Property valuation can make or break a deal. Whether you’re selling, refinancing, or handling a business appraisal, getting the value right matters.

At Unbroker, we’ve seen both approaches work-and fail. This guide breaks down what separates professional appraisals from DIY methods, so you can pick the right path for your situation.

What Professional Appraisers Actually Do

A professional appraisal is far more than a price guess. It’s a formal, regulated assessment conducted by a licensed or certified appraiser who inspects your property in person, analyzes comparable sales in your area, and produces a legally recognized report. The appraiser visits your home, documents its condition, location, and features, then compares it against recent nearby sales to establish a defensible value. This process takes weeks to complete for most properties, though simpler cases may finish faster. The appraiser must follow USPAP standards set by the Appraisal Foundation, meaning every appraisal meets strict ethical and performance requirements.

What You’ll Pay for a Professional Appraisal

The average cost to appraise a single-family home runs about $357 according to Angi data from 2025, with typical prices ranging from $314 to $423 depending on property size, condition, and location. In Cleveland, expect around $325, while Seattle properties average $500. The buyer typically pays this fee as part of closing costs during a purchase, whereas homeowners pay for refinance appraisals themselves.

Who Can Actually Perform an Appraisal

Not everyone can hang out a shingle as an appraiser. Most states require appraisers to hold specific licenses or certifications, and the appraiser must be hired through a third-party management company rather than directly by you or the lender. This independence rule exists specifically to prevent conflicts of interest, a safeguard strengthened after the 2008 financial crisis. Certified appraisers have completed education requirements, passed exams, and maintain continuing education to keep their credentials current.

