Working capital adjustments can shift your business sale price by hundreds of thousands of dollars. Most sellers don’t realize how these calculations work until it’s too late.

We at Unbroker see deals fall apart because owners misunderstand working capital terms. The difference between a smooth closing and a pricing dispute often comes down to proper preparation.

What Are Working Capital Adjustments

Definition and Components of Working Capital

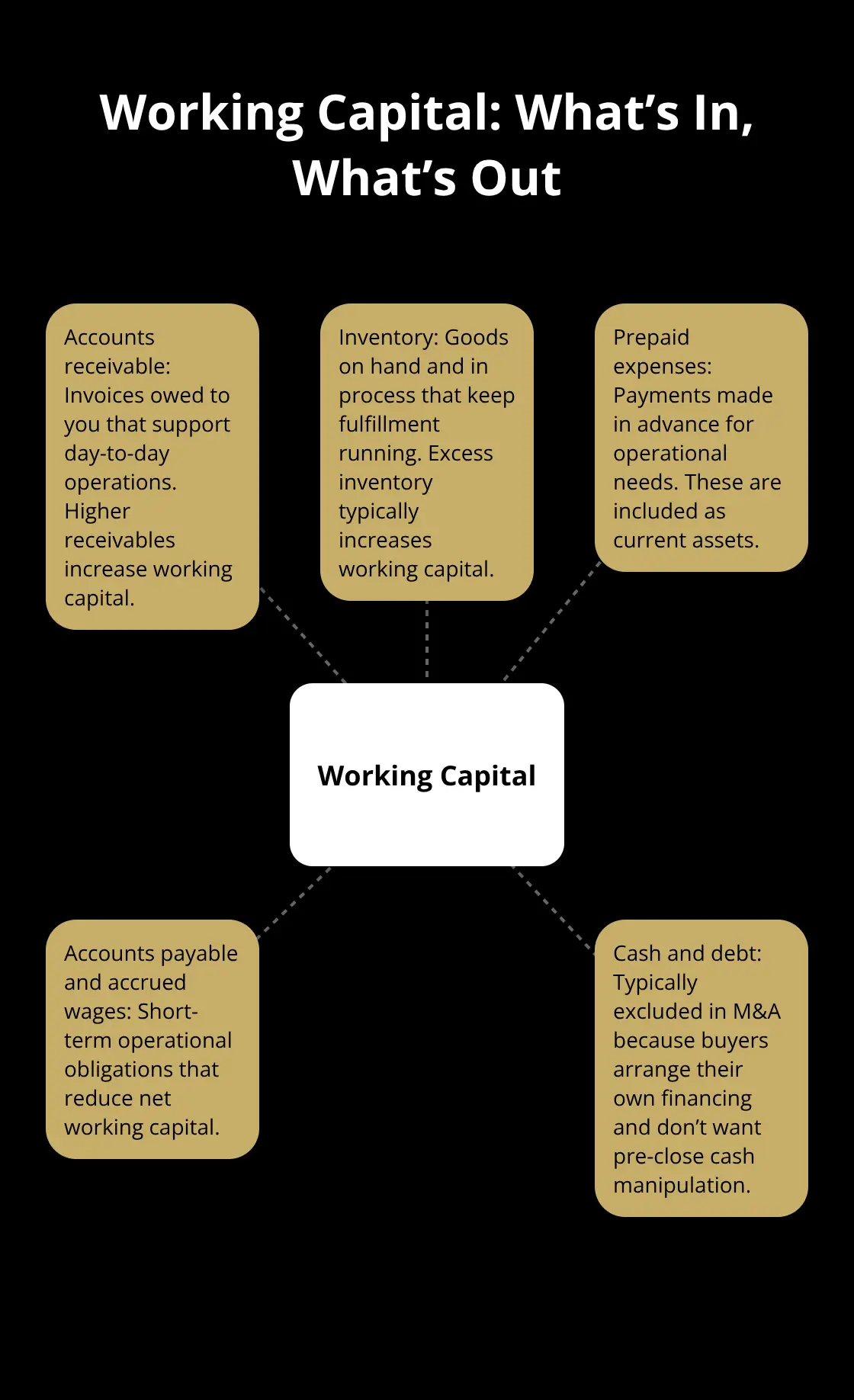

Working capital represents your business’s operational assets minus operational liabilities. The key components include accounts receivable, inventory, and prepaid expenses as assets, while accounts payable, accrued wages, and other short-term operational debts count as liabilities. Cash and debt get excluded from these calculations in most M&A transactions because buyers establish their own financing arrangements. This exclusion prevents sellers from manipulating cash balances right before closing to artificially inflate the business value.

