Selling a business is one of the biggest financial decisions you’ll make. The difference between a smooth transaction and a painful one often comes down to one thing: whether you’ve qualified your buyer properly.

At Unbroker, we’ve seen deals fall apart weeks into negotiations because sellers didn’t vet their prospects upfront. A solid buyer qualification process catches problems early, saves you months of wasted time, and protects your bottom line.

What Makes a Buyer Unqualified

The moment you meet a potential buyer, you need to assess whether they can actually close. Too many sellers spend weeks negotiating with buyers who were never serious contenders.

Funding Red Flags

The first red flag appears in how a buyer talks about funding. If someone claims they’re getting a loan but can’t name their lender, hasn’t spoken to a bank, or keeps changing their financing story, that’s a sign they haven’t done their homework. Real buyers have pre-approval letters or clear documentation of available capital.

Ask directly: Where is the money coming from? Have you been pre-approved? A qualified buyer answers these questions without hesitation. If you receive vague responses or they keep pushing the conversation toward price without addressing funding, move on. Unqualified buyers waste your time and create false momentum that leads nowhere.

Spotting Lack of Genuine Commitment

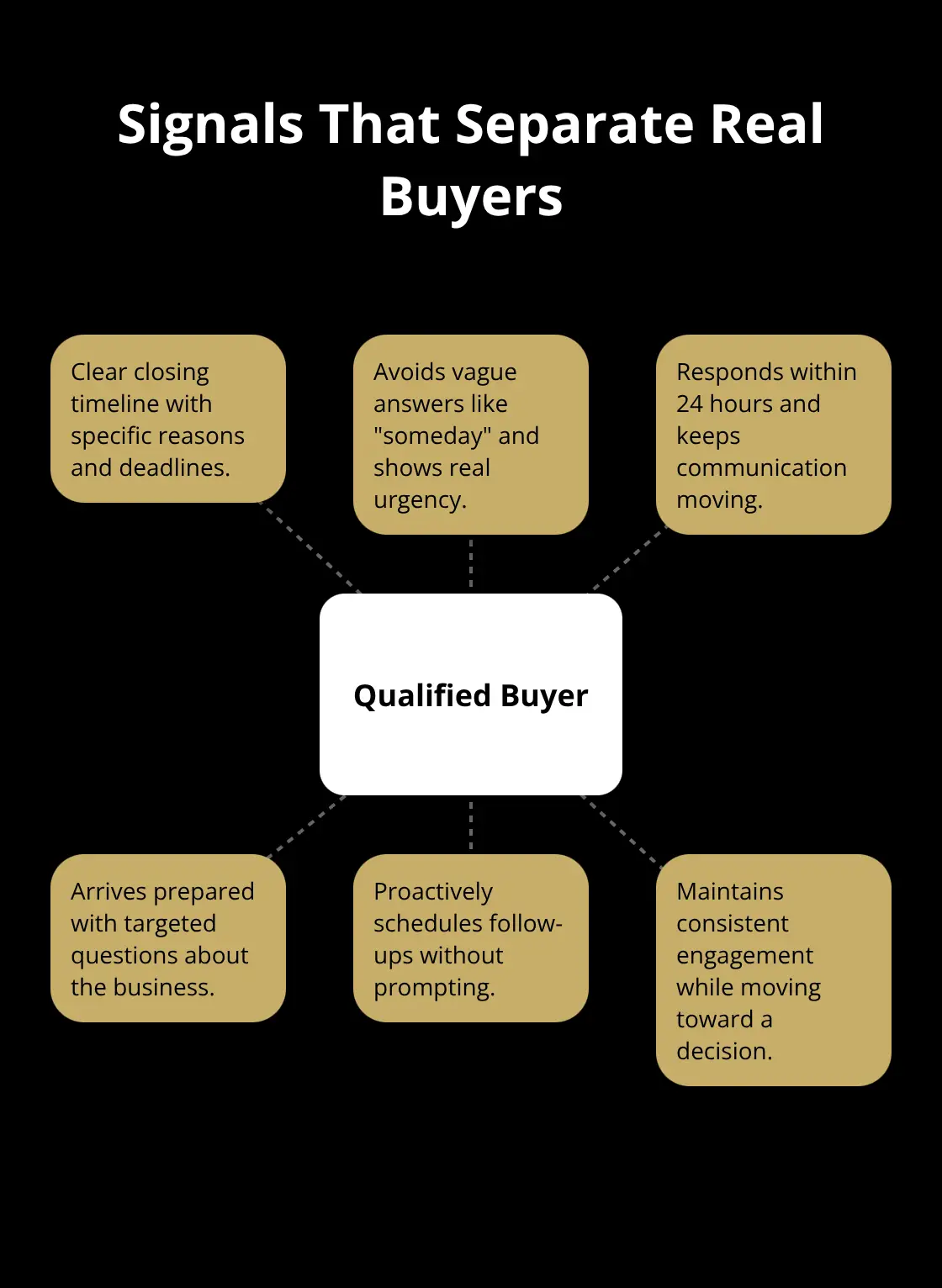

Interest and commitment are not the same thing. A buyer might express enthusiasm in your first call but disappear for weeks or avoid scheduling follow-ups. Genuine buyers create momentum-they respond to emails within 24 hours, show up prepared to meetings, and ask specific questions about operations, financials, and transition plans.

If a buyer postpones due diligence, refuses to sign an NDA, or avoids discussing their timeline for closing, they’re either not serious or shopping around without commitment. Set clear expectations early: you need a signed NDA before sharing detailed financial information, and you need a timeline commitment before moving into deeper negotiations. Buyers who balk at these basic requirements aren’t worth your energy. Real buyers understand that business sales require trust and structure.

When Expectations Don’t Match Reality

Unrealistic expectations kill deals. Some buyers lowball offers by 30% or 40% below market value and expect you to negotiate downward. Others demand closing in 30 days when a proper business sale takes time for due diligence, financing, and legal work.