What Sets Professional Appraisers Apart

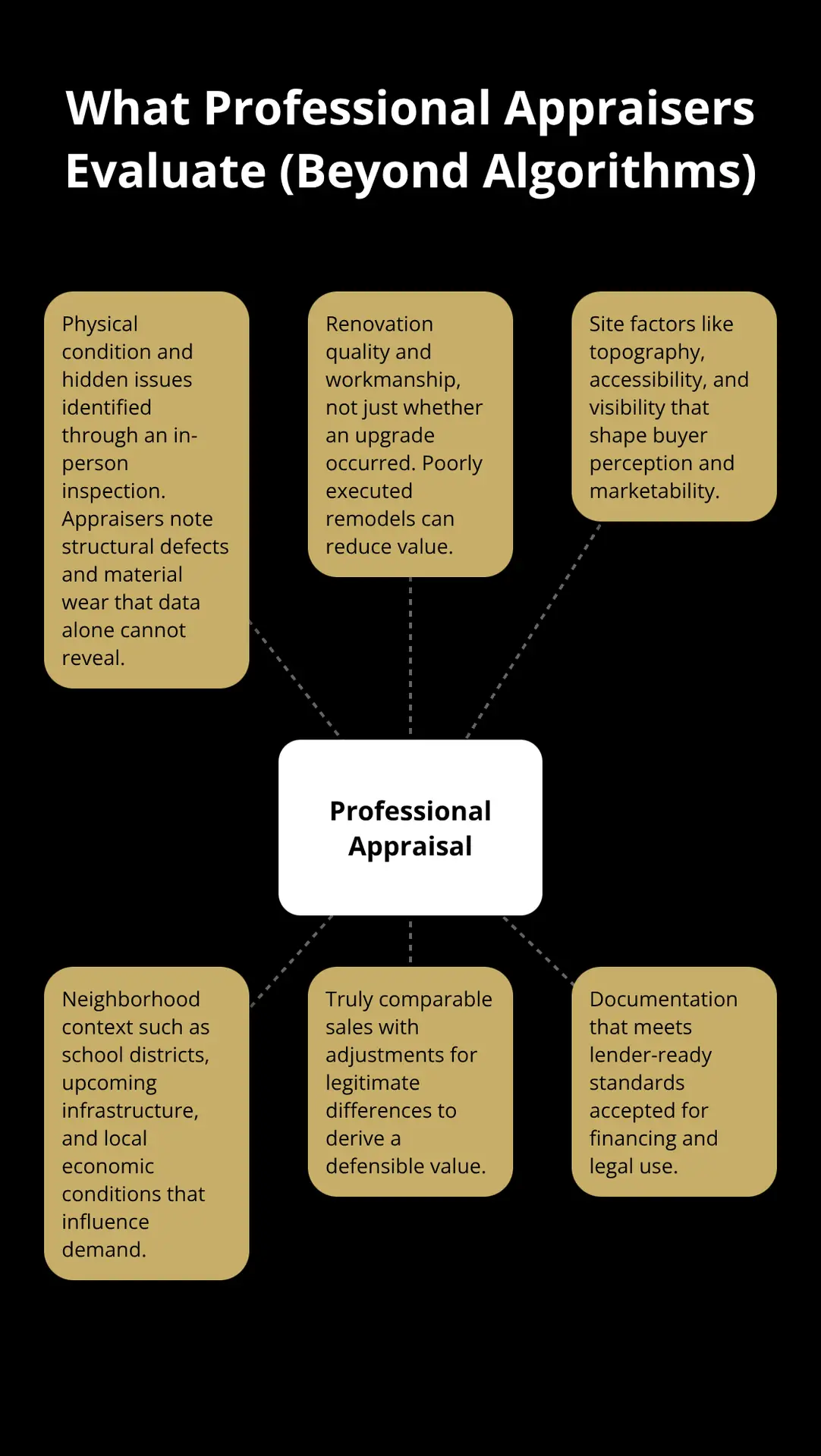

They understand local market dynamics, zoning regulations, neighborhood trends, and how recent developments affect property values. A qualified appraiser catches details that online tools miss: structural issues, renovation quality, site topography, accessibility, and visibility factors that influence how buyers perceive the property.

These professionals analyze the neighborhood itself, examining school districts, upcoming infrastructure projects, economic conditions, and comparable sales data that paint a complete market picture. Their in-person inspection and analytical depth produce appraisals that banks accept for financing, tax appeals, estate planning, and legal proceedings.

Now that you understand what professional appraisers bring to the table, let’s look at the DIY side of the equation and why so many property owners attempt to value their own homes.