How Working Capital Differs from Cash Flow

Working capital differs fundamentally from cash flow because it measures balance sheet positions at a specific moment rather than cash movement over time. Your business might show strong monthly cash flow while it carries inadequate working capital levels for smooth operations. Private equity firms report that transaction disputes frequently stem from working capital misunderstandings, with sellers who confuse cash generation ability with the operational capital needed to run the business day-to-day.

Why Working Capital Matters in Business Sales

Working capital adjustments directly impact your sale proceeds through dollar-for-dollar price modifications. When your actual working capital at closing falls below the agreed target, buyers reduce the purchase price by that exact shortfall amount. Conversely, excess working capital above the target increases your final proceeds. M&A advisors track working capital changes throughout the sale process because a $100,000 working capital shortfall means $100,000 less in your pocket at closing (regardless of your business’s profitability or growth potential).

The Working Capital Peg Mechanism

The working capital peg establishes the baseline amount that must transfer to the buyer at closing. Buyers and sellers typically calculate this peg based on the company’s average working capital over 12 to 18 months prior to the sale. This historical approach accounts for seasonal fluctuations and operational variations that might skew a single month’s snapshot. The peg serves as the reference point for all adjustments and determines whether you receive more or less than the base purchase price.

Understanding these fundamentals sets the stage for examining how these adjustments actually work in practice and their real-world impact on transaction outcomes.

How Working Capital Adjustments Work in Practice

The Working Capital Peg Calculation Method

The working capital peg calculation demands analysis of six to 12 months of historical financial data to establish your baseline. Most buyers calculate the average monthly working capital during this period, then adjust for seasonal patterns and one-time events. A manufacturing company with $2.4 million in average working capital over 18 months would typically set their peg at this level. However, seasonal businesses need deeper analysis-a landscaping company might show $800,000 working capital in winter but $1.8 million during peak season. Smart sellers present normalized calculations that account for these variations rather than allow buyers to cherry-pick favorable periods.