Ask about their price expectations early and listen carefully to their reasoning. If their offer sits significantly below industry standards for your business type and size, ask them how they arrived at that number. A qualified buyer has done research and understands market rates. They also understand that complex transactions take time. If someone pressures you to rush the process or presents an offer so low it signals they don’t understand your business, you haven’t found the right buyer.

Set your minimum acceptable offer and timeline upfront, then stick to it. Deals that feel forced from the start rarely close smoothly. The buyers worth your time demonstrate financial readiness, genuine commitment, and realistic expectations-and that’s exactly what you’ll learn to spot in the next section.

What Qualified Buyers Actually Look Like

A qualified buyer moves with purpose. They’ve already verified their financing, understand the market, and can articulate why they want your business. The shift from unqualified to qualified buyers is stark: one group stalls and negotiates endlessly, while the other closes deals.

Financial Capacity Speaks Louder Than Promises

Financial capacity matters most. A buyer with a pre-approval letter from a lender has cleared a real hurdle-they’ve submitted documentation, passed underwriting, and have confirmed access to capital. When a buyer tells you they’re pre-approved, ask to see the letter. It should specify the loan amount, the property or business type it covers, and the expiration date. If they hesitate or claim their lender prefers confidentiality, that’s a warning. Legitimate lenders issue pre-approval letters as a standard practice.

Beyond bank financing, some buyers bring cash or have lines of credit ready. The key question isn’t how they’re funding the deal-it’s whether they’ve already taken steps to secure that funding. A qualified buyer has done this work before scheduling serious conversations with you.

Timeline and Momentum Separate Real Buyers from Tire-Kickers

Genuine buyers operate on a clear timeline. They know when they need to close and why. Maybe they’re launching a new business by Q2, or they’ve just received a bonus and want to deploy it within six months. This clarity matters because it aligns expectations and creates natural deadlines that keep deals moving.

When you ask a qualified buyer when they want to close, they give a specific answer with reasoning. Unqualified buyers say things like “someday” or “whenever” or “it depends,” which translates to no real urgency. Momentum shows up in responsiveness. Qualified buyers return calls within 24 hours, arrive to meetings prepared with questions, and schedule follow-ups without prompting.

They treat the purchase seriously because it represents a major commitment. If a prospect goes silent for two weeks, resurfaces with a question about pricing, then disappears again, they’re not ready to buy. Real buyers maintain consistent engagement because they’re actively moving toward a decision.

