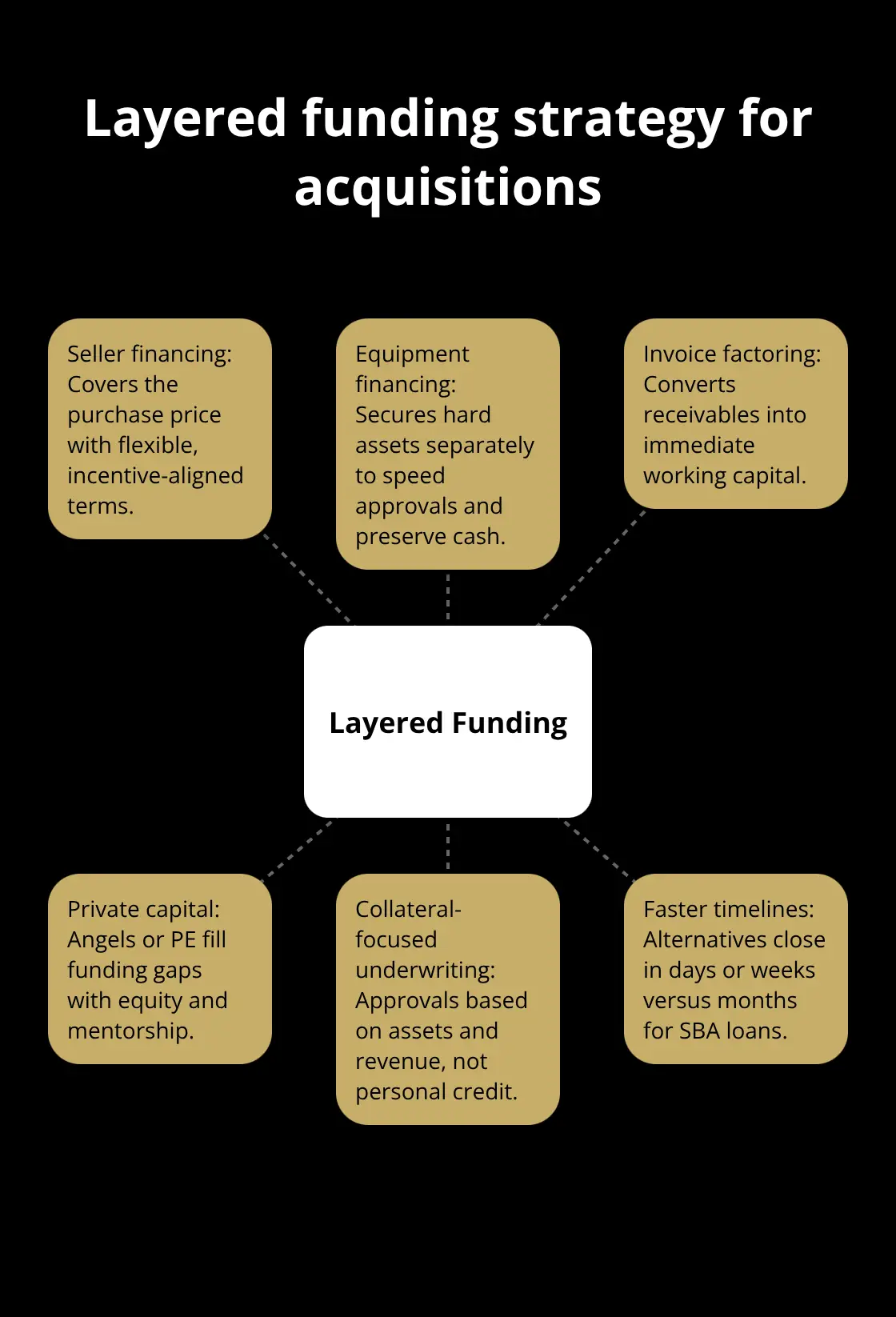

The combination of seller financing for the purchase price plus asset-based lending for equipment plus invoice factoring for working capital creates a layered funding strategy that banks would never assemble but that matches how real acquisitions actually operate. These tools work together to address different parts of your capital needs, and when you layer them strategically, you reduce reliance on any single funding source. The next section explores how to evaluate which combination of these alternatives fits your specific acquisition timeline and financial situation.