Common Working Capital Items That Get Adjusted

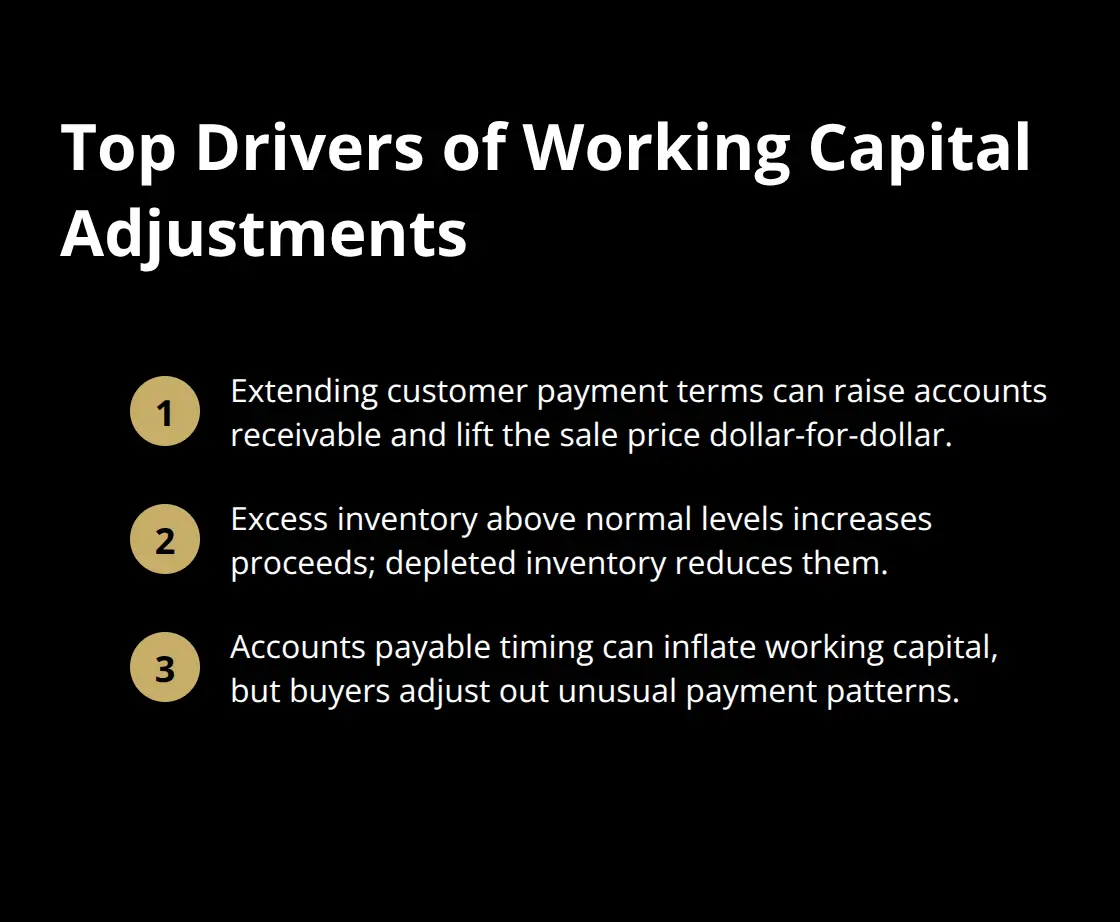

Accounts receivable changes create the biggest working capital swings in most transactions. When a $5 million revenue company extends payment terms from 30 to 45 days before closing, their receivables increase by roughly $625,000, which boosts the final sale price by the same amount. Inventory adjustments work similarly-excess stock above normal levels increases your proceeds, while depleted inventory reduces them.

Accounts payable timing also matters significantly. Delayed supplier payments artificially inflate working capital, but sophisticated buyers will adjust for unusual payment patterns during due diligence.

Real Examples of Working Capital Impact on Sale Price

A $15 million software company sale demonstrates how these adjustments affect actual proceeds. The agreed working capital target was $2.2 million based on historical averages. At closing, actual working capital measured $1.9 million due to accelerated customer collections and reduced inventory levels. This $300,000 shortfall directly reduced the seller’s proceeds from $15 million to $14.7 million. Conversely, a $8 million manufacturing deal saw working capital exceed the $1.5 million target by $400,000 due to seasonal inventory buildup (which increased final proceeds to $8.4 million). These dollar-for-dollar adjustments make working capital management in the months before closing financially material for sellers.

The mechanics of these calculations reveal why sellers must understand not just the numbers, but also the negotiation strategies that protect their interests when buyers propose working capital terms. A comprehensive business valuation report should detail these working capital methodologies to ensure transparency throughout the transaction process.

Negotiating Working Capital Terms

Set Your Baseline with Historical Data

Sellers must establish working capital targets with 12 to 24 months of clean financial data before buyers propose their calculations. Investment bankers recommend that you remove one-time events and seasonal anomalies from this analysis to prevent buyers from cherry-picking outlier months as benchmarks. A distribution company with $3.2 million average working capital should exclude months that major customer losses or unusual inventory purchases affected. Present your normalized calculation first with clear documentation of all adjustments made. This proactive approach stops buyers from selecting low working capital months that favor their position.

Define Calculation Methods Before You Sign

Specify exactly which balance sheet items count toward working capital before you sign letters of intent. Buyers often exclude favorable items like customer deposits or include unfavorable ones like accrued bonuses after initial negotiations conclude. A $12 million technology company lost $180,000 at closing when buyers reclassified deferred revenue as a working capital liability instead of excluding it entirely. Write calculation methodologies into your agreement and require mutual consent for any changes. Demand that buyers apply the same accounting treatment for working capital items throughout the entire historical calculation period.