Values and Culture Alignment Determines Long-Term Success

A buyer who’s financially ready but philosophically misaligned with your business creates problems. Some buyers want to strip assets and flip the operation. Others plan to cut staff or change the company’s mission entirely. If those outcomes trouble you, a qualified buyer is one whose vision for the business aligns with yours.

Ask directly about their plans: What will they keep? What will they change? How do they treat employees? A qualified buyer answers these questions with specificity, not vague platitudes. They’ve thought about operations, culture, and transition. If their answers conflict sharply with your values, the deal may close but you’ll carry regret. The best deals happen when buyer and seller share fundamental assumptions about what the business should become.

How to Verify What Buyers Tell You

Don’t take a buyer’s word at face value. Qualified buyers expect you to verify their claims. Request documentation of pre-approval, ask for references from previous purchases they’ve made, and check their background through public records. A buyer who resists verification or becomes defensive about your questions is signaling that something doesn’t add up.

You can also ask them to walk you through their due diligence process. How will they evaluate your financials? What advisors (accountants, lawyers, consultants) will they involve? Their answers reveal whether they’ve purchased a business before or are winging it. Experienced buyers have a process. First-time buyers may not, but they should still demonstrate willingness to do the work properly. The buyers worth your time welcome scrutiny because they have nothing to hide.