What DIY Valuation Tools Actually Get Wrong

The Accuracy Problem With Online Platforms

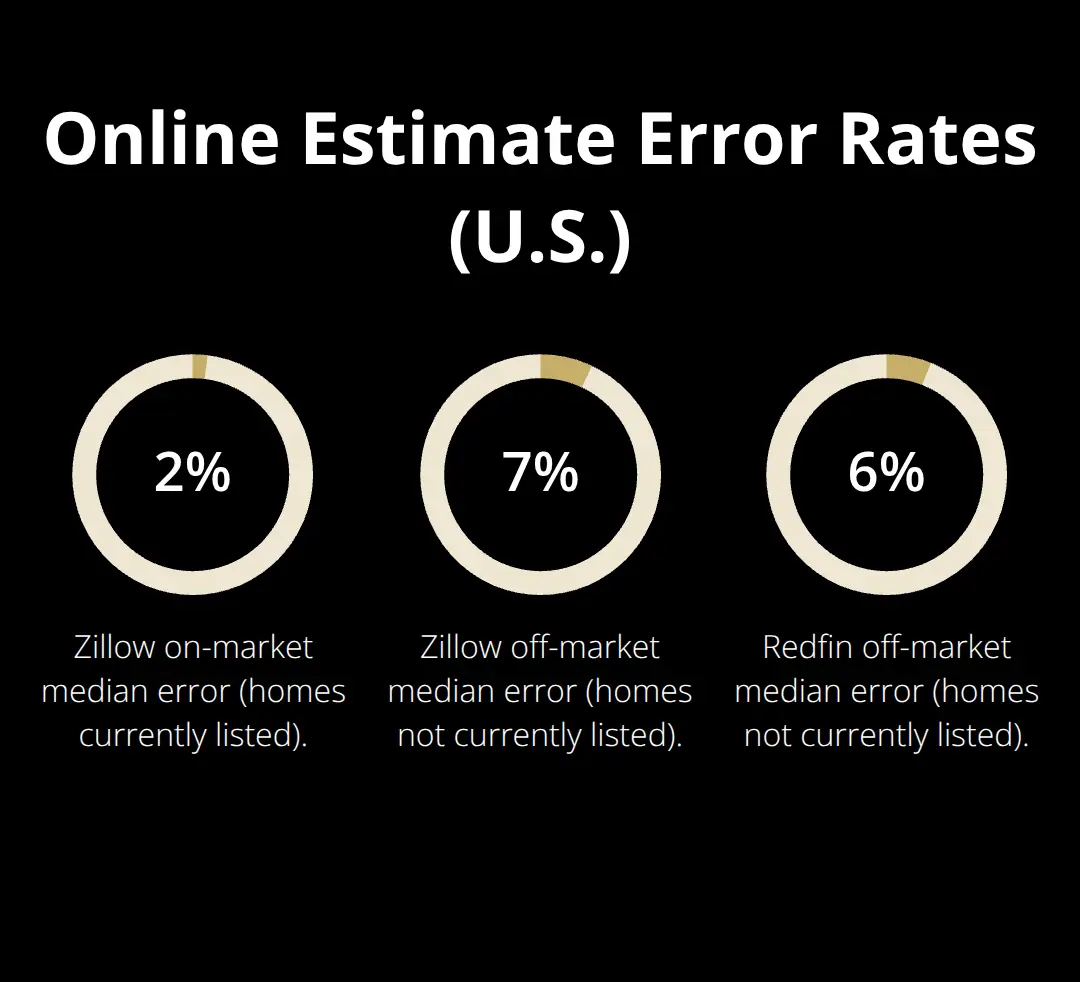

DIY valuation through platforms like Zillow, Redfin, and Realtor.com feels convenient, but the numbers tell a different story. Zillow reports a median error of 1.83% for homes currently on the market and 7.01% for off-market properties, according to their own disclosures. Redfin performs slightly better at 1.71% for on-market homes but still hits 6.31% for off-market properties.

On a $500,000 home, a 7% error translates to a $35,000 swing in valuation, which can torpedo a sale or cost you serious money on a refinance.

Why Algorithms Miss What Appraisers See

These automated estimates rely on public records, recent sales data, and algorithms that simply cannot see what an appraiser sees during an in-person inspection. They miss structural problems, renovation quality, and hidden damage, and they struggle with unique architectural features or irregular lots that don’t fit standard comp patterns. Neighborhood boundary confusion is another common pitfall where the algorithm compares your property against homes in a different market entirely, skewing results wildly. Online tools also cannot account for how well a renovation was executed, only that it happened. A poorly installed kitchen remodel might actually hurt value, but the algorithm counts it as an upgrade. These platforms work fine for casual curiosity or tracking trends, but they fail when real money is on the line.

The Self-Assessment Trap

Self-assessment methods fare even worse because they layer personal bias onto incomplete data. Homeowners overvalued their properties by only 1.94% on average, according to research, though individual cases vary widely. You notice the updated HVAC but forget that the roof is aging, or you remember the new flooring but overlook foundation concerns a professional would flag immediately. Without access to comprehensive comparable sales databases or the training to adjust for legitimate differences between properties, your estimates become guesses dressed up as analysis.

Real Costs of Getting Valuation Wrong

The cost of getting this wrong extends beyond a single transaction. Overpricing during a sale extends time on market, triggers multiple price reductions that signal weakness to buyers, and often results in selling below what an accurate appraisal would have suggested. Underpricing leaves money directly on the table. For refinancing, an inaccurate DIY valuation might lead you to pursue a cash-out refi that a lender won’t approve because the actual value doesn’t support it, or you miss the opportunity to refinance at better terms because you underestimated equity. Banks won’t lend against a valuation anyway; they require an appraisal from a licensed professional hired through a third party. So pursuing DIY methods for financing decisions wastes time and delays your transaction while you eventually end up paying for an appraisal anyway.