Avoid These Costly Seller Mistakes

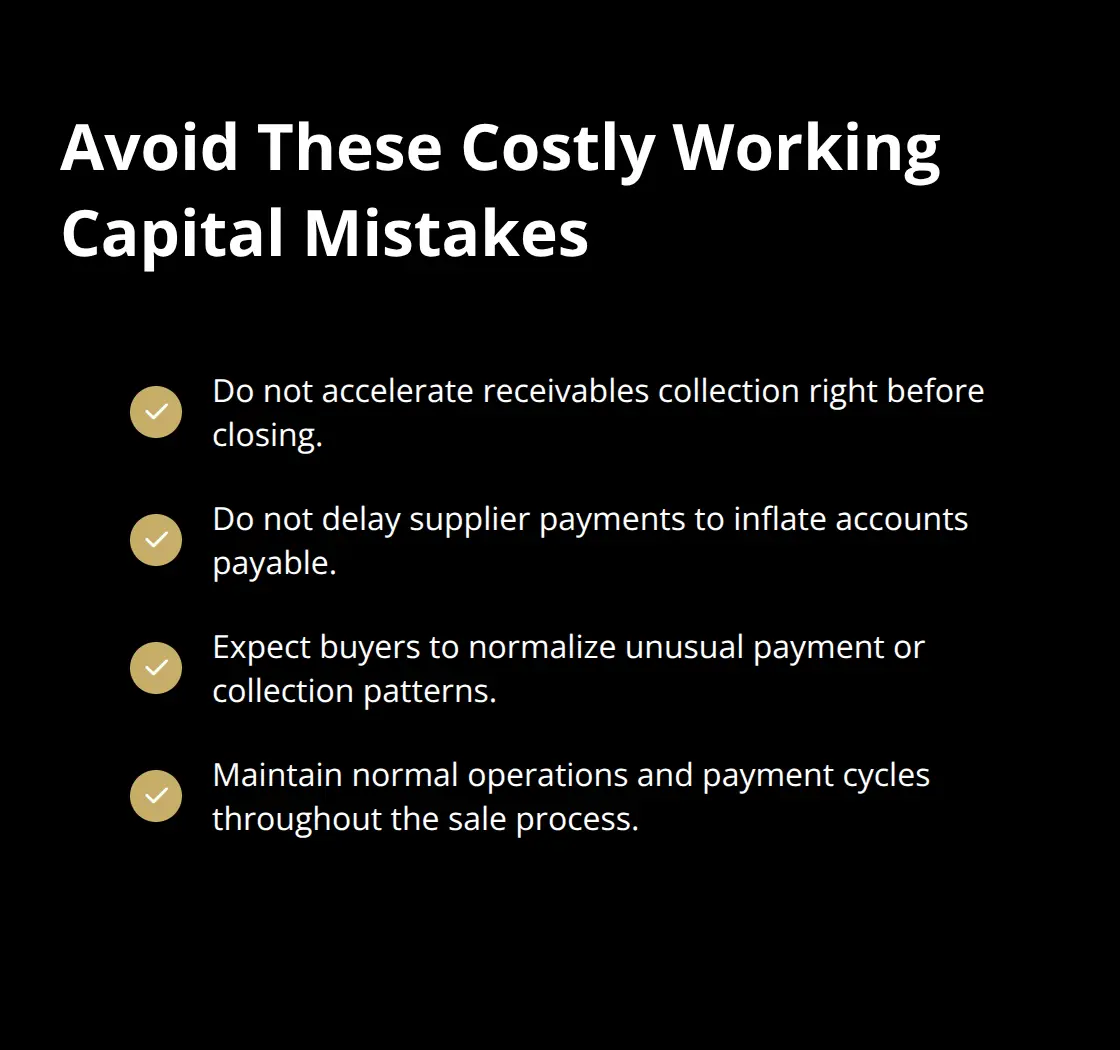

The biggest mistake involves aggressive receivables collection right before closing to boost cash flow. This action reduces accounts receivable and lowers working capital below target levels, which directly reduces sale proceeds. A $8 million manufacturing company collected $400,000 in receivables two weeks before closing, which decreased their final proceeds by the same amount. Similarly, delayed supplier payments to inflate accounts payable backfire when buyers adjust for unusual payment patterns during final due diligence (sophisticated buyers identify these tactics quickly). Smart sellers maintain normal business operations and payment cycles throughout the sale process rather than attempt working capital manipulation.

Protect Yourself from Buyer Tactics

Buyers may propose working capital targets based on the lowest historical months or exclude items that benefit sellers. Challenge any calculation that deviates from standard industry practices or your company’s normal operations. Request detailed explanations for all proposed adjustments and compare them against your historical data. Some buyers attempt to include non-operational items like legal reserves or warranty accruals in working capital calculations. Push back on these inclusions and insist on operational items only. Mastering effective negotiation tactics becomes crucial when buyers pressure you to accept unfavorable terms, and understanding what terms should never appear in your sale agreement helps you identify problematic clauses before they become binding.

Final Thoughts

Working capital adjustments represent one of the most significant yet misunderstood factors that affect your final sale price. These dollar-for-dollar adjustments can shift your proceeds by hundreds of thousands of dollars. Proper preparation becomes essential for maximizing your exit value.

Start your preparation at least 18 months before your planned sale date. Gather clean financial data and calculate normalized working capital baselines during this period. Remove seasonal fluctuations and one-time events from your analysis to present the strongest possible position when negotiations begin (sophisticated buyers will scrutinize every detail).

We at Unbroker help sellers understand working capital implications through our transparent business sale platform. Our team combines expert support with modern technology to maximize your sale proceeds. Working capital adjustments will impact your deal whether you understand them or not, so take control through early preparation and smart negotiation terms.