How to Screen Buyers Before Wasting Your Time

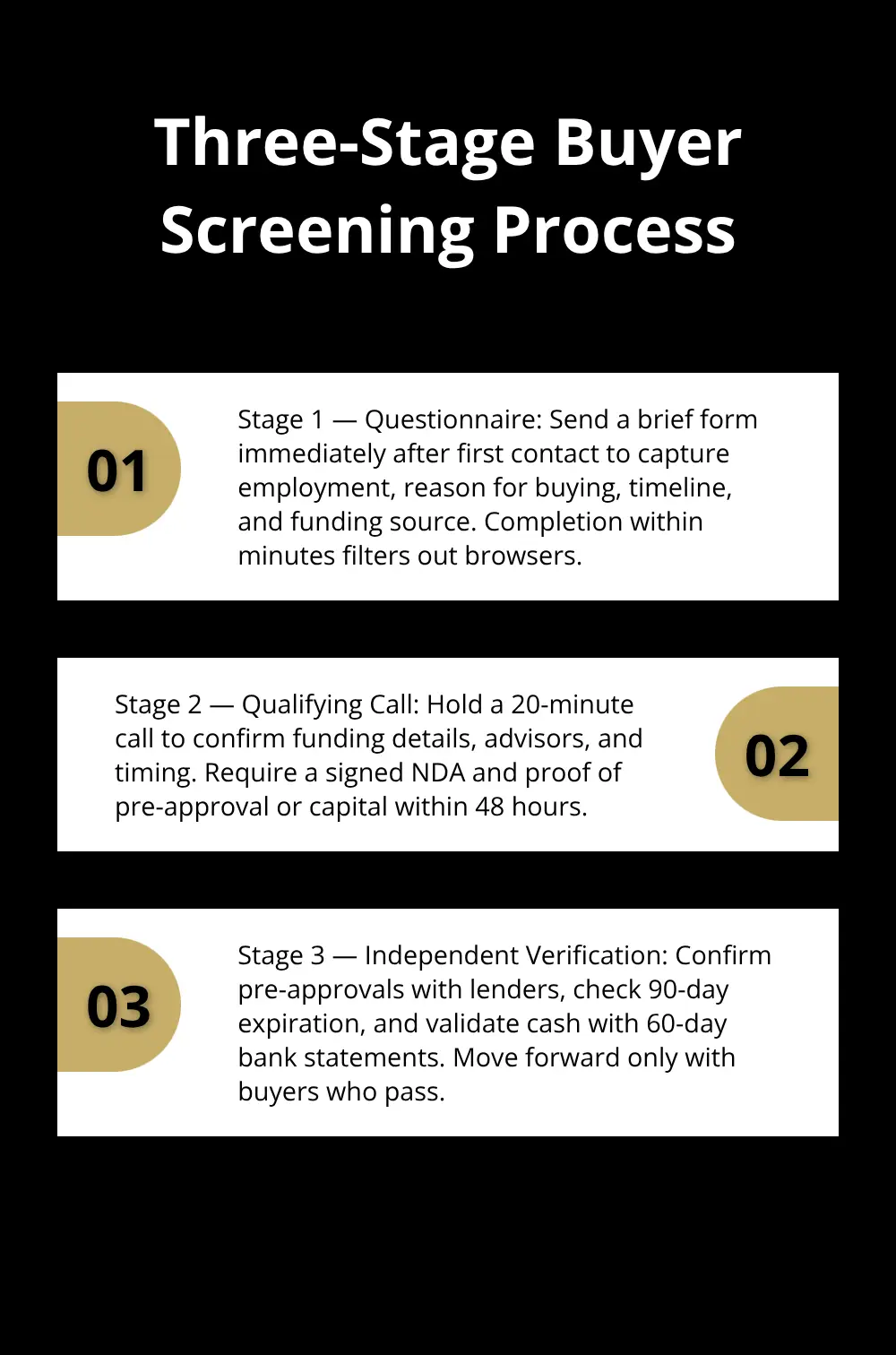

The most efficient sellers use a three-stage screening process that eliminates unqualified buyers within days, not weeks. Start with a brief questionnaire sent immediately after initial contact. Ask for basic information: current employment, reason for buying, target timeline, and funding source.

This takes ten minutes to complete and separates serious prospects from browsers. Buyers who ghost on a simple form weren’t going to close anyway. Those who respond promptly move to stage two.

Stage Two: The Qualifying Phone Call

Schedule a 20-minute phone call where you dig into their answers. Ask them to walk you through how they’ll fund the purchase, what advisors they’ve already consulted, and why they’re buying now rather than next year. Listen for specificity. A buyer who says they’re getting a bank loan but hasn’t actually contacted a lender yet is still in fantasy mode. A buyer who names their banker, describes the pre-approval process they’ve started, and explains their timeline with concrete reasoning is moving forward.

During this call, request that they sign an NDA and provide documentation of pre-approval or proof of available capital within 48 hours. This is your filter. Many prospects will disappear here, which is exactly what should happen. The ones who comply and submit documents have demonstrated real commitment and financial readiness in a single week.

Stage Three: Verify Financial Claims Independently

Once you have pre-approval letters or bank statements showing available funds, verify the details independently. Call the lender to confirm the pre-approval is legitimate and matches what the buyer told you. Check the expiration date on the letter, which typically runs 90 days. If it’s expired, they need a new one.

For cash buyers, request bank statements from the past 60 days showing the funds are actually there and haven’t been borrowed. Some sellers hesitate to ask for this level of verification, fearing it will offend the buyer. The opposite is true. Qualified buyers expect rigorous verification and understand it protects both parties. Unqualified buyers resist because they know they can’t pass the test.

Speed Determines Your Success Rate

Speed matters here. The longer you take to verify, the more time you waste if the buyer doesn’t qualify. Complete financial verification within a reasonable timeframe of initial contact. If a buyer can’t or won’t provide documentation within that window, they’re not ready, and you should move to your next prospect (this disciplined approach means you spend your negotiation time only with buyers who can actually close).

Final Thoughts

A rigorous buyer qualification process isn’t bureaucracy-it’s your protection. The sellers who move fastest are the ones who qualify buyers first, not last. Filtering out unqualified prospects in the first week eliminates months of wasted negotiation with people who can’t actually close.

If you spend eight weeks negotiating with an unqualified buyer before discovering they lack funding or commitment, you’ve lost two months you could have spent with a real buyer. Qualified buyers move faster because they’ve already done their homework. They have pre-approval letters, clear timelines, and realistic expectations.

Use the three-stage screening process outlined here: send that questionnaire today, schedule qualifying calls this week, and request documentation immediately. Move fast with qualified buyers and walk away from those who don’t meet your standards. If you’re selling a business and want expert guidance through this process, Unbroker offers transparent support with tools and assistance designed to help you close with confidence.