Why SBA Loans Lose to Faster Alternatives

SBA loans move slowly, and that slowness costs you real opportunities. The SBA’s 7(a) loan program approved 64,231 loans totaling $29.19 billion in July 2025, with an average loan size around $454,472, but the timeline to reach approval stretches across months. A typical SBA application demands tax returns for three years, detailed financial statements, personal credit reports, ownership history, collateral appraisals, and business plans that lenders scrutinize line by line. During a federal shutdown in 2025, approximately 320 small businesses per day lost access to SBA-backed loans, blocking roughly $170 million in funding daily. That disruption illustrates a hard truth: SBA programs depend on government operations, and when politics interfere, your acquisition stalls.

Speed Kills SBA Timelines

Alternative lenders approve faster and close quicker. BlueVine approves invoice factoring within 24 hours, and SBG Funding delivers equipment financing same-day. When you compete against other buyers for a specific acquisition, the seller won’t wait six months for your SBA approval. They accept an offer from someone using seller financing or private capital that closes in weeks. The months you spend in SBA underwriting represent months you could spend building the business after acquisition. Market conditions shift, and seller patience runs out. Another buyer with faster funding appears, and the seller moves on. SBA lenders also impose eligibility walls that reject solid borrowers. You need strong personal credit, typically 680 or higher, and the business must have operated for at least two years. Many acquisition targets fail these tests because they’re newer operations or have inconsistent revenue histories.

A January 2025 Treasury analysis found that potential borrowers never even apply for traditional financing because they know they won’t qualify. The SBA’s strict collateral requirements demand that you pledge personal assets beyond the business itself, meaning your home or savings sit at risk if the acquisition underperforms. Invoice factoring from BlueVine requires only a 530 FICO score and three months in business. Equipment financing from National Funding approves borrowers with scores as low as 475. These alternatives assess risk differently, focusing on the business’s actual revenue and assets rather than your personal credit history.

Hidden Costs Inflate SBA Expenses

SBA loans hide costs that don’t appear in the headline interest rate. The SBA guarantees 75–90% of the loan amount, but lenders charge guarantee fees ranging from 2–3.75% of the total loan, which gets rolled into your principal. An origination fee of 1–2% adds another layer. Closing costs, appraisals, and legal fees push total upfront expenses to 4–6% of the loan amount before you make a single payment. A $500,000 SBA loan carries $20,000–$30,000 in hidden fees beyond interest.

Invoice factoring at BlueVine charges 1–5% monthly on the invoice value, which sounds high but applies only to the cash you actually advance, not the full loan amount. Equipment financing from National Funding offers early payoff discounts of 6–7% if you pay within 100 days, rewarding fast repayment rather than penalizing it. Seller financing eliminates these hidden costs entirely. You negotiate interest directly with the seller, typically 5–9%, with no origination fees, no guarantee fees, and no appraisal costs. The only expense is a business attorney to draft the promissory note, running $1,500–$3,000, which protects both parties and prevents disputes.

Layered Funding Beats Single-Source Loans

When you layer seller financing with asset-based lending for equipment and invoice factoring for working capital, your total cost of capital drops dramatically compared to a single SBA loan. Seller financing covers the purchase price. Equipment financing handles hard assets separately. Invoice factoring converts receivables into immediate cash.

This combination addresses different parts of your capital needs without forcing every deal into a standardized SBA mold. The business’s actual revenue and assets drive approval decisions, not your personal credit score or years in operation. Alternative lenders approve faster because they assess risk differently. They focus on what the business generates today, not what your credit report shows from years past.

Final Thoughts

Buying a business without traditional SBA lenders is not just possible-it’s often smarter. Seller financing, equipment lending, invoice factoring, and private capital each solve different parts of your acquisition puzzle. When you layer these SBA loan alternatives together, you create a funding strategy that matches how real acquisitions actually work, not how banks want them to work.

Speed matters in acquisitions because while SBA applications stretch across months, alternative lenders approve in days. A January 2025 Treasury analysis found that 40% of potential borrowers never apply for traditional financing because they know they won’t qualify, yet many of these same buyers successfully acquire businesses using layered funding from multiple sources. The business’s actual revenue and assets drive approval, not your personal credit history or years in operation.

When you’re ready to sell, Unbroker connects you with qualified buyers who understand modern financing and can move fast. Your acquisition strategy should reflect how capital actually flows in today’s market-through multiple sources, faster timelines, and terms that work for your specific situation.