Understanding these limitations sets the stage for comparing what professional appraisals actually deliver against what DIY tools promise.

Professional Appraisal vs DIY Valuation: What You’ll Actually Spend

The Real Cost of Each Approach

A professional appraisal costs $357 on average according to Angi’s 2025 data, with typical prices ranging from $314 to $423 depending on property complexity and location. That’s the upfront fee you’ll pay. A DIY valuation through Zillow or Redfin costs nothing initially, which attracts many property owners. However, the real math tells a different story: that $357 appraisal fee becomes insignificant compared to what happens when you price your property wrong. Overpricing by just 5% on a $400,000 home costs you $20,000 in lost equity before you factor in extended time on market, multiple price reductions that signal distress to buyers, and eventual sale below fair value. Underpricing leaves money directly on the table.

For refinancing, an inaccurate DIY estimate might push you toward a cash-out refi that a lender ultimately rejects because the actual appraised value won’t support it. You then restart the process and pay for the appraisal anyway. Banks will not lend based on your own valuation or an online estimate; they require a licensed appraiser hired through a third-party management company. Choosing DIY methods for any financing decision simply delays the inevitable while costing you time and frustration.

Why Accuracy Gaps Matter in Real Dollars

The accuracy gap between these approaches is substantial. Redfin reports 6.45% accuracy for off-market homes. On a $500,000 property, that error represents approximately $32,000 in valuation swing. Professional appraisals operate within a much tighter range because appraisers conduct physical inspections, analyze neighborhood-specific factors like zoning changes and school district boundaries, and compare genuinely comparable properties after adjusting for legitimate differences. They document renovation quality, catch hidden structural issues, and account for how site topography and visibility affect buyer perception. An appraiser spots that the kitchen remodel was poorly executed and adjusts value downward accordingly; an algorithm cannot.

Legal Weight and Regulatory Requirements

For transactions involving lenders, insurance, tax appeals, or estate planning, only a professional appraisal carries legal weight. Courts won’t accept an online estimate as evidence. Lenders won’t fund based on it. Tax assessors won’t consider it for appeals.

Appraisals must follow USPAP standards set by the Appraisal Foundation, meaning they meet strict ethical and performance requirements that protect you legally. DIY methods have no regulatory framework, no accountability, and no recourse if the valuation proves wildly inaccurate. A licensed appraiser carries errors-and-omissions insurance and faces professional consequences for negligence. An online calculator carries neither.

Timeline Considerations for Your Decision

A professional appraisal typically takes two to four weeks from order to completion, though the appraiser’s actual work spans several days. That timeline works fine for most purchase transactions and refinances because lenders require it anyway. DIY valuation takes minutes online, which appeals to impatient sellers, but that speed means nothing if the number is wrong by tens of thousands of dollars. For serious financial decisions, the weeks required for a professional appraisal represent time well spent. This distinction matters enormously when you’re making decisions that affect hundreds of thousands of dollars.

Final Thoughts

Professional appraisals matter when lenders, courts, or tax assessors will review your valuation. If you’re buying with a mortgage, refinancing, appealing property taxes, handling estate planning, or securing any loan backed by real estate, you need a professional appraisal-lenders won’t fund without one, and courts won’t accept anything else. The $357 average cost becomes trivial compared to the financial consequences of mispricing by tens of thousands of dollars, and if you’re selling, a professional appraisal removes guesswork and positions you for faster sales at fair value.

DIY valuation tools work only for casual market tracking, preliminary research, or understanding general neighborhood trends. Online estimates cost nothing and take minutes, making them useful starting points when you’re simply curious about your home’s ballpark value and no transaction hangs in the balance. However, the moment you make decisions that affect your finances-whether for a property or a business appraisal-DIY methods fail because 6-7% error rates on off-market properties translate to five-figure mistakes on typical homes.

Skip the DIY trap and invest in professional assessment whenever real money is on the line. The weeks required for a professional appraisal represent time well spent, and the accuracy plus legal protection you gain far outweigh the